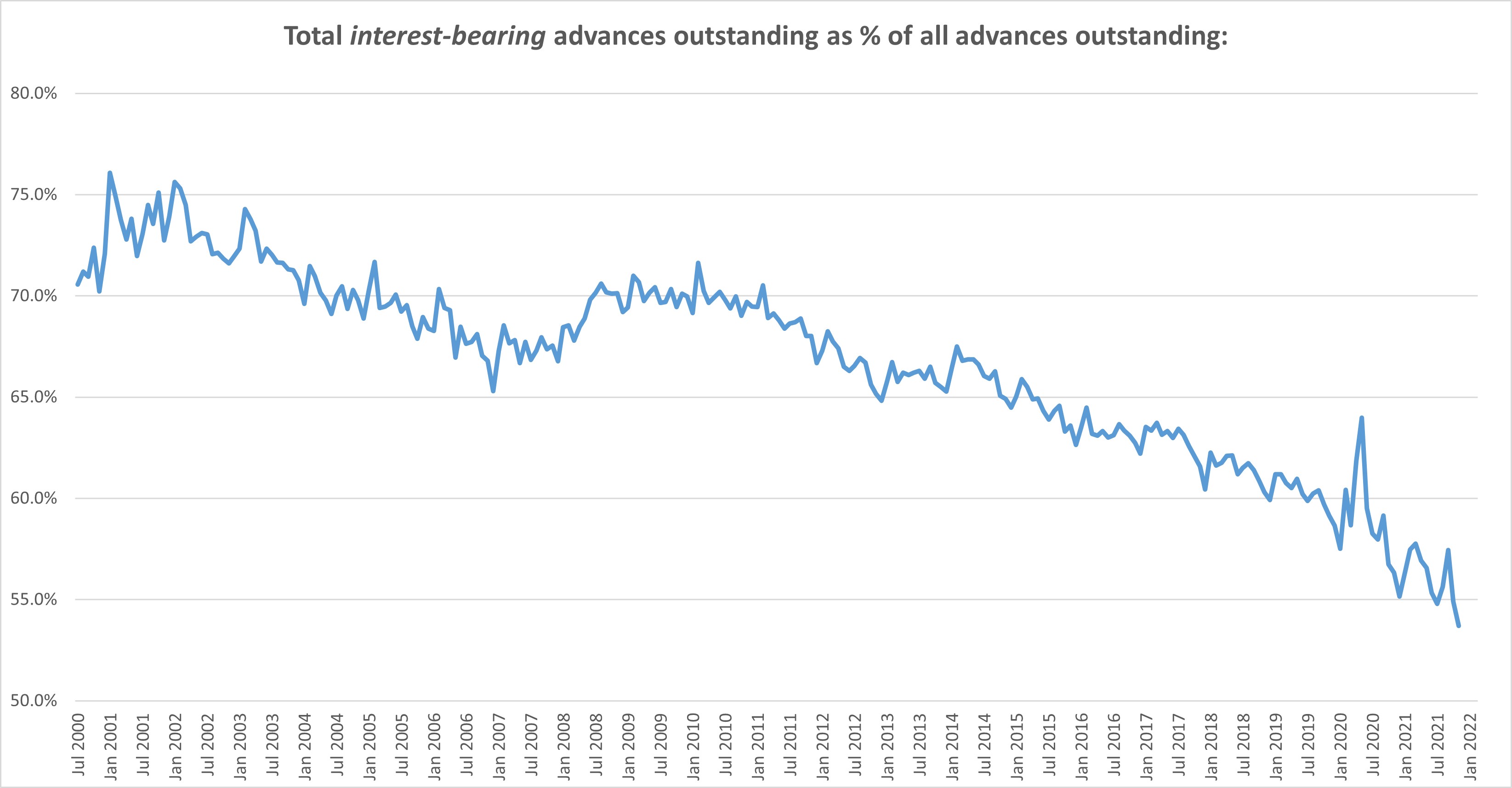

The amount of interest bearing balances left over on credit cards at the end of each month has been falling and dropped even further over the last two pandemic years, according to RBNZ data.

Though for some the lockdowns provided time to pore over their finances and embed better habits, it seems more likely to be as a result of transference to other lines of credit.

Buy Now Pay Later (BNPL) is a recent, and increasingly popular, entrant to the consumer credit space.

The chart below shows the change in total personal interest-bearing advances outstanding, as a percentage of total personal advances outstanding, using RBNZ data:

Hannah McQueen, founder of enable.me said that if the credit balances on BNPL were added to those of traditional credit cards, she would be surprised if the overall rate of credit remaining unpaid month-on-month is actually falling.

BNPL, offered online and in retail stores under a number of different 'brands', is a popular short term finance option which allows the borrower to make an initial payment, take the goods immediately and pay the rest off over a number of installments.

Unlike a credit card, there are a set number of (usually equal) payments, interest is not usually charged and a balance cannot be carried over indefinitely simply by making minimum payments.

However there are still potential pitfalls, including penalty fees for late payments or getting swamped in debt by taking on too many BNPL plans - there are usually no credit checks.

Late last year, the Government issued a consultation paper looking at the the triggers of financial hardship caused by BNPL sector and proposing ways to regulate it, including the possibility of applying the Credit Contracts and Consumer Finance Act (CCCFA) to the providers.

McQueen said lockdown was financially reflective for some and this included their credit card habits and questioning behaviours like carrying balances over, despite having enough in savings to pay off the full amount each month.

Though quite common, she said the behaviour was not necessarily deliberate, and rather was a product of "lazy budgeting."

At the same time there was a feeling of security that came with having a "rainy day fund" in a savings account, despite its ability to offset the credit card interest.

"They haven't got around to putting savings against their credit card and have been carrying higher balances than they needed to.

"The pandemic sharpened their approach to it but they're not as deliberate as they need to be and don’t realise the impact of the interest rates and not paying it off in full," said McQueen

In credit-card-world slang, someone who does pay their credit card balance off in full each month is known as a 'deadbeat' because they are a less profitable customer for their bank or credit institution.

Though they often rack up rewards points for 'nothing', the saving grace of a 'deadbeat' is that they do not leave bad debts for the financial institution to mop up.

McQueen said that sometimes financial advisers suggest managing your credit card this way but obviously you'd never hear it from banks themselves.

One suggestion she gives for getting out of a credit card hole is a three-month detox, which she likens to a Level 4 financial lockdown which trims the fat out of the budget in order to build a surplus again.

McQueen said it was important to make steps in the right direction to avoid spiraling backwards and becoming disheartened.

"Once you start getting a high balance, it can feel impossible, you start disengaging further and start to become more [financially] relaxed at the very same point you’re trying to lean into getting better," she said.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.