Today's Top 10 is a guest post from Martien Lubberink, an Associate Professor in the School of Accounting and Commercial Law at Victoria University. He previously worked for the central bank of the Netherlands where he contributed to the development of new regulatory capital standards and regulatory capital disclosure standards for banks worldwide and for banks in Europe (Basel III and CRD IV respectively).

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

The cost of bad behaviour

1) Bad apples and groups.

I once was part of a team with this odd colleague. He had a strong belief in what we now call alternative facts, said “yes” but he did “no”, kept important information to himself, and thought and acted as if he was acting team leader. When he spoke, he used all sixty minutes of his allotted five.

It was a pain, especially sitting through team meetings. We did not want to be lectured about the flat world around us. Unfortunately, our real team leader did not know how to deal with this ‘bad apple’ – Instead, our manager left. Actually, all of us left. It was so bad that our team’s annual budget for farewell functions was fully exhausted by October(!) But the ‘bad apple’ stayed – no surprise.

2) Slackers, downers, jerks.

Professor Will Felpps of UNSW has published on ‘bad apples’ and groups. There is this funny section of the U.S. radio show This American Life where Will explains one of his studies: He ran an experiment with groups of students where he assigned an actor to each group. Unknown to the other students, the actor played the role of a slacker, a downer, and a jerk. Felpps’ study shows that having just one slacker or jerk in a group can bring down performance by 30% to 40%. One single person can take down an entire group.

If your group has a bad apple problem, then it is worthwhile listening to the first 13 minutes of this This American Life section, because it has this remarkable discovery around minute 11 of the show. Felpps reveals a surprising way to cure a group from a bad apple problem.

3) Why bad behaviour, and why won’t it stop?

It often amazes me to see how difficult people find it to recognise bad behaviour as such and then fail to take appropriate action. It also amazes me to see the efforts people make to over-analyse obvious badness - often to the point that no corrective action can be taken because relevant evidence has evaporated or got snowed under by irrelevant facts. Paralysis by analysis is often real.

4) Recognising badness, then what?

The first attack on the World Trade centre happened in 1993: a truck bomb exploded in the basement of one of the twin towers. With the benefit of hindsight, this attack did not attract the attention that it deserved. However, one person who realised the significance of the 1993 attack was Rick Rescorla, a former military man who became director of security for Dean Witter-Morgan Stanley in 1997. He had predicted the 1993 attack. He also expected that a next attack could involve a plane crashing into one of the towers.

Dissatisfied with normal emergency procedures, Risk started a three-monthly emergency evacuation drill that ultimately led him to save the lives of 2,687 employees who worked in the North tower on 9/11. Rescorla insisted that all Morgan Stanley employees participated in the emergency evacuation drill. This led to conflict with his superiors who did not want to waste valuable time. He also ignored instructions from the Port Authority of New York to remain seated after the second plane hit the north tower.

The story of Rick Rescorla shows how important it is to recognise bad behaviour as such and act decisively. And if you wonder why you worked off-site because of the Kaikoura earthquake, maybe it is because your firm lacks a person like Rick Rescorla.

5) Method acting – or just doing your homework.

But doing what Rick did is easier said than done. Many people are just clueless. They are inexperienced, lack the relevant knowledge to identify bad behaviour, or they rely on wrong information. Rick Rescorla did not suffer from any of these imperfections. He had was an experienced military man. He served in the British and the U.S. armies and was sent to Vietnam.

Following the 1993 twin towers attack, Rick grew a beard and attended morning prayers at Mosques. He spoke fluent Arabic to infiltrate in the Muslim community.

Agreed, method acting is over the top for most jobs, but there is nothing wrong in doing proper homework and using your intelligence to help your colleagues. A problem, however is facts.

6) The problem with facts.

The Financial Times this week offered a long-read that shows the efforts large companies make to confuse us. In The problem with facts, Tim Harford shows the strategies that Big Tobacco pursued to deliberately produce tobacco ignorance. For example, the dangers of smoking were scientifically documented in the nineteen-fifties. But thanks to cunning strategies of Big Tobacco, it took decades before effective measures against smoking were taken.

“The tobacco industry was the leading funder of research into genetics, viruses, immunology, air pollution,”… . Almost anything, in short, except tobacco. “It was a massive ‘distraction research’ project.”

The same applies to climate change. Big Oil companies realised that carbon emissions would make our planet warmer. In 1991 Shell Royal Dutch knew that our climate was changing at a ‘faster rate than at any time since end of ice age’. The company even produced a film - Climate of Concern - about climate change. But the film was left unseen. Uh oh!

Oil giant Exxon learned about climate change in 1981, but, according to the Guardian Exxon funded climate change deniers for many decades.

7) It takes a village.

A similar story applies to bank capital. There is ample evidence of the benefits of high bank capital ratios. See this recent speech by Claudio Borio. He shows that more bank capital is better for all of us. Borio makes it perfectly clear that “capital is the foundation of all lending.” More capital leads banks to lend more and create more liquidity. It puts banks in a stronger position competitively, and it enables them to survive a financial crisis. This all leads to higher bank valuations.

So why then do banks dislike capital? Professor Anat Admati, in It Takes a Village to Maintain a Dangerous Financial System, examines why many of us persistently contribute to a financial system that is inherently dangerous. She puts is it down to willful blindness. “The underlying problem is a powerful mix of distorted incentives, ignorance, confusion, and lack of accountability. Willful blindness seems to play a role in flawed claims by the system’s enablers that obscure reality and muddle the policy debate.”

So, if you want to know why some central banks claim that they did not see the Global Financial Crisis coming, then it is likely because there is this large village that turns a blind eye to big and important problems.

8) Willful blindness at the Spanish central bank.

In the same week that I taught about bank governance, news broke that current and former leaders of the central bank of Spain (Banco de España), including former governor Miguel Ángel Fernández Ordóñez, had been charged over the Bankia banking scandal.

Bankia is a large amalgamation of failed banks that floated on the stock market in 2010. Shortly after floatation, its share price collapsed. Spanish taxpayers had to rescue the bank, many retail investors lost their money.

Mergers almost always fail. The AOL -Time Warner merger failed in a spectacular way. Knowing that mergers tend to fail then begs the question: Who at the Banco de España would have thought that merging seven failed banks into one would work?

Insiders knew about the problems, that is for sure. Just look at what some of the internal emails revealed: “This is not working, it’s getting worse. … Bankia’s capacity to generate resources is deteriorating.” Bankia is a “money-losing machine”; Bankia had “very severe and growing problems of profitability, liquidity and solvency”. Bankia was “unviable”.

Which makes me wonder, what do about other prudential supervisors, are they well governed?

9) Blinded by a lack of experience?

I applied for a position at the central bank of the Netherlands in March 2008. It was the week that Bear Stearns was bailed out. At that time I lived and worked in the U.S. During the job interview, I asked my to-be managers to respond to Bear’s failure: would this, and other bank problems, affect Europe as well? I don’t remember the answer, but when I started my work at the central bank in July 2008, I noticed the naiveté of the Dutch. Where I had noticed UK’s Northern Rock and foreclosures in the U.S., the Dutch seemed oblivious. Only when Lehman Brothers fell, we all started realising there was something seriously wrong. It then took until April 2009, more than a year after my application, before bank regulators started to redraft bank rules and promised to:

“take action, once recovery is assured, to improve the quality, quantity, and international consistency of capital in the banking system. In future, regulation must prevent excessive leverage and require buffers of resources to be built up in good times;” (G20 London Summit – Leaders’ Statement).

What may have contributed to this delayed response is the accounting and bank regulation itself. Two import new sets of rules were introduced shortly before the crisis: IFRS and Basel II. Until the onset of the crisis, IFRS allowed banks to recognise gains with greater ease than old-style accounting. No supervisor had dealt with the rules in adverse economic conditions. Note that the Dow Jones stood at 14,000 in November 2007. In addition, Basel II may have allowed banks to estimate risks based on data that was free of crises.

It took a while for supervisors to figure out how to deal with the new rules in a crisis, when correlations increase and valuations drop. Supervisors may have just been clueless: they had two new measurement instruments, but lacked the experience to read them.

At one point during the crisis, the International Accounting Standards Board even reversed some of the IFRS fair value accounting rules, because banks and regulators were more comfortable with the old rules.

The new rules / measurement tools were weird too. There was a rule that required banks to add back to capital any fair value losses on assets that were held for sale. Such rules do not inspire trust in bank supervisors, who apparently lulled themselves into a false sense of security - thinking that banks were still well capitalised. They weren’t.

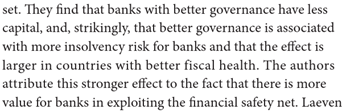

10) Bank governance is special.

Poor bank governance also contributed to the Global Financial Crisis. Checks and balances in the banking sectors were apparently ineffective, pay was excessive, accountability had taken a holiday. The Basel Committee responded to this by issuing Corporate governance principles for banks. These principles, however, do not necessarily reflect state of the art knowledge.

Professor René Stulz in this paper documents some interesting misconceptions about bank governance. Some of them conflict with the Basel governance principles. Professor Stulz critically evaluated the applicability to banks of traditional governance ideas. His article highlights studies that examine governance, where ‘governance’ refers to traditional ideas of governance that work for non-banks:

And where the Basel governance principles highlight the importance of board qualifications, Stulz shows this remarkable result:

14 Comments

Interesting post, thanks. There is no effective law that can constrain the greed of a human heart.

RE#9 - There was a rule that required banks to add back to capital any fair value losses on assets that were held for sale

Wasn't this related to bank liabilities that had similar characteristics to the falling value of the assets held for sale, hence the institution could theoretically buy in/extinguish the liability at a lower price, for an unrealised gain at the time they were marked to market and claim the capital write back?

Gotta laugh.

As regards number 10, perhaps this is because the predatory large banks sold their worthless goods to smaller banks who were better capitalised. "We can always sell this crap to some banker from Dusseldorf" comes to mind. If you've got the time this is a brilliant and entertaining Michael Lewis article:

http://www.vanityfair.com/news/2011/09/europe-201109

The global financial system may exist to bring borrowers and lenders together, but it has become over the past few decades something else too: a tool for maximizing the number of encounters between the strong and the weak, so that one might exploit the other. Extremely smart traders inside Wall Street investment banks devise deeply unfair, diabolically complicated bets, and then send their sales forces out to scour the world for some idiot who will take the other side of those bets. During the boom years a wildly disproportionate number of those idiots were in Germany. As a reporter for Bloomberg News in Frankfurt, named Aaron Kirchfeld, put it to me, “You’d talk to a New York investment banker, and they’d say, ‘No one is going to buy this crap. Oh. Wait. The Landesbanks will!’ ” When Morgan Stanley designed extremely complicated credit-default swaps all but certain to fail so that their own proprietary traders could bet against them, the main buyers were German. When Goldman Sachs helped the New York hedge-fund manager John Paulson design a bond to bet against—a bond that Paulson hoped would fail—the buyer on the other side was a German bank called IKB. IKB, along with another famous fool at the Wall Street poker table called WestLB, is based in Düsseldorf—which is why, when you asked a smart Wall Street bond trader who was buying all this crap during the boom, he might well say, simply, “Stupid Germans in Düsseldorf.”

Trump is making America 'grate' again.

Seriously...No Joke.

http://www.marketwatch.com/story/this-is-how-much-it-costs-meals-on-whe…

A Yuge amount of wilful blindness in the USA; now how can I leverage Trumpism??

Nice top 10, thanks. Particularly enjoyed the FT article on facts. I have a question on bank capital. What would happen if we phased in 100% reserve on lending for existing residential real estate? Would that not help eliminate speculative credit based bubbles? Is there any real benefit in allowing banks to create credit for such lending?

Random thoughts:

A large collapse on the demand side as buyers without capital are removed from the real estate market (unable to borrow).

A big increase in demand for rentals for same reason as above (renters cannot borrow to be buyers).

Anyone with legal access to foreign lending gets a huge market advantage (might be any multi-national corporation).

Possible massive increase in interest rates (if banks lending is limited they might as well make as much as they can on what they *are* allowed to lend).

Big increase in interest rates for term deposits grants huge gain to anyone with savings (banks try to attract more local capital).

Regulations required to stop foreigners buying everything (NZer's generally are not "savers" & some foreign groups do plus foreigners have access to lending).

Maybe the Australian banks would pull out of NZ as a poor return on capital/under performing market?

Maybe - would certainly have to be phased in to gauge effects. Some of those, like rising deposit rates, are arguments for. My understanding is that, at least in the UK, residential real estate lending requires less reserve then business lending (as deemed less risky) making loans for business hard to get - would reverse that distortion. Also, can't see large corporations entering our housing market given the current pitiful yields. I think it's one reason we don't see the large commercially managed apartment complexes you get in other countries - the mom and pop's are accepting a below-market rate of rent, so it's not worth their while. Note, my proposal is for existing residential property - loans for new builds and commercial properties would be as now.

I am hopeful that 100% equity based lending will steadily gain market share over time. Peer to peer lending is 100% equity based (although the lenders may have borrowed the money against their other assets of course). Hopefully as they get bigger they will be able to mount a political attack on the excessive privilege of the bankers.

But it's so much more profitable to create the credit out of nowhere?

When people refuse to accept the truth (on terrorism, human damage to planet, financial chicanery etc), then they actively accept the delusion sent to them. Rational well-educated career/business successful people included.

Make your own path & plans #4.

If you're interested in how the fossil fuel industry buried the science and shaped public opinion then there's an excellent free book available see link below (230 pages).

"What Australia knew and buried...then framed a new reality for the public" by Maria Taylor

"Taylor’s book shows how Australia could have acted on climate change a quarter of a century ago, but how corporate interests and economic ideologies not only stopped the clock on action, but wound it back."

https://press.anu.edu.au/publications/global-warming-and-climate-change for download.

The science as far as I follow it now gives humanity less than 50% chance of keeping global warming to 2 degrees- there's been precious little action to reduce emissions since 1990 globally, NZ emissions are 40% over 1990 levels. The "carbon budget" was 800 Giga tons of C02 to release before we exceed 2 degrees warming in 2011; since then we have used 15% of this. So can we turn around our C02 use in time - its going to be a monumental effort & we need to do way way way better than we have now to this point.

Ignorance is bliss when it comes to global warming. Unfortunately this won't help our children and their children who will live with te consequences of our actions.

If there's one thing I've learned reading the comments of many a property investor it's that they don't really give two hoots what's left to the next generations of Kiwis. They're too busy trying to import as many buyers as possible to displace them with prices far beyond NZ incomes. Selfish people who aren't interested in what's left to coming generations.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.