We spend most our working lives conscious of building a nest egg.

But what then? How do we make sure that nest egg sees us through 10, 20, 30 years of retirement?

The Society of Actuaries has released a report outlining four strategies it suggests New Zealanders consider as a guide to deciding how much of our retirement savings to spend each year.

In its paper, ‘Decumulation Options in the New Zealand Market: How Rules of Thumb can help’, it details different approaches, who they may be best suitable for, and what their pros and cons may be.

It poses its strategies based on the assumption a retiree has around $100,000 in a conservative or balanced investment fund (including KiwiSaver), receives New Zealand Superannuation and has some savings to call on in an emergency.

Its research indicates the median KiwiSaver balance of those aged 65 will reach $100,000 in inflation-adjusted terms in 25 years’ time.

Here are the Society’s ‘Rules of Thumb’ (in its own words):

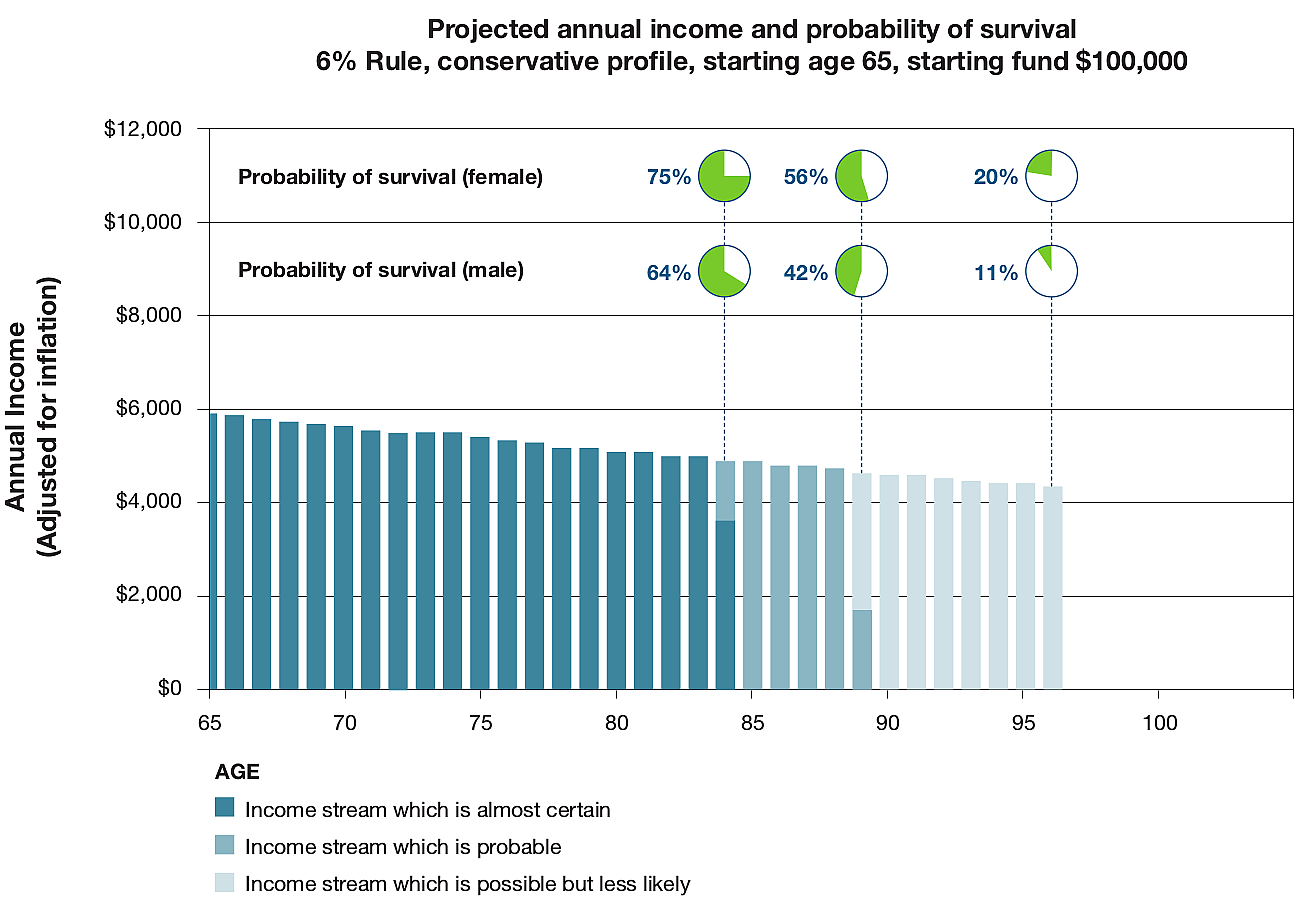

RULE 1: 6% RULE

| Rule | Most suitable for | Pros | Cons | Inheritance |

| Each year, take 6% of the starting value of your retirement savings. | People who want more income at the start of their retirement, to “front-load” their spending, and are not concerned with inheritance. | Very simple. Known, regular income. |

Income will not rise with inflation. Risk of retirement savings running out within lifetime. |

Average inheritance low if drawdown commences at age 65; larger if it commences at a later age. |

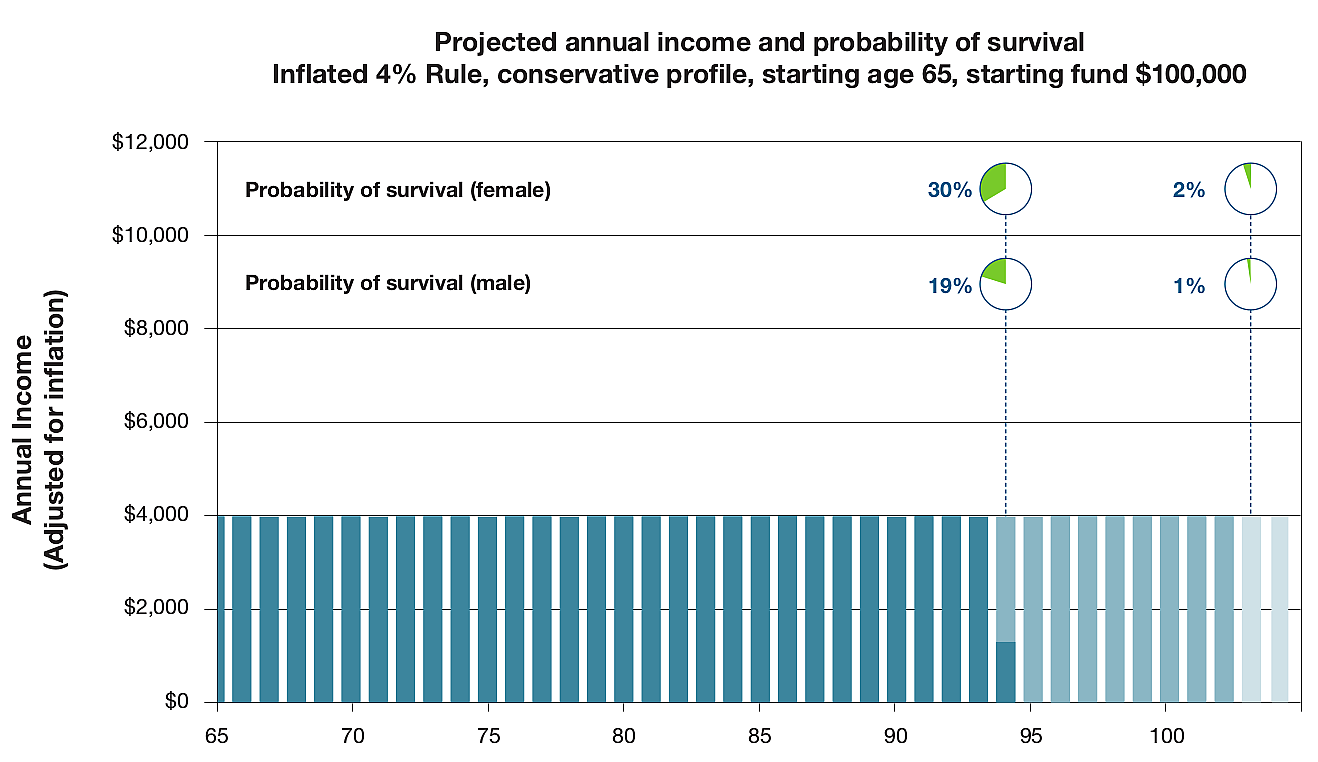

RULE 2: INFLATED 4% RULE

| Rule | Most suitable for | Pros | Cons | Inheritance |

| Take 4% of the starting value of your retirement savings, then increase that amount each year with inflation. | People worried about running out of money in retirement or who want to leave an inheritance. | Fund likely to last a lifetime. Income will rise with inflation. |

Lower income than other options. | Inheritance payment likely and average inheritance amount large in relation to starting value. |

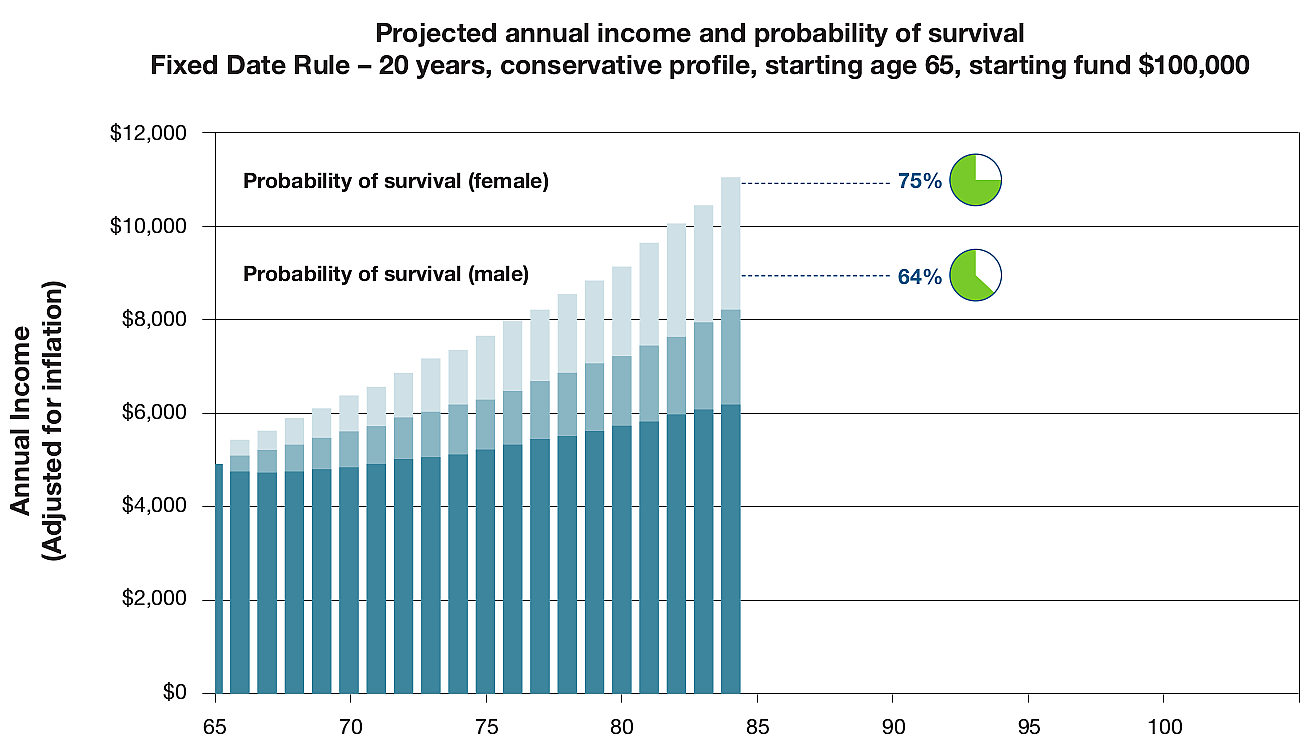

RULE 3: FIXED DATE RULE - 20 YEARS

| Rule | Most suitable for | Pros | Cons | Inheritance |

| Run your retirement savings down over the period to a set date – each year take out the current value of your retirement savings divided by the number of years left to that date. | People comfortable with living on other income (for example New Zealand Superannuation) after the set date. Those wanting to maximise income throughout life, not concerned with inheritance. |

Income for a known selected period. | Amount of income varies from year to year. Annual calculation necessary. |

Lowest average inheritance amounts. High probability of no inheritance, especially if selected date is age 85 or earlier; average inheritance amounts greater when selected date is later. |

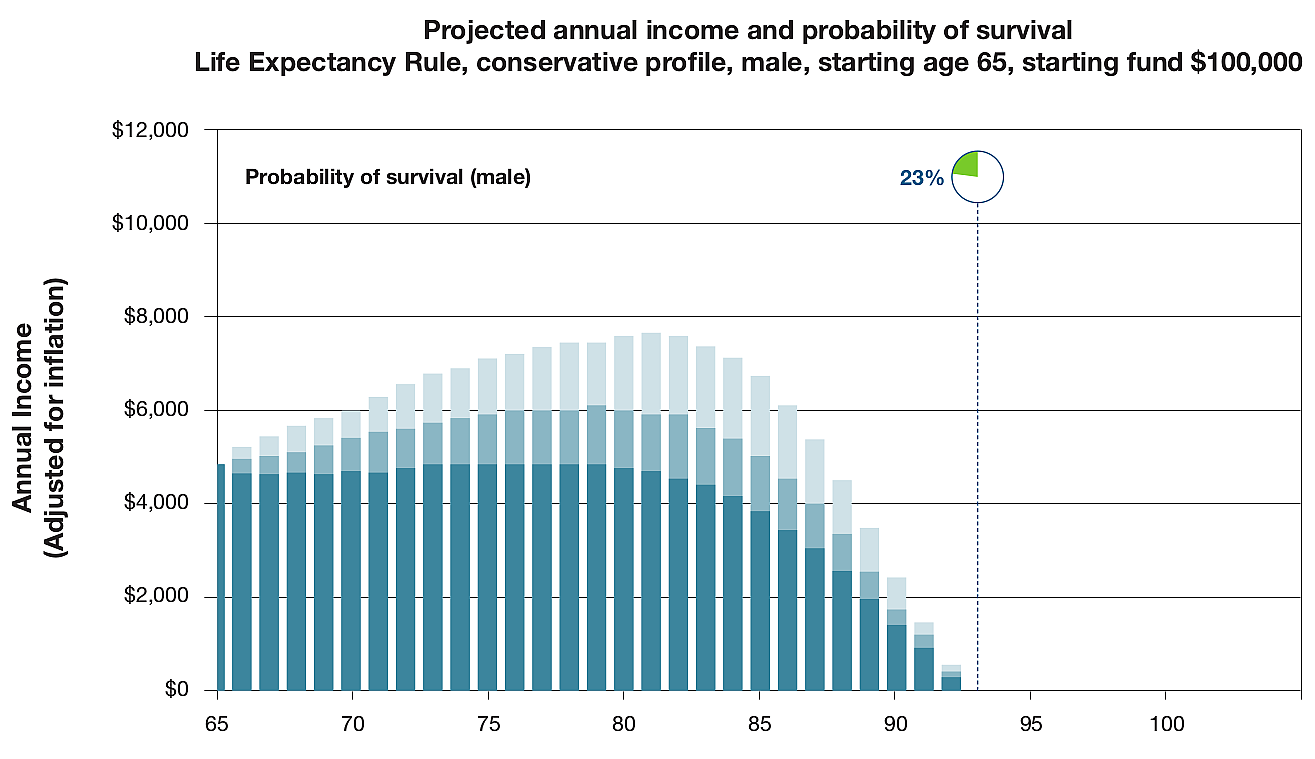

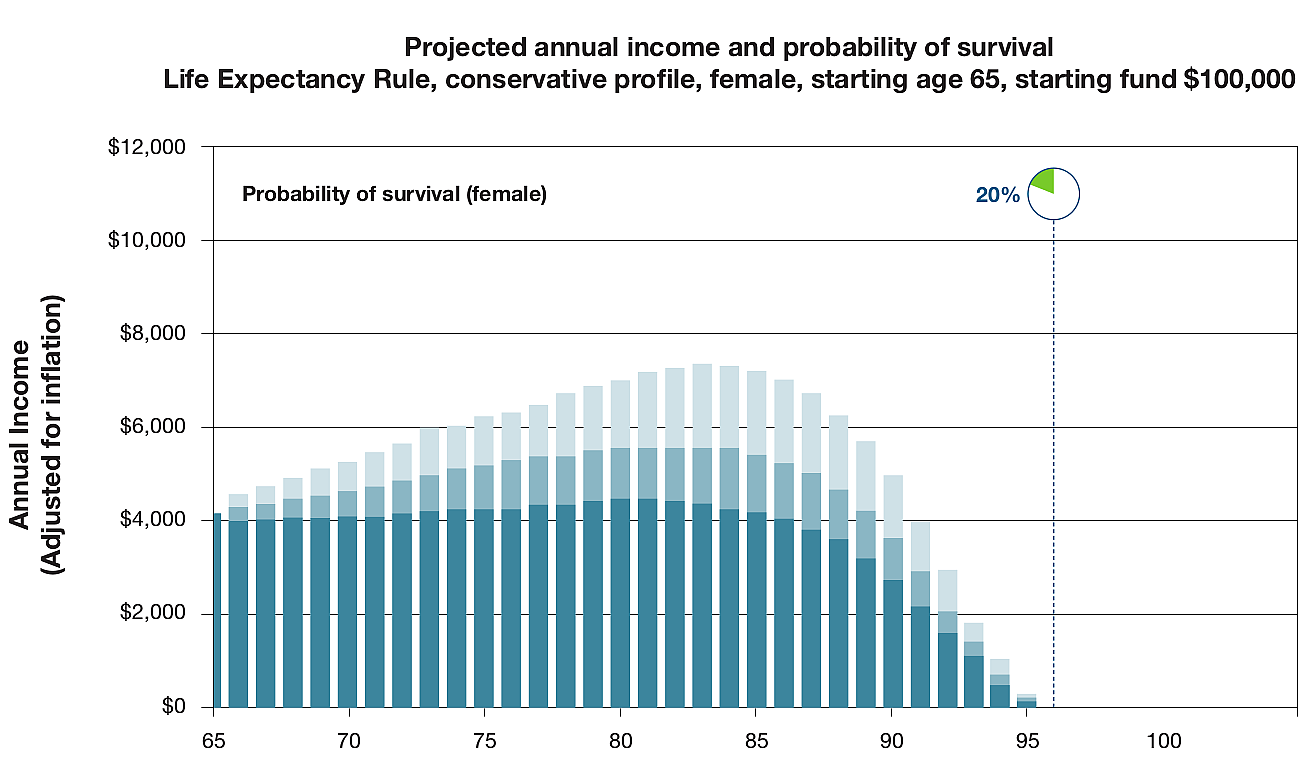

RULE 4: LIFE EXPECTANCY RULE

| Rule | Most suitable for | Pros | Cons | Inheritance |

| Each year take out the current value of your retirement savings divided by the average remaining life expectancy at that time. | Those wanting to maximise income throughout life, not concerned with inheritance. | Efficient use of fund to provide income for whole of life. | Amount of income varies from year to year; low in later years. Annual calculation necessary and relatively more complicated. |

Some inheritance normally paid; average inheritance amount moderate. |

While the Minister of Commerce and Consumer Affairs Minister Jacqui Dean has effectively endorsed the Society’s paper by launching it an event at Parliament, the Society says:

“We believe that Rules of Thumb will be most effective if there is a single set of Rules that is referenced widely and consistently.

“This set of Rules would be available to providers, distributors, regulators, commentators and others who communicate with New Zealanders on decumulation matters.

“There would need to be confidence in this set of Rules and we envisage the Financial Markets Authority approving a set of Rules for this purpose.”

For more on decumulation, see this interview interest.co.nz has done with the Retirement Commissioner. Diane Maxwell believes New Zealand's "love affair” with property is preventing our suite of financial products for retirees from growing as it needs to.

14 Comments

Excellent article, thank you. Really good to see some facts and figures instead of the usual waffle ``how much you will need to save depends on a number of factors''. Also interesting to see that $100K in Kiwisaver, while better than nothing, won't provide much in the way of retirement income: $4,000 per year is about $80 a week, and therefore assumes that NZ Super will still be the main source of income for most retirees.

Best advice: multiply everything by 10, and aim to have $1million in savings, plus a mortgage-free house. That should allow for a modest retirement. It won't be easy to achieve, and will be impossible for most.

Good article, but the key point is missed. If you are investing for 30 years plus, Conservative fund options aren't really conservative - inflation of even 2% will destroy value, and we are still at risk of inflation spike over that long a period. You are going to be hammered by inflation, and if the worst should happen and you are fit and healthy and want to be active in your 80s, you won't have the money. Invest in funds on growth settings, or if you are investing directly, perhaps include some listed property for more earnings than conservative funds plus inflation protection.

As Dave 2 says, the assumptions which are inherent in the returns made by the invested funds in this article are absolutely crucial. Going extreme may not be wise though.

Another huge factor is whether there will be an OBR event during this period. The defense: spread your funds very widely. Even if all the banks fail, hopefully there may be small sums excluded from the haircut at each individual bank.

You should only be holding short-term and emergency money in cash. The medium-term money should be conservatively invested and the long-term money investing in growth. With term deposits only returning about 1% after tax and inflation, you would be seriously limiting your retirement income by keeping your funds there.

Spot on, seems you also heard the RBNZ suggesting that in the event of an OBR RB would TRY & ensure every account had an availability of $5,000.

Don't be reassured by RBNZ saying it will "try":- remember in 2012 the RBNZ indicating that because of the OBR placing bank failure costs on depositors rather than the Government, they would be more tolerant of banks having lower capital (so placing even more risk on depositors). (See para 44 of the RBNZ's Regulatory impact assessment of Basel III in Sept 2012)

Say you have a mortgage free house and 100k each in Kiwisaver and in the Bank, when you reach 65. Super of about $1200 a month coupled with taking out $500 each every month from the Kiwisaver and the other savings, making it to a total of $2200 per month, won't that be enough for one person, for the next 20 years ?

Good to see this end of the retirement puzzle being addressed. As pythagoras, dave2, & uninterested say: 30 years is a long time and weird things may happen. I'd suggest staying diversified as long as possible and aiming to subsist on NZ Super, with extra spending calculated on realized past returns, not expected future ones.

Retirement is toast as a concept. Anyone who believes that there will be a surplus lying round in 30 years time to provide for retirees has to believe the world is not a fixed size. Either that, or they are under the illusion that a compounding interest graph on a excel chart can be eaten.

Note that the probability of survival means your chances of being alive

What are the chances of being alive and disabled in long-term residential care; how should this affect the equation???

I hate to say it, but probably a bigger house if your spouse is in better shape, to protect your assets for your beneficiaries, and throw yourself on the mercy of the state.

Good article. You do have to work out an approach to it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.