By Janine Starks* (email)

From my mail bag:

We are red stickered and expect that our section will be condemned, so we may not be able to rebuild. The big question is what will we get from EQC for the value of our section? We have the City Council valuation of 2007 but we expect the value should be 12.5 percent higher, because we are right by a river in a picturesque spot. Are we dreaming? Will EQC give us a fair market value for our lost section?

Hmmm. That was a yes-and-no ‘hmm’.

The issue of whether your land will even be ‘condemned’ was the first thing that crossed my mind. Remember we’ve gone from sweeping statements that 10,000 homes could go, to more conservative theories that only pockets of land, or a street here and there will be written off.

While you live by a river (and that must increase the likelihood of this fate), make sure you prepare yourself for either option. Expect the unexpected, as you never know what recommendation the geotechnical experts might make.

Everyone’s patience is being sorely tested as no one can think ahead or plan their lives. Things have ground to a halt as we wonder “will I stay, or will I go?”

Those words bring back memories of the 1980s British punk band, The Clash, whose lyrics could almost become an anthem for the liquefied suburbs of Christchurch; “so you got to let me know, should I stay or should I go”. If only EQC could tell us.

Fair market value?

When it comes to the value of your land and whether this will be a ‘fair market value’, there is good news and bad news.

The good news is that EQC’s literature states “claims for land will be based on a professional valuation” and “EQC appoints a registered valuer." You can’t get fairer than that, so it does keep the dream alive.

| Do you have a question for Janine? You can email her starkadvice@gmail.com, subject line: Financial Agony Aunt. Anonymity is guaranteed. |

No doubt there will be a level of negotiation required and some homeowners may be tempted to get their own independent land valuations to double check. So it seems clear that the valuation techniques should be fair, but you have to read the fine print of the rules to work out what size section will be covered.The unknown question is how granular those valuations are going to be. One would hope that they don’t apply a rate to an entire street, when we all know one end of a street or certain spots within it, can be far more desirable than others.

The bad news is as follows:

a) For many homeowners, they will receive a valuation on a smaller sized section than they actually own.

b) There is an excess deducted of 10% of the value of the land (minimum excess of $500 and maximum $5,000).

c) When it comes to valuing retaining walls, bridges or culverts on your land, EQC only pay out an ‘indemnity’ value (a depreciated value which accounts for age)

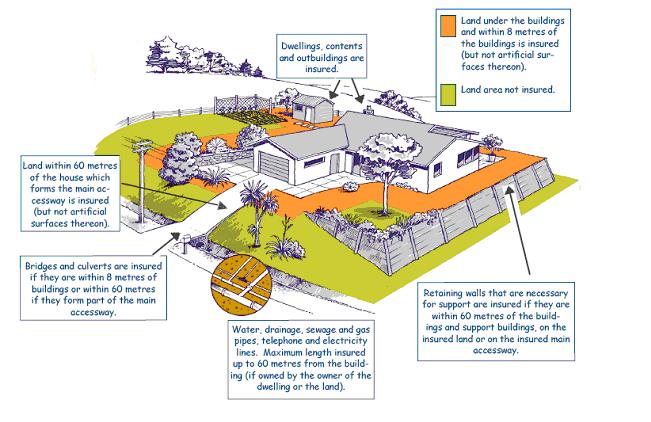

What land does EQC cover?

Take a look at the diagram below. EQC will only cover damage to certain areas of your section; the land that sits directly under your home; the land within eight metres of your home; and the land on the main accessway up to 60 metres from your home, including retained areas (but not the driveway surfaces like asphalt or concrete).

This means there could be sizable areas of your section which are not taken into account. Plus, brace yourself as there’s a second round of bad news.EQC does not cover trees, plants, lawns, fences, drains, paths or retaining walls more than eight metres from your house.

If your section is condemned and can’t be rebuilt on, the area detailed above could shrink even further when it comes to a valuation.

Devilish details

The devil is always in the detail, and this little gem can be found under Part 2 Section 19 of the EQC Act.

The payout will be based on the value of the smallest area listed below:

1. The area of a minimum sized section allowed for in the district plan.

2. An area of land of 4000sqm (about an acre)

3. The area of land that is actually lost or damaged.

In the list above, note the use of the word ‘smallest’. For most people in the suburbs, it will mean the payout is based on item one.

In Christchurch the minimum lot size is 450 square metres for those zoned ‘Living 1’ and 330 square metres for those who are ‘Living 2’.

On Banks Peninsula it's 400 square metres, with the exception of Diamond Harbour at 600 square metres. The result will depend on where you live, so phone the council and ask what applies to your location.

In addition, the indemnity value of any retaining walls, bridges or culverts will be added on to your payout.

On a happy note: In a previous column on earthquake insurance confusion, I wrote about a couple who had under-insured themselves and were desperately worried about the consequences. Just as an update, they have now met with State Insurance and the outcome has been very positive.

I won’t divulge the exact details, but well done to State for acting so fairly in this case, and well done to our reader for coming forward and facing up to the problem with their insurer.

Do you have a question for Janine? You can email her starkadvice@gmail.com, subject line: Financial Agony Aunt. Anonymity is guaranteed.

*Janine Starks is Co-Managing Director of Liontamer Investments. Opinions in this column represent her personal views and are not made on behalf of Liontamer. These opinions are general in nature and are not a recommendation, opinion or guidance to any individuals in relation to acquiring or disposing of a financial product. Readers should not rely on these opinions and should always seek specific independent financial advice appropriate to their own individual circumstances.

(Updated with EQC illustration)

29 Comments

With 2007 having been the peak, I wonder why the landowner thinks the land value has increased 12.5% since then? It's not as if the river and the picturesque area wasn't there in 2007.

I guess its the confusion over rateable vs. market valuations. They were probably happy at the low rateable valuation so it kept their rates down.....but now......

“claims for land will be based on a professional valuation” . As at when? Then or now? It was easy to do a market value on an isolated case pre-quake, as the surrounding properties gave a guide to "market value". But what is the market now? And what will it be? Are insurers likely to pay out on past value, when current/future fair market value is likely to be less?

thanks janine, I really didn't know the exact details and I suspect thant many many home owners do not realise that most of there section is not covered by EQC or insurance.

I wonder if it is the government who is going to pay the difference ?The banks must also be worried on this as most property's will have a mortgage on them and with only getting maybe half your land value out with insurance (thats if your section is 700sq plus) .

I would say this is exactly why Governemtn has not said anything on the land, and that it will have to be the government that will need to buy up huge amounts of land and putting in there own sub divisions, as I cant see the developments out there at the moment selling there 700 sqm sections for the prcie of a 330 or 450 sq m amount that EQC are paying out on. (Wigram sections up for Sale now- start price $175k)

Expect the following FCM...areas will be classified as not fit for residential construction and property will have to be demolished. Owners will be balloted on new sections in new suburbs built by CERA. The cost of the new sections will be kept as low as possible with the govt cutting away the bureaucratic red tape and rorting charges normally associated with new developments. But any difference between the final cost and the EQC payout sum will be for the owner to pay.

Once paid for, the sections are the property of the owners and they can sell if they wish. So people will not be forced to build and reside there. If CERA get their act together...a big if...the new suburbs could become desirable places to live...with better services and facilities than before...no bloody reason why this should not be the case other than useless inept CCC and sloppy govt behaviour.

The areas deemed uninhabitable will become the property of the CCC and destined for parkland development and bush reserves.

Yeap agree and there are a lot of IF's...and I guess the banks will want there 2 cents worth in here somewhere as well..considering they probably hold the majority of the risk on the damaged land now.....there is going to be a cost for the home owner thats for sure..how much I guess we will wait and see...No wonder so many lawyers are hanging around in CHC..they're going to have a field day.

I hope you are wrong Wolly. Surely if the Govmint is going to take your land they should be expected to pay you a Sept 3 2010 "market value" less what EQC pay up for the land. As for getting a section by ballot - does this take into account where one works, where the kids go to school etc? You've given me a whole new set of things to pray about!

I would prefer being able to choose a section suitable for recreating our house and in an area that suits my family. We don't live in a dictatorship do we?

Sorry about that Crooked Thumb...I doubt prayer will help you...it hasn't so far has it!...as to govt theft of land...goes on all the time...councils can take what they want for a road and you get nuffin unless your plot is bigger than about 4 acres I think...I forget the minimum size...

Best to count on NOT getting a bailout from govt equal to what the land might have sold for pre the first event. If you were not insured then count on getting nothing. Otherwise it will be somewhere in between.

The govt can do what it bloodywell wants...that's the measure of our "democracy" and all you can do is scream...mind the language though or they will throw the police at you.

I suspect Gerry already knows the bulldozer will be going through large tracts of housing and in 50 years there will be large tracts of native bush and parkland.

Thing is...you might get offered a Ballot Right and it would be your property to sell...but then you could miss out on one of the best sections in a new suburb with lovely beach views and even if it costs you $25000 to top up the EQC payout and buy the plot...it might in a matter of years be worth many times that.....

Think outside the square, Janine.

Build yoursef a houseboat. You know, Huck Finn, Proud Mary, all that. Decks all round, it'd be a fun thing to design (talk to Scarfie....

Keep your land. Set out moorings up and down of it. Use you currend pad (or pour one) as a slip-plane. Design the interface to tolerate, oh, say, 3g.

Services? Flexible links, or holding tanks if the Council pull up stakes.

You'd keep your view. Hell, it it was transportable, you could take it away for the hols....

Fat chance PDK....the law will take the land and boot the owners off it....sort of thing happened to Maori a few decades back ...and the Aborigines....and the Red Indians....and the Saxons....and it happens regular like in NZ when some swine decides to draw a new road across your property...or slap in some power pylons...or run a bloody sewer main under your land....

Isn't the "Fair market value" of a section likely to be condemned close to nil? Market value is what someone would pay for the section and quite frankly, I can't see anyone wanting to actually pay for this section. Or does the "fair market value" refer to the value of the section prior to the events?

It would sort of defeat the purpose of insurance if the insured value was the value after damage had occurred! I can just imagine a Monty Python skit,

John Cleese (an EQC assessor) asks Mr Palin (the homeowner) what content damage he had. Palin produces a dinnerset., Cleese assesses it, "10 cents", he proclaims. "What?" erupts Palin, "This dinnerset cost me $100". Cleese replies "But it's broken now isn't it.".

NAILED IT....EQC is run a bit like fawlty towers , Ian Simpson (EQC) kind of looks like Manuel....

Quite true, but by all the EQC stories I've heard so far, I wouldn't be that surprised :)

They need leverage Elley....if they all joined the National Party...!

Hi Elley,

This is Janine's response. She's mired down in Chch so posting it on her behalf.

"EQC will pay the value of your damaged land at the time of the earthquake or natural disaster, or the repair cost, whichever is lower. "

That is a direct quote from their Householders Guide.

I don’t believe this means they will say it is worth nil, otherwise there isn’t any point to offering the cover in the first place as all damaged land, if it can’t be rebuilt on, would be worth nil. They mean the value of the land at the time of the loss.

But only a small size portion of the value...this is the bit I dont think people are aware of.

Why don't the government just buy this land cheap and then give to the Maori to settle a claim (and then over value the land) as Maori are a low % of the population in Christchurch compared to other areas of NZ.

They've already settled the Ngai Tahu claim.

A reader suffering from "quake-brain" asked me to post this link from the Canterbury Employers Chamber of Commerce commenting on assorted Christchurch issues. Kind interesting.

http://www.cecc.org.nz/main/business_information_forum/

This bit below from CEO Peter Townsend on the "elephant under the carpet" (ie. the insurance issues getting in the way of the rebuild) is quite interesting. He outlines 11 critical issues that need to put to the insurance industry for " some real answers."

- There needs to be some Government intervention in getting insurance companies to pay out in full.

- Part payments are being made with no details of what it is for or how it is made up. There needs to be clarity around partial payments.

- Insurance companies need the same information over and over up to three or four times. There needs to be clarity of process and accountability that claims have been received and acknowledgement of where they are up to in the claims process.

- Insurance companies seem to be nervous to pay out in case they break contractual obligations with their underwriters. As a result they are being too cautious and this is crippling payments.

- There is no information from the insurance industry on how claims are progressing. There needs to be reporting back into the community of progress with settling claims.

- A perceived lack of man power. Businesses are dealing with different consultants all the time. A lot of the consultants have been brought in from overseas and seem to leave after a short time. Is this because of tax implications? There needs to be Government interference regards tax exemption.

- No clarity around what constitutes loss. Businesses in the red zone are not being paid out because they cannot quantify their loss. However it could be 12 months or more before they can get to their businesses and in the meantime they have to relocate with no insurance money coming in.

- There is a knock on effect where people are waiting to be paid by insurance monies before paying their debts.

- Lots of promises but no delivery. Even insurance brokers are throwing their hands up.

- A big question – If you are in the red zone but have relocated, should you keep paying insurance on your old premises as well?

- A request to compile a list of tips on “how to deal with insurance companies”.

Gosh.... anyone would think the insurance companies are out to protect themselves from fraud!......

Gosh.... anyone would think the insurance companies are out to protect themselves from their customers, and their legal obligations!......

FTFY.

Maybe somethng for Gerry to show some leadership on?

TV3 should be commended for keeping these sorts of stories in the public eye. TVNZs coverage of the ongoing Chch problems has been poor, and appears they are more interested in stories that get ratings. I

thought the closeup interview with Gerry Brownlie was terrible, and you could see Gerry was close to tears. Obvioulsy he couldn't answer the question due to it still being negotiated, so why did the interviewer keep pushing and pushing like a bully.

Hey --- There's a reason it's known within the trade as 'One National Party News', and has been ever since the Don and Judy show of 2007. ;)

Perhaps the interviewer was wanting Gerry to pop his cork...man that would be some rumble....never seen an interviewer stuffed into a mic before!

Future full moon dates times etc.... http://www.rasnz.org.nz/SolarSys/lunarphases.html

EQC dealt with slips some years ago in the Otumoetai suburb of Tauranga, on an expensive street. OK it was small-scale compared with Chch, I think they retired 27 properties(might have the number wrong) which are now a park/reserve area, several owners commmented that they got top valuations.

Bums on seats!

"CHCH101 attempts to dive deeper into those experiences and formalise the reflection process in connection with other texts and readings from the world of volunteer service and community engagement."

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.