The New Zealand Superannuation Fund has unveiled a strong June year performance.

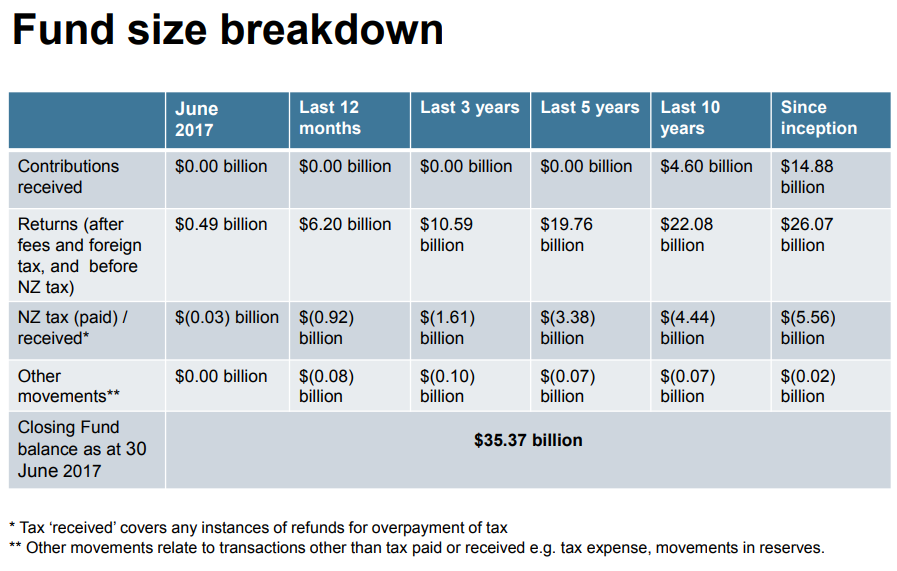

It returned 20.7% after costs and before New Zealand tax, swelling $5 billion to $35 billion.

Established by the previous Labour Party-led government to help meet the rising cost of superannuation payments to retirees, the Super Fund began investing in September 2003 with about $2.4 billion. The National Party-led government stopped making contributions to the Super Fund in 2009, with the Government having tipped in about $12.34 billion of taxpayers' money to that point.

The Super Fund is one of New Zealand's biggest taxpayers having paid $920 million of tax in the year to June 2017. We discussed this, and other issues, with its CEO Adrian Orr in this 2015 video interview.

Below is the NZ Super Fund's statement on its latest annual performance.

NZ SUPER FUND ANNOUNCES 20.7% RETURN FOR 2016/17

The NZ Super Fund has enjoyed one of its best annual performances yet, turning in a 20.7% (after costs, before NZ tax) return for the 12 months to 30 June 2017. It finished the year at $35 billion, up $5 billion on the year before.

Chair Catherine Savage said: “The Fund is generating world class returns and creating significant wealth for New Zealanders on a sustained basis. It should not, however, be measured on its short-term returns. We are here to create long-term value for New Zealand taxpayers. The Fund has now returned 10.2% p.a., more than double the cost to the Government of contributing to it,* over a period of nearly 14 years.”

The 20.7% annual result reflects a sustained rally in global equity markets, and resulted in the Fund paying a record high $1.2 billion in New Zealand income tax for the financial year.

Ms Savage said the Fund’s active investment strategies had performed strongly during the year, adding value of 4.4% ($1.3 billion) over the Fund’s passive benchmark. “Over the long term we expect to beat the passive benchmark by 1% p.a., so this has been an excellent year.”

She said the Guardians’ strategic tilting programme, in which it adjusts the Fund’s exposure to different asset classes; its significant investment in North Island forestry business Kaingaroa Timberlands; and the Guardians’ internally-managed credit mandates, were the key reasons the Fund beat the passive benchmark.

Since inception in 2003, active investments by the Guardians have generated an extra $6.2 billion (1.4% p.a.), over what an entirely passive strategy would have done.

Chief Executive Officer Adrian Orr said the Fund continued to be heavily weighted towards growth assets. “A long investment horizon and low need for liquidity give us some unique advantages in the investment marketplace both in New Zealand and overseas. Our active investment strategies and strong weighting towards growth assets exploit these advantages in a disciplined and cost-conscious way.”

Fund volatility was within expected parameters and the amount of risk being taken was appropriate, he said. Total risk at the Fund level, and active risk taken, had both been reduced over the year as markets continued to rally. “The returns we have been achieving are above our long run expectations, and we are cautious about the outlook,” Mr Orr said.

“As a long-term, contrarian investor the Fund has the ability to look through and profit from market cycles. While global growth prospects are currently quite encouraging, should markets drop we are well positioned to capitalise. The Fund’s expected returns over the long term (rolling 20 year periods) remain at around 8% p.a.”

Fund ranks highly in CEM survey

The latest CEM survey of international pension fund cost effectiveness ranks the NZ Super Fund highly, relative to a group of its peers, for net value add. CEM put the NZ Super Fund at the 100th percentile for net value add over four and five year periods. The NZ Super Fund also ranked well on cost measures, lower than the peer group average and trending down over time. The CEM survey, which is as at 31 December 2016, is available at https://www.nzsuperfund.co.nz/

documents/cem-survey-2016 .Summary Results as at 30 June 2017

2016/17 Financial Year:

- Total Fund returns: 20.71%

- Estimated $ earned by active investment: $1.28b

- Estimated $ earned relative to T-Bill return: $5.56b

Since Inception (September 2003):

- Total Fund returns: 10.22%

- Estimated $ earned by active investment: $6.25b

- Estimated $ earned relative to T-Bill return: $19.09b

See our June 2017 Performance Report for more information.

* As measured by Treasury Bill returns. All performance figures are after costs, before NZ tax.

20 Comments

The Kiwibank "investment" will have detracted from the above results (Its Coremod event). Was the Kiwibank purchase voluntary or were they told to buy in? Probably doesn't matter. Its all crown holdings anyway but that does not detract from the scandalous waste of money that those IT (and Management) people presided over.

I have heard that when Chinese IT people make a ballsup, they just change their name and work in another town. Do people change their name like that in NZ?

Year - Actual - If National had Contributed $2.4b/year from 2009

2009 - 13.30 - 13.30

2010 - 15.60 - 18.42

2011 - 19.03 - 25.39

2012 - 19.00 - 27.75

2013 - 22.97 - 36.45

2014 - 25.82 - 43.67

2015 - 29.54 - 52.70

2016 - 30.10 - 56.15

2017 - 35.00 - 68.08

They would have got back $33.1b for the 19.2b invested. Assuming interest at 4%, that total cost of borrowing to invest would have been $23b, giving a $10.1b profit.

I staggers me that National are regarded by many as financially literate. I thought it was dumb in 2009 and still do. By not contributing $2.4 billion annually since 2009, those funds missed out on one of the largest market rebounds in recent history. As you have estimated. we are $10b or more (the govt cost is less than 4% per ann) worse off.

If any financial advisor did something akin to this, they would be unemployed.

And you watch what happens to it when we have another crisis.

I honestly think it's going to get pillaged.

Yes, a money grab to further stiff the future

Delivering for New Zealanders

Muldoon did that and whatever National leader in the future will do the same. If National was financially competent we would be a lot better off.

10B. Exactly the same amount of the hole the Taxinda party would have put us. Fortunately Newzealanders can see who are good economy stewards and who are not. National put us back in surplus and that's what counts.

Oh no $10b. Compared to the equivalent of $9b per year National increase public debt that's nothing. Too bad the $10b hole was a fantasy anyway.

Perhaps National shouldn't have put us in deficit in the first place.

It staggers me equally that so many people operate on a perfect hindsight basis in making such claims, like they knew where the markets were going to go. It also staggers me that anyone really thinks that a country should borrow money to speculate in the markets to try to grow its pension fund (I have always considered it that when you leverage i.e. Invest money you don't own). God help any Govt that does that and then faces a GLC event and experiences massive lose excentuated by borrowed funds, they would be toast on this site. The after the event experts are typically very poor investors themselves in my experience of observing a multitude of them over the years.

.

Grant.

The NZ Govt has access to funds at a comparatively low cost on the international markets that you I and could never access. The negative gearing risk is relatively slight, when the market has already dropped 50-60%. Think dollar cost averaging, it works for ordinary punters, it can work for bigger players too.

This country has borrowed money for all sorts of projects for several decades where the true return has been negative. The lost opportunity I described above in comparison was a gift that was never taken because of a neoliberal mindset that opportunity (and risk) is best left to private players. Governments (and taxpayers) are meant to stay out of that opportunity zone. The corollary of that bias is that losses inevitably get to be socialised anyway. Instead of a win - lose risk profile for the tax payer its a lose -lose scenario.

In the event of a major crisis that drops markets sufficient to wipe out 70-95% of govt and personal wealth in NZ, priorities will shift to basic survival. What the NZ Fund or what ones KiwiSaver is worth, will be somewhat unimportant.

Macadder - I understand your points, but I do see a bit of difference between investing/speculating in an attempt to have sufficient money in the bank to meet pensions, than say the much criticised, but I would have thought more justified, think big type infrastructure projects that would generate returns over a very long-term period, plus provide some security of supply etc.

Yes timing would have been perfect and I can't argue against that having been an investor towards those lows, but of course if you run a policy of borrowing to invest would the Govt do it right now with markets globally at or near market highs? ..but as we also know well, with interest rates still likely low for a fair while longer, the equities boom for instance could conceivably still have more legs to go - so do we always "average in" with borrowed funds regardless, or expect the Govt to pick the period based upon its superior forecasting skills ?

"It staggers me equally that so many people operate on a perfect hindsight basis in making such claims, like they knew where the markets were going to go."

Um, the consensus is that over time markets go up, this is not in dispute. One does not invest if one does not expect an upside.

With sharemarkets returning a total real return of 7%/year (after inflation, dividends reinvested) and the government able to borrow at a real 1%/year then this should be a no brainer in the long-term. Yes, there will always be ups and down in the short term but the long-term trend only goes one way.

Everyone talks about the 1987 crash. Here is a graph of the S&P500 total return (change dropdown for real total return). http://thume.ca/indexView/ 1987 is a tiny blip historically and any money invested at the peak then would have gone up 7-fold after inflation.

Time in the market is the most important thing and thanks to National, we have lost 9 years.

So, Mac, have you borrowed heavily to buy shares lately??Or did you in 2009?

Anyone who has a mortgage and owns shares has borrowed to invest (although likely structured it poorly for tax deductibility)

Dollar Cost Averageing - thge simplest form of investing and the Nats managed to F4%k it up.

They have similarly castrated Kiwisaver. Both Labour pearls.

Pissup / Brewery.

Kiwis so dumb lah!

DCA is going on Smalltown, it happens every time a NZer puts a dollar in - Whats that's got to do with National in less you think borrowing to have that extra dollar is a guarantee positive?

Authentic frontier gibberish - have you been hacked GA?

"Dollar-cost averaging (DCA) is an investment technique of buying a fixed dollar amount of a particular investment on a regular schedule, regardless of the share price. The investor purchases more shares when prices are low and fewer shares when prices are high."

Smalltown - from my post what makes you think that I need a lesson on something as basic as DCA ? Did you mis-read the couple of sentence before you felt like a rant ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.