This week in tax, we’re going to be talking to Andrea Black, the former independent advisor to the late Tax Working Group and author of a very good blog on tax – it’s the best blog on tax, in fact – called “Let’s Talk About Tax NZ” talking to her about the workings of the late Tax Working Group.

TERRY BAUCHER:

Kia ora, Andrea! Welcome!

First up, what was your role within the Tax Working Group? How did you interact, and it interact with Treasury and Inland Revenue?

ANDREA BLACK:

My role was to provide independent assurance to the Group that officials advice was right and where I disagreed I would provide alternative advice. That could be written or orally at the meeting.

I largely worked alongside officials as they were preparing their advice. When it came time to draft the reports there was a lead official – Bevan Lye – and I worked with him and at times I would provide alternative text for the Group to review.

I would also largely be the bridge between the Group and officials in refining text for the reports.

TB:

It sounds pretty much a full-time role though for you, wasn’t it?

ANDREA BLACK:

About 25 or so hours a week but it took all my emotional energy (laughs)

TB:

I would say it would. I mean, enormous input. What I saw there from my brief contact with it was there was just an enormous amount of work going on. I mean, how big was the secretariat working on it?

ANDREA BLACK:

I think about 10 people as core but I read somewhere up to 75 as specialists got brought in for particular topics.

TB:

Yes, there’s quite a bit of work there. We’ll come to that a bit later on.

What surprised you during your time with the Tax Working Group? Were there any really big surprises?

ANDREA BLACK:

First thing was a good surprise. I was employed after the Group has been appointed and when I saw big 4 partner, chief economist CTU, ecological economist, head Air NZ tax … I though wow this is going to be interesting particularly since I would have a role in shaping a consensus. But everyone was great. There were differing views but everyone was genuinely interested in each others views, engaging and looking to do the job the government gave them which was reviewing the structure fairness and balance of the tax system.

The other nice surprise was the level of submissions. 6700. From lots of groups and people that wouldn’t normally be anywhere near a tax consultation.

TB:

It’s interesting to hear that as well because much has been made about this all – the minority view of that – but, as I said somewhere else, you know, tax specialists, we’ve all got big egos, to be frank, so we’re always arguing. It is the nature of the game. We’ll split hairs readily, so that’s really encouraging to hear.

ANDREA BLACK:

That’s true and I know exactly what you mean Terry but I didn’t see any of that with the Group.

TB:

I mean, that minority view, that’s not an unsurprising view because that’s been the view of Inland Revenue. Certainly, if I was to categorize this agency a little bit, they’ve always taken the view about the difficulties around introducing a capital gains tax.

ANDREA BLACK:

I am not sure that is still the case but I can't speak for Inland Revenue.

TB:

Yes, that’s interesting to hear.

Just moving on, did preconceptions change for you during the process?

ANDREA BLACK:

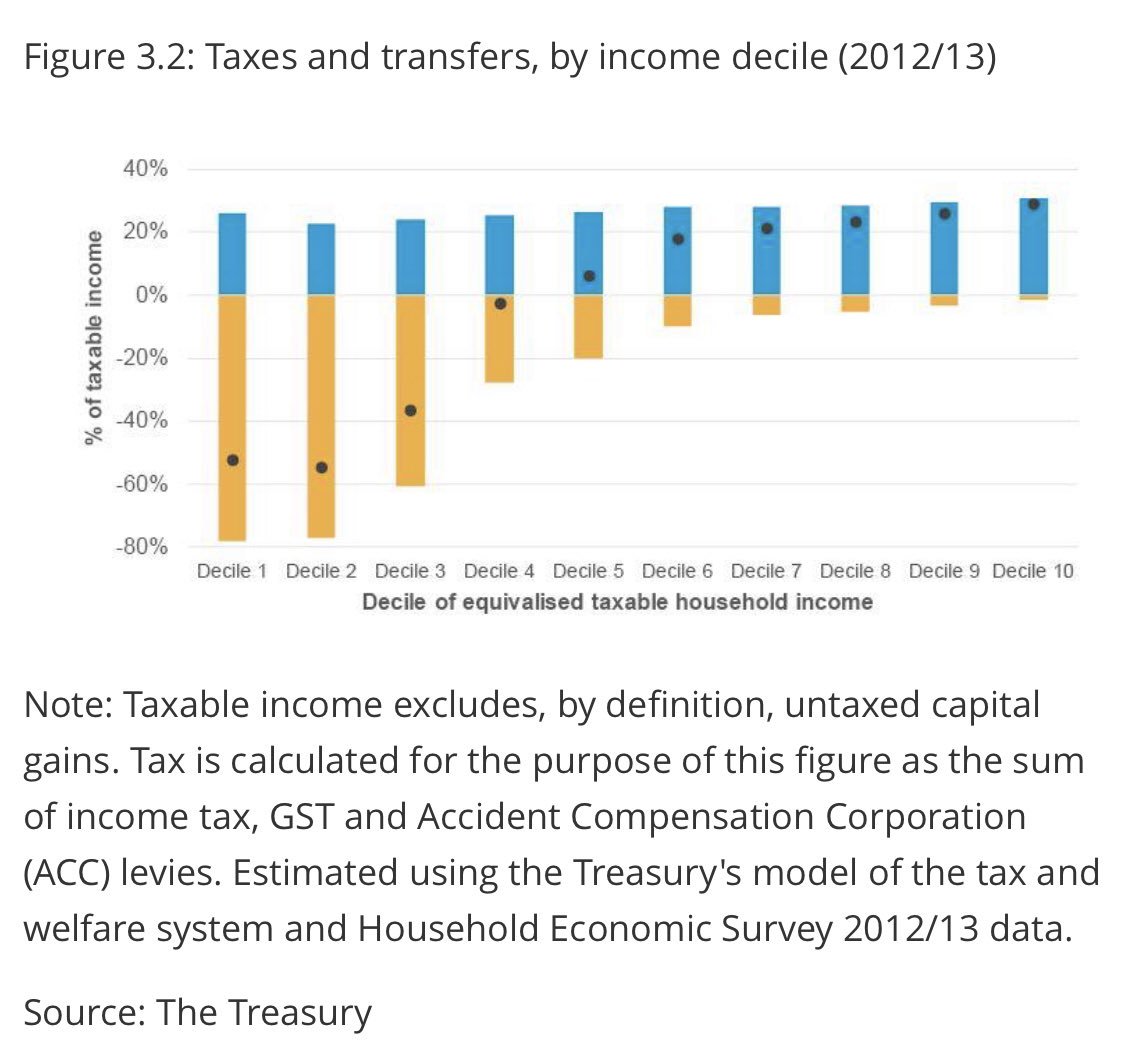

My main thing is that I always thought the tax system was progressive. I guess that comes from spending my life in income tax and international tax at that. I was quite frankly stunned to see that the bottom deciles paid something like 23% tax when you include GST and the top deciles something like 32%. And all of that is before you add in untaxed capital gains so the top decile could be even lower than that.

If I could give a shout out to two exceptional papers by the Treasury on all the distribution stuff. Really worth looking at.

https://taxworkinggroup.govt.nz/sites/default/files/2018-09/twg-bg-distributional-analysis.pdf

TB:

That’s fascinating.

I guess that’s one area where everyone has said nothing much has changed – you know, business as usual, waste of time. You know, KPMG Tax Partner Bruce Bernacchi was on Breakfast TV saying, “This was a complete waste of time.”

I disagree with that because I think one of the things that tax working groups throw up every time they get into it is all this sort of background work which highlights issues which we have taken for granted or pushed aside or we’re just unaware of what needs to be done.

What you’re saying is that could be something that the government can look at regardless of what this whole flagship of capital gains tax being part indefinitely. Or at least for ten years it would seem. Would you agree with that?

I’m thinking, also, you had worked within the living standards framework as well. That would definitely seem that there’s something there that should be moving up the policy pile.

ANDREA BLACK:

Yeah we had a good go at applying the living standards framework. The idea was that the living standards framework would be applied first to give the direction of travel and then the more traditional principles of efficiency equity and so on for analysing particular policy choices.

And of course there is some overlap. Social capital speaks to fairness or equity which in turn speaks to social license and ultimately voluntary compliance.

Oh yes and the four capitals are financial, human, social and natural capital. Also known as money, people, the community and the environment.

TB:

That’s a nice way of putting it.

I know, for example – just as a quick aside – that, on the Small Business Council, we are working within the living standards framework, but I think you, the Tax Working Group, took that much further, and something was of interest to me. It had provoked controversy from the rednecks which is unfortunate but typical about Te Ao Māori. Do you want to have a quick word about the role of Te Ao Māori and the Tax Working Group? Because I think it’s something that’s not being talked about. Just a quick overview because I’m thinking it would be very interesting to hear about that.

ANDREA BLACK:

That was something the Chair was very keen on and it was led by Hinerangi Raumati a member of the Group and a very able senior Treasury official. There was a lot of thinking done and a paper commissioned from Sacha McMechan.

However as I ‘worked to the gaps’ and this was being handled very well other than recommending reading the papers – I can't comment very competently on it.

TB:

No, I appreciate what you say on that because it’s something that I think would be actually good to speak with – you mentioned her name on who was on the working group about that. I think it’s a fascinating thing probably worthy of a podcast in itself.

ANDREA BLACK:

Absolutely.

TB:

And you mentioned a chair there – Sir Michael. Of course, he’s a vastly experienced politician and a long-time finance minister. He seemed to me as a chair that managed the whole process, given what you said earlier about how the group collaborated extremely effectively, that’s attributed also to himself in corralling and moving things forward. That’s my personal view.

You had gotten to work with him quite closely as a consequence, I presume?

ANDREA BLACK:

Yes. Is there a question there Terry?

TB:

One thing he mentioned, I asked him directly about the surprise for him in the process – of course, given his experience – he responded that he was amazed to find out that 60 percent of all charitable donations are made to religious organizations. That’s something that’s actually one of the priorities for the group for the policy process moving forward. What is going on in this space? Because you (0:20:12 unclear) more about what the tax grouping book found in that space. It’s quite fascinating. I thought.

ANDREA BLACK:

I think that was a personal view of the Chair.

Oh the charities stuff. I think what the Group did there was quite interesting especially with the whole charitable businesses thing. There is a theory or idea called competitive neutrality which says that the tax exemption doesn’t matter as charities will still charge market prices as they will effectively bank the tax exemption. Because if they can earn passive income and not pay tax why would they want to earn less with business income. And so the tax exemption doesn’t matter. But then there is also the thing – and this came out in the 2001 charities review that if the charitable business doesn’t pay tax it can grow faster. But then if it borrows it costs more as they don’t get the benefit of the tax deduction.

And it this point normal people start to spin out.

So what I thought the Group did well was to cut through all of this and focus on the distributions of the charitable business. Because ultimately the tax exemptions are given to benefit New Zealand society not to benefit the charitable business. And so if the charitable business distributes to charitable causes it ends up being the same as another business that pays tax.

And then all the pointy headed stuff disappears.

Where it gets tricky though is that there can be situations where not distributing is the right thing for the charity’s objectives. Like red cross for example it is reasonable to not always distribute if it needs to save money for a disaster.

And then that all gets quite micro as to when it is ok or not and really the best people to determine that is Charities Services at DIA. So what the Group said was – as there is a Charities review on – the government should let that go ahead and then look again to see if it all made sense from a tax perspective. And if not look to make change then. After the DIA review is done.

TB:

I saw that the group got quite a lot of submissions. From time to time, that is a point of discussion about what’s going on with the charities and the unfair advantage, but I think the approach that the group took was to look at the distributions, the end point, the whole purpose is the best approach. As you say, it cuts through all some pointy-headed stuff.

Returning to your preconceptions as you progress through the thing, well, I guess, coming onto it now, now we know the government’s response. What would be – without telling tales out of school – your biggest disappointments of you’ve seen or what’s gone forward as recommendations?

ANDREA BLACK:

While I have a few disappointments (laughs) most of them I understand from the politics of it all. I am not quite sure what it is with New Zealand and capital gains – it is almost like our third rail.

But the one that really stuns me relates to the Group’s recommendation for a Tax Advocate which would be a departmental agency reporting to the Minister.

The idea behind it – the presenting problem – was that small business or taxpayers when they find themselves in dispute with IRD will concede rather than take the dispute because the dispute system was all too complicated and expensive. So they just pay the tax even if they are right.

The idea was the Tax Advocate which would be a paid position would have a group of retired practitioners helping out on a pro bono basis. And interestingly CAANZ were strongly supportive of it which I thought was interesting given their members would normally be the ones such taxpayers would turn to. But the more I thought about it their support made sense as it was all about taking noise out of the tax system which benefits everyone. Taxpayers Agents and the Revenue.

And also as I thought more about it In my time in the field I ran into taxpayers who were adamant they were right about an issue and they just weren’t. I could also see merit with the Independent advocates who could explain this to taxpayers. And maybe even when IRD ran projects they could get the advocates in, explain what was going on and who to contact if they had issues. I saw it as a win all round.

So while the presenting problem was small taxpayers who were right conceding incorrectly- I also saw benefits to the Revenue for the opposite situation.

TB:

That’s a really good point. That’s something that the former inspector general of taxation in Australia (the equivalent of an ombudsman) and I talked about and he made a similar point saying that these are independent agencies.

Government agencies such as Inland Revenue might see them as a rival for want of a better word or something that might compromise them. He saw them as actually, for the very example you’ve given, a potential strength for Inland Revenue when they say, “Actually, these guys are right, so you’re just going to have to suck it.”

ANDREA BLACK:

I don’t think I said IRD opposed it. It was a decision made by Ministers. And as I say it really really surprises me. I could understand that it could all be too much for the work programme if IRD was also implementing taxing more capital gains but as that isn’t happening. I don’t get it. I have OIA'ed the Minister of Revenue for advice leading up to the decision so it will be interesting what comes of that.

TB:

I see, actually, that there is work on a sort of simplified disputes process for smaller businesses. It’s still on the web program, but not a priority.

ANDREA BLACK:

Yeah I am not sure how that is going to work as I did the paper for the working group and it was all predicated on their being a Tax Advocate in the first instance.

TB:

From that, Inland Revenue, as we both mentioned probably would not have been terribly keen on a tax advocate as a potential. Now, you might not say that, although I would, but it comes to a point that was raised by Bruce Bernacchi of KPMG on TV – TVNZ, Breakfast TV.

Basically, he said, “Well, there’s nothing much to see here. At the end of the day, business as usual for Inland Revenue.” He said two points. One is he thought Inland Revenue is possibly a bit overmighty at this space – in the policy space but, at the same time, it was under-resourced.

What’s your take on that?

ANDREA BLACK:

Overmighty. I am not sure that is quite fair. Tax policy is the responsibility of Treasury and Inland Revenue it’s just that over time Treasury’s input has varied. For example, when I started at IR policy in 2000 there were like 4 teams at Inland Revenue and 2 teams at Treasury and they had 2 managers and a director. Then Treasury did a restructure in like 2002 and reduced their involvement down to one team and a manager. Now I think IR has maybe 6 teams and Treasury one. My observation is that Treasury’s involvement has waxed and waned over the years but that as it has waned Inland Revenue has waxed.

TB:

You were saying about the question of Inland Revenue perhaps being under-resourced.

ANDREA BLACK:

Yes. I mean, that comes up quite often.

In my view, the tax work program, the kind of demand for legislative change is very similar to the demand for health services. It’s largely infinite. You can increase tax policy resource. I’m going to say it like that rather than Inland Revenue. But, ultimately, there’s only one minister, there’s only one cabinet. I mean, while the private sector is kind of large, there’s only kind of one private sector that can comment on everything.

I’m not sure that necessarily increasing Inland Revenue’s resource is the thing. I think what people often mean when they say Inland Revenue needs more resource is that people are saying Inland Revenue needs to be working on the things that I want them to be working on. I think it’s just one of life’s tensions in trade-offs and that is for the minister and cabinet to prioritize the issues they want their officials to work on.

Also, there’s the other issue because there’s the tax policy work programme but the there’s the government’s work programme in total and how much of the government’s work programme do they want tax to be part of because, again, the cabinet has only got a certain amount of bandwidth, so how much do they want tax to be part of that?

TB:

Finally, was it all worthwhile? This was a year of your life – more than a year of your life!

ANDREA BLACK:

More like 17 months of my life.

Was it worthwhile?

I’ve had a bit of time to reflect on that. The way I would look at it is the tax system is really, really important in terms of government and society. And so, in my time in tax, it seems to be, when you get a new government, you get a tax review in some sort – an independent tax review.

I think that it’s right and I think it’s right that the new government should start their term in office with a review of the system that’s going to bring in the money for them to do things. I think, inherently, always having every sort of ten years or so an independent look at the tax system, I think, is a very good idea.

Now, in terms of the comments of what’s come out if it is a lot of business as usual, the inference behind that is that that’s somehow bad when another way of looking at it is, yes, the government has said a lot of things are being worked on, but isn’t that good? Isn’t it good that the direction of tax policy is largely fine?

There are lots of things that are being worked on like withholding taxes for contractors and things like that which will have a huge impact on the hidden economy. I’m speaking personally, my first time in the tax system property. You know, I had withholding taxes come out of my money. Brilliant. I’d hate to think what would have happened if I’d had to kind of manage it through provisional tax.

There are a lot of things going on already, so I think just because there’s not major change did not mean that it wasn’t worthwhile. I think having an independent look is good, and I don’t see that a lot of the things that have been adopted are already business-as-usual is bad. I think, actually, it’s great and we can take a lot of comfort that things are going in the right direction.

TB:

Fantastic.

The final comment on the nature of a Tax Working Group, you actually work now and have been involved either through Treasury, Inland Revenue, or as an independent advisor with the last three tax working groups. Would that be right? And this would be possibly the most substantial of them all, would that be fair?

ANDREA BLACK:

I don’t know if it’s my involvement.

I was a junior during the 2001 working group. I was in the field during the 2008 one.

I think it’s comparable to the 2001 working group because they went back to first principles in a lot of cases. I think, actually, a lot of the concern was that this working group wasn’t duplicating the work of the previous one. I don’t think it was any more substantial or whatever than any of the others. It’s just more recent.

TB:

The 2010 group – the Bob Buckle-led group – which reported in 2010 suggested that there was perhaps a need for a permanent working group on these areas. What are your thoughts about that?

ANDREA BLACK:

Well, if you actually want independent people, I don’t think you can make them permanent because the advantage of this group is that they were knowledgeable people, but they weren’t insiders. If you start becoming permanent, how are they different to the officials? Or how are they different to senior officials who were reviewing work?

I think there’s a lot to be said, for every new government, a really good look because it is a lot of time and a lot of kind of emotional and intellectual bandwidth. It’s not something that springs to my mind as being necessarily a desired state because, also, if you think about it, the members are quite different from the 2001 to 2008. It’s good. Each government can kind of put their glass or their direction on the types of people they want to do the reviewing.

TB:

Fantastic.

Well, thank you very much, Andrea! It’s been an absolutely riveting episode, I believe.

If you’re a tax nerd, it’s really, really interesting to hear your side of things and a brilliantly different perspective on what’s going on is the point about the mix of how the group worked together, the living standards framework, and particularly just how progressive our system is. That alone shows that there’s still scope for what might be seen as quite radical change even though it’s not – for want of a better word – a snappy thing such as a capital gains tax. That’s been fascinating.

This article is a transcript of the April 26 edition of The Week In Tax, a podcast by Terry Baucher. This transcript is here with permission. You can also listen here.

5 Comments

Aren’t the bottom decile net tax consumers? How does that 23% figure come about?

They pay income tax and GST first and then depending on eligibility they may or may not receive additional financial assistance. For example somebody receiving the unemployment benefit pays income tax on that income and GST on purchases. They may receive no other assistance. At the other end of the scale I recall a client who earned a top decile salary, made a capital gain on the side, made a "bad/wrong" business investment, still earned a top decile salary albeit in a different form and because of how it's been arranged not only does not suffer consequences of bad decisions as some here believe should be the case, but will pay no tax other than GST for the rest of his life. What is a net tax consumer? Be careful how statistics are reported and be able to read through the bias and spin.

Thanks for your comments. Here is the graph Andrea mentioned during the podcast. The blue stuff is tax.

{kind=link}

Seems pretty pointless to look at the tax collected in isolation from tax returned in form of various benefits ( once that is factored in the bottom decide becomes "net consumer" of tax , and some ) .

Pretty pointless - unless the aim is to obscure the true state of things - which I think is the idea .

Him paying no tax other than GST for the rest of his life makes it sound like GST is the way forward.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.