Here's my Top 10 items from around the Internet over the last week or so. As always, we welcome your additions in the comments below or via email to bernard.hickey@interest.co.nz.

See all previous Top 10s here.

My must read is #7 from Gavyn Davies on the need for a Chinese devaluation because it's 'big switch' from factories to services is not working. Happy New Year!

See more Dilbert cartoons here. They're excellent.

1. The story behind 'The Big Short' - Regular readers of my Top 10s will know I'm a big fan of Michael Lewis, the author of The Big Short, Liar's Poker and countless other brilliant books and articles on matters financial.

Here's an excellent profile in The Observer by Tim Adams on how he came up with all the juicy detail behind 'The Big Short' and his other books.

I haven't seen the movie yet, but it's getting rave reviews and a few Oscar nominations. I have plans to see it this weekend.

I hope his followup book, Flash Boys, also gets made into a film. Another one of his books, Moneyball, has already been made into a movie. It's good too. The only time I've liked watching Brad Pitt.

Here's a sample of Lewis' method, including this little gem about how Michael Burry simply handed all his emails over to Lewis:

Perhaps the most fascinating character of all was Michael Burry. Burry had been a medical doctor, self-diagnosed with Asperger’s, before he proved so obsessively inspired at stock picking that he had been entrusted with a billion dollar hedge fund. It was his libertarian belief that the crash was a necessary evil. “Michael thought we are living in an age where there has been a collapse in personal responsibility, all these people should not be borrowing this money. Yes, the banks were disguising it and not making the checks, but the main cause of his moral disapproval was the ordinary man,” says Lewis. “Burry still thinks it would have done us good to have a full-on depression to realise the importance of taking full personal responsibility for everything we do.”

Lewis himself didn’t agree with that appraisal, but the thing that made Burry especially valuable to the story was a character trait that led him to avoid face-to-face contact with any of his investors. As a result, Lewis says, “he just handed me three or four years of emails, unedited – ‘here they are.’ It was a great resource because people’s memories of complex events are tricky. And here I had a day-to-day account from perhaps the only person following the situation with this degree of interest of exactly what was happening in those markets.”

2. It's all about China - Financial markets began the year with a bang, and not ih a good way. It's all about China and you could say it's always been about China, at least for our part of the world. There's lots of chatter about hard landings and capital flights and currency depreciations, but lots of debt is at the heart of the issue, or at least is a symptom of a problem.

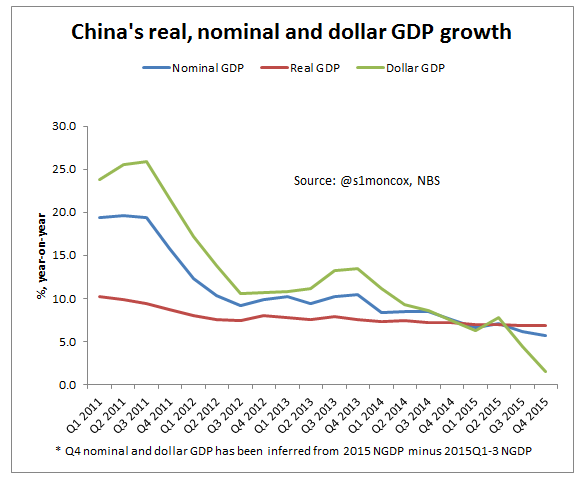

How China gets rid of its debt mountain is another issue. Given almost all of it is lent by state banks to state owned companies, there's a few options for orderly (or at least ordered) writedowns and recapitalisations and reshuffles that would not be possible elsewhere. But it could all get ugly, particularly given these state banks are likely to stop lending new amounts to all these loss-making companies. The chart below on the way nominal GDP growth in China has fallen is also sobering.

Here's Bloomberg with a look at the credit-fuelled growth model that China is currently using.

The flashing yellow light: there’s less and less power behind policy makers’ stimulus. For each $1 in credit expansion, China added the equivalent of 27 cents of gross domestic product last year, the least since 2009, according to data compiled by Bloomberg from government figures released Tuesday. As recently as 2011, each $1 generated 59 cents.

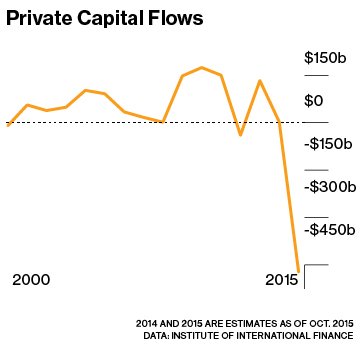

3. Capital flight - The issue of whether and how Chinese savers might try to get their money out before a renminbi devaluation is top of mind right now. Even with the capital controls in place at the moment, there's some room for some big flight, as the WSJ points out. Individuals are still allowed to each take out US$50,000 a year.

Do the math and the numbers get large rather quickly. China’s urban population in 2014 came to 737 million, according to World Bank estimates.

Assume that the wealthiest 1%, who easily have enough savings, convert the maximum allowed amount into dollars this year. That would amount to nearly $370 billion of outflows. If the top 2% of urban individuals do so, it would mean $740 billion of outflows. That is to say nothing of the many other ways to get money out of the country, legal or otherwise.

China has $3.3 trillion of reserves. For now, it can step in to meet this demand for dollars, offsetting pressure for the currency to depreciate. But the cushion is smaller than it appears. Part of the reserves—though it is unclear how much—is tied up in illiquid investments, such as funding for the Asian Infrastructure Investment Bank, and some risky ventures, like loans to Venezuela against oil assets. And reserves don’t have to go to zero before alarm bells start ringing. Beijing’s financial firepower won’t save it if its citizens take fright.

4. Chinese New Year could be interesting - The Chinese New Year is on February 8 this year and is a time when many Chinese people like to travel overseas. Don't expect to find a hotel room in Auckland easily around that time.

But as Christopher Balding points out, this year's holiday travellers may be taking more with them than a suitcase full of clothes. The chart tells the story too.

China watchers are missing the primary story that capital outflows are a domestic vote of confidence not an international portfolio issue. Portfolio investment by foreigners remains very limited.

Direct investment in China isn’t rising but there is no evidence that there is any real selling of operations to take capital out. The vast majority of capital outflows and pressures on the RMB come from Chinese voting with their RMB.

Watch the January February numbers as the spike in international travel and people with obvious opportunities to move capital abroad, will tell us something about their thoughts.

5. Can China really switch ? - The other big question about China's growth slowdown is how easily and well it will be able to switch from an industrialised and investment-led economy to one based on services and consumption. China itself is confident it can manage the switch without skipping too much of a beat. Sounds easy, but the reality may not be so so simple.

Here's Tom Mitchell at the FT with an explanation:

There are at least two known unknowns that could disrupt China’s smooth glide path. The first is what happens to rust-belt regions that have plenty of the old economy but not much of the new. “It will be very difficult for those who work in the old economy to transition into the new economy,” says Chen Long, China economist at Gavekal Dragonomics. “Coal miners do not become internet programmers overnight, or even delivery men.”

The second is a potential debt crisis of historic proportions, stemming in part from the government’s fears about the consequences for coal country if they were to turn off the credit taps. In 2007, on the eve of the global financial crisis, China’s overall debt to GDP ratio was 147 per cent. Now it is at 231 per cent and climbing.

“They absolutely have no room left for further debt accumulation,” says Rodney Jones at Wigram Capital, an economic advisory firm. “That’s the central issue — not the exchange rate, not the stock market. These are symptoms. The problem is unsustainable growth and continued rapid accumulation of debt, leverage and credit.”

On Friday, the government said that new borrowing surged to Rmb1.7tn ($260bn) in December, the biggest monthly increase since January.

6. A few more China bears - In the last couple of weeks even those who have been cautiously optimistic on China have started to become worried. Here's Mitchell again:

In a China-watching community where those at the extremes — “maximum” bulls and “coming collapse” Cassandras — often make the most noise, Jonathan Anderson at the Shanghai-based Emerging Advisors Group has long been regarded as one of the most thoughtful analysts. For years he laid out a convincing case for cautious optimism on the Chinese economy, but not any more.

“For years we have been waiting for China to make the tough choice and sacrifice near-term growth in order to stabilise macro balance sheets and stop its exploding debt cycle,” he wrote on January 4, the first day of this month’s market and currency mayhem. “[But] the costs of taking real adjustment are clearly too high for the government to bear . . . Right now we put the initial potential crisis threshold at around five years.”

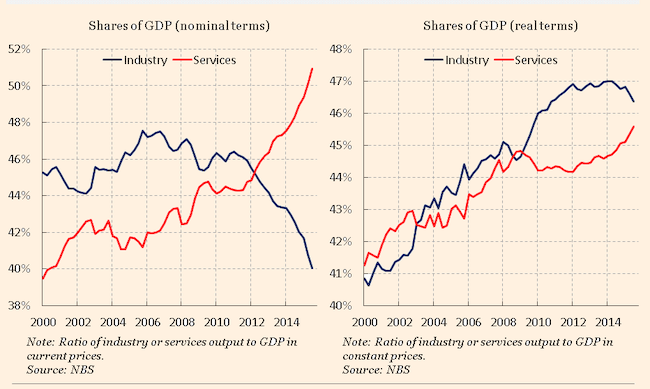

7. That switch is elusive - Gavyn Davies, who has certainly been no bear on China in the past, also expresses scepticism on China's ability to manage or even start the transition without a significant renminbi devaluation. The chart below shows why it's not happening yet.

There is a severe problem in the shape of the rebalancing of the economy away from old manufacturing sectors towards the new economy. Western economists have tended to see this as a silver lining in the recent economic history of China, arguing that the economy is successfully shifting resources towards the sectors that will dominate its future. But a careful look at the data suggest that this is far from the whole story:

The optimists point to the rise in the share of services in nominal GDP, and the corresponding decline in industrial sectors, as shown in the below left graph. Measured in current prices, the rebalancing appears to be well underway, with the share of industrial sectors falling from 47 per cent in 2011 to 40 per cent now.

However, almost the whole of this rebalancing in nominal terms has occurred because of a large drop in the relative price of industrial products compared to services. In real, inflation adjusted terms (below right graph), there has been no rebalancing whatsoever in the past decade taken as a whole (though there has been a percent or two in 2014-15). The needed shift in real resources – labour and capital – out of the moribund sectors has therefore barely started.

This conundrum is explained by the collapse in industrial goods prices that has occurred as excess industrial capacity has built up in the Chinese economy. Although this has happened in most manufacturing sectors, it has been at its most severe at the low-value added end – ie in heavy goods industries that are probably now making significant losses but are still being propped up by the state.

Most other economies, both developed and emerging, are experiencing negative producer price inflation as commodity prices have collapsed, but the size of the industrial sector in China makes it a particular problem there, and it has been exacerbated by the rising renminbi in 2013-15.

8. Net job destruction - The Future of Jobs report released this week for Davos is an eye opener. It's based on a survey of HR people in 15 major economies with 13 million staff. It predicts the net destruction of 5 million jobs by 2020 because of the 'Rise of the Robots' and other new technologies replacing white and blue collar jobs. That's a net number. There are 7.1 million jobs lost in this forecast, and 2.1 million jobs crated.

This is at the heart of the fears of a bunch of 'new Luddites'. The 'old' Luddites were eventually wrong the first time around because many multiples of new jobs were created after the machines replaced the artisans, although it took decades and not a few revolutions, wars and reshapings of governments and the creation of social safety nets to do it.

The assumption always is that eventually the new technologies will be net creators of jobs. But what if this time around is different?

Here's an excerpt from the report:

In terms of overall impact, the report indicates that the nature of change over the next five years is such that as many as 7.1 million jobs could be lost through redundancy, automation or disintermediation, with the greatest losses in white-collar office and administrative roles. This loss is predicted to be partially offset by the creation of 2.1 million new jobs, mainly in more specialized “job families”, such as Computer and Mathematical or Architecture and Engineering.

These predictions are likely to be relatively conservative and leave no room for complacency. Yet the impact of disruption will vary considerably across industry and gender as well as job type. For example, Healthcare is expected to experience the greatest negative impact in terms of jobs in the next five years, followed jointly by Energy and Financial Services and Investors. The industry that stands to create the most jobs, perhaps less surprisingly, is Information and Communication Technology, followed by Professional Services and Media, Entertainment and Information professionals.

“Without urgent and targeted action today to manage the near-term transition and build a workforce with futureproof skills, governments will have to cope with ever-growing unemployment and inequality, and businesses with a shrinking consumer base,” said Klaus Schwab, Founder and Executive Chairman of the World Economic Forum

9. Donald Trump? Really? - The amazing resilience of Donald Trump in the polls of Republican voters might be convincing a few of the party grandees to back Trump. They should be careful, as Nate Silver points out here. Trump is the most unpopular candidate by a mile with the voters who will actually decide who gets to be President.

Trump would start at a disadvantage: Most Americans just really don’t like the guy.

Contra Rupert Murdoch’s assertion about Trump having crossover appeal, Trump is extraordinarily unpopular with independent voters and Democrats. Gallup polling conducted over the past six weeks found Trump with a -27-percentage-point net favorability rating among independent voters, and a -70-point net rating among Democrats; both marks are easily the worst in the GOP field.

10. Totally Clarke and Dawe in holiday mood below - Cricket can be a wonderful metaphor.

14 Comments

#1 well worth watching, but have a stiff scotch to hand.

#3 note to sharetrader

3 they are keeping a closer eye on outflows

http://www.reuters.com/article/china-yuan-outflows-idUSL3N1532DW

World faces wave of epic debt defaults, fears central bank veteran

www.telegraph.co.uk/finance/financetopics/davos/12108569/World-faces-wa…

I don't think it would be a stretch of the imagination to see debt defaults. The more refinancing that occurs (paying debt with more debt), the bigger the inevitable collapse will be.

Clarke and Dawe!

What can you say?

Masterful

ya gotta watch Clarke and Dawe

As Chinese communism falls apart, watch for more, serious, jingoism in spots like S China sea, Taiwan, Sino-India border etc.

If it's happening in California, it's going to happen in Auckland. You just know it is. Prices up 30% in our biggest city over the next 18 months... 12000 IRD numbers given. Binge buying soon and many more cashed up on NZ residencey visas gifted.

http://www.forbes.com/sites/kenrapoza/2016/01/19/stock-market-crash-has…

You can buy in California but the tax man will never let you leave. The housing bubble is in small wealth enclaves, bay area tech centers and their weekend hideouts around Nappa.

The rest of California is still where it was years ago.

http://www.zillow.com/homes/for_sale/San-Diego-CA/16960887_zpid/54296_r…

http://www.zillow.com/homes/for_sale/Red-Bluff-CA/16172120_zpid/40516_r…

http://www.zillow.com/homes/for_sale/Chico-CA/18241781_zpid/37863_rid/4…

So what you're saying is, "greater returns in Auckland.." No taxes on houses, instant residency if investment big enough (no tax) free(ish) education and health and free money if you're old enough... A housing market that doubles every seven or eight years... You'd really be silly not to, wouldn't you.

Just got to keep the debt flowing. As NZ has over 100k a head in debt already that could be a big ask.

The government must be heading for some large falls in tax take, it could get creative, just thinking.

One would hope so Andrewj. But I fear our powers-that-be are more worried about the next election. So while hundreds of hours are racked up by Customs desperately trying to grab 6 bucks of GST, from that book you bought for your Musses from Amzon, hundreds of thousands of dollars is getting away tax free on every house sold in Auckland. I can't see that ever changing even under Labour, in the highly unlikely event they are ever voted into power.

To my mind, the first loop hole that needs to be shut, is the ability for permanent residents to vote. Should be a citizen only option, like pretty much every first world country. It's not like five years is a long time to wait. If you are allowing smurfed and smuggled money out of the PRC and then granting residency on the back of the property investment, you are certainly hedging your being elected bet.

Of course many of the MP's are multiple property owners on both sides of the debating chamber - many vested interests to protect.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.