By David Chaston

Banks have been increasing their fixed mortgage rates recently. They claim their "funding costs" are rising.

For the major banks, current funding costs are based in the wholesale swap markets.

For minor banks, current funding costs are more about what they have to pay depositors to keep their funds and win new investors.

That is also true for the major banks, but retail deposit costs are less of a dominant issue for them.

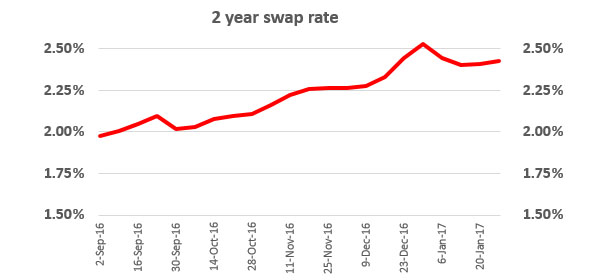

Since September 2016, wholesale funding costs have risen. This chart shows what has happened to 2 year swap rates.

Notice how this cost has been basically unchanged in 2017.

These rises have been driving the increases in the fixed rate carded offers, which we have been reporting as they have been coming through. In 2017, banks have been making frequent changes (usually, but not always rises), sometimes more than one per week.

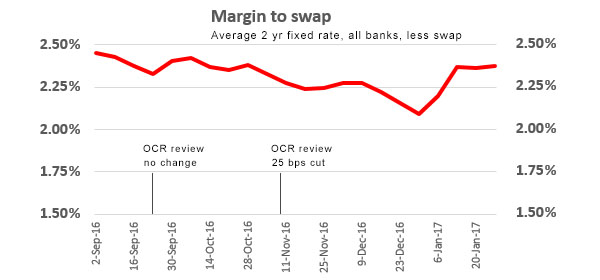

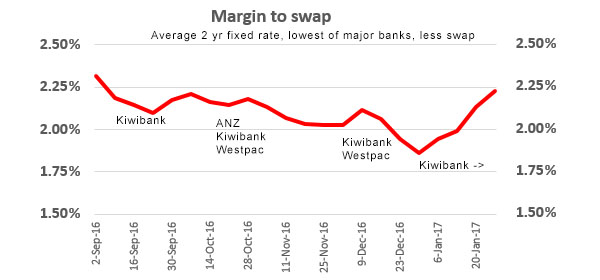

The best way to assess the banks' response to the rise in wholesale swap rates is to look at the margin-to-swap. That is, the carded mortgage offer rate, less the related swap rate. This story concentrates on the popular two year rate.

The marking on the above chart of the RBNZ OCR review dates is not to suggest that any 2 year fixed mortgage should be sensitive to an OCR review; it is just there as background.

The above chart focuses on the average two year rate for all banks.

And it shows that bank margins broadly declined from September to December. It also suggests that the early 2017 rate rises are more about restoring bank margins than actually responding to recent (non-existent) wholesale swap rate changes.

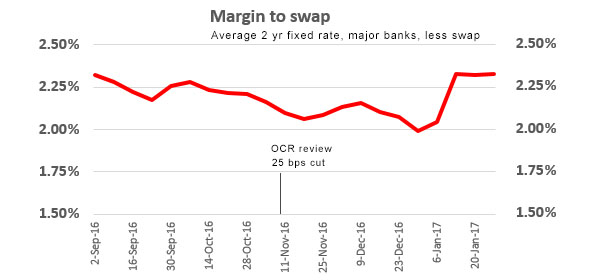

For most home loan borrowers, the all-bank averages are 'interesting' but not nearly as important as the offers from the major banks.

Just focusing on the majors, the charting of the changes reveals an extra dimension:

And that is, the major banks are not just restoring margin, they seem to be embellishing it higher. Not by much, it is true, but certainly at the higher end of the range.

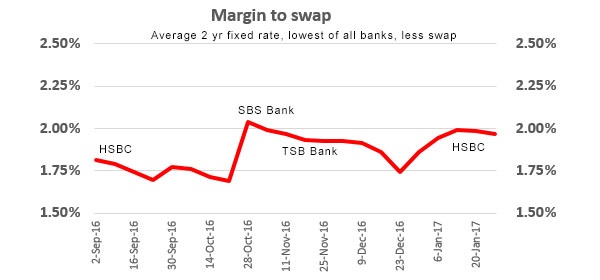

However, at the cutting edge, some banks are prepared to forego margin for market share.

And this is equally true for the major banks, although they have taken their opportunities over the holiday break to restore margins while borrower scrutiny is lower.

At the other end of the range, high rates really do turbo charge their margins.

A close comparison of these charts shows there is not much between the "lowest major" and the "highest major" in terms of margin percent. But banks fight for every 0.1% gain.

This analysis has focused only on the two year offers. In fact, some banks have targeted their best offers at other terms. Kiwibank's one year 4.19% offer is especially attractive a t present and the impact of that does not get reflected on our narrower review.

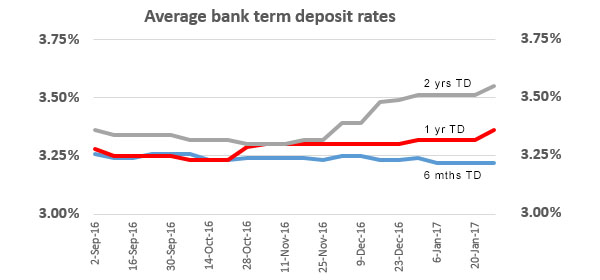

The final element to review is what banks have been paying retail depositors.

So, yes, banks have been raising term deposit offers over the same period, but unless you are prepared to commit to at least a two year term, the increases are minor (or in the case of a 6 month term, non-existent).

2 Comments

Increasing profits is pretty plausible. The Australian banks are heavily depending on money coming in from New Zealand. Expectations will be forced on the New Zealand branches. Anyone who has worked in an Australian owned corporate environment will be familiar with the orders that are handed down from the head office.

Of course every other bank will follow because: profits.

Excellent information DC and good labelled charts. It's good to see hard data research amongst all the phaffing that us common taters present.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.