A war, inflation, a proposed Tax Principles Act, dramatic U-turns and the Trustastrophe. 2022 has been quite the year and I'm certain I'm not the only one whose predictions ended finished up wide of the mark.

Back in January, I saw three main themes for the year. Firstly, the ongoing response to COVID 19 and what new fiscal support will be offered. As part of this, the question of inequality and the taxation of capital would be on the agenda. Secondly, international tax reform and progress in the deal announced in October 2021. And finally, with Inland Revenue, how it was going to administer the tax system in the future.

Well, on the first there was a new COVID support package announced shortly afterwards in February, which ran through until May. However, although COVID is still very much around, the government's focus has rapidly shifted to dealing with a cost-of-living crisis in part, the result of COVID 19 and supply chain issues and the spike in oil prices after Russia invaded Ukraine.

By the way, as for financial support for COVID, only the Leave Support Payment Scheme, which pays $600 per week, remains available

Now, this is the year the details of the international tax deal announced in October 2021 were meant to be worked out, so everything would then be ready for implementation next year. Instead, it ran into a series of obstacles which has delayed this implementation until 2024 at least. Fortunately, however, this week a key obstacle has been removed, after first Hungary and then, following some last-minute shenanigans, Poland, dropped their objections to the deal. This enabled the EU to unanimously agree to implement Pillar two of the OECD proposals. This will impose the minimum corporate tax rate of 15%, which will apply to all national and domestic groups with combined annual turnover at least €750 million.

Overall, although progress is being made, it is at a slower pace than was expected back in 2021, and I would expect that will still continue to be the case next year. In fact reading the tax press, some are beginning to wonder if it will ever happen. But we will see.

Inland Revenue and the Cost of Living payments

After completing its Business Transformation programme, I expected Inland Revenue to turn its attention back to how the tax system is run. And certainly, at the start of the year there was a quite a bit of activity in this area with a particularly useful paper prepared by business New Zealand on the matter. However, the topic dropped off the radar in the wake of the cost-of-living crisis, which somewhat ironically then put the spotlight on how Inland Revenue operates

In May’s Budget the Government announced a Cost of Living payment of $350 to be paid in three monthly instalments starting on 1st of August. To say there were a few teething issues would be one of the understatements of the year. Although mistakes were inevitable, given that were potentially over 2.1 million recipients, right from the outset, Inland Revenue seem to be struggling to manage the delivery of the payments.

As has been reported, quite significant numbers of ineligible recipients and a large number of whom were outside New Zealand, had received payments incorrectly. And Inland Revenue also acknowledged there had been a systemic problem in respect of one group of 12,000 recipients.

Inland Revenue does now appear to have got on top of the issue of identifying the correct recipients of the payments. By the time the third payment was made on 1st October, the number of payments, compared with the first instalment in August had reduced by 96,000.

Inland Revenue now calculates that between 70 and 80,000 people may have incorrectly received a cost of payment and has now begun contacting this group about those payments.

Given payments were expected be made to 2.1 million people, some mistakes were inevitable. It is however, of concern that there were systemic issues identified. It's arguably more problematic that Inland Revenue required by its own estimate, 750 staff, almost 20% of its current staff, to process those payments. This, combined with persistent rumours about now frequent overtime indicates potentially serious under-resourcing issues at Inland Revenue and that is something we will be keeping an eye on going forward.

The Cost of Living payment was one of the few surprises in May's Budget. Grant Robertson chose again to do nothing about increasing thresholds, which, although tax rates were changed on 1st October 2010, the actual thresholds at which those tax rates apply, haven't actually been adjusted since 1st October 2008. The theory behind the Cost of Living payments were that they were more targeted than raising the thresholds. But as we've just discussed administrative errors by Inland Revenue meant that the payments attracted more controversy than anticipated.

Politics trumps tax policy, again

That said, the controversy around the Cost of Living payments paled beside the reaction to a proposal in the August tax bill to raise GST on management fees paid by KiwiSaver funds. On the face of it this was a routine tax measure designed to tidy up what was an unclear tax treatment and would not have taken effect until 1st April 2026. But it was expected to realise an estimated $225 million a year and then a political storm erupted once the accompanying Regulatory Impact Statement revealed that on the assumption the increase in GST would be fully passed on to KiwiSaver fund members, KiwiSaver balances would be reduced by an estimated $103 billion by 2070.

The Government rapidly decided to retreat, and the offending proposals were withdrawn inside 24 hours, which is a quite unprecedented move. It is one of the clear cases of politics trumping tax policy because once the dust has settled, the issue the matter was trying to resolve is still to be addressed. I suspect that whoever tries again might think about addressing criticism by using the funds raised to either restore the fee subsidy of $40, which was withdrawn in 2009, or adopting one of the Tax Working Group's proposals for minimising the effect of tax on KiwiSaver funds of low-income earners.

The Trusstastrophe

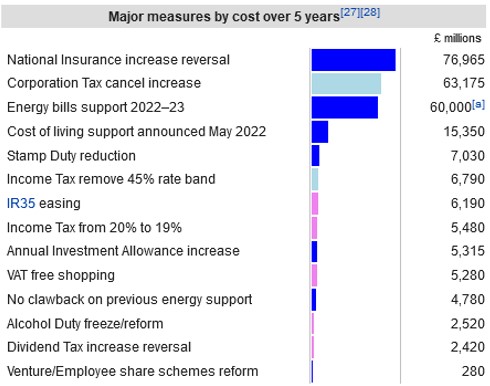

That controversy and U-turn was, quite frankly, nothing compared with what might politely be described as the Trusstastrophe (I've seen ruder descriptions) which happened barely a month later in the UK. To recap new Prime Minister Liz Truss and her Chancellor of the Exchequer, (finance minister) Kwasi Kwarteng decided to go for broke with a bold tax cutting mini-Budget in September. This proposed significant tax cuts, primarily the reversal of a proposed corporation tax increase and the removal of the 45% tax rate on the income tax rate. This provoked a massive run on the Pound and more worryingly in the gilt markets, the UK Government's bond market.

Within four weeks, no fewer than seven of the tax cutting proposals were gone and shortly afterwards so too were Kwarteng and Truss to become footnotes in history. Truss becoming the shortest serving prime minister in British history. (Remarkably, Kwarteng is only the second shortest Chancellorship in history, after Iain Macleod who died in office after just 30 days).

What Kwarteng proposed

What eventually transpired

But if that was all great fun to watch from this side of the world, Truss and Kwarteng’s dramatic fall actually had a knock-on effect here. Arguably the most controversial proposal was the withdrawal of the highest 45% income tax rate band, it highlighted how a disproportionate amount of the proposed tax cuts would have gone to relatively few people. In the wake of the fallout, National here felt compelled to announce it wouldn't go ahead with its proposed abolition of the 39% tax rate in its first term if it forms the Government after next year's election.

There was also something else amidst the mayhem which didn't attract a lot of attention. There were no attempts at all by Truss and Kwarteng to reduce capital gains tax or inheritance tax. In fact, Kwarteng's successor as Chancellor Jeremy Hunt, has actually increased the tax on capital gains by reducing the annual tax-free allowance from its current £12,300 steadily to £3,000. This is an interesting insight into the relative states of the tax systems in the UK and here. The UK system even when being managed by bold tax cutters left alone the taxation of capital. Whereas as we know here, the taxation of capital is a perennial problem.

A Tax Principles Act?

It was in part to this issue that David Parker, the Minister of Revenue made a very interesting speech in April in which he proposing a Tax Principles Act across by which the system could be judged, regardless of the Government in charge. It's well worth reading again the proposals, but we have not seen anything regarding the proposed bill which at the time he suggested would be coming out this year. Given how the Government reacted to the GST on management fees issue, I think it's probably likely we won't see this at all until next year, if Labour is re-elected and forms the next Government.

A constant theme of this podcast is around taxation of capital, because there's a lot going on in the world in this space. As we just mentioned, the UK despite bold tax cuts, wasn't prepared to make changes to the taxation of capital. Over in Ireland, the Irish Government Commission asked a Commission on Taxation and Welfare to report on the Irish tax and welfare systems. Its final report published in September, made 116 recommendations, one of which was that the overall yield from wealth and capital taxes, including property, land, capital acquisitions and capital gains taxes should increase materially as a proportion of overall tax revenues.

And this is so one of the areas we think New Zealand is out of sync with global trends. But the politics are very difficult. It's easy to say what’s needed as a tax consultant, but politicians want to be re-elected and they have to deal with the political fallout. But whenever I do address this topic, it always provokes a lively discussion.

Top Five most read transcripts

It's interesting to look at what are the most read transcripts and most listened posts and try and pick a common theme. They're actually surprisingly different. By far the most read transcript for the year was when I discussed an interpretation statement on the application of land sale rules to co-ownership changes and changes of trustees. Interestingly, this was one of the top five most listened podcasts.

The Budget special was the second most read transcript for the year. At number three was when I discussed extended reporting requirements for trusts. (In that episode I also warned about the risks of mis-understanding the UK’s remittance basis rules after then Chancellor, and now Prime Minister Rishi Sunak became embroiled in a scandal).

The consistent theme emerging is about the taxation of property/wealth and that's the case for the fourth and fifth most read transcripts. The fourth-place transcript covered a Reserve Bank of New Zealand's Analytical Note on the housing market in an international context. The RBNZ note compared our housing market with several other developed markets and suggested that favourable tax settings have not helped the housing crisis.

In the fifth-place transcript I looked at the question of wealth and windfall taxes. Certainly, the comment section gets pretty lively whenever I make a suggestion that maybe we do need to change tax settings around the taxation of capital, such as introducing the fair economic return that Associate Professor Susan St John and I have been talking about for some time.

Top podcast tracks

With podcast listeners the top five is slightly different. The most listened to podcast for the year involved the proposed income insurance scheme, which has slipped under the radar although it's still progressing in the background. Housing and countering tax avoidance was also in the top five podcast tracks for the year but only the episode covering the changes in ownership appeared in both top five lists.

Time for a more open discussion on tax?

As I said, whenever we deal with the taxation of housing, that pushes a few buttons which is sometimes amusing to see, but inevitable. But debates about what we tax aren't going to go away. We're going to see them more so next year being an election year. I do think we need to be asking a lot more about why we're raising the tax – this point frequently comes up in the comments to a transcript.

This is important because one of the things that is emerging is the longer-term trends for the tax-take relative to the demands and pressures on it, such as rising superannuation costs. Those aren't being very publicly discussed, but they're very clearly being pointed out to in by Treasury's report on Wellbeing and particularly in He Tirohanga Mokopuna 2021, its combined Statement on the Long-Term Fiscal Position and Long-Term Insights Briefing. But the Government doesn't really want to talk about capital gains taxes at all. When Inland Revenue was preparing its Long-Term Insights Briefing it was specifically told not to consider the impact of capital gains tax.

I think politicians have deliberately, if understandably proscribed debate on the matter. But the fact is those debates aren't going to go away. Tax systems evolve over time and these issues are going to need to be discussed because ultimately if “taxes are what we pay for a civilised society”[1], they also meet the demands of the economy and society at that time. If tax doesn't change or adapt to meet those needs we have future problems brewing.

And on that note, that's all for this week and for 2022. I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you to all my listeners and readers and for all the feedback I greatly appreciate it even if we don’t always agree.

Until next year kia pai te Kirihimete, have a great Christmas!

[1] US Supreme Court Justice Oliver Wendell Holmes, Jr, in the 1927 case General de Tabacos de Filipinas v. Collector of Internal Revenue

*Terry Baucher is an Auckland-based tax specialist with 25 years experience. He works with individuals and entities who have complex tax issues. Prior to starting his own business, he spent six years with one of the "Big Four' accountancy firms including a period advising Australian businesses how to do business in New Zealand. You can contact him here.

23 Comments

Always an interesting read . Merry Christmas.

'As has been reported, quite significant numbers of an eligible recipients and a large number of whom were outside New Zealand, had received payments incorrectly. I think 'an eligible' should be 'ineligible'.

'I think politicians have deliberately, if understandably prescribed debate on the matter.' For 'prescribed' read 'proscribed'.

Thanks John, duly revised. (In my defence it was getting near Beer O'Clock)

Taxation has nothing to do with financing the government. The government spends currency as central bank reserves, while taxation only deletes bank deposits and these exist on opposite sides of the Reserve Banks balance sheet and also a commercial banks balance sheet.

The Levy Economics Institute tells us,

Publications

Working Paper No. 244 | July 1998

Can Taxes and Bonds Finance Government Spending?

This paper investigates the commonly held belief that government spending is normally financed through a combination of taxes and bond sales. The argument is a technical one and requires a detailed analysis of reserve accounting at the central bank. After carefully considering the complexities of reserve accounting, it is argued that the proceeds from taxation and bond sales are technically incapable of financing government spending and that modern governments actually finance all of their spending through the direct creation of high-powered money. The analysis carries significant implications for fiscal as well as monetary policy.

https://www.levyinstitute.org/publications/can-taxes-and-bonds-finance-…

Perhaps supporting your point, but emphasising that a 'no-tax system' would eventually implode under the weight of uncontrollable inflation (what we have today, and why 'they' are hell-bent on containing it?).

With banks holding an abundance of reserves acquired at almost no cost, they would offer loans at very low interest rates. If the low rates continued for an appreciable time, the resulting excess liquidity in the private sector would overheat the economy and cause serious price inflation. It is evident then that without taxes, the combination of no government borrowing and no interest paid on bank reserves is not a viable system in the long run.

No one is suggesting that we don't need taxation or that it is not important but we should move the conversation away from it financing spending and only then can we design an equitable and effective taxation system and with the government spending in the public interest. The government is always hamstrung by the argument of "where will the money come from" or being accused of being a tax and spend government and wasting taxpayers money.

Far too much nonsense has also been spoken about QE and it flooding the economy with money and causing inflation when in fact it has done none of this.

Government budget deficits are the only way in which households can acquire the 'net financial assets' to add to their savings and we must also finance our current account deficits, (sectoral balances).

'Taxation has nothing to do with financing the government.'

The tasks of taxation are (1) to subdue inflation (revenue for burning), and (2) to transfer wealth from rich to poor, to sustain social cohesion (revenue for disbursement, either directly to recipients, or indirectly by free services, health care, education, etc).

Do you feel there is any appetite from any political party to address the issues surrounding the taxation of unrealized gains on overseas investments ? I ask as this is clearly one of the reasons there is a heavy bias towards investment in domestic residential real estate.

Yes, OECD countries like Canada and the U.S. have no such tax on unrealized gains like NZ. But next year--if Labour is re-elected--the Greens are proposing a wealth tax on all assets, with a threshold of only a million dollars--including the family home. It would kill investment in NZ, and many people with money would flee to Australia.

Ah yes, the Greens' insane policy that saw a single family home in Auckland tip families into the wealth tax net, yet you could have multiple rental properties in all sorts of backwaters and still come under the threshold for being captured.

Pure garbage.

Enjoyed your learned articles this year Terry - thank you.

The lack of a tax on accumulated / unearned wealth is an Achilles heel for our tax system. The money that enters our economy via bank loans or govt spending is transferred efficiently into the accounts of the already wealthy - leaving the rest of us in debt. Our tax system is illequipped to tackle the concentration of wealth and the resultant inequality is going to destroy our society.

Accumulated wealth and unearned wealth are very different. When my 61 year old wife cashes in her KiwiSaver in four years time she will be unhappy to see it taxed (firstly the PAYE income that went it to it was taxed, then your proposed wealth tax and finally GST on her purchases).

"The lack of a tax on accumulated / unearned wealth is an Achilles heel for our tax system" - not really .

It is merely what prevents Terry from running a more profitable business ; he will keep droning on about it of course.

I think you got it there jfoe, there is an element of citizens that should pay more in tax. I have been a low earner for most of my life but we are doing good now and paying our fair share in tax. So as you point out those so called clever people need to be brought to account and pay their dues.

All business with funds coming from without or within our country should be taxed here.

Amazing how the inequality of wealth should be a prime concern for the tax system, but not the inequality of taxpayers - with some paying a huge amount and a huge amount more paying next to nothing or even negative tax.

This agonising over whether the tax system should be used to drive down inequality is nuts. The tax system should be used to fund the state. End.

Is it the fault of those paying next to nothing? I'm sure a lower income working family would like to have the gratification of being tax positive. I know I'm grateful for being a net positive tax contributor, and I don't begrudge those that aren't.

Maybe we could scrap Working for Families, while simultaneously legislating a 20% drop in all rents across the country. Magically the low income family are now tax positive.

Exactly. I have real hatred of the use of stats to suggest low income earners pay no tax. Complete and utter bollocks and your magic is a good way of putting it.

Why? Because it shows the 'fair share' talking point nonsense to be exactly that - a meritless talking point?

If you're counting on the tax system to make just make rich people less rich instead of using tax revenue to make it easier for people on low incomes to access what are fundamentally basic services then you've taken the bait. Maybe we should be asking how well the state is using the dollars it gets and how effective our civil service and political class is at delivering meaningful policy change before you let them convince you that dicking about with the tax system is a valid substitute for just providing those services directly?

If it actually mattered, they'd do something about it. You're defending the excuse they've made for not doing so. How many decades of that not working do you need to see before you accept it might not actually work?

Nope. But that's where the tax system has been distorted by this idea it should act as a Robin Hood mechanism instead of directly funding the services those people need as provided by the Crown. School lunches, dental services, the works. Decide what sort of services we should be directly providing and set the tax system up to collect what you need to fund it.

The money-go-round approach to our tax system isn't sustainable. It creates too many competing interests when you need to modernise your tax system and disconnects the reality that the state should be providing a lot of these services, not just dishing out dollars for them (which is usually never enough) for people on low incomes to compete for access with each other for them. It ends up being a bad deal for everyone.

The problem with not having a CGT or a LVT is you are then required to have higher income, company and sales taxes than what would otherwise be the case to maintain a given level of spending

Council Rates have a LVT component. The govt just needs to double that component. More than double would be too dramatic.

Many countries have CGT but aren't they all small contributions to Govt tax revenue? Isn't there a danger they will just keep lawyers and tax accountants happy. When there is a recession a govt needs usually more money for unemployment benefit, etc just at the time the CGT income shrinks.

Looking at UK tax (All in pounds) (Excluding dividends which are taxed less). 2020/2021

Personal Allowance (Tax free) 12500

First 37500 ($75000) in excess of personal allowance 20%

Next 112500 ($225000) 40%

Anything else 45%

Revenue collected

Income Tax 194 billion pounds

Vat 130 billion

National insurance 143.1 billion

Corporation tax 61.3 billion

SDLT?? 11.6 billion

Capital gains 10 billion

Inheritance tax 5.1 billion

Capital gains tax is about 2.5% of the tax take and inheritance tax half again, about the amount this government squanders on consultants for projects that go no where.

Not sure this is the silver bullet it is made out to be.

Also shows that the UK has greater income wealth than NZ and skewed to the upper earners of which we don't have enough, would be interesting to compare our revenue collected, which I will do when time permits and compare who pays the tax.

A major issue with taxing accumulated capital and assets whose value increases due to inflation is the disincentive to saving rather than spending. Inflation adjustment is only a partial solution given CPI is not reflective of actual inflation of specific assets. Many new business's rely on Bank funding geared to a properties value so Banks may choose to adjust loan to reflect the potential CGT and hinder the transfer of assets between parties for good commercial reasons. Every time Govt interferes in the market the results are usually bad, people respond much better to incentives than disincentives and like a Donkey keep hitting it with a stick it will kick out and if you are in the way pain will result - the current Beehive clowns are likely to feel much pain after NOV 2023 unless an earlier kick bring the reckoning forward.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.