Here's my Top 10 items from around the Internet over the last week or so. As always, we welcome your additions in the comments below or via email to bernard.hickey@interest.co.nz.

See all previous Top 10s here.

My must read is #5 from Andy Haldane on the nature of wages, work and jobs in the age of the machine.

1. Remember the taper tantrum? - The world's financial markets are in a delicate state and are about to be tested in a way they haven't been before.

The US Federal Reserve looks set to increase interest rates from almost zero for the first time in almost a decade in about a month's time.

There are large chunks of the world's financial markets that have never had to adjust or think about such a thing, particularly in emerging markets, that have loaded up on huge dollops of easy US dollar denominated debt.

Now they're about to find out if they can cope with higher interest rates and a higher US dollar at the same time as their economies are slowing.

What could possibly go wrong?

We had a sneak preview of this in mid-2013 when the Fed's decision to wind down its Quantitative Easing programme unleashed severe volatility.

There are some early warning signs from the bowels of the world's debt markets that it might not go smoothly.

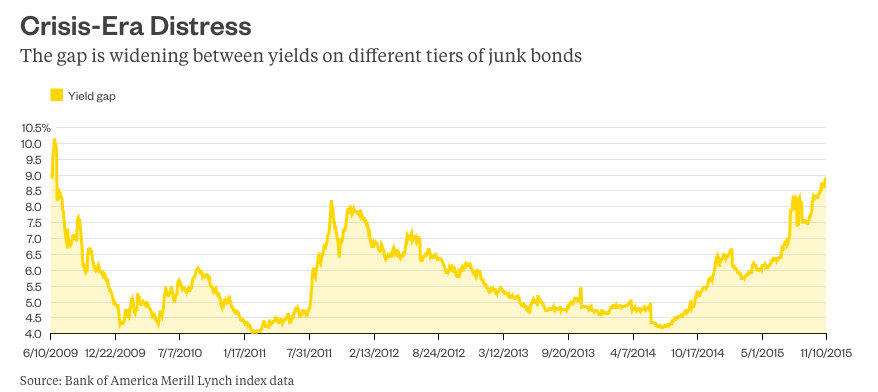

Bloomberg reports the premium charged for the riskiest type of corporate bonds relative to safer bonds has widened to its highest since the dark days of 2009. The chart below tells the story. Also The Telegraph reports on the risks of liquidity in bond markets drying up for all sorts of reasons, including that central banks and regulators have bought large amounts of bonds and then virtually banned banks from holding and trading them.

Investors from retirees to pension and insurance companies are more tied to the fate of U.S. corporations than ever after buying trillions of dollars of their debt over the past seven years.

Companies are about to face their biggest test in years, when the Fed raises interest rates from about zero, where they’ve been since 2008. The low-rate policies were intended to help these corporations borrow enough to hire more employees, pay higher salaries, allow consumers to buy more stuff and create a virtuous cycle. Perhaps that happened to some extent.

But plenty of companies simply got fat with debt without improving their revenues. Now they are paying the price, and the economy may have to foot part of the bill.

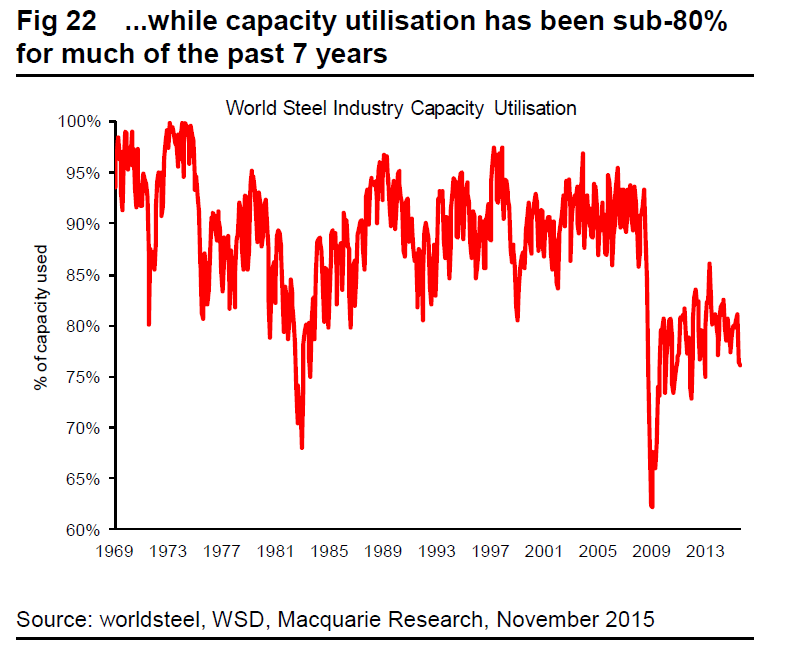

2. The price of steel - This is worth watching to see how China's smoke-stack industries are faring and to see what Australia will soon experience, given it produces the iron ore and coal used to power China's steel mills.

It's not good.

Bloomberg reports steel futures prices have dropped 40% over the last year. The story is as much about supply as demand. Iron ore prices also plunged again overnight.

Forecasts for a boom in Chinese consumption helped spur a rise in production that left the segment with a massive glut. The successful realization of economic rebalancing in China, meanwhile, necessarily entails a material slowdown in that nation's demand for steel.

Macquarie observes that global steel consumption has contracted on an annual basis throughout 2015.

"With 1.6 billion tonnes of consumption globally, steel remains the lynchpin of industrial growth," wrote Hamilton. "However, the growth part of this equation is an increasing problem, and not only in China."

India, which has the potential to buoy demand for steel, is also contributing significantly to supply growth. Bloomberg Intelligence's Yi Zhu notes that 37 million metric tons of production capacity in India are currently under construction or in planning to be added.

3. Cheap money and perversity - One fascinating point is made in this article about the steel glut. Cheap money actually makes over-capacity worse. That means that all this money printing that is going on right now is helping to create deflation in the prices of goods made in these sorts of capital-intensive businesses. Talk about perverse.

Arguably, overcapacity across the commodity complex is a perverse side effect of years of near-zero interest rates and asset purchases by the Federal Reserve. Lower input prices, however, can have a silver lining. For example, the collapse in oil prices, in simple terms, represents a transfer of wealth from major oil conglomerates to consumers. The largest positive effects accrue to lower-income households that spend a heftier portion of take-home pay on energy costs.

"A world of cheap money not only sees new capacity built, it also means existing capacity doesn’t disappear," explains Hamilton. "While most regions are well off their peak production levels over the last decade, permanent capacity closures have been few and far between."

The old adage of "the best cure for low prices is low prices" hasn't been able to come to fruition just yet, as low-cost credit has allowed even unprofitable production to be maintained—for now.

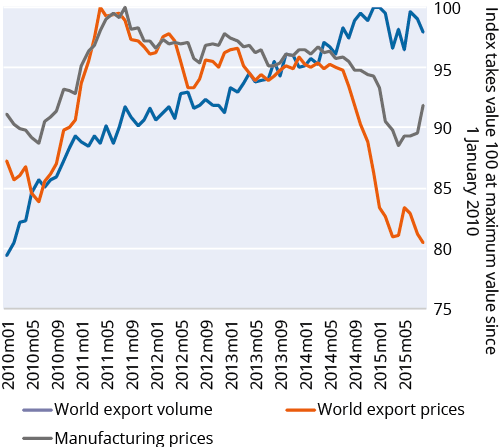

4. What on earth is happening to global trade? - It is one of the mysteries of the last two or three years. How is it that in an increasingly globalised world with still-growing emerging economies that global trade has started falling, both in value and volume terms.

Simon Evenett and Johannes Fritz from the London-based Centre for Economic Policy Research have written a piece over at VoxEU on the strange phenomena. It turns out there's been quite a few trade restrictions introduced over the last year, although falling oil and other commodity prices are a factor.

I also wonder whether the shift from goods consumption to services is a factor.

World trade growth isn’t slowing down – the subject of a growing academic literature (Hoekman 2015); the latest available monthly data suggests that world trade has been contracting during 2015 in both volume and value terms. On average G20 exports have fallen 4.5% since world trade peaked in value in October 2014.

5. 'This time it could be different' - I read and think a lot about how technology is changing the economy, wages and jobs. So a speech on the topic last week by Andy Haldane, the Chief Economist at the Bank of England, was the perfect thing to read.

He has some great insights and a whole lot of fresh research to bring to bear to the debate. Even he isn't sure that the latest wave of productivity-enhancing technology will generate subsequent waves of higher wages and more job creation, as has happened for most of the last 250 years.

Andy notes that arguments about “technological unemployment” – the idea that technological advance puts people out of work and bears down on wages – have been raging for centuries. According to Andy, most evidence shows that over the broad sweep of history technological progress has not damaged jobs but rather boosted wages: “Technology has enriched labour, not immiserated it.”

However, Andy notes that this broad pattern obscures the fact that there has an increasing skills premium has emerged with each passing wave of technological progress. This was especially the case in the late 20th century, as new machines such as computers began replacing not only physical but cognitive labour. He finds that each phase has eventually resulted in a “growing tree of rising skills, wages and productivity”.

But they have also been associated with a “hollowing out of this tree”. Indeed, this hollowing-out of jobs has “widened and deepened with each new technological wave”. This has resulted in a widening income gap between high- and low- skilled workers. Andy states: “By itself, a widening distribution of incomes need not imply any change in labour’s share of national income: in the past, technology’s impact on the labour share appears to have been broadly neutral. But this time could be different.” The question now is therefore whether the latest technological cycle will follow the pattern of its 18th and 19th century predecessors, where productivity gains eventually boost wages for all – or whether the hollowing out of employment, widening distribution of wages and fall in labour’s share of income are permanent.

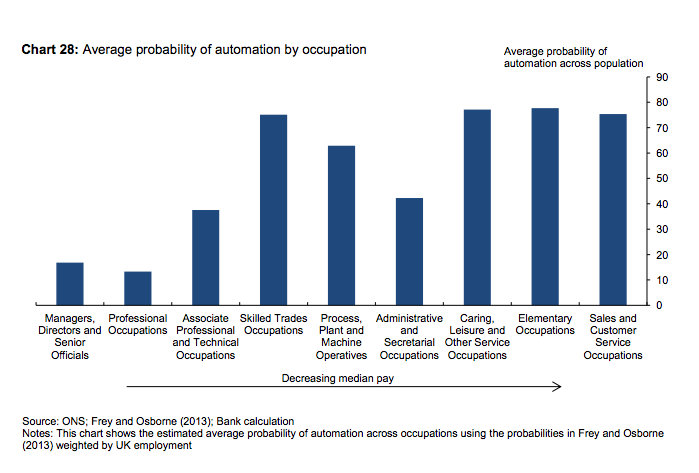

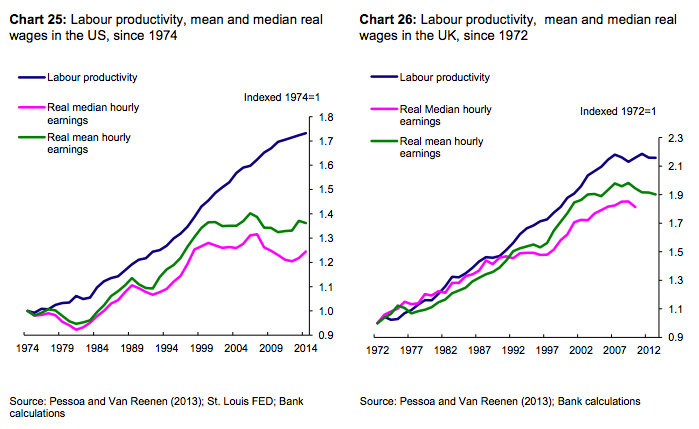

6. The wage share - Haldane spends quite a bit of time looking at whether the rise of the machines will worsen or reverse the fall in the share of income going to wages over the last 30 years or so.

He's not super confident it will get better. The charts below showing how productivity has diverged from wages is just devastating for those who argue all we need to do is improve productivity and the wages will follow...

Machines are becoming ever smarter, Andy notes. The Bank’s own calculations show that, over the course of the next several decades, many millions jobs in the UK could be at risk of automation, with those most at risk tending to be the lowest wage. As machines improve, he states: “the greater the likelihood that the space remaining for uniquely-human skills could shrink further”.

Andy states: “If these visions were to be realised, however futuristic this sounds, the labour market patterns of the past three centuries would shift to warp speed. If the option of skilling-up is no longer available, this increases the risk of large scale un- or under-employment. The wage premium for those occupying skilled positions could explode, further widening wage differentials. And labour’s share of the pie could fall even more dramatically than in the past. On this view, the tree would be so thoroughly hollowed-out that it may no longer be able to support itself.”

If technological progress reduces the bargaining power of labour relative to capital, Andy notes that “it would manifest itself in weaker than expected wage growth and a secular fall in the labour share of income over time, both of which we have seen in a number of countries”.

7. So what does it mean for interest rates? - So if there's enormous downward pressure on wages and the wage share of income, what would happen to inflation and interest rates?

Haldane doesn't mince words. They'll stay super low. The implication of course is for everyone to go out there and borrow more to buy property because they can be sure of lower interest rates for longer....

It would be nice to see a speech from the Reserve Bank of New Zealand on this topic and what it might mean for interest rates. Remember that New Zealand's OCR is a full 225 basis points higher than the Bank of England's rate, even though Britain's unemployment rate is 5.4% and New Zealand's is 6.0%...

If technological progress reduces the bargaining power of labour relative to capital, Andy notes that “it would manifest itself in weaker than expected wage growth and a secular fall in the labour share of income over time, both of which we have seen in a number of countries”. The MPC’s current forecast assumes labour’s share of income reverts to its historical average, meaning that wages are expected to outpace productivity over the next few years.

While Andy agrees that this path is plausible, if labour’s bargaining power and share of income prove to be lower than in the past – as has been the case before and after the crisis in a number of countries – there is a different path possible. This would result in weaker wage growth and a “materially lower path for inflation than contained in November’s Inflation Report”, with CPI reaching 1.6% at the two year horizon.

Andy states: “That would put the balance of risks squarely towards a more protracted undershoot of the inflation target, even without any downdraught from external prices and demand.” Andy concludes: “Against that backdrop, my view is that the case for raising interest rates is still some way from being made. Whatever the reason, the economic aircraft appears to be losing speed on the runway. That is an awkward, indeed risky, time to be contemplating take-off.”

8. Robots could displace a third of jobs - The Guardian's Heather Stuart reports on a 300 page BankofAmericaMerrillLynch report on how robots and new technology will transform the workplace in a fourth industrial revoluation. Remember. BOAML is no hotbed of communism. It's an investment bank (that used to employ our Prime Minister),

“We are facing a paradigm shift which will change the way we live and work,” the authors say. “The pace of disruptive technological innovation has gone from linear to parabolic in recent years. Penetration of robots and artificial intelligence has hit every industry sector, and has become an integral part of our daily lives.”

However, this revolution could leave up to 35% of all workers in the UK, and 47% of those in the US, at risk of being displaced by technology over the next 20 years, according to Oxford University research cited in the report, with job losses likely to be concentrated at the bottom of the income scale.

“The trend is worrisome in markets like the US because many of the jobs created in recent years are low-paying, manual or services jobs which are generally considered ‘high risk’ for replacement,” the bank says.

“One major risk off the back of the take-up of robots and artificial intelligence is the potential for increasing labour polarisation, particularly for low-paying jobs such as service occupations, and a hollowing-out of middle income manual labour jobs.”

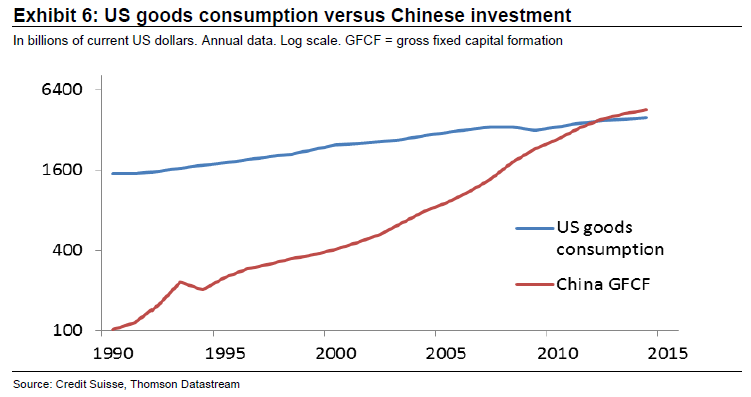

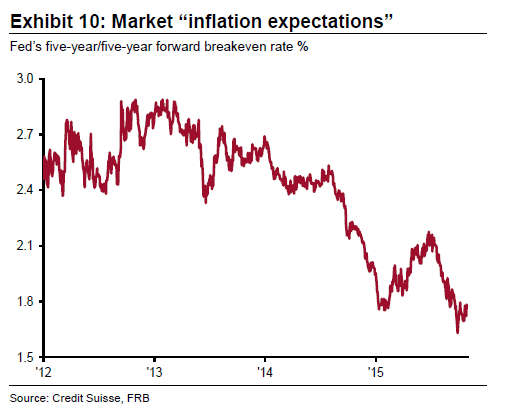

9. The two big risks - Bloomberg reports Credit Suisse has warned in its 2016 Global Outlook that two things could derail the global economy -- a cut in Chinese investment spending and a rise in core inflation in America. The startling charts below tell the story.

And this (bolded) fact stunned me:

Chinese capital spending is bigger than U.S. consumer spending on goods. This does not mean, however, that Chinese investment has supplanted the U.S. consumer as the engine of the global economy. The necessary qualifier here is that in the third quarter, real personal consumption expenditures on services in the U.S. were nearly double that of spending on goods.

32 Comments

#1 - 3 Excuse my ignorance, but why are low prices a problem? If any commodity can be sold cost plus (covering reasonable costs of production, operations etc) but are still low why the fuss? If an organisation cannot sell the products to cover costs plus a MODEST profit, and cannot reduce it's costs then should it be in business? Why must we forever pander to Capitalism?

#5 the "hollowing out" is driven by rapid technological change occurring faster than the majority of a labour force to keep up. A significant problem for Governments will be that while kids are being educated to the latest technology and will be used to rapid change, older workers will not be, but older may only be from 30 something +, so keeping them constructively occupied (preferably employed) to maintain a reasonable standard of living in comparatively "low skilled" occupations. Also the issue is defining skills - what is highly skilled? A computer programmer who can earn $150 k a year or the plumber (on $18 per hour) who fixes his toilet? I know a few computer geeks who wouldn't know how to fix a toilet, or change oil in a car. As an aircraft engineer my skills could have impacted on the safety of hundreds at a time, but there was no way I could get paid the same as a doctor who only deals with one at a time, or a lawyer who delivers bugger all benefit to anyone.

Deflation becomes a problem when it causes people to put off purchases (because they know the price next month will be lower). Decreasing revenues -> companies going out of business -> layoffs -> less money to spend -> decreasing revenues... This was the cycle in the great depression and it is what people are worried about. Decreasing prices because of increased efficiency (like we've seen in the tech industry for years) are not really a problem.

No issue there. My point is that excessive profits have been, and still are being milked from too many areas. Case in point the four major banks (all Australian owned) have declared a $4 billion dollar profit from NZ this year. that is pretty close to $1000 for every man, woman and child in the country. While the Government might rub their hands in glee from the tax revenue, where is that level of profit become reasonable when they offset the majority of their risk to their customers. The banks have been a major player in the causal factors behind house prices, dairy farmers under threat from falling milk solid prices and so on. When it comes to commodities, the manufacturers might well be trying to achieve what I have suggested, a modest profit, but their bank charges and other second tier costs that are limited in their ability to control them are excessive. I remember costing a business to buy a couple of years ago and while I could mortgage my house for about 6% a business loan through my bank started at around 14 - 15%. Indeed the bank charges were what caused the deal to not go ahead. When I discussed Risk with them, to try to understand the cost of the loan, I still had to secure the loan against my personal assets, so they had virtually no risk, while I carried all of it.

I agree that banking regulations are seriously flawed and encourage banks to go into mortgages rather than investing in productive businesses. "Just $1.50 in assets will now support a $100 loan" (http://www.abc.net.au/news/2014-10-02/big-bank-profit-to-be-hit-as-apra…) but for business loans the risk weightings are regulated differently and I think they need about $10 in "real money" to issue (print) a $100 business loan (don't have the numbers handy). So if they are paying out interest on those deposits then obviously a mortgage is much cheaper for them than a business loan, even if they have the same risk of default. Further, the fact that banks are allowed to create money (http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin…) feeds fuel into asset bubbles. There are lots of alternatives to our current system but politicians don't want to touch them becuase most people don't understand the current system and certainly don't realise that "majority of money in the modern economy is created by commercial

banks making loans."

For the big four banks, only 16 per cent, on average, of a real estate mortgage is counted when measuring the bank’s capital ratio. This is rising to 25 per cent next year.

But every dollar of an unsecured personal and business loans counts against capital and in some cases the risk weighting is 150 per cent.

Capital — that is, the bank owners’ money — has to be 8 per cent of assets, although mostly it’s around 10 per cent. That is, the ratio of owners money to other peoples’ money has to be no greater than 12.5 to 1 and is usually 10 to 1. The result is that for every dollar of capital, the big four banks can choose to lend $62.50 secured against real estate or $10 unsecured.

https://www.thincats.com.au/news/

The net result is that the benefits of progress are passed to the managers and owners of financial capital rather than to other sectors of society.

Not quite Roger. The banks shareholders have very little skin in the game for the types of return they manage - approximately 16% plus on equity, in my day. Most of the capital at risk is depositor's funds and other unsecured lenders. Foreign wholesale creditors are protected by swap agreements and of course covered bond holders have recourse to the property underlying the pledged mortgages. From the article you link it is clear, at best Aussie banks have to put up capital of $1.60 per $100 per residential mortgage extended . Does any one believe banks have more than 3% in the game when commercial undertakings are included? Hence, depositors have at least 50% exposure without an advocate to manage their risk. And in fact the RBNZ has plunged them in the deep end and legally bound term depositors to underwrite the banks' working capital in the event of a solvency crisis. But because the wholesale and covered bond creditors are protected, depositors eat the most risk up to near 100%.

Thanks Stephen. I am rather fumbling in the dark here. I guess I am trying to see who benefits from the process. I can see that bank management are well paid, but that only appears to account for a very small percentage of the massive wealth transfer they manage.

There is a theory that the benefits of progress get capitalised into real estate value over time. I'm not entirely convinced, but clearly the banking system is the agent of wealth transfer in our society. It is clear who wealth is transferred from, but not clear to me who it is transferred to.

The benefactors are a) the staff who get the nice large bonuses lending others money out. b) the "wholesale" investors. c) the shareholders. d) the depositors. The impacts/losses however do seem to be going in the opposite direction . On top of that the present prices are at a 9 to 1 ration and are just silly, I cant see how the losses will ever be recovered myself.

"transferred to" on a global scale the financial industry and the very rich.

Thanks for quantifying the size of that potential impact. It also of course shows how much the tax payer would be liable. In terms of "legally bound", well that is a clear indication that if you think an OBR event is near you should not be tieing yourself down, though just where you run to is an interesting Q, is it not?

SH - If unsecured depositors actually formed some type of group, maybe they could lobby for change and enforce the granting of security instruments to be secured over their deposits.!!

#3 Rather than an individual business think of an essential item/commodity, say oil. So consider, if oil takes $80 / barrel to extract and the selling price is $60, because no one can afford to pay more, no company will drill for oil. How do you have any economy if the energy needed to run it is greater than the economy can afford?

#5 kids need job experience to get a job. That then goes further, jobs are getting more specialist and high end needing more experience to do. If you cannot even get a job how do you ever become a specialist?

A plumber fixing a toilet isnt particularly skilled, a programmer I'd say is. Such a geek however doesnt need to change oil, specialisation, see adam smith for that.

Go back to my original statement Steven, I talked about making a MODEST profit, not selling at a loss. If the product cannot be provided for a price that a given market can sustain then the inventors will generally create an alternative that will do the job at a cost that is affordable. In fact your choice of oil is a good one as there are many stories that allude to big oil suppressing alternative energy inventions over the years. Great for the conspiracy theorists! I am an aircraft engineer and have an IT degree and have done programming, and am a quality specialist. I can tell you that the skill levels between the engineer and the programmer are actually quite comparable, but the level of responsibility on the engineer is many, many times greater (do you feel safe when you fly?) but the pay rates are virtually inverted. Specialisation is the same, it takes a plumber 5 years to become qualified, it took me 5 years to get my engineers ticket, it took me 2 1/2 but a lot more money to get my IT degree. Tell me again why the pay rates are different? Ask any one when their toilet won't flush or a pipe breaks in their house how important their plumber is.

As no sovereign country is revenue constrained surely the answer to robots taking over jobs or part taking over jobs is to give everybody an inflation/wages indexed pension from leaving school age.

This is the Universal Basic Income (UBI) proposed by Gareth Mogan (and others):

http://www.bigkahuna.org.nz/

Switzerland have a referendum next year voting on whether to introduce one. It is not quite true that there are no revenue constraints as too much money printing causes inflation. However, certainly if a society becomes much more efficient (e.g., through robots) a UBI becomes more attractive.

I fail to see how you arrive at no sovereign country being revenue constrained. Real Govn revenue is based on taxation on the production of a good, what is left is printing and that has never really worked.

So no one ever works? kind of a wtf moment. a) Robots of course use energy where does this come from? b) Robots cannot do all work.

Steven, I suggest you start reading the MMT and then you will understand. http://bilbo.economicoutlook.net/blog/

#5

What people have not woken up to as yet is that the economy has moved, or become, digital in the digital world.

Banking work is being carried out by electron digits not people

Facebook, Google, Trademe and others work is being carried out by electron digits not people

Apple makes products so people can do things in the digital world, not the real world.

Entertainment such as Netflix work is being carried out by electron digits not people.

We are becomming just spectators while electrons do the work. - People are redundant.

unlikely, there are thousands of more IT programmers, techs, than there were 20 years ago.

all that is happening is people are doing different jobs gone are the typists they have been replaced by the IT department and so on and so on.

if roberts come along , you are going to need people to maintain them, programe them, oversea their production or progress.

the one that really peaks my interest is driverless trucks, who would want to be on a highway at night with a 44 tonne driverless truck on the same road

Are you talking about driver-less trucks that have better reflexes than a human, never get tired and never get drunk? I think all trucks should be driver-less. We'd be so much safer on the roads, imagine a world where trucks were never aggressive, always drove to the conditions, and were 500% more aware of their surroundings than those pesky bags of meat that used to drive them around and occasionally use them to block roads as part of "strikes". Driver-less trucks also sound like they could run 24/7 improving efficiency, reducing the cost of goods and generally making everyone's lives better.

..sharetarder...ever watched this.. robots bots will do to humans what the car did to the horse..

https://www.youtube.com/watch?v=7Pq-S557XQU

thanks food for thought, I was around just as computers came into my industry so have seen paper processing jobs replaced with IT departments and not seen the overall staff numbers fall dramatically.

if robots start to problem solve maybe could change big time.

interesting some really smart people have said that is dangerous

Stephen Hawking, the pre-eminent physicist, recently warned that artificial intelligence (AI), once it surpasses human intelligence, could pose a threat to the existence of human civilization. Elon Musk, the pioneer of digital money, private spaceflight and electric cars, has voiced similar concerns

Me! driverless vehicles will have wide safety margins programmed in meaning controlled, conservative speeds, a pre-mapped path on the road and no likelihood of the operator falling asleep or being ill or substance impaired.

one day the tech maybe ok but I think its a decade or two away

http://www.dailymail.co.uk/sciencetech/article-3281562/Tesla-autopilot-…

https://www.youtube.com/watch?v=mY1Bpvee2wI

2. China's story is either a miracle in the 21st century or a fairy tale - you be the judge and research how does China do it? Each year they import less means of production like oil and steal and each they grow their economy 6 or 7%.

#8

There is another posibility for the future.

We have seen how 3D printers are becomming better and cheaper.

Add to this that robots will also become better and cheaper

Add to this new materials being developed.

Now imagine a future in which big corporations are gone and there are lots of very small factories with robots and 3D printers.

Imagine as big corporations are gone we finance Universities to develop new materials, drugs and so on. Or that with AI robots could be our brains for designing these things.

These small (in your garage) factories not only produce more robots and 3D printers for other small factories but produce most of what we consume creating thriving mini markets scattered everywhere.

Imagine those who own these small factories bartering with each other. I will 3D print you a flash electric self driving car if you 3D print me an electric boat. and so on.

With tecnology ideas are endless.

I can't wait to buy a new chainsaw from the local 3d printing factory :) Will they sell new chains as well? Will they print the engine components separately ready to be assembled, or will they print the whole engine as one contiguous piece?

How about I swap you a couple of lambs for the freezer for....... have you got something I want?

skudiv - the earth is not flat and change does happen.

Who would have thought back in the 1800's that we would be flying around the world in metal airoplanes. skudive would have laughed at them for suggesting such a stupid thing.

Obviously the world is not flat, it is spherical and finite, though sometimes I think you pretend it is flat and infinite.

And another thing skudiv - this new nanotechnology and this carbon they are working on is tougher than steel and flexible. It may be possible in the near future to use in a 3d printer.

Look to the future - dont remain in the past

World growth is slowing down, that is why world trade is slowing down. Of course if you have your head stuck in the sand, and pretend that global growth is still growing, THEN you will be very, very confused why global trade is slowing. In fact you would even call it a mystery, and start babbling incoherently about services blah, de blah blah, blah.

Null hypothesis: "global growth is slowing"

Now prove it is wrong, global growth is not slowing because..............??????

#5 C-level execs will ultimately be replaced by decision software using big data and analytics. Will likely make better decisions.

dp

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.