New Zealand is one of the most “trusted” countries in the world with estimates of at least 500,000 trusts in a population of just five million.

Trusts are one of the most flexible asset ownership vehicles that we have, and while there are good reasons for many of the trusts in New Zealand, a large proportion of them are more than likely not needed.

Trusts have been around since the days of the Crusades in the middle ages. The knight would go off to fight in the crusades, not sure whether he would return, so would leave his estate in the hands of his neighbour to hold the property in trust for his wife, children and future generations – a worthy reason to have a trust relationship.

Trusts really began to take off in New Zealand in the 1980s and 1990s. Back then we had estate duty, meaning that if you died, depending on your wealth, a proportion of your estate would have to be paid to the government as a tax. Carefully planned trust structures could help to ensure that estate duty was not payable, by taking assets out of your hands and placing them in trust.

Over time, other benefits of placing assets in trust became apparent – it could mean that income wasn’t assessed for superannuation qualification (back when there was a surcharge which effectively meant means testing) and for many New Zealanders that they would still qualify for a rest home subsidy as their assets were no longer in their own names.

There were also tax planning opportunities with the ability to tax split through a trust structure – simply put, many people set up trusts and moved their assets into them because their accountant told them to. Many others set them up because that was what everyone else was doing and they didn’t want to get left behind – perhaps a case of the Emperor’s new clothes?

Over time though, many of these perceived advantages of trusts have been eroded. The surcharge on superannuation was abolished in the early 1990’s. Death duties were zero rated in the late 1990s and then subsequently abolished. Limitations on being able to allocate income to minor beneficiaries at their lower tax rates was introduced in the early 2000’s and then in the late 2000’s, marginal tax rates were flattened, pulling the top personal tax rate down to be in line with the trust tax rate of 33%. This reduced many of the tax benefits in having income producing assets in trust.

Lastly, the landscape of rest home care in New Zealand has vastly changed since the 1990s. Rest home subsidies are now very difficult to get and are only really available for those in need. Having a trust will certainly not ensure that you will get the subsidy if you go into care, regardless of how long you have had your assets in trust or when you gifted them.

For many people, particularly those whose main asset is their family home, having a trust may in fact be detrimental when applying for the subsidy. Some people may be in a position where they are more likely to receive the subsidy if they don’t have a trust than if they do.

Coupled with some of the perceived benefits no longer being there, a higher duty on trustees to keep accurate records, hold trustee meetings and provide certain information to beneficiaries, means that the costs of continuing to run some trusts will outstrip any potential benefits.

The new Trusts Act 2019 which comes into force in January 2021 outlines more stringent rules for how trusts must operate. This has got many people thinking as to whether a trust is actually the best asset owning vehicle for them.

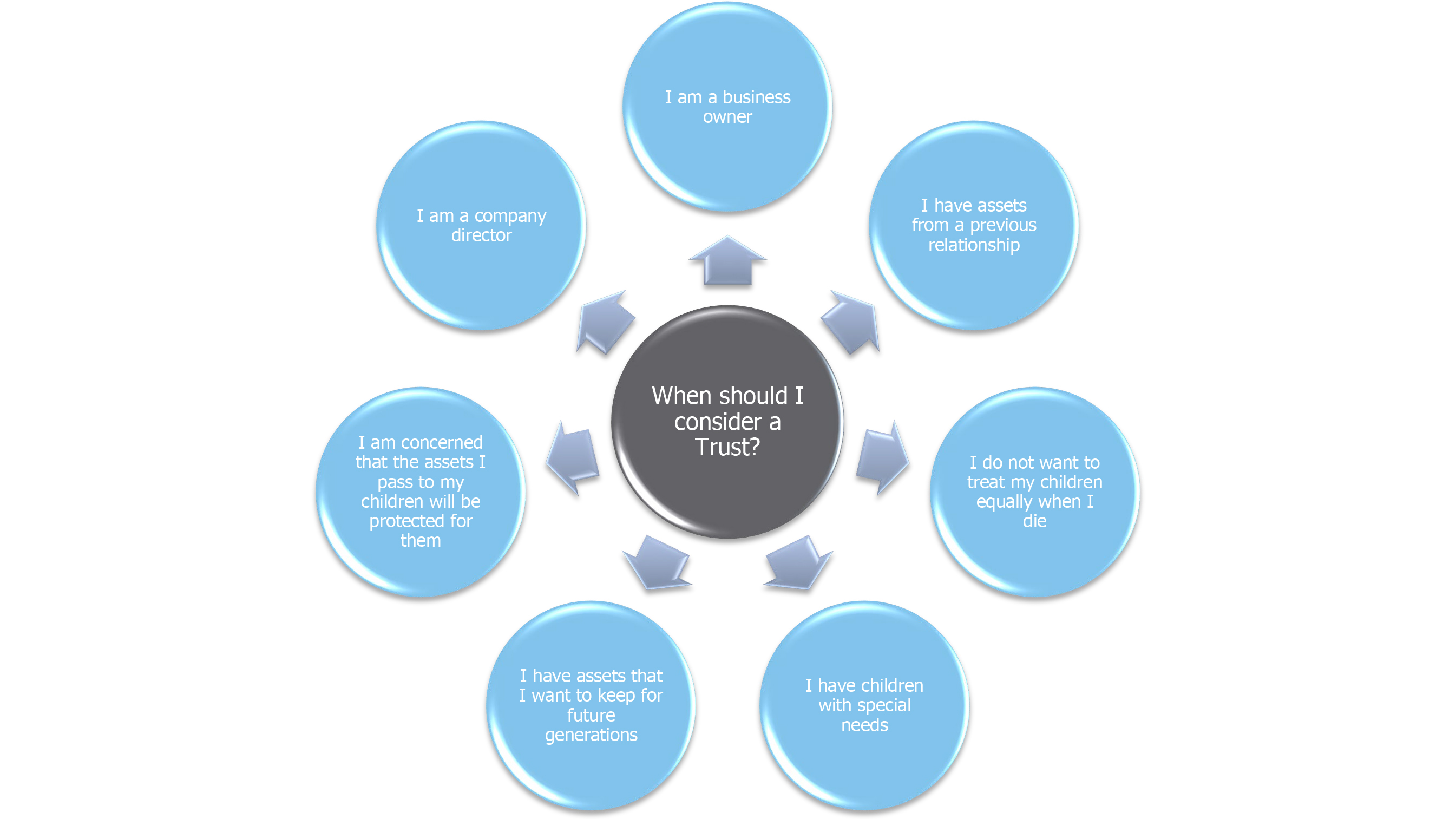

There are of course many good reasons why a trust might be right for you and your family. The simple flow chart below can help with the decision as to whether you need a trust or maybe should be thinking about other ways of dealing with your assets. The benefits are great for many.

However, trusts are not the only asset planning tool and for many New Zealanders; a well-crafted Will may be the best thing for them rather than a Trust. The important thing is to take advice, consider your options and do what is best for you and your family.

Tammy McLeod is the is the managing director at Davenports Harbour, specialising in the areas of personal asset planning, trust law and Property (Relationships) Act.

22 Comments

Fully agree.

Trusts are now both cumbersome and can be expensive.

Property transactions - especially when involving a mortgage - are very cumbersome due to both increasing bank and anti-money laundering legislation requirements.

Mother (94) has had a trust for 30 years; as well as costs of setting it up paid annual accountancy fees of $850 pa. for many years for no benefit. Sold house, bank anti-money laundering requirements required an eight page document with numerous details of all beneficiaries (including grand children) simply to make a term deposit with the bank with the Trust had always banked with.

Even the reason give that one has property from a previous relationship is increasingly becoming questionable as Trusts are increasingly being looked through by the courts. A cheaper and seemingly more robust option is a Relationship Property Agreement in which both parties with legal advice agree to at the outset.

Making a price-based decision for usefulness of a trust is not necessarily that helpful. Your example leaves out the very real issue for business owners of potential creditor claims.

A fairly backward looking article.

I feel that the tsunami of taxation and regulation coming our way to pay for the Covid handout packages, will make Trusts more relevant than ever.

This article doesn't address the much bigger issue for those whom trusts are useful for of the trusts being sham trusts.

Trusts became more in vogue when the clark/cullen govt introduced their "rich prick" tax as did limited liability entities.

Did the knight not just write a will and the "trust" is the relationship with whomever he chose to enact his wishes?

Limited liability and trusts have all been perverted into ways and means to avoid responsibility and accountability, and legal tax avoidance mechanisms.

True democracy would suggest that we the people should have more say in our tax laws and corporate structures. A vote at the election, at the AGM is an illusion of democracy if you don't have a say in the rules first.

The author says that "rest home subsidies are now difficult to get".

However, it's my understanding from expert financial columnists like Mary Holmes in her regular Saturday column in the business section of the NZHerald that there is asset testing in place.

Asset testing, for instance, allows a person to retain about $230,000 if they are single (eg widowed), and they don't own a home, before they pay rest home fees for themselves on entering a resthome. If she lives in her own home or a jointly-owned home with husband, eg wife at home and husband in rest home, the cash amount they may jointly retain before rest home fees (for the husband) have to be paid is reduced to around $124,000 but they are additionally allowed to retain the value of their home.

$230,000, or $124,000 plus a home, are not insignificant amounts to most New Zealanders including most readers of these columns.

No trusts are involved in these examples.

I think that the author is obliged to clarify whether or not I am am wrong on this point.

Eligibility for subsidies depends also on deliberate deprivation of income and assets in the years prior to claiming the rest home subsidy.

You can have a massive property worth several millions and only a little income and savings and still get the reathome subsidie.

That's correct, as long as the expensive property was bought a long time before the spouse or partner enters the rest home.

The couple couldn't, say, sell the long-lived-in family home worth $600,000 and buy a new home for say $1,600,000 using the proceeds of the house sale plus $1,000,000 in the joint savings account, shortly before one spouse goes into the rest home. That would obviously be what the law would describe as 'defeating' the law; i.e. an intentional attempt to avoid the payment of rest home fees. And the prior creation of a family trust would, today, not prevent the fees being paid for out of that $1,000,000; it couldn't be retained for the beneficiaries of the trust.

What should happen in this case is that the wife would retain the original home to live in, and the $1,000,000 would be used to defray the rest home fees incurred by her husband until they were reduced to around the $124,000 threshold prescribed by asset-testing law at which stage no more fees would be payable.

The thresholds for both single and partnered people is increased every year to keep abreast of inflation, but obviously there has been little increase in recent times.

As no answer has been forthcoming to address my above query in my original 3.12 pm (now 8.20 pm) comment I can only surmise that this article is not a genuine objective argument on the usefulness of trusts but a touting for business, in other words an advertisement.

Putting on my more powerful glasses I can see in the blue circles that every reason why the author advises one to get a trust are the very same reasons that one has always got a trust for if they had half a brain. This story is not new, it has been around for years. But I know that there are unscrupulous lawyers that have persuaded their clients to create trusts when they are not necessary.

But I will stand by my statement that there are subsidies for rest home care for the vast mass of New Zealanders. But, for say 5% of the population who are particularly wealthy, there will be rest home fees payable, despite the existence of a trust, until the thresholds are reached. I don't know how many readers out there fall into this category.....not all that many I suspect as so many of them appear to be FHBs (First Home Buyers) in waiting.

hi streetwise yes, you are correct, there are subsidies still available for a large amount of New Zealanders. However, my point was that having a trust will not mean that you will absolutely qualify for the subsidy regardless of what your asset base would have been, but for the trust.

So essentially trusts enable people to avoid paying their fair share towards running society. Remind me again why this is OK?

It generally seems to be because welfare benefits are only bad when they're for dirty poor people.

2 out of 3 of the people in my fathers rest home were NOT paying the fees when it was costing him $1000 a week with his house sold and $750k in the bank so YES there must be one hell of a lot of people using a trust to avoid paying at rest homes. Basically if you want free rest home care you need less than $230k in the bank or the house in a trust 7 years or more before hand or gift any excess money 7 years or more before entering a rest home.As this was a generation where im sure home ownership was more than 30% then clearly trusts are used as avoidance.

Hi Tammy, I know this is out of your topic regarding subsidies, as I heard start from next year due to change in trust laws all the trustees are required to inform the trust income to all the beneficiaries added to the trust. My question is the parents generally formed this trust just to ensure they have material support from the trust for the rest of their lives. Please let me know why trustees have to inform the kids which eventually demotivate them in the expectation that they will receive substantial sums of money from the trust.

Beneficiaries are already entitled to see trust financial records etc.

Hi Ben, as noted by Rastus, the law already requires trustees to give certain information to beneficiaries. The new law just makes that a statutory right. I look forward to writing more about the implications of the new law and what that will mean for trusts.

Thanks Tammy. Looking forward to your second article.

There is the question of if you have a house and more than $124k of cash so as to be able to pay the $1000 a week for care perhaps being cared for under some arrangement in you own home might be preferable. Does

anyone know of examples of this happening which are working well?

Doesnt work because if you need a rest home you need 24hr care. If your in your own home you can generally care for yourself. There is only a very small window in between where a bit of outside help will work and yes homecare is available but then the recipient ends up needing a home due to increased rates of falling over or even just being helped to dress or get into bed.

The one big advantage of trusts is to keep safe assets that might otherwise be available to creditors if a beneficiary faces bankruptcy. So long as the trust has been set up for some years before the beneficiary got into trouble it works well. The other reasons for trusts have largely gone, but the protection given to assets is a valuable thing.

Thank you for all reading my first article for interest.co.nz and your comments. I look forward to contributing further.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.