By Bernard Hickey

Did you know that your money in a term deposit in a bank is not guaranteed by the Government?

Those in the know are aware that there is no Government guarantee, but it turns out most regular people, and certainly most term depositors, either still think there's a guarantee, or think there's always has been one.

New Zealand briefly had a government guarantee for retail bank deposits from October 2008 to December 2011. It was introduced at the worst point in the Global Financial Crisis to stop a run of deposits across the Tasman to the banks' parents in Australia, where the Kevin Rudd Government offered a guarantee for depositors there.

It was quietly dropped once global markets had settled down and was replaced by a system called 'Open Bank Resolution'. This means there is no Government guarantee and if a bank was to fail, the Reserve Bank would shut it down and manage a capital restructure overnight so that it could re-open the next day. One way a bank's capital could be restructured by the Reserve Bank is through a 'hair-cut' for depositors. Essentially, the Reserve Bank would slice a certain percentage - say 10% - off the value of term deposits to allow the bank to re-open with enough capital to survive.

This is, of course, a last resort that no one thinks is remotely likely any time soon. New Zealand's banks have stored away a lot more capital over the last eight years and are both well regulated and very profitable. They also have very large parents in Australia who would be expected to help out in a crisis and who demonstrated that support in 2008 and 2009.

The Reserve Bank regularly stress tests the banks for the worst case scenarios. In 2014 it tested the big banks with the scenario of a 40% fall in national house prices and a 13% unemployment rate and found their capital levels would fall, but would still be well above the regulatory minimums. Late last year the Reserve Bank tested the scenario of unprofitable dairy payouts for five years and a 40% fall in farm prices. It found the banks could easily absorb the losses through lower profits and would not have to eat into their capital.

That said, if there was a more extreme version of the GFC and the Australian parents went AWOL, and the local banks' capital reserves were wiped out, then the last resort would be for the Reserve Bank to 'hair cut' deposits. No one wants to talk about this for obvious reasons. It's painful to think the unthinkable and there's also the inconvenient political truth that the Government would come under enormous pressure to intervene to back a rescue before term deposits were cut.

If the Government did intervene again to guarantee all deposits and rescue the bank then the public's currently incorrect view about a guarantee would have been validated again, as it was in 2008. Essentially, depositors and bank shareholders would have been receiving an effective guarantee for free all along at the expense of taxpayers who don't have term deposits.

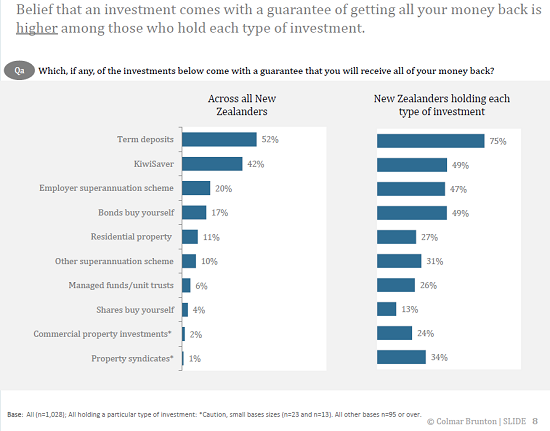

There is no question the public is poorly informed about this. A Financial Markets Authority survey in 2014 found that 75% of people with term deposits believed they were guaranteed and 52% of all New Zealanders believed term deposits were guaranteed.

However, there has been one exception to that incorrect view up until this week. Deposits in Kiwibank were guaranteed by New Zealand Post, but that will lapse once the deal proposed this week to sell 45% of Kiwibank to New Zealand Superannuation and ACC is completed. It will become just as un-guaranteed as the other banks, although the Government has offered to inject up to NZ$300 million in fresh capital directly if Kiwibank gets into trouble. The Government does not guarantee to repay the creditors of state owned enterprises, as Solid Energy's bankers found out last year when they had to write off most of their loans.

One of the reasons why New Zealand Post wanted to sell the stake is because it couldn't afford to keep offering the guarantee, and as Bill English pointed out this week, it wasn't really very credible anyway.

"The guarantee was not a strong one in that you had an entity worth NZ$1 billion guaranteeing NZ$17 billion of banking assets," English said.

"It wasn't really an effective guarantee, but now that's been replaced by an arrangement where the Government underwrites any capital requirements related to the bank coming under pressure...so that depositors know that if anything went wrong with Kiwibank, then the Government is able to stand behind it," he said.

He compared the Government's role behind Kiwibank to that of the Australian parents of ANZ, ASB, BNZ and Westpac, which is true, but not the same as a Government guarantee.

The problem remains that most New Zealanders believe their NZ$152 billion worth of term deposits in banks is guaranteed in some form when they are not. Those deposits have risen by NZ$45.1 billion since the end of the guarantee in December 2011 and have risen by NZ$63.7 billion since the guarantee was introduced in a hurry in October 2008.

The Commerce Commission would demand that any other product properly advertise its features, or it's lack of assumed features. If a seller of torches failed to put 'batteries not included' on the packet then there would rightly be questions about its compliance under the Fair Trading Act.

It's time the Reserve Bank and the banking industry ran a public education campaign during a calm and confident period to inform savers that there is no Government guarantee. It would reduce the pressure for politicians to act in a crisis and help investors think more clearly about the risks and returns from different types of investments.

A 'guarantee not included' label on their advertising would go some way to achieving that, but a proper industry publicity campaign would help too. The Government is forever informing drivers about the risks and their responsibilities in advertising campaigns. It's time we had one for savers too.

A version of this article was also published in the Herald on Sunday. It is here with permission.

64 Comments

Lets say that the govt said: "There will be no govt bailout of any bank in NZ. The OBR will be enforced", would the banks become more prudent all of a sudden? Hahaha!

The Aussi banks are already facing a huge losses in the minerals field:

http://www.bloomberg.com/news/articles/2016-04-08/bank-dangers-exposed-…

Well this adds even more urgency to get my savings out of a TD at ASB and into Auckland property. Thank you for this insight. It's almost as the goal of OBR is to pump up housing.

which is ironic as it's the Auckland housing market that is causing most of the risk.

It would appear that the banks have confidence in the Auckland market. This article was in Stuff today which was quite interesting:

http://www.stuff.co.nz/business/money/78674407/where-were-2007s-worst-p…

Quote:

But buyers in the market now can feel reassured they are not going to see prices plummet in the same way.

Goodall (Corelogic senior research analyst) said it would be hard for the same thing to happen again because banks were now more particular about their lending. "It was too easy to get ridiculous amounts of money, that's not so likely any more."

All of NZ need to see The Big Short

Anyone left now not knowing how fraudulent the system is not going to change their views let alone understand TBS. Infact for many knowing the truth would lead to chronic depression. Don't underestimate human ignorance to facts that don't suit their ingrained life long feed of propaganda. Governments know this, hence no mass riots on Wall St post bailouts

people living in bubbles never see them, all it takes is a reversal of Chinese money flowing into the west.

>>>

The expansion of Chinese Credit has been greater than I previously imagined possible. Hundreds of billions – perhaps Trillions - have flowed out of China, with untold amounts flowing into the U.S. (real estate, securities and M&A). For that matter, I believe huge inbound flows have been inflating U.S. securities and some real estate markets, especially “money” fleeing bursting EM Bubbles.

Indeed, extraordinary international financial flows are fundamental to the global government finance Bubble thesis, flows that I believe are increasingly at risk. Along with Bubble flows from China and out of faltering EM, I believe speculative flows grew to immense proportions. And, importantly, the massive global pool of destabilizing speculative finance has been inflated by the proliferation of leveraged strategies. Chair Yellen may not see “high leverage,” yet on a globalized basis I strongly believe speculative leverage reached new heights over recent years. “Carry trade” speculation – borrowing in low-yielding currencies (yen, swissy, euro, etc.) - has proliferated over recent years, especially after the 2012 “whatever it takes” devaluations orchestrated by the European Central Bank and Bank of Japan.

http://creditbubblebulletin.blogspot.com/2016/04/weekly-commentary-bubb…

Chinese money is not going to stop.

Like I said, people living in bubbles.

http://www.thisismoney.co.uk/money/markets/article-3523194/Internationa…

http://www.scmp.com/business/global-economy/article/1934198/chinas-debt…

The Chinese Communist Party are playing wack-a-mole but they are clamping down as new avenues are found to circumvent the rules of getting money out of China. I wouldn't rely on Chinese money propping up the Auckland property market.

Is Corelogic going to bet its house on that statement?

How does this quote relate to the Auckland market. There is nothing in the article about banks confidence in Auckland. The article refers to markets outside Auckland that have declined due to "artificial price peaks that were not sustainable".

I would assume the banks would look at each region and assess the risks peculiar to the region/city/town. The banks being nationwide would have an assessment for the Auckland market.

While true - it doesn't mean they actually they follow their own risk assessments. If you have enough equity - the banks will lend to you even if the market turns - your equity is lost first....

The Auckland market is as safe as money in the bank, so sayeth the bank.

At least with a collapse you would still own a place to live, if i love my savings then I have nothing.

Buy gold?

Or buy a safe and put cash in it.

An OBR event would occur after the bank has lost all its assets/reserves. This implies the housing market would have already collapsed by 30%+ ergo you would lose your money earlier, IMHO.

I’ve read in various articles that in case of a bank bail-in, derivatives will get paid out before the depositors as these are regarded as unsecured loans.

My question is, do any of the NZ banks dabble, read gamble, on these financial structures?

And if so which banks?

for certain the 'covered bonds' issued by NZ banks to overseas investors are exempt from OBR. As of last June "some $20 billion of residential mortgages in New Zealand were encumbered by covered bond programmes, of which 44% were against properties in Auckland, Fitch said". These assets will not be available to NZ depositors in case their bank gets into difficulty.

In contrast to the RBNZ approach, in Australia the RBA did not allow covered bonds to be introduced until all deposits were backed by deposit insurance ($250,000 per person per bank). The RBNZ has chosen to leave NZ depositors exposed to banking failure while protecting the overseas holders of covered bonds.

Try explaining that to the hoi-poloi

I don't believe that covered bonds are exempt from the OBR. I believe it just shuffles the holders ahead of other bond holders.

Perhaps someone could clarify this.

As per their name and intent covered bonds are guaranteed by a specific pool of low LVR residential mortgages and any non-performing mortgages are regularly removed from the covered bond pool - in New Zealand. In Australia the RBA can stop that removal if a bank gets into financial trouble. This is not the case in NZ. Hence the covered bonds are guaranteed by performing loans which are not available to NZ depositors. You could be forgiven if you view this as a pre-determined 'good' bank versus what is left for NZ depositors.

ANZ's latest annual disclosure statement page 22 of 70 claims exposure to $1.412447 trillion derivatives held for trading. As per usual it will not be the actual final realised losses that imperil ANZ but interim marked to market losses that demand sourcing margin collateral to meet contractual counterparty demands. Read more The share price is indicative of some troubling balance sheet stress in need of liquidation.

The main implementation issue with OBR is it would destabilise the entire banking system, with four banks A,B,C,D. If you take a bank over with a Statutory Manager OBR and haircut 10% the next day when said bank "reopens" as a recapitalised bank with implied gummint backing (would be impossible for said bank to trade internationally without unless RBNZ stood as man in middle) people in the other banks would withdraw cash to put into the OBRed bank. Otherwise they could also have a haircut coming in their bank.

Simple really as you cant be OBRed twice.

So it would create a bank run... not a thing to do in such a time of stress.

This is an interesting comment!

Yes, I believe this also. Any implementation would create an immediate run elsewhere....so I believe the other banks would immediately limit withdrawals with the RBNZ and government approval. Look to Greece as examples. €300 a day limit put in place. Here it would be less. This is why the KB deal was really made as they heavily rely on holding deposits.

I think though the critical thing to NZ having a crash of any sort will be sudden job loses on a large scale cascading into bank defaults

You might imagine that the "rescued" bank would have restrictions on the opening of new accounts, or that the guarantee would apply only to balances at the time of failure.

Although, as a prudent person, you might want to have active accounts spread across the entire industry.

If a bank has just been OBR's I'd wonder on how may ppl would be happy moving into it? though it could be a safer bet than staying in where you are. Yes a second bank account seems sensible, and/or even a credit card from a different bank(s) which is what I have done also (VISA and Mcard).

I think the OBR is an empty threat. They'd never do it. Too deflationary. There'd be hell to pay .

Have a look at Cyprus and Greece. That might change your mind.

I think those countries are fundamentally different from NZ because they don't have their own central banks, or their own currencies. They couldn't liquidate their debt by devaluing themselves out of trouble.

A bank failure's a bank failure, no matter what the currency, and yes, they do have central banks.

They both use the Euro and they're at the mercy of the European central bank.

That is a different argument, ie that would force a default /OBR quicker I think. --edit-- also if NZ did that no one would lend to us aka Greece? and we'd have to print? or stop paying ppls money.

So lets say the private banks needed a large sum to become solvent again. Wouldn't the RBNZ just loan a large sum the government who would then purchase the non performing loans from the banks. This would lower our currency favouring the export sector Things would probably have turned to custard overseas anyway so it might not adversely affect the countries cost of borrowing? The cost would be borne by holders of cash who would see quite severe inflation, but I dont think the government would care too much about that.

That is of course a gamble. However if we get an OBR I think we will already be in severe deflation anyway with the Govn close to financial default itself so I am not so sure.

There would be hell either way, there would be hell from the OAPs but also on the opposite side there would be hell to pay from the tax payer and younger generations expected to pay for it for many decades.

Austria Just Announced A 54% Haircut Of Senior Creditors In First "Bail In" Under New European Rules Read more

the banks only have to put up %24 of %8 as capital, around $1.90 for every $100. So lending 1.7 bill into AKL every week, is a bit of a no brainer of you are keeping an eye on your bonus and the other option is?

Thanks for the answers all, but it hasn't answered the question whether the big 4 Oz banks and Kiwibank trade in derivatives.

Here an article from last year that makes me worried about these derivatives.

What happens when/if things go belly-up for the Oz banks, will that affect their NZ offshoots?

http://investmentwatchblog.com/how-australias-big-4-banks-can-sink-the-…

Kiwibank advised me that they don't trade derivatives. But can one trust a banker?

In addition to my comment above some account must be taken of the NZDs raised from ...foreign currency funding, which accounts for approximately 21% (~$67.4 billion) of total registered bank funding as at December 2015...

The cross currency basis swapped NZD lent to the NZ banks by say a foreign supranational NZD lender is protected by the receipt, via the swap, of say USD borrowed by our local NZD banks' foreign subsidiaries. The leaves the NZ domestic OBR exposed depositor liable for the additional instability carnage caused by this type of exempt funding source. Read more for info links

Why wouldn't foreign wholesale funding costs rise for Aussie banking units?

Those Australians struggling with mortgage payments and the possibility of damage from the global commodity price slump are helping to inflate bond risk for Macquarie Group Ltd.’s banking unit.

The cost of insuring Macquarie Bank notes against non-payment climbed to as much as 172 basis points last month, the highest since June 2013, after the lender flagged a rise in overdue home loans. The Sydney-based bank’s credit-default swaps have increased 39 basis points in 2016, the second most in the benchmark Markit iTraxx Australia index, and were at 155 basis points April 8. Read more

Is this the wheeze whereby reserve funding for domestic lenders has been taken up and applied to international distressed debt.

The margins must be epic.

The reporting a nightmare as discounted secondary mkt loan purchase deals don't look flash on a domestic home loan report format.

So, let's say you had $100,000 in a term deposit, and the bank failed, what is the likely scenario?

The Govt would allow the bank to keep all transactional accounts running, while you might take a 50% haircut on your TD.

So, best to buy the new car now, buy all deferred maintenance on your house e.g. New fire, solar etc, prepay all ongoing accounts like rates, power etc.

and run a larger amount in your chequered account/s.

Keep a reasonable sum of physical cash.

Cheque.

Freudian slip!

I like Freudian Slips.... it brings out the best in a person ;-)

It still sucks though if we, the depositors, have to pay for the "over-enthusiasm" of the banker's lending.

The banks lend what the RBNZ allows them to lend with the RBNZ's unique lack of real oversight and regulation. Inadequate retained NZ earnings, inadequate provision for bad loans, excess one-way expatriation of bank declared profits. After all, the RBNZ have put the NZ depositors as the ones at risk for any over-enthusiasm of lending. It's not them nor the bankers who will suffer from OBR.

It would be good if you could pay off say 10 yrs of future rates. But no council would want this because it would force them to predict what the future rates may be. And in Ak, the rail tunnel job and IT spend (and future infrastructure maintenance catchup when its forced upon council) will make the future rates look horrendous. In which case people may start to reassess the viability of living in Ak. (Len's most live-able city).

Bank deposits in Cyprus and Greece are better protected than those in New Zealand.

However they're a little far away, so the best option would probably be to ship your money to Australia, which operates a government guarantee scheme (AUD250k per person per bank).

So depositing money in the bank is like smoking, requiring caution in the package about the risks to the health ?

I really can’t reconcile two concepts, both of which I believe to be true. It makes me want to behave in two different ways. I think it’s called cognitive dissonance. Here are the two concepts:

1. Governments and central banks will do anything to avoid deflation because deflation increases peoples purchasing power in a way that’s not taxable, and deflation increases the real debt burden. I find it hard to imagine the OBR being implemented in this context. This makes me want to get rid of all cash and be reasonably indebted to a safe degree say 300-400K.

2. Steve Keens financial modelling which shows that high debt to GDP ratios lead to a collapse of the financial system. Or if not collapse, at least what happened to Japan. Perhaps we’re witnessing that now with collapsing commodity prices, global trade, and velocity of money. This makes me want to hold cash (or gold/silver if I’m feeling really pessimistic), keep powder dry and wait for opportunity.

Anyone else having these thoughts?

Panama anyone?

Yah, it's best to keep your money in a shell company.

Fundamentally I have a huge issue with the language used here; "government guarantee for retail bank deposits" suggests that the Government is protecting depositors funds, but in reality as the law directs, that money actually is the bank's, then in reality the Government is protecting private institutions from their own excesses. Isn't this a form of corruption? We would be much better off if the Government required banks to provide protection for depositors funds themselves (probably through insurance) and consequently would likely see improved bank behaviour, and more prudent business decisions.

It need not involve government guarantees as such. In the USA for instance the FDIC receives no government appropriations and never has. "it is funded by premiums that banks and thrift institutions pay for deposit insurance coverage" says their website and as a consequence "Since the start of FDIC insurance on January 1, 1934, no depositor has lost a single cent of insured funds as a result of a failure." And any banking failure has short term impact on depositors - "Most of the time, the transition is seamless from the customer's point of view."

The FDIC is also pro-active in identifying and regulating and addressing risks - which has not been the NZ approach to date.

Not suggesting that the FDIC model is the only approach, but the RBNZ is definitely unique in its hands-off approach and implementation of the OBR system to make NZ depositors responsible for potential banking failure.

The question is, what constitutes "insured funds"? Banks are like slippery weasels, so I can imagine, given the opportunity they'd ask depositors if they wanted their deposits insured, at a cost of course! This would effectively penalise the lower end of society. Whereas I'd like to see it being a statutory requirement for all depositors funds, at the banks expense. Can't see a banker putting it into law though, just like us not being a tax haven.

Wow, so many kiwis think the money is guaranteed by the government! LOL. 49% of those with kiwisaver think the money is guaranteed, and that is just ridiculous, but statistics never lie.

50% think national are doing a good job, sometimes people just astond me. on what measure are they thinking this i am guessing because they like JK and can not see what is happening in the backround

I'm no lefty, but it seems to me that if a Big 4 bank gets into this much trouble after all this warning, the government should nationalise all the NZ assets of said bank.

Right you are.

Review your diagram, reverse the arrows.

Then correct, non.

Simply solution, banks should not be able to call them deposits if it's not guaranteed. Dictionary definition for deposit "to place for safekeeping or in trust, especially in a bank account."

Force the name to be Term Investment/Etc,

Not so simple, the average depositor would not consider that they are "investing" their money, but rather placing it with the bank for safe keeping. If the banks cannot be trusted to act with the integrity expected of such responsibility without regulation (specifically or otherwise) as is being demonstrated then they must be made to statutorily. If a bank collapse did occur and the general public became aware of how little the Government were prepared to protect their interests, it would likely be the pollies at the top of the lynch mob's list rather than the bankers. JK is both so he can't run and hide anywhere. More to the point his unwillingness to act just makes him look more corrupt.

perhaps if a bank goes under we should have all mortgages increased by %20 to %40, that way both depositors and debtors share the pain of an OBR event.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.