By Ryan Greenaway-McGrevy*

One of the stated goals of the Auckland Unitary Plan (AUP) is to restore housing affordability in the city. But it will not be easy to tell if it is working – at least not at first.

Let me explain.

The plan is designed to increase the supply of residential dwellings by, among other things, relaxing restrictions on urban density. If successful, that increase in supply will help put downward pressure on prices.

But relaxed urban density restrictions will also increase the value of land. That will put upward pressure on the price of dwellings that sit on land that is able to be profitably redeveloped. This is because the value of the option to redevelop the property is embedded in the sales price. In other words, the right to pull down the old bungalow and replace it with a block of units is going to attract a premium.

Disentangling these offsetting effects when measuring overall trends in property prices will be key to evaluating the efficacy of the AUP. But the widely-reported price indices published by Quotable Value and the Real Estate Institute of New Zealand are an average across all residential sales, which obscures any bifurcation in the market. As such, these indices may not be that useful when evaluating whether the plan is restoring affordability to the Auckland housing market.

What we need are price indices that distinguish between properties that can be profitably re-developed on the one hand, and those that cannot on the other.

This redevelopment premium depends, in part, on where a property is located, since density is only permitted to increase in certain targeted areas of the city. But it also depends on the existing extent of site development – which I will refer to as ‘site intensity’. While it makes sense to pull down a three-bedroom bungalow to build an apartment block, it makes less sense to pull down a block of apartments to build another block of apartments. In economic terms, the opportunity cost of the forgone rent from the demolished bungalow is much less than the opportunity cost of the forgone rent from the demolished apartments.

One simple way we can evaluate whether the AUP is working is to first identify sales transactions that are located in areas zoned for additional density, and then distinguish between low-intensity and high-intensity properties before constructing price indices for each separate group.

If intensification is working, we should expect to see an increase in the price of low-intensity housing that has been upzoned to support additional density. Think about a three-bedroom bungalow sitting on a quarter acre that that falls into the ‘Terrace Housing and Apartments’ residential zone, which is one of the highest density residential zones under the AUP. This low-intensity housing should have appreciated significantly in value, reflecting the increase in the value of the option to redevelop the site.

Meanwhile, existing high-intensity housing that has been upzoned should not increase in value, and, over time, should decline in value if intensification brings additional construction of high-intensity housing to the market. Think about an apartment block on Mt Eden Road that has just been upzoned under the AUP. The apartment block already is the kind of housing that the plan is designed to encourage, and it makes little sense to redevelop the site. The redevelopment premium embedded in this kind of property should therefore be rather small. And if the zoning changes encourage construction of more high-intensity housing, the apartments within the block should also decline in value (at least relative to price trends in the rest of the housing market).

But in order to observe these price trends, we would have to construct a different price index for each type of property – high-intensity and low-intensity - for each residential planning zone in the city. This is exactly what Kade Sorensen and I do in our Centre for Applied Research in Economics discussion paper.

We first define a ‘low-intensity’ property as having an intensity ratio below the median intensity ratio of all transactions in the quarter of sale, while a ‘high-intensity’ property has a ratio above the median. The intensity ratio, in turn, is the ratio of the assessed value of improvements to the total assessed value of the property. This ratio is our measure of the existing extent of site development. A small state house sitting on a quarter acre typically has a low intensity ratio, while at the other end of the scale, an apartment typically has a high intensity ratio.

Having sorted transactions according to their intensities and residential zone, we construct price indices for each different group. The price indices are based on repeat sales – this is the same methodology used in the US for the Case-Shiller price indices. Repeat sales circumvent many – but not all problems – associated with measuring house price inflation.

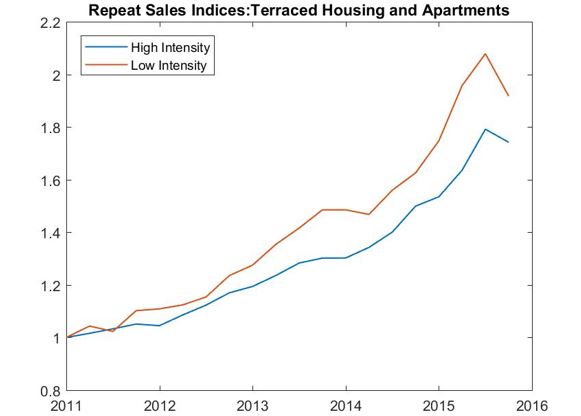

The figure below exhibits prototypes of these price indices for Auckland from quarter one 2011 to quarter four 2015 for the ‘Terrace Housing and Apartments’ residential zone. This zone has the least restrictive land use regulations among the residential planning zones in the AUP. For example, it permits five storeys to be built. We begin in 2011 as this is immediately after amalgamation into the super city. Our data ends in 2015, but we soon hope to update our results to 2016.

The blue line is a price index based on sales of high-intensity properties, while the red line is a price index based on sales of low-intensity properties. The price indices are normalized to one for Q1 2011.

Evidently there is a marked divergence in prices across the two groups. High-intensity properties appreciated by 77% between Q1 2011 and Q4 2015, while low-intensity properties appreciated by about 95%.

This result is what we would expect if upzoning inflated the redevelopment premium. Within the Terrace Housing and Apartment Zone, low-intensity properties (e.g., the bungalow sitting on a quarter acre) have appreciated by significantly more than high-intensity properties (e.g., apartments and flats).

If the AUP is successful, we should expect this divergence to continue. But, more importantly, the price index on high-intensity properties in this zone will decline if construction brings additional supply of terraced housing and apartments to the market.

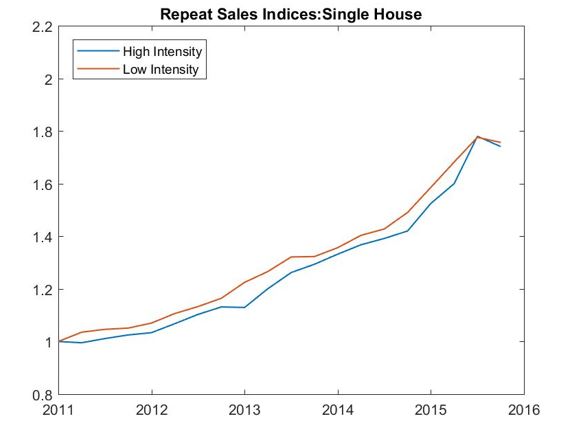

Next, let’s have a look at price trends for properties located in the ‘Single House’ residential zone under the AUP. This is one of the lowest density residential zones in the plan.

High-intensity properties in this zone appreciated by 74% over the five-year period, which is qualitatively indistinguishable from the 76% increase in low-intensity properties. These properties have generally not been upzoned for additional density – and thus we would not expect to see a big difference between the price indices.

In the full paper we also examine price trends in the ‘Mixed Use Urban’ and ‘Mixed Use Suburban’ zones. We observe patterns that are consistent with upzoning inflating the price of redevelopable properties. Within the Mixed Use Urban zone – which permits up to three storeys – low-intensity properties appreciated by 14.8% more than high-intensity properties over the 2011 to 2015 period. Meanwhile, within the Mixed Use Suburban zone – which only permits up to two storeys – low-intensity properties appreciated by only 2% more, on average, compared to high-intensity properties.

Unfortunately our sample ends in 2015 due to data constraints. But we hope to be able to update these and the other indices in our discussion paper soon – and on an ongoing basis – in order to see whether intensification is bringing affordable housing options to Auckland.

*Ryan Greenaway-McGrevy is a Senior Lecturer in Economics and the Director of the Centre for Applied Research in Economics at the University of Auckland. Kade Sorensen is a PhD candidate at the University of Auckland and recipient of the Kelliher Charitable Trust PhD Scholarship in Economics.

52 Comments

This is a very interesting, and important, piece of research.

However, there are some big research questions that remain, given the sampling finished in 2015, including:

- The final Unitary Plan was MUCH more liberal (development friendly) than the Plan 'as notified' that existed in 2015. What impact will the 'carpet bombing' approach to widespread density in the final Plan have on reducing the potential gains on sites with higher density potential? With the opportunities much less scarce, will that lessen gains in the value of the 'lower intensity, high density zoned' properties?

Thanks Fritz. You are indeed right in that there are some big differences between the various versions of the plan. Although I understand from planners and developers that the height-in-relation-to-boundary restrictions still present a significant obstacle even in the high density zones like TH&A. And there is always the problem of parcel assembly that impacts cost-effective redevelopment. I'd be interested to hear your thoughts on these issues.

Rather than speculate as to what prices have done across the various zones in 2016, I would like to let the data speak. I'm afraid you and I both will have to wait until we can update the indices. That should not be too far away!

"Mixed Use Urban zone – which only permits up to two storeys – low-intensity properties appreciated by only 2% more, on average, compared to high-intensity properties".

I think this should be mixed used suburban.

Yup, you are right. I will see if I can get the article corrected. Thanks!

Thanks Ryan, look forward to seeing the updates.

"Evidently there is a marked divergence in prices across the two groups. High-intensity properties appreciated by 77% between Q1 2011 and Q4 2015, while low-intensity properties appreciated by about 95%. This result is what we would expect if upzoning inflated the redevelopment premium. Within the Terrace Housing and Apartment Zone, low-intensity properties (e.g., the bungalow sitting on a quarter acre) have appreciated by significantly more than high-intensity properties (e.g., apartments and flats). If the AUP is successful, we should expect this divergence to continue."

And that folk's sums up everything you need to know about Auckland planning. The above is as near as you can get to distilling the "logic" of Auckland Council.

Single house prices are a cost factor against redevelopment. Apartment prices are the value realised by redevelopment. Auckland Council makes the costs go up faster than the value, which means it becomes less profitable to construct apartments.

And this is supposed to be a plan to build more apartments.

Here is the logic Auckland Council says will result in lots of apartments being built:

- You have some land on which you can build apartments.

- You borrow $millions and take lots of risk to transform it into a poorer performing asset class.

- You will do this.

I think there might be a slight flaw in the logic.

"One of the stated goals of the Auckland Unitary Plan (AUP) is to restore housing affordability in the city. [And it will be incredibly] easy to tell if it is working [or not]."

Let me explain.

If this is a plan to build lots of apartments, we count the number of apartments built and divide by the number of people. We can compare our numbers to cities of similar size.

I've done this exercise and Auckland does not rank highly.

"High-intensity properties appreciated by 77% between Q1 2011 and Q4 2015, while low-intensity properties appreciated by about 95%."

This result is the I would expect if something deflated the redevelopment "premium". This result is what I expect when the council slashes land supply and inflates the "cost" of land.

What this shows is that between 2011 and 2015 the premium of high intensity over low intensity deflated.

"What this shows is that between 2011 and 2015 the premium of high intensity over low intensity deflated."

How so?

Doesn't RGM argue that up-zoning increased the redevelopment premium exhibited by low intensity property?

'Doesn't RGM argue that up-zoning increased the redevelopment premium?'

He distinguishes between 'high intensity' / 'low intensity' (whether the existing development on a site is intensively developed or not) and 'High Density' / 'Low Density' (it's development potential under the Unitary Plan zonings)

Low Intensity / High Density properties increased in value much more than High Intensity / High Density properties, which is what one would suspect (as the latter are already 'built out' despite their potential under zoning) - but this is great data.

Yes, thanks Fritz.

Sorry, I should of added that differentiation in density.

My point was that OP seemed to be saying that the premium of high intensity was decreasing relative to low intensity.

There is no high intensity premium, though. It's counter-intuitive to think of it that way.

How so?

His own data shows that the cost of acquiring land (low density property) is rising faster than the value of high density property. From 2011 to 2015 the land costs of building an apartment increased faster than the price of an apartment.

The redevelopment premium, the profitability of building apartments, is therefore decreasing.

Redevelopment premium is increasing in the wake of upzoning.

Intensity (or opportunity cost of redevelopment) is decreasing.

Terminology.

So terminology aside.

RGM says Auckland will build more apartments by making sure the cost of land goes up faster than the price of apartments. Which seems crazy, to me.

Are you sure you aren't confusing what the "intensity" specifically refers to in this?

No, seriously the argument RGM makes is that (1) we make land really expensive relative to improvements, (2) we then build lots of apartments (3) the ratio value of high intensity will fall and everything will be good.

How does step 2 work?

Step 2 doesn't work, because Step 1 represents the exact opposite conditions to why people build apartments.

People build apartments to make money, so they want to be pretty confident that the value they are constructing will increase relative to costs.

I think you are still misunderstanding.

The argument is that supply pressure on prices is only going to occur at the top and with high intensity property. The goal is to achieve a greater amount of high intensity property in order to lower property costs. Upzoned low intensity only increases land prices.

Step 2 works because low intensity indicates a low opportunity cost of redevelopment. If you have a sink cost of ownership, you are incentivised to redevelop as intensity ratio decreases.

3 - the intensity ratio of property only increases after redevelopment. It cannot fall, unless the developer is an idiot.

And I am saying that the argument is BS.

Many things impact land prices, these things work in parallel. For instance, Auckland severely constricting land supply for single dwelling housing increases prices. Only if you were to pretend no other mechanisms exist, will the argument make any sense. Which means the argument is BS.

Owning low intensity property in Auckland means having a well performing asset class appreciating in relative value. If you hold onto a single dwelling you gain spectacularly in Auckland. But if you redevelop the property, you lose all of that relative appreciation instead creating a poorly performing asset class. Step 2 means taking the hit of a large and ever increasing opportunity cost.

There is no sink cost of land ownership when land owners can sell easily.

There is however a pertinent sunk cost that applies, the sunk costs of the construction industry (equipment, skills and payroll). But Auckland Council is providing massive exurban sprawls and the construction industry can build profitable single dwelling.

Good to see some rigorous discussion here. Thanks.

> The redevelopment premium, the profitability of building apartments, is therefore decreasing.

But we are looking at upzoned properties, meaning that a developer could not build apartments or terraced housing before the AUP. Prior to the AUP the return to the developer was effectively zero.

Prior to the AUP the return to the developer was effectively zero.

Prior to the AUP upzoning the return to the developer was spectacular.

The return to the developer derived from upzoning was zero, but the return to the developer from all factors was huge.

> Prior to the AUP upzoning the return to the developer was spectacular.

How so? Take a bungalow sitting on 600m2, and for argument's sake suppose that before the AUP it is zoned for one dwelling per 600m2. The return to development is limited by the density restriction. You can pull down the bungalow and build another single dwelling, but the profit from doing so would be minimal (and probably negative).

How so?

Auckland 2011-2016. Put on a fresh coat of paint, wait 12 months and then sell the property for 30% more. The returns on this sort of development are spectacular and not limited to the effects of density restriction. These returns are driven by other factors.

You could use your data to estimate the actual effect of upzoning on prices in Auckland. Instead of restricting your analysis to upzoned areas only, examine the price changes in single dwelling areas and compare to low intensity housing in upzoned areas.

I see. But I cannot agree that a fresh coat of paint constitutes redevelopment. At the very least the structure must be altered in some way, or else a second separate structure built on the parcel. Obviously we are interested in cases where redevelopment results in additional dwellings being built.

As you will see the article (and the full paper), we do not restrict our selves to upzoned areas only. Have a look at the results for single house zones. Low intensity housing in SH appreciated by 76% 2011-2015. Low intensity in THA appreciated by 95%.

EDIT: You'll also note that we are not laying claim to estimating the effect of the AUP on house prices in this paper. That will come in future work. Here we are just interested in house price measurement.

We are all very interested in the cases where building occurs, if we want to make sure building occurs.

If a coat of paint doesn't equal redevelopment and yet offers great returns, then return on non-development is effectively much larger than zero. Your data shows that from 2011-15 the return of non-development (keeping low intensity) was larger than the return on apartments when the choice was available. Auckland built very few apartments between 2011-15, your data is exactly what I expected to have found - it shows building apartments was unprofitable.

But if we assign a value of zero to the profitability of non-development. Then yes, you would conclude based on that adjustment that the AUP will be successful if it continues the trends of 2011-15.

(If you do end up measuring the effects of upsizing, try comparing upzoned areas to adjacent non-upzoned areas. Using all SH areas, will skew appreciation lower by including the remote suburbs.)

I think you need to read the article, again.

What you are trying to say is that the data shows something which is impossible for it to represent - that people didn't redevelop.

Note: the AUP was only finalised in late 2016. The ability to redevelop was not possible until then. This article examines the impact that the AUP signal had on properties relative to their up-zoning potential and intensity measure.

The ability to redevelop was possible 2010-2015, in quite a bit of Auckland. Auckland 2010-2015 was less constrained in that period than Brisbane. Brisbane built way more apartments than Auckland.

Evidently there is a marked divergence in prices across the two groups. High-intensity properties appreciated by 77% between Q1 2011 and Q4 2015, while low-intensity properties appreciated by about 95%. This result is what we would expect if upzoning inflated the redevelopment premium. Within the Terrace Housing and Apartment Zone, low-intensity properties (e.g., the bungalow sitting on a quarter acre) have appreciated by significantly more than high-intensity properties (e.g., apartments and flats).

Unfortunately this is also the result we would expect if Auckland's land supply constraints have inflated land costs.

The article has used all of Auckland SH zone data to suggest that land price appreciation has not occurred in Auckland. I think this is flawed, because lots of SH zones in Auckland are subject to land over supply (Warkworth, Orewa, Beachlands, Kumeu, Pukekohe) and I am of the opinion that Ponsonby (SH zone) out performed city apartments 2011-15 by a very big margin.

> The article has used all of Auckland SH zone data to suggest that land price appreciation has not occurred in Auckland

Again, I am not sure how you came to that conclusion. The article does not suggest that there has been no land price appreciation. It shows the opposite. (Low intensity housing being more similar to undeveloped land than high intensity housing.)

"High-intensity properties in this [SH] zone appreciated by 74% over the five-year period, which is qualitatively indistinguishable from the 76% increase in low-intensity properties. These properties have generally not been upzoned for additional density – and thus we would not expect to see a big difference between the price indices."

I think Auckland City is under supplied with land and a significant difference in these price indices should exist in Auckland City, but the article states there is not a significant difference. My personal experience and the data seemingly disagree.

But I also think the Auckland Region is over supplied with land supply, because Phil Goff is building so much exurban sprawl. So therefore these indices measured over the wider Auckland Region could be anything.

But the SH group accounts for only roughly 15% of transactions for the period.

In the full paper you will see indices sorted only on high and low intensity (not sorted by residential zone). There you will see that across the city, LI properties gained relative to HI properties.

There is a lot here; I will reply point-by-point:

> Your data shows that from 2011-15 the return of non-development (keeping low intensity) was larger than the return on apartments when the choice was available.

The price indices cannot tell us whether keeping low intensity offered a higher return than tearing-down and building a block of apartments or terraced housing (assuming that was possible).

> your data is exactly what I expected to have found - it shows building apartments was unprofitable.

As per above, the price indices cannot tell us about profitability of building apartments (or flats, units, terraced housing) at all. I am not sure how you came to that conclusion.

> (If you do end up measuring the effects of upsizing, try comparing upzoned areas to adjacent non-upzoned areas. Using all SH areas, will skew appreciation lower by including the remote suburbs.)

Thanks. We can (and do) control for a variety of factors including distance to CBD, suburb income, etc.

Why can't I use the indices to estimate relative profitability of building apartments?

The cost of single housing (low intensity) + all other building expenses = cost of producing an apartment block.

Price of apartment block (high intensity) - cost of apartment block = profit.

Assume for extreme simplicity all other building expenses are held constant and assign a value of x = 0.

2011: high intensity = 1; low intensity = 1. Profitability = 1 – 1 = 0.

2015: high intensity = 1.77; low intensity = 1.95 Profitability = 1.77 – 1.95 = -0.18.

The price indices only tell you about relative price changes within each group - you cannot use the price indices to compare price levels across the two groups

I am aware of how the price level compares between the two groups and I assume you are as well.

So yeah, if apartments were priced higher than centrally located single dwellings then my assertion on profitability would be dubious. But they aren't, so lets move on.

We're seeing a significant cost go up faster than apartment sale prices. If the profits of building apartments get squeezed, Auckland builds less apartments.

But apartments (or whatever higher-density dwelling one might have in mind) do not have to be priced higher than stand alone dwellings for redevelopment to be profitable. You pull down the house and build X new dwellings in its place. The comparison you should make is to X times the apartment price - not the average price for a single apartment.

And, of course, that figure X just increased. That is why you can't use the price indices to back out changes in profitability over time either.

Yes I agree - the figure X increases. The required critical value of X increases as the cost of land has goes up faster than the sale price of apartments. A progression which reduces profitability on ever larger numbers of potential redevelopments.

Therefore if the AUP was changed to make sure the divergence reversed, all apartment building would be unambiguously more profitable and the critical value of X would fall making a wider range of redevelopment profitable.

BTW - there is a comment down below that concerns value of apartments, which I would like your opinion on.

One of the interesting quirks to me in the AUP is that in some cases it encouraged Single house zone properties up-zoned to Mixed Use Suburban to expand the existing site coverage with extensions, rather than subdivide, thereby actively working against the property being subdivided anytime soon based on the sunk cost.

Another interesting facet was that the Council must have know how many properties were 800m2 or above and therefore subdividable into two at 400m2 each. Upzoning properties smaller than that seems relatively pointless if consent is required. Another barrier to a developer.

If anyone is interested the "other thing" the AUP does is mostly constricting suburban land supplies from Auckland City in favour of building much bigger exurbs miles away. So Auckland can have a much longer and more polluting commute.

Edit: RGM - this comment has been re-edited to remove a rehashing of the other thread.

Meanwhile, existing high-intensity housing that has been upzoned should not increase in value, and, over time, should decline in value if intensification brings additional construction of high-intensity housing to the market. Think about an apartment block on Mt Eden Road that has just been upzoned under the AUP. The apartment block already is the kind of housing that the plan is designed to encourage, and it makes little sense to redevelop the site. The redevelopment premium embedded in this kind of property should therefore be rather small. And if the zoning changes encourage construction of more high-intensity housing, the apartments within the block should also decline in value (at least relative to price trends in the rest of the housing market).

[...]Apartments derive their value largely from their close proximity to jobs and amenities and people. This is called agglomeration value and is the reason we have cities. If a city builds lots of office space and apartments, then businesses move in with lots of jobs and more people crowd into the city - the value of central apartments goes up relative to the rest of the city. This trend continues until an oversupply of apartments is reached, in a typical boom/bust fashion. When an apartment block/office space is built next to an apartment block in Mt Eden the utility value of the existing apartments goes up more than the rarity value decreases.

[...] Auckland creates massive areas of disconnected sprawl far away from apartments to destroy the value of apartments - central living apartment dwellers cannot access these areas jobs and so the utility value of apartments falls.

I agree regarding your points on utility value and the benefits of agglomeration. But there is a difference between utility value and price - my use of 'value' in the quote refers to price.

I would argue that we need an abundant supply of apartments (and other forms of high/medium density housing) so that workers - not dwelling owners - capture the productivity gains from agglomeration. When agglomeration productivities are capitalized into housing costs it discourages further agglomeration since it increases the cost of living. Households that would have moved to AKL do not because real incomes are higher elsewhere. Other households out-migrate for the same reason.

I agree regarding the problem of over-capitalisation having a detrimental impact on future migration inflows. (This is my second biggest concern about Auckland, after the pollution aspect.) However the problem is not housing, it is land. Really the same logic that applies to households moving into and out of Auckland applies to construction investment capital, if the costs are too high in Auckland then real construction incomes are much higher elsewhere.

People can live and work in apartments. Apartment pricing going up at a rapid rate encourages people to build more apartments. Prices represent speculated expected agglomeration value over the life of the apartment. Current utility value might be low, but there is an expectation that much more development will pour into the area and lift future utility. (This price is not the same as rent, rent should indeed be kept attractively low to attract people in their 20s.)

The problem is land, which is never anything more than a cost.

Apartment price appreciation in excess of land cost appreciation is the sign of a healthy city. Melbourne and Brisbane have this, they build apartments 300% - 400% faster than Auckland.

Interesting. btw the THAB zone does not permit 7-8 stories. The height is 16m so 5 stories is standard (with increased heights only in some overlay areas).

The big difference we are finding in feasibility is between zones that have a density limit and zones that don't. When there is a density limit land cost is the big factor and so houses tend to be big (construction price not so important). When there is no density limit construction price becomes important, land cost less so, and so houses tend to be smaller. So over time would expect the AUP to provide cheaper housing choices as well as the choice of more expensive larger dwellings.

Thanks Bob. You are right. Although I could have said something along the lines of "up to seven or eight storeys", since 19.5m to 22.5m is permitted in specific localities. I will see if it can be corrected.

Your work sounds very interesting, and makes intuitive sense. Best to maximise floor space if you cannot build a second dwelling.

Ryan what if there was a superabundance of intensification opportunities? What if every single Auckland residential/commercial plot had the right to say triple or more its built space? Would that increase the property value of those plots? Wouldn't competition from this superabundant supply push down the cost of intensification to its true construction marginal cost?

Isn't that the lesson from economists like Edward Glaeser? This is discussed as part of the article here. https://medium.com/land-buildings-identity-and-values/what-is-the-true-…

Also there is a good discussion about housing by Michael Reddell at Croaking Cassandra today -here.

https://croakingcassandra.com/2017/11/01/making-progress-on-housing/

Hi Brendan:

I agree that increased competition would push down the redevelopment premium. But even if all density restrictions were removed, I do not think that we would reach a point of superabundance (in which the redevelopment premium was zero), because the amenities embedded in land in different locations are very heterogenous. Some land is close to downtown, other land is not. Some land is close to the beach with a nice view etc., other land is not. That kind of heterogeneity in land is sufficient to generate a development premium - even without land use regulation and competition between land owners. See Graeme Guthrie's paper here for more on this issue:

https://ideas.repec.org/a/eee/juecon/v68y2010i1p56-71.html

Although it deals with development - not redevelopment - the logic still applies.

Ryan I cannot open the Guthrie paper because I am poor nurse..... But sure I agree that there will always be amenity price curves within cities. Sure land is heterogenous and this gives some landowners some pricing power. The question is how much pricing power does upzoning give landowners. Does a little upzoning like the Unitary Plan give a lot, but if upzoning had been many times that magnitude the pricing power would be less?

It is late and I am tired -so will not look up the real figures -but from memory the Unitary Plan is staged and at its maximum timeframe -400,000 extra residential units is possible -much of that greenfield growth. There are already about 500,000 built residential plots in Auckland so this is less than double at its maximum potential.

Whereas in my article which I linked the actual amount that inner Tokyo expanded its built environment is almost 300% in the last 55 years and there is clearly the potential for further upward expansion. In recent decades Tokyo has done this affordably. https://medium.com/land-buildings-identity-and-values/what-is-the-secre…

Thanks Brendan. We are in broad agreement here: More upzoning = lesser premium for the upzoned.

I am aware of the figures that have come out of the various capacity for growth studies. But despite such apparent capacity in Auckland - even before the AUP - we still have sky high prices. I am inclined to think that much of that spare capacity was extremely costly to bring online under pre-AUP

Ryan it is later and I am still tired......but your paper is probably onto something (I haven't read your original article in full)...... increasing the intensification potential of a city may split the urban property market and some existing landowners/housing with intensification possibilities will go up in value (how much depending on competition) even as more affordable housing comes on stream which pushes down the value of some other housing stock which do not have the same intensification possibilities. Is that what you are saying? If so, this is an important point -because it means more affordable housing supply doesn't necessary mean all existing households are worse off.

Yes! You got it. I have made this point before I had the data to show it:

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=116…

Ryan it is later again (had short nap) woke thinking about your article. If the number/proportion of low intensity houses with greater potential value uplift increased then more existing home owners would support affordable housing supply initiatives and the whole affordable housing issue would be less controversial.

I have a proposal that would greatly increase the number of low intensity houses that would have intensification/development potential by creating a right for neighbouring properties to waiver their common boundary setback and shade plane restrictions -if both parties agree.

The last government made some steps to legalise that -with an amendment to the RMA, which came into power in October. I think the idea could be promoted more and streamlined -Ryan what do you think?

Peter Nunns the economist who writes for Greater Auckland did a write-up on it in August. https://www.greaterauckland.org.nz/2017/08/29/legalising-perimeter-bloc…

That sounds like a great proposal. And I do remember this post ... Must read again. Thanks!

Peter is great, BTW.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.