Today's Top 10 is a guest post from Martien Lubberink, an Associate Professor in the School of Accounting and Commercial Law at Victoria University. He previously worked for the central bank of the Netherlands where he contributed to the development of new regulatory capital standards and regulatory capital disclosure standards for banks worldwide and for banks in Europe (Basel III and CRD IV respectively).

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

Europe and the policy bouillabaisse

1) The Euro.

For the first time since I moved to New Zealand, I was able to visit Europe for two weeks, in May. I visited Brussels, The Hague, Amsterdam, Maastricht, Bonn, and Cologne: cities that conjure up associations with the great European project called "European Union." As a tourist, you will probably admire Europe for its culture, architecture, efficient public transport, and affordable beer and wine. But then there is the Euro.

A blessing for tourists, the Euro always reminds me of the time that I took a taxi from Raleigh–Durham International Airport in the U.S. and had forgotten to convert my Euros into dollars. With no cash dollars and no ATM in sight, I offered the taxi driver a fare of twice the dollar amount in Euros, my cash. Unaware of the single currency and the favourable rate that I offered him, I started explaining the colorful banknotes that I showed him: you can use them to pay foie gras in France, Parmesan cheese in Italy, and BMWs in Germany. Lots of advantages. "It is legal tender, backed by European 20 countries," I said, "so you can trust the Euro. Really!" It all failed to impress him, he declined my offer.

That was ten years back, and I am not sure if matters have improved since. The Euro area is struggling. One in five young Europeans are unemployed, with Greece, Spain, and Italy reporting 40% of their under-25s having no work, visit this link to see for yourself. This is a tragedy for sure.

2) Easy money

To get things going in Europe, the ECB adopted a fierce policy of monetary expansion. Mind you, from this month on, the ECB will start buying corporate bonds.

The expansionary policy of the ECB is controversial. German finance minister Wolfgang Schäuble wants to end it, because low interest rates hurt the retirement savings of Otto Normalverbraucher (German for Joe Sixpack). It also fuels anti-European sentiment, which, with politicians like Marine Le Pen, Nigel Farage, and Geert Wilders, is in no short supply.

3) Super Mario

However, ECB's Mario Draghi, took Schauble head-on. He wants Germany (with a current account surplus above 5% of GDP for almost a decade) to start spending: “Those advocating a lesser role for monetary policy or a shorter period of monetary expansion necessarily imply a larger role for fiscal policy.”

We obey the law, not politicians

4) Low profitability, is it risk or incompetence?

Low interest rates lead to perverse outcomes. One, for example, is low bank profitability. In her speech on the 22nd of February, ECB's top bank supervisor Sabine Läutheschalger identified weak bank profitability as a challenge, which in English means that it constitutes a potential risk for Europe's financial stability.

Defining low profitability as a risk is remarkable, because it is also a manifestation of outdated business models and incompetent management.

5) So, how to cure Europe's weak banks?

The obvious solution would be to reduce the number of banks. As ECB's other top supervisor Daniele Nouy last week explained: banking costs remained too high in proportion to their incomes and lenders would actually benefit from a wave of consolidation as there are too many banks in the bloc.

The alternative solution would be to allow banks to become more risky: more risk leads to more profits. However, with the GFC fresh in mind you would rightly question the prudential merits of this solution.

6) So, how not to cure Europe's weak banks?

Unfortunately, the European Commission decided to allow the banks to play the risk game, as if a financial crisis never happened. Last week for example, in his unabated pursuit to "help" European banks, Commissioner Jonathan Hill presented watered-down rules for 'bail-inable' capital. Bank should have this type of capital in issue to protect taxpayers from the effects of bank-failure. However, the European Commission, apparently ruling against taxpayers, now allows banks to issue less of this type of capital. The Commission decided so despite opposition from the European Banking Authority. In an exceptional move late last year, the EBA openly expressed its dissent over the Commission's plans.

7) Elke König the hawk, Elke König the dove.

In Brussels, I attended the Single Resolution Board (SRB) conference. The SRB is the resolution authority for large European banks. It’s like a fire service: if a bank is on the verge of collapsing, the SRB will make sure this happens in an orderly fashion.

Now, what you don't want of course, is that a fire service starts setting houses on fire, just to keep the firefighters busy. Likewise, the head of the SRB (Elke König) wants to keep banks as safe as possible, also because her "fire service" has the budget to save only ten banks in the next 4 years(!)

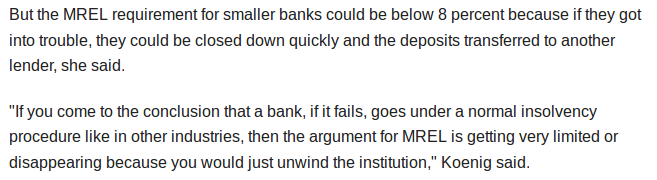

So expect some tough-talking from König on 'bail-inable' capital requirements (MREL - see them as fire extinguishers), which she did last December. 8% of total assets is the suggested baseline or minimum:

In other words: any house should have at least eight fire extinguishers, a fairly steep requirement.

How different things are now. This is the same Elke König, now making the case for lower bail-in requirements:

Ah, well, maybe if your house is made of straw, then who cares about your place burning down.

I imagine somewhere in Brussels a conversation like the following between Jonathan Hill (or was it the French or Italian treasury?) and Elke König took place:

8) From Bail-in to death to bail-out.

At the SRB conference in Brussels, there was a lot of talk about bail-inable securities and Contingent Convertible Securities (CoCos). These securities are risky, as they can be written off if a bank runs into trouble. This is kind of good for the bank and for financial stability: conversion allows a bank to recover from a perilous situation. The bank will then not contaminate the financial system. But conversion is not so great for the holder of a CoCo. There is a risk that he loses the value of the security.

CoCos are also difficult to understand, so there is a case to prevent them from "hitting the streets." Some countries (UK, Netherlands) do not allow retail investors to buy CoCos. However, other countries are more relaxed - at their peril.

Italy, for example allowed retail investors to buy CoCos. Last year, however, one retiree from Civitavecchia, near Rome, took his own life after losing about €110,000 because of such a conversion.

As a result of the controversy that ensued, bail-in is now off-limits in Italy. Instead, the country appears to have reverted to bailing-out its poor performing banks through a special purpose vehicle called Atlas (Atlante). It will impose losses on its shareholders, taxpayers: strong and large Italian banks (UniCredit, Intesa Sanpaolo, UBI Banca), and the publicly controlled Cassa Depositi e Prestiti.

To add insult to injury, this week, Bank of Italy Governor Ignazio Visco urged the European Union to return to pre-GFC times when bailout and state support were totally acceptable:

This obviously undermines Europe's plans to protect taxpayers from the fallout of failing banks.

9) CoCos and creativity

Meanwhile, financial firms in this part of the world appear blissfully unaware of the morbid effects that CoCos can have on retail investors. Look at the artwork on the documentation of CoCos issued by the Commonwealth Bank of Australia earlier this year:

School Savings Bank NO. 1

How cute is that!

A recent issuance of insurer Insurance Australia Group Limited (IAG) looks equally promising. It sports a fixed rate of 5.15% p.a. - but there is the risk that your investment will suffer a write-down. The documentation mentions that "all or some of the Notes will convert into ordinary shares in IAG if a non-viability event occurs. ... Or, if conversion does not occur, the Notes will be written off.” At conversion, the shares are probably worth very little, so buyer beware.

10) Exotic convertibles

To end on a lighter note, an investment banker recently alerted me to what looks like a novelty in the land of contingent convertible securities. Credit Suisse sold bonds that would protect the bank from operational risks, such as risks of rogue trading and fraud. Insurance against this risk is new. It looks like a catastrophe bond, a bond that may be written off when a disaster happens.

It is ironic though, since it is not that Credit Suisse is whiter than white. Not so long ago the bank blamed its "worst January ever" on rogue traders.

Selling rogue trader insurance to Credit Suisse, anyone?

8 Comments

Re:#8

At the SRB conference in Brussels, there was a lot of talk about bail-inable securities and Contingent Convertible Securities (CoCos). These securities are risky, as they can be written off if a bank runs into trouble. This is kind of good for the bank and for financial stability: conversion allows a bank to recover from a perilous situation. The bank will then not contaminate the financial system. But conversion is not so great for the holder of a CoCo. There is a risk that he loses the value of the security.

What are the differentiating end-game features between CoCos and New Zealand bank deposits under the RBNZ OBR regime, in the event of a bank solvency crisis?

Idiot question, but all this appears to be talk about bailing out banks rather than regulating their behaviour. The talk is all about the risks that banks are taking, the risks that their actions pose, the risk of the impacts of what they are doing will have. Yet the German Finance minister, Wolfgang Schäuble when he mentions Otto Normalverbraucher touches on the real victim of banking behaviour, but not with a view to protecting him. These banks are private right? since when then did it become incumbent on the tax payer to protect and prevent private institutions from failing? I assume that the general public in Europe have it the same as here in NZ, they have little choice but to use a bank, and all banks behave pretty much the same, so ultimately there is no choice, so why are the banks being protected and not the private depositor?

When you are a depositor, you are one of the banks suppliers and are treated with contempt. You are a customer when you borrow from them. Does that help?

It's more a function of state sponsored institutional support.

This is not the case in respect of foreign wholesale funding.

Why are international investors demanding greater credit spreads from the major banks? In short, it’s because they can – international investors are well aware of the dependence of the banks on international debt markets to meet the funding requirement of their loan books.

As a result, international investors are the price setters for the banks’ wholesale funding. Arbitrage will ensure the cost of domestic wholesale funding is closely aligned. Yeah right!!!

While Australia’s major banks are dependent on international bond markets for term debt funding, international investors are not dependent on Australia’s major banks for investment opportunities. Read more

Disgraceful Google and its nefarious influence on the Brexit vote. No wonder the electorate is so ill informed.

"Google has demoted the site EU Referendum to “below the fold” in searches for the term “EU referendum”, where it isn’t visible to most web surfers unless they scroll down.

The political site, which was founded by author and researcher Richard A.E. North in 2004, was the top search result for the topical expression across all the major search engines for a decade.

At Google, the site has been demoted to 10th (or 13th, depending on how you count it) for the search term, with links to the BBC and the pro-EU Guardian newspaper ranking higher. North’s site still ranks No.1 for the same term over at Yahoo! and Bing.

Google dominates the market with over 90 per cent share of search engine traffic in Europe.

The No.1 ranking search result on average receives 33 per cent of the traffic generated from a search, studies have found, a number which diminishes rapidly as the ranking falls. Sites in 10th place receive only around 2.4 per cent.

Europhile newspaper the Financial Times ranked EUreferendum.com as the most influential British political blog in 2006, and the site kept its top spot in the search results even after a domain move."

http://www.theregister.co.uk/2016/05/31/google_axes_eu_referendum_websi…

Reminds me of an old joke:

Where's the best place to hide a dead body? A: On page 2 of a google search result.

The picture about Incompetence..Is it a sly dig at how Auckland is being run ? Especially about the new Rail line, which seems to be more of a beautification project for the CBD at a high cost, rather than an effort to provide speedier transport alternatives from the suburbs into the city ?

It is possible to feel sorry for banks. They have one lot of regulators telling them to issue more bail-inable capital and another lot warning people not to buy these securities. Yet another lot saying that banks should not grow too big to fail and another set saying the industry needs to consolidate.

To cap it off when the banks struggle to make a decent profit with interest rates negative and conflicting regulation, Mr Lubberink suggests their business models are outdated and management incompetent. Maybe bankers do deserve their big salaries!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.