Well, it's been the great problem for a little while now.

How do you get anything like a decent return on a little nest egg you are stashing away in a time when 'conventional' investments such as bank term deposits are paying much less than they did?

Now the coronavirus has provided a two punch blow to even this poor state of affairs.

First, it's knocked the super low interest rates even lower as central banks around the globe struggle to pump liquidity and life into the financial system.

And second, it's got us all worried about job security and whether we'll even have a nest egg to be gathering interest.

At a time when money in the bank has been a safe but not spectacular source of earnings, shares have offered some great results in recent years, both in terms of capital growth and strong dividends.

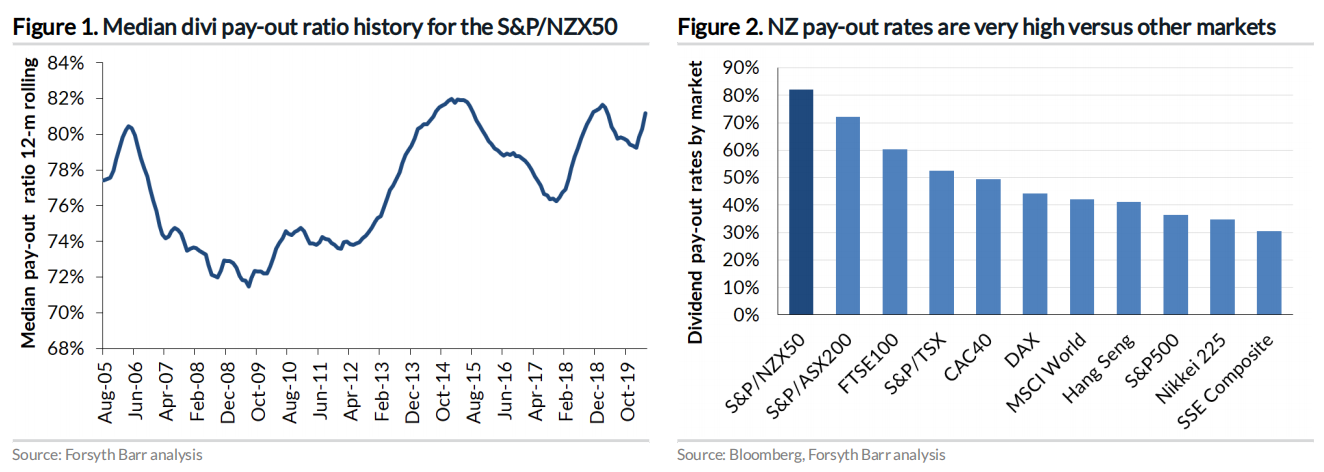

In fact as Forsyth Barr analysts Andy Bowley and Matthew Leach have highlighted in a recent report the dividend payout ratios for New Zealand companies - how much of the profit is paid to shareholders as dividends - have been getting right up there by international standards.

But the virus will have a say there too. In fact the analysts have titled their report: "The dividend hit has only just started".

"Over the past 10 years median pay-out ratios for the NZX50 have climbed from the low 70s [percent] to the low 80s," they say.

"We accept that compositional changes [in the NZX50 Index] have occurred but even taking into account new arrivals and share market departures, the same trend is visible. Pay-out ratios have increased - but similar to what was observed through the GFC are now set to decline sharply."

They've produced the below graphs, which show that NZ companies have indeed been paying out big portions of their profits relative to counterparts in other countries.

Bowley and Leach say the "host of dividend suspensions" recently seen from companies that reported results in February reflected cash preservation for companies exposed to Covid-19 and sets the scene for further suspensions over the next 12 months.

They say the "politics of dividend distribution" will heavily influence how corporates navigate capital management decisions as a result of Covid-19.

"In an environment where workers are being made redundant or being paid only a proportion of wages, where government's are providing wage subsidies, and where supplier contractual relief is happening, distributions to shareholders will need to be carefully considered by boards."

Consequently the analysts say that even as profits shrink, so will the portion of them being paid out as dividends be reduced.

"We expect pay-out ratios to fall from recent elevated levels. Investors will likely receive less income for the foreseeable future," they say.

They go on to say though that with lower bond rates and changes to bank funding requirements leading to still lower term deposit rates, dividends dividends that are paid will be highly valued by "yield thirsty investors".

"This theme is, therefore, supportive to those dividend payers with relative Covid-19 immunity — in particular, utilities (Contact, Genesis, Meridian, Mercury, Trustpower, Vector) and telcos (Chorus, Spark)."

And as a parting shot the analysts say that companies that effectively balance the social good over shareholder distributions and profits will better navigate COVID-19 than those that don't.

"This may mean a greater impact than otherwise on near term profitability, but good corporate citizenship will likely have a longer lasting impact on labour productivity/retention, customer/brand loyalty and supplier relationships."

81 Comments

neoliberal creators, contributors, protectors in this crash movie are easily identified, mostly males & always advises/act to socialise the private debt loss, they purposely created a program 'without' undo button - NZ, wake up!:

https://www.scoop.co.nz/stories/HL1507/S00101/the-fire-economy-new-zeal…

If you want a dividend, get off your bum and earn it.

Been there, done that, saved and invested some of it instead of burning it on lifestyle.

That path is only available in times of growth, quite a lot of it, actually. When growth goes out the window, then so does passive income, which while not a great outcome for some, it is for the planet.

There is always a chance to make money in both up and down cycles. It is how fast you can see it and capitalize on it.

Correct but look outside NZX as it is overvalued and picked clean being so small.

The ASX has plenty of options that have plenty potential.

The gold mining stocks took a big hit a few weeks back but still plenty upside if Aud Usd stays low as gold sitting 1700usd this week.

NZX needs some new blood like when Xero A2M DIL listed they had a big potential.

I would be in in a flash and most likely many others if some new blood shows me a real potential listing that is thinking outside the box in this new world.

There have been sizable gains since late march as shares were incredibly oversold. Example Ryman 6.50 and retailers 25 percent of previous highs. I recall you warning people to stay out as they were fodder "for day traders". This morning's business report highlighted there would be fresh buying interest this week at current levels.

Week on Demand - NewstalkZB

https://www.newstalkzb.co.nz/on-demand/week-on-demand/

Very brave buying at moment on NZX as we are still trading above Jan 2019 levels but look at what is happening around the world.

Yes buy the dips but be very careful as this could easily drop back down 40 percent from here over next 6-12months.

I have been buying but also just as quick getting back out as prices are just heading back to over bought in my view quick profits.

This sort of market is great when like you say RYM got smashed down but I still believe most stocks have a long way to go.

How about MET that is showing the big boys know the risks are very high now versus values.

If this is the bottom then the markets are no longer healthy in my view and we now live in a world full of zombie companies (thanks FED) for buying nearly everything in the states to keep bubble going.

Impt to make selective choices. As the article said the directors have to balance shareholder returns with other stakeholders and apportion the pie accordingly or at least watch out for wrong perceptions. KPG kiwi property is probably a good example, if commercial tenants are struggling to stay afloat kpg would be very stupid to ignore their genuine pleas.

But the whole idea of the path to wealth is to take money, park it somewhere and expect great returns through the exploitation of others without getting off your bum.

Can't the Marxists, who aren't interested in having a prosperous economy or lives free of the state, go find their own site. Perhaps one of you set up an instagram or something, where you can all share pictures of the show trials and food queues in Soviet Russia, back in the good old days when you didn't have to think (until the KGB came knocking).

I can't wait to all the school kids go back and leave these forums alone.

Did the Easter Bunny piss in your Crispy Crunchy Granola this morning?

Anyway, what's a billion here or there of taxpayer money to bail out capitalism, for prosperity's sake of course. The name Allan Hubbard is one that comes to mind, no relation of course?

So what if he is a relative?

No relation. But of course ad hominem is your next comment.

To the Editor: we all make our choices. I'm not interested in posting here with comments like these. It's like playschool and it serves no purpose useful to me.

Keep up the good work, but I'm out. I'll keep my commenting to NBR (ironically, I didn't use to hold with their moderation policy, but at least you can have a grown-up discussion on there).

... My last post not to you Middleman, but that NZDan troll account.

Actually, to the Editor: get a policy of only posting under your name on here and I'm back. Part of the problem is these troll accounts hiding behind pseudonyms.

That stance suggests you're missing a lot of the value the internet can provide. I've been on NBR comment threads plenty. I often found them more likely to devolve into ad hominem when people were clearly identifiable, rather than statements being debated for their actual worth distinct from that of the person.

Mark decries Ad Hom attacks yet his comments on this article are full of them. It's no wonder he's an advocate for removal of monikers, probably the sort to Facebook stalk anyone he enters a debate with.

No. You’re truly evil, matey. And proving everything i’ve said about you.

I thought you were leaving. Reminds me of the time, i would have been 6 or 7 years old. I told my mum I was running away because I didn't get my way, so I packed my school bag with a sweatshirt and a packet of Super Wine biscuits and hid in the bushes at the end of the driveway waiting for mum to come look for me.

This is annoying me enough to change my mind.

Why are you here?

I enjoy the content, joined when I was looking to purchase my first home a couple of years back as I stumbled across the site when I was reading up on a few things. There's quite a polarising mix of commentators on this website that makes the comments section quite entertaining at times.

Your first comment worth making.

Not everyone who disagrees with your extreme right wing strawman rantings is a troll.

I’m not right wing. I’m classical liberal.

How did all you communists end up on a site that celebrates business, freedom and living? You are by definition trolls on this site.

Again, to editor: moderate or no posting anonymously.

Because I have a bootstrapped small business and am an investor. I was 90% in cash before the crash because markets were obviously a bubble, sorry you didn't see it, but the fact you didn't see it doesn't mean Nzdan = Stalin for taking the mickey out of the poisonous NZ rentier culture. But by all means pack up your bat and ball and go home because there is an educated younger cohort on this site who don't agree with you. After all nothing says democracy like screaming for censorship of opposing viewpoints.

I have no shares other than shorts, for three years now. Read my comments re command econ central bank stimulunacy.

You don’t believe in democracy because you don’t believe in free markets. The owners of this site have every right to moderate to enhance comments; it’s their private property... not a censorship issue.

Poisonous rentier culture? It’s just the market.

Why are you here if you hate capitalism so much?

Free markets good, freedom of speech bad. Got it.

The free market sure is making short work of this virus huh?

Engaging you is clearly not productive (remember productivity?), I'll leave you to continue ranting into the wind.

There’s no freedom of speech issue with a private site moderating their own content. Think it through.

Re the virus, with the Soviet styled command agency of central banks destroying free market price discovery, we have no free market. Not for a long time. Financial markets are broken because of it; that’s why I am only short on shares. If we had free markets (and lives free of the state), our economies could have weathered this relatively easily.

I don’t understand why you are here, other than to destroy someone else’s work.

WTF has central banking got to do with epidemiology?

Let me try to untangle the madness here, do you think if the central banks weren't manipulating the economy the private sector would have developed a cure/vaccine already? Is that actually what you're trying to argue?

You have absolutely no connection to reality right now.

I’m not saying that at all. The world would not have been drowning in a sea of debt.

What part of reality do you think negative interest rates inform?

You figure it out.

Hear hear!

Interest.co.nz is publishing some great articles that generate interest in debating the points made but the comments section is woeful. It has become an echo chamber for economic incels that want to see the downfall of a group of society, presumably so they can take their place. There is no incentive to pay for access. If it were my business I would only offer commenting access to paying subscribers and I would actively moderate the section. It might get more views with whack-a-mole threads having protagonists go toe to toe, but there’s an awful lot of dross to wade through. Are you a serious business site or an entertainment option for a select group of incels? I don’t think the latter will pay the bills.

Noted Mark but I hope your withdrawal intention was heat of the moment and you'll revisit it. I value your from the shoulder contributions.

And your comment regarding "school kids" wasn't Ad Hom? You don't have to agree with other people's comments, if you're going to throw a tantrum and leave the website please do it quietly. I'm sure the Ed has better things to do than pander to your emotions.

If you want to conduct yourself in the manner of a school kid who has just found socialism and is scornful of all other view points, and you can only make infantile quips and disparagement in comments from anonymity around those of us invested in markets, and worried rightly now, then it's just being called out. You add nothing to these threads; you obviously have no skin in the markets.

So my point remains. I will be commenting on no other posts until Interest.co.nz either moderates or goes to name only accounts, no anonymous posting from trolls.

A good opportunity to take some time out and do a little soul searching. It's quite obvious that you're under a lot of stress, given your unwarranted outburst at a flippant comment not even directed at you. Try being a little introspective before you start calling others "school kids". We've all got skin in this game.

To make your comment at 11.12am, and to post anonymously, I don't believe you. You have no skin in the investment markets other than perhaps your Kiwisaver. It's the nihilist level and pointless tone of all the socialist comments on these posts that I find unfathomable: I guess it's a sign of how utterly broken the free world is, and financial markets, under the central banked command economy that has destroyed the price discovery of free markets, thus share valuations which have no connection at all to fundamentals, and a business site's comments which is filled with socialists and communists who despise free market capitalism anyway, and the free individual lives they, and only they, support. For your comments you have to believe in a huge state to control all aspects of life and no doubt subsistence living via a UBI paid by taxes that make no recovery possible (which is well on the way). Actually, re that last point, since the draconian AML was forced on us, and I ceased to be able to beat inflation with prudent investments thanks to central bank stimulunacy turning every asset class toxic, I realised you big staters - in the cold war we called you useful idiots (fact not ad hom) - won some time ago.

For people like me, we are dinosaurs that got to live in a much better age when free markets and free lives seemed a possibility. All gone.

As :) am I from this thread, and these comments (until anonymous accounts go). Enjoy laying waste to every thread you touch with your cynical poison.

Weird flex but okay. Does it feel better to get that all off your chest? I'm happy to be an "e-punching bag" for you to release your frustrations on, no hard feelings.

Should have invested in houses.....

Level of skin in the game is not determined by how much money you're losing.

I made money on the post Feb 24 share correction, shorts and treasuries, and will do so when share markets leave the suckers rally - now I think - and correct a further 30% ASX and NZX; 60% US indices.

You do not have to be a Marxist to understand that you cannot have never ending growth in a finite world, and it is growth that provides passive income.

Nonsense.

You've left out the most important capital: a human mind.

As long as there are productivity gains via smarter ways to do things, technology gains, etc, there can be growth in a finite world.

That said, I am a strong proponent of a sustainable economy, and a sustainable society. We need to shun and penalize people that have more than two children (okay, maybe have a lottery to choose the tenth female that gets to bring up the average to the required 2.1 per family).

I am looking for return OF capital, not return on capital. I've saved enough of my hard earned income to live the rest of my days on this saved funds unless massive inflation returns.. The large majority of this is put into term deposits, which barely returns enough to meet inflation. I am okay with that. I'd prefer that reserve banks targeted 0% inflation instead of devaluing my savings every year, but I have to live within the current reality of imprudent spending (on both the government as well as consumer level).

Regarding your last para Yankiwi that's me also, although in frustration (as opposed to desperation) seven months ago put some - not fatal - portion of savings in an unlisted commercial property fund, just to get a yield. Learned a quick lesson there. I do resent this command system we have exists to whack prudence (aka the elderly) every turn, while feeding speculation (ie, asset bubbles).

Waiting for the real correction to sharemarkets, which have in no way at all priced in this crisis (earnings collapse) despite it's the biggest economic crisis we will probably go through, then I may put 15% of savings (outside house) back into shares; but that's months off.

Overall the NZX50 was down 15 to 20 percent. Some stocks kept the index artificially high and others (am thinking retailers) were smashed. Recovery has started

There's a worldwide earnings collapse and depression coming (here): NZX and certainly all the US share indexes have none of it priced in. US is on historically high share valuations with 17 million peeps unemployed in 3 weeks. ... Nothing makes sense, because the Fed is totally down a rabbit hole, indeed, worse, since by proxy buying corporate junk debt last week, is physically dismantling free market capitalism. Next stop will be a Soviet styled collapse. And I mean that.

Well I hope you're wrong in relation to nz. The thing I have noticed is that nz inc keeps coming through despite the odds. Early 90s recession was a tough one indeed but largely companies and individuals were left to fend for themselves. Todays episode of tipping point the winner is spending her prize on an airticket here. I know the episode is out of date but the effect is representative. Nz is so small that only a small upswing can have a disproportionate effect.

Completely agree. How do you determine the price of something if you have no idea what company earnings are going to be, nor what discount rate should be used. Both variables could signficantly alter the value of share prices. I'm leaning towards the idea that we've just witnessed the opening act, the main show is yet to start.

Dp

do resent this command system we have exists to whack prudence (aka the elderly) every turn, while feeding speculation (ie, asset bubbles).

Absolutely. The problem is we seem to only have political parties who are keen to keep doing this. ACT is now the Epsom Homeowners / Investors Association, National were feeding and encouraging the bubble, and Labour have not yet shown any inkling to reverse this course.

Selling down assets might be the only way boomers can afford retirement.

Yep, I think you are on the money there. Most of we boomers will have no option and if, as some forecasters are predicting, part of the cost of C19 QE will have to be paid through increased taxation and means testing of NZ super the incentive to consume capital will ratchet up strongly.

About 1990 I researched just what the population relative ages were in the US, and made some basic projections about what would happen when the boomers started retiring in large numbers (back then they were baby boomers, before the phrase was shortened and redefined as a pejorative). My conclusion was that there would be an asset valuation peak around 2007. Yes, I am serious about making this long term projection so far in advance... Went to cash in 2007, and sold the house and started renting in late 2006. Turned out that both moves were highly appropriate... didn't expect the moral hazard behavior of Bernanke and the long term asset inflation effects of QE though... should have thought that one through a bit better!

Well done on your foresight. As you observe with your Bernanke comment, had you bought back in to equities and housing during the early part of 2009 you'd be significantly better off than staying in cash (assuming that's what you did) , even after the current 20% equity market drop. I was also in cash by late 2008 apart from the house but waded back in over march 2009. I pretend I had your prescience but blind faith was as much my guide. The market would have to drop by multiples more for my portfolio value to fall below 2009. Who knows, it could but I'm a long term highly defensive investor and will ride it out.

I think the dividend suspensions are the right move in the near term, however once trading gets back under way it might suprise more than a few of us just how quickly the majority of listed companies actually reinstate dividends once the smoke clears...I have to say I have been stunned by how kathmandu's share price has collapsed, I noticed Rod Duke did not partake in the recent capital raising exercise either...

But is Rod Duke's non participation because he thinks Kathmandu is a poor prospect or because he doesn't have the money to spare. Briscoes for all we know is haemorrhaging cash. Rod Duke's holding in Kamthamdu dropped from 16.290% to 7.953%. Currently I'm more inclined to think that Briscoe's is just conserving cash.

http://nzx-prod-s7fsd7f98s.s3-website-ap-southeast-2.amazonaws.com/atta…

http://nzx-prod-s7fsd7f98s.s3-website-ap-southeast-2.amazonaws.com/atta…

Briscoes were part of my portfolio a few years back and they are flush with cash and virtually debt free. They will survive. Kathmandoo will not. My intuition tells me Duke is sitting back to wait for a few bargain priced businesses to fall into his lap and he has always wanted Kathmandu, but only at the right price, they were definitely over valued and I think the right price has been discovered. I held Kathmandu briefly a few years back also but was appalled at the leadership teams inability to improve the companies direction so dropped them before things really fell through the floor. The current leadership have gone round in slightly less diminishing circles but the gig is well and truly up for them now. It will be interesting to see how Hallenstein Glassons fares as well...

Looking at the most recent annual report for Hallensteins doesn't indicate any long term debt or non-current liabilities. Similarly for Briscoes. Kathmandu are a different kettle of fish.

Yeah agree, I wasn't putting H&G in the naughty corner with Kathmando, just wondering how they will fare as things move along.

KMD is facing onslaught fromMacpac https://www.mountainwarehouse.com/nz/ plus Decathlon Australia was shipping here but are now opening dedicated website for NZ.

https://help.decathlon.com.au/support/solutions/articles/8000057135-del…

I used to support KMD but last few items fell to pieces in a year.

They will in my eyes struggle big time as they have failed to innovate/adjust to markets.

People are going to be a lot tighter when spending resumes and they will burn through the CR in no time.

Given how high our payout ratio is relative to other countries, why isn't consideration given to reducing it, and increasing worker pay instead of dividends to investors? And by worker pay, I don't mean company boards/executive - I mean general staff.

To me, its just another sign that the current form of capitalism need to be tweaked a bit (share buy backs anyone...who do they benefit...). Motivated and engaged staff are more important to the company than investors who will come and go - your staff are your business and future earnings - not a random investor. Too much focus on share prices and not staff/performance/engagement/motivation.

The share of the net of tax return going to labour relative to capital owners has been stable to improving over recent times. The support of NZs equity market is in large part due to its high dividend ratio payout. Under your proposal for regulation of the shareholder ppn it would degrade from its current thin status to deep emaciation as capital flees to other markets.

Perhaps comes down our whole concept of capitalism and who we want to protect/benefit going forward. If having a high share price is the goal then great - if its making our system more sustainable and benefiting the workers (and that will have flow on effects for our society as well don't forget) - more evenly distributing the pie - then I think it should be considered.

Are we not protecting the workers via working for families and rental subsidies.

Benefiting the investors via large profits so subsidizing them.

Then people wonder why the system is failing.

https://www.odt.co.nz/business/pay-unfair-scott-workers-claim

Just who are the bludgers?

My point is that if companies paid their staff better - instead of having higher payout ratios in terms of dividends and director/management wages (remember the ratio of CEO pay to average worker is becoming further distorted over time), then there would be less reliance on the need for government to provide assistance to average workers. Its just another sign to me that capitalism - as we know it - is broken and needs reform.

There's two aspect of investing (as we all know):

(1) Return On your investment, and

(2) Return Of your investment.

Whilst Number 1 may have occupied our minds until last month Number 2 certainly should now. Further,

The Return On you Investment also comes in two parts;

(a) How much more is it worth nominally than when I took is out? (Principal + Interest, say), and

(b) What can that returned investment now buy me compared to when I invested it? ( Real return)

Getting 0% on your Term Deposit is still a positive 'return' if what you can buy costs less than what it did as inception.

THAT is where the value of investments is likely to come from in the near future - from Deflation. And that...is what lower and lower interest rates has been telling us, all along.

Exactly last few years I have been waiting for collapse and scratching my head thinking why are people paying such a premium for 4-5 percent dividend when the shareprices had boomed so much that they may drop 30-60 percent.

Same as buying rentals hoping from capitals gains and rent money to go up very risky.

Now its collapsed. And by huge percentages in many cases. Those stocks including tourism focused are recovering. We know that tourism is facing a very uncertain future but what about others such as restaurant brands (kfc etc)

I checked out of RBD Dec last year - purchased in 2014. Was becoming too good to be true. Can't remember what the P/E was at that point - perhaps 50-60.

Looks like its around 37 at the moment, but guessing earnings will drop. Still very elevated (in my opinion).

FPH had a P/E of around 60 or 70 when I last looked. Wouldn't be surprised to see that fall at some point (price that is).

Have you looked at the work Robert Shiller did/does around the CAPE?

Thanks but I have seen his name mentioned here on interest.co numerous times by (mainly) dgm commentators extolling him which leads me to think it's not the sort of toff I would bother with. As I didnt get where I am today without a dose of realism mixed with practicality. Not long winded intellectualists only interested in impressing people. Please tell me I am wrong.

"By the summer of 1919, the flu pandemic came to an end, as those that were infected either died or developed immunity."

Without a vaccine, which there may never be, dividends may be a few years off. Slowing immunity by flattening the curve is good short term but prolongs the effects of the virus.

Things might change for many Boomers with No Dividend, No Interest on Fixed Deposit, No Capital Gain.............

Things are going to change have changed for all of us. The year we were all born in doesn't matter now ( if it ever did).

At the risk of repetition, the only thing we all have to decide is, "What happens next?"

Clinging onto 'what was' isn't going to help.

Said on another thread. not for profit involvement I had recommended having 3 months gross expenses in reserves at all times. All income ceases you have 3 months covered to work out a plan or wind up orderly.

That was the advice of accountants to that volunteer org , maybe it applies to for profits too before dividends are paid. Hoping they applied it to their business advice too.

Totally agree..or hold at least 3 months 80% overheads. Maybe IRD should look into that hold in trust...as taxpayer fitting bill this time.

When I started my business (bootstrapped) my first priority was a self-insurance cash account of 6x monthly expenses, ie the business could run on $0 revenue for 6 months if required. Took tuna-and-rice level personal salary out until that was in place.

To conventional wisdom that would have looked like a paranoid, massively over-conservative performance drag. All my competitors were borrowing and deficit spending their way to growth hand over fist. Now it will probably make me the last man standing in my industry. If it were general practice, we would have a smaller but infinitely more robust economy right now.

NFPs generally cannot borrow any money. As the name suggest though, they do not care about financial return so who cares if they have piles of money sitting in the bank returning nothing.

A for profit entity needs to use every dollar they have to return profit. Most of the for profit entities use debt to achieve better return as equity is the most expensive form of capital. There are exceptions to this capital structure formula though, if my memory is right, Apple does not have any debts. But the point remains, if you have even a rather low % of your total capital from debt (lets say 20%), you would struggle to keep 3 month worth of money sitting idle. Investing in anything (as the current situation clearly shows) is pointless as on a rainy day liquidity goes out of wack and you get a significant hit. The for profit entities are better off closing down their shops and go home (as they motive is to make money as opposed to NFPs). The sad consequence of that though is many people will lose their jobs and income.

I liked every F.I.RE economy contributors enthusiasm in NZ: (any ones from RE, painted future upbeat drum)

https://www.stuff.co.nz/life-style/homed/residential/120987250/coronavi…

Except: something just stop, 'no demand' - no people movement from China?=no capital out. Airlines, Tourist, hospitality, education, resto/hotel/motel, 'migrants'. Easy money from Far East surely Not to distort RE in Africa, India.. Noo, it's competing it's way into OECDs: UK, OZ, NZ, Canada, US.. wonder why?

Keen Observer (KO) The nz and world economies are DEAD, KOed. Is that what you want to hear? Investments in the future will involve looking for value, how is that different from the past?

Actually, as a shareholder, I'd anticipate that in the medium to long term lower interest rates will prompt companies to increase the rate of financial engineering. The temptation to artificially inflate earnings by concentrating risk is too great for most executives because that is the path to self enrichment.

The exception may be banks, they have accrued a higher level of risk and the margins available on lending portfolios is in decline. It is unlikely that consolidation will be permitted so I expect a prolonged period of cost cutting, risk unloading and revenue diversification will commence immediately. It is essential for their survival.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.