Today's Top 10 is a guest post from Martien Lubberink, Associate Professor in the School of Accounting and Commercial Law at Victoria University. He previously worked for the central bank of the Netherlands where he contributed to the development of new regulatory capital standards and regulatory capital disclosure standards for banks worldwide including Europe (Basel III and CRD IV respectively).

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

Ten years after the start of the Global Financial Crisis (GFC) - some lessons learnt.

1) Many happy returns. Last week it was the 10th anniversary of the GFC, though probably some of you do not see it this way. On August 10, 2007, the Financial Times reported it in an innocuous way. I mean, who would have thought that this headline would lead to a crisis with a magnitude that few of us had experienced before: “BNP Paribas investment funds hit by volatility.” This event shocked people close to the source of the problem, but most of us were blissfully unaware of the big trouble ahead.

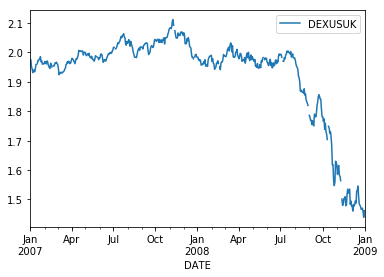

At the time I lived in the US, on sabbatical from Lancaster University. We had rented out our UK home for £1,500 per month and rented a Chapel Hill, North Carolina, home for $3,000. This was a perfect hedge: the Pound traded at two US dollars. Aware of the risk of foreign exchange rates, I kept an eye on the cable.

My tenth anniversary of the GFC therefore will be on 14 September. That is ten years after the Bank of England bailed out Northern Rock. At the time, I feared this event would affect the exchange rate. I had nightmares of a forced return to the UK.

Luckily, the Pound held up until July 2008 - when I had moved to Holland and commenced working at the Dutch bank supervisor - still unaware of any big trouble ahead.

Expect many anniversaries in the year ahead. Bear Stearns got into trouble in March 2008. Regulators seized troubled IndyMac mid July and in September 2008, everything went pear shaped when someone erred by not bailing out Lehman Brothers.

Stories will be told again and again, one hopes we will learn.

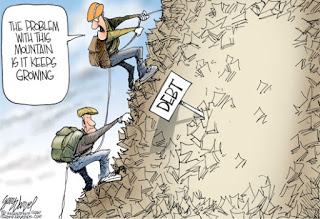

2) Ten years with little economic progress. Concerted efforts prevented a crisis from happening again. But the regulatory response to the GFC went hand in hand with some disappointing outcomes. Economic growth in many countries picked up only moderately. Debt to GDP ratios have remained constant, indebtedness just moved from the private sector to governments, as Martin Sandbu writes in the Financial Times.

The problem with this mountain is it keeps growing.

3) Now things start falling apart. One regulatory response to the lacklustre growth has been to undo parts of the post-GFC regulation. Donald Trump promised to do a 'big number' on the controversial Dodd-Frank financial regulations, and it looks like he is delivering on this promise.

The undoing of Dodd Frank has begun, and it is a win for the American people. That is, if we want to believe a victorious House Financial Services Committee Chairman Jeb Hensarling in this interview: “Hopefully the nightmare of Dodd Frank will be gone soon, … too much capital is sitting on the sidelines, … . The animal spirits of free enterprise can roam yet again and we are going to see Americans with pay increases. The economy is gonna come back.” Really?

Jeb Hensarling

4) Even the Federal Reserve jumps on the reregulation bandwagon. This was a surprise to me: the Fed board recently fell victim to the idea that regulation has become excessive: “After a multiyear review, the regulator concluded that excessive regulatory duties are hobbling bank boards and distracting directors from the more important work of guiding bank strategy and adopting effective governance at their institutions.”

The Fed proposal wants to protect bank boards from information overload: “Absent actively managing its information flow, boards can be overwhelmed by the quantity and complexity of information.” The proposal intends to end the practice of examiners reporting all regulatory matters requiring immediate attention (MRIA) to a bank’s board as well as its senior management. Instead, the Fed proposal leaves it to senior management to report to the board.

The idea is to enhance bank board effectiveness, more or less like this:

5) Europe, in the meanwhile, discovers how the post-GFC regulation works, … . Since I last wrote for interest.co.nz, Europe has experienced the effects of its bank resolution and recovery directive (BRRD). The idea behind this directive is to protect taxpayers from the fallout of failing banks. An important tool to help accomplish this objective is the bail-in tool, which allows losses to be imposed on banks’ owners, creditors, and depositors.

The results of recent supervisory actions under the BRRD are mixed. First was Banca Monte dei Paschi di Siena, the oldest surviving bank in the world. It has been a basket case for many years, but after it failed last year’s EBA stress test, matters went downhill quickly. That bank was bailed out, by way of a precautionary recapitalisation.

This is all well within the European rules, which allows Italy to inject €5.4 billion aid into the bank (bail out). At the same time, junior bondholders and shareholders share a burden of losses amounting to €4.3 billion from the conversion of junior bonds into equity (bail in). To prevent political fallout, the bank will pay retail investors €1.5 billion to compensate them for bain mis-sold financial products.

6) … works like charm. On June 6, the European Central Bank determined Banco Popular Español was failing or likely to fail. The next day, the Spanish bank entered resolution, after which it was sold for €1 to Santander. A bank run, in which Popular burnt €3.6 billion in the days prior to the rescue, drove the ECB to publish its declaration.

About €3.3 billion losses were imposed on Popular's owners and bondholders. Shareholders were wiped out in full, holders of convertible capital instruments (AT1) and subordinated debt capital (AT2) shared a burden of €2 billion.

European officials were elated by the success of this transaction. Valdis Dombrovskis, the EU’s Vice-President in charge of Financial Stability claimed “We believe this test is passed with success”. According to Elke König, chair of the Single Resolution Board, this “shows that the tools given to resolution authorities after the crisis are effective to protect taxpayers’ money from bailing out banks.”

7) ... or can be sidelined. The relative success of the Banco Popular case was short-lived. On 23 June, the ECB deemed Veneto Banca and Banca Popolare di Vicenza failing or likely to fail. Silvia Merler explains the deal in a blog post on the Bruegel website.

The short story is that Italian big bank Intesa "offered to buy the 'good' parts of the two Veneto banks for a symbolic sum of €1. All the non-performing loans, equity and junior debt will be bailed in. Equity is mostly held by the Atlas fund, whose participating banks have already started to write-off their stakes. Junior bondholders – for about €200 million – will be bailed-in and reimbursed afterwards ...".

The controversial part of this deal is that the Italian government circumvented the European Banking Recovery and Resolution Directive (BRRD) with a special law to facilitate bailout. This law respects European state aid rules, it is not illegal. However, the Italian special purpose law enfeebled the stricter BRRD. This did not go down well with some European bank officials: Eurogroup leader Jeroen Dijsselbloem wanted to make "sure that even if other legal frameworks apply, the state aid rules should be to the same kind of level". German Finance Minister Wolfgang Schäuble chimed and found the EU insolvency rules “difficult to explain.” Last week, Elke König, the head of the eurozone’s Single Resolution Board, urged the EU to close down national loopholes that allow some governments to bail out some banks, where other EU governments abstain from doing so.

Interestingly, this week the ECB released new non-confidential information on the Banco Popular deal, which shows that the bank was solvent in the lead up to its demise. Similar ECB disclosures on the two Italian banks can be found here and here.

All in all, 10 years after the onset of the GFC, we are getting there.

8) Groundhog day? In the meantime, the Reserve Bank of New Zealand published a second consultation paper on bank capital. It concentrates on answering the question: "What should qualify as bank capital?" It brings back fond memories of the time I was involved in helping solve this question, when I was member of the Basel and EBA sub-groups of own funds/capital.

One point I noticed while reading the consultation paper. It suggests that preference shares issued by the four big subsidiaries may fail to perform: "A capital instrument issued by a bank to its parent is thus recognised as capital. However, given the instrument transfers a potential loss from the bank to its parent, it is possible that transferring the loss to the parent will contribute to distress in the parent that in turn harms the New Zealand bank (i.e. the loss transfer may be ineffective)."

But note that the parent bank needs to fund these instruments too. It will unlikely use equity capital for that purpose: equity is costly. Neither can the parent fund the instruments with inexpensive, short-dated debt, as this would create double gearing and other prudential no-nos. Consequently, the parent will likely issue an equivalent instrument to outside investors, thus offering an efficient and effective solution. This renders the subsidiary's instrument effective. In fact, this is what many parent banks do: they issue back-to-back equivalent instruments to outside investors. And it is crucial to have the same regulatory treatment across the group as well. Another way of looking at this issue is by asking this question: would the chief risk manager of National Australia Bank allow problems at BNZ to imperil NAB … if it can impose these problems on outside investors?

9) Healed capital issues. Last week, the Reserve Bank and Kiwibank resolved their differences on two regulatory capital instruments. Press coverage on last week's restorative event was pallid. Kiwibank's press release shows that the bank has fixed the problem by de-consolidating its Special Purpose Vehicle. Whether this solves the potential tax liability that made capital specialist Cetier the First worry, remains unclear. The consultation paper on capital indicates that, to date, the risk that Cetier identified has not been reflected in the capital requirements of banks. To be continued?

10) Lessons learnt. First, due process is sooo important! The rules that entered into force since 2009 are largely effective. This is because much of the new financial regulation is the result of long and intensive discussions between knowledgeable people with diverse backgrounds from many countries, extensive consultations, and outreach to stakeholders (and no, there is no compelling evidence showing undoing the bank regulation will help the economy). Because of due process, the Basel III definition of capital is a success. Resolution rules may need some time to achieve satisfactory effectiveness, but the Banco Popular case shows that practice can follow theory: convertible capital absorbed losses without affecting financial stability.

Second: do not confuse association with causality. For example, the idea of contagion does not necessarily make sense - it implies causality. Think again: why would problems in Hershey's cause problems in Whittaker's? Why would a risk manager give a competitor power over the fate of her own company? The case of Banco Popular demonstrates this point: contingent convertible regulatory capital instruments were bailed in, and there was no contagion. Still, some academics and policy makers point to Deutsche Bank's spreading CoCo hazards of 2016 to point out the flaws of contingent convertible capital. However, the Deutsche CoCo case was association more than causality: problems arose because of amended EBA rules on Pillar II. They affected all banks and forced investors to reprice.

Third: sometimes bank supervisors mix up confidentiality with opacity and in doing so sacrifice transparency. Confidentiality is there to protect banks and their clients, opacity is there to protect the supervisor. The tension between both requires careful management and should preferably not be at the expense of transparency.

Lastly: Watch out for the months ahead, in particular September:

14 Comments

Really useful and interesting thanks

+1 - Thanks

Yes, wonderful links from Martien.

In NZ's case, what have we learned?

-- Do most people really understand why NZD is traded at a magnitude disproportionate to the trade of goods and services?

-- Do most people understand what the carry trade is and why NZD and AUD collapsed against JPY (the currency of a far more indebted country) during the GFC?

-- What proportion of NZers think that we dodged a bullet relative to the rest of the developed countries (and the Anglosphere which has natural "ownership" of monetary paradigms), therefore our bubbles are different to the bubbles that burst?

We are told NZ was one of the countries which was left relatively unscathed by the GFC.

I dispute this. 10 years on we have sold major assets to overseas companies and interests to bring in money.

We borrowed about $200 million a week. Most NZers were made to feel rich selling houses to each other and to overseas buyers at a higher and higher price and now houses are unaffordable to a large part of the community.

I feel we would be much better off if we had of just bit the bullet at the start.

All we did was tread water while the tide went out and now that no real increase in production occurred, the economy will suffer long term.

To be *relative* would require a comparison to *something* else. Relative to what?

Brazil, Italy, Japan, South Sudan .. ??

I think he means relative to the countries that were negatively impacted to a greater degree by the GFC. In the case of Japan, house prices were already in the toilet and the Nikkei plummeted while the yen strengthened more than any other (not good for an exporting nation). The primary destination for their exports, the U.S., also fell into the doldrums.

On the surface, it appears NZ did relatively well. As well as Australia. Interestingly, I think relative household debt levels in NZ and Australia compared to other developed countries were not that much different to what they are now.

I guess, but being relative to nothing doesn't leave much substance to the 'dispute' does it.

Relative to the man who died a woman who just received a negative diagnosis for cancer is better off.

Relative to a woman who just received a negative diagnosis for cancer a man who just lost one leg is better off.

Relative to a man who just lost one leg a woman who just went bankrupt is better off.

Someone who presents a relative argument without any point of relativity is like a one legged man. Not that I have anything against his other leg - but neither does he.

lolol, good stuff

Fair enough, but your analogy is limited. You already gave an example of your anchor: relative to other countries. Your reference point doe not necessarily have to be other objects; it can be other dimensions, such as time. Therefore, you might want to compare NZ at points in time: now and a point of time before, say immediately before the GFC.

Well of course, all analogies are limited, that is their nature.

OK. I think it is useful to compare NZ to other countries (and time), but it's probably how you shape your sample set. And I think we typically do that: the Anglosphere and OECD nations.

Yes, if itsme had done that his/her post might make some sense.

Actually I agree with the sentiment: Our economic buoyancy has been driven by selling houses (don't know about the wholesale pawning of other assets). I cannot quantify the extent to how that has driven the economy (neither can Treasury or any other institution). The situation is similar, generally speaking, to all the countries that have suffered from corrections in asset prices.

RalphLove it haha

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.