The New Zealand property market in May could well be called a “tale of two islands,” with a relatively buoyant South Island while the North Island appears largely to be in a holding position, according to realestate.co.nz.

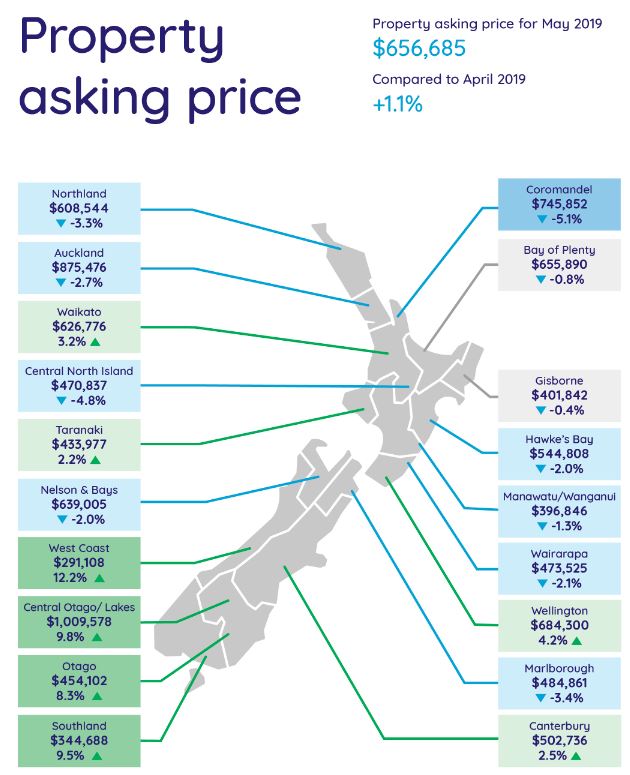

Nationally, the average asking price in May lifted +1% to $656,685 from April. However more than half of the North Island regions registered asking price falls (seven of twelve). The exceptions were the Waikato and Wellington regions with all-time highs, the Bay of Plenty and Gisborne remaining static, while Taranaki saw an increase of +2%.

“This is in stark contrast to the South Island, with five of the seven South Island regions registering lifts in average asking prices. An active Central Otago/Lakes region tipped back over the one-million-dollar price tag and two other regions hit new record asking price highs,” says spokesperson Vanessa Taylor.

Auckland languishing, unsold inventory at seven year high

The Auckland region’s average asking price fell almost -3% from the prior month to $875,476 while new property listings fell almost -4% compared to May 2018 (3,398 new listings).

Total inventories rose +11% when compared to May 2018, up to 9,997 residential listings. At 28 weeks of inventory, this level is the highest for a May in Auckland in seven years and weighs heavily on this market.

“With stock sitting around longer, people will be looking to whether they need to be more negotiable on price, particularly as they will be selling and buying in the same market,” she says.

Housing inventory

Select chart tabs

All-time asking price highs in Otago, Southland, Wellington and Waikato regions, since records began in 2007

While the Central Otago/Lakes region’s average asking price lifted, it was the neighbouring regions of Otago and Southland which hit all-time asking price highs since realestate.co.nz records began 12 years ago.

The average asking price in the Otago region rose +8% to $454,102, while Southland’s average asking price climbed +10% to $344,688.

The Central Otago Lakes region remains strong, no doubt because Aussies are not restricted from buying, unlike other foreigners.

The Wellington region’s average asking price has been hovering in the mid-$600,000s during the first four months of this year, but in May leapt to an all-time high of $684,300 (a +4% rise on the previous month).

However in May, the total number of homes for sale in the capital city (1,244) was well up on the same period last year (+18.4 per cent), although there was only a modest increase in new listings (724) representing a 2.4 per cent increase on May 2018.

Further north it was a similar picture for the Waikato region.

The region hit an all-time high in asking prices (up +3% to $626,776) compared to the previous month. New listings were up +4% to 751 new listings, as was the total number of homes for sale, up 15%.

110 Comments

Asking price falls of 2 3 4 and 5% over the course of a month is not really a ‘holding pattern’ - as the saying goes ‘You can’t polish a turd, but you can roll it in glitter but even if you do, it still smells bad’

Calm down Wilkes, it's likely mainly seasonality.

It's not necessarily seasonality. Let's look at previous years to see what the April -> May seasonal drop was as comparison.

I don't have historical average asking price data available, so I'll used Auckland median sale price instead. In 2018, median price fell 0.5% from April to May, in 2017 it went up 0.8%, and in 2016 it went down 0.7%. I'd say that those deltas are small enough for -3% to be notable.

I'm not saying that the Auckland market fell 3% in one month, because asking price isn't the same as sales price, but there may be more going on here than just seasonality.

Don't compare asking price and median price. They are two very, very different things.

Aside from seasonality it can be down to other things such as mix. The point being that a 'shock' drop of "2,3,4" % in monthly figures isn't really cause for hyperbole.

In the absence of other timely data, I'll happily compare asking price and median price trends with the usual caveats. I think there's signal there, but there's also noise. That ratio of signal to noise will of course be revealed once the REINZ figures are released in a week or so...

There's a signal, but without an understanding of the noise you don't know what it is.

A reduction in asking prices could be correlated with/determine unchanged or higher (aggregate) median prices. (Should be thinking of quality adjusted prices, anyway)

The ratio of signal to noise? It's not possible to estimate the variance ratios from broad REINZ data.

Asking price encompasses loss aversion and various other non market vendor factors.

Transaction prices represent arms length (mostly) market prices. Like I said; very different things.

How about the REINZ Housing Price Index, down 4.4% YoY in April. Does the "gold measure" of housing prices count at all?

Will be interesting to see it for May, whether it also is "lightly seasoned".

We aren't talking about the HPI. We are talking about frivolous comments made about monthly variance in asking price moments.

Considering the May results does not remove the seasonality.

Just pointing out that results have been relatively aligned in the direction they've tended to point. Very few seem to be pointing North.

Hi Nymad

Here’s an article for you... made me smile.

‘How to grow household debt exponentially!’ Lessons from NZ. Believe it of not lil ole New Zealand policies are now being touted In the UK. We should be proud.. first we came up with the idea of 2% inflation targeting (yep, that was us) you just have to forget about the housing being measured in the CPI - distorts the numbers too much and could lead to a need to raise rates. Second, I’m not sure if we were first to introduce negative gearing allowances to prop it all up but it helps and doesn’t exist in many other places and third we are now an example to the UK for encouraging the stripping of retirement savings to underpin a housing bubble (not just first time buyers are doing that here) all to allow more credit growth - not sure how much further that that policy can last here though given the size of the KiwiSaver average fund (19k) 2.2% of a median Auckland home. We should be so proud for the ingenuity. No Debt to income restrictions (despite it being requested by the RBNZ during the term of the last government) .. no proportional limits on interest only lending and question marks over amalgamation of loans or not when reported to the regulators ... A shining beacon of household debt for the rest of the world to follow.

https://www.propertyindustryeye.com/housing-secretary-in-backlash-after…

Hi Joe,

Well that's a bit of a tangent from you. Dunno how it relates to the seasonality of monthly asking prices. But because I have a few minutes let's clear a few things up for you.

"How to grow household debt exponentially" - again, hyperbole for two reasons. The growth rate definitely isn't exponential - the rate of growth isn't growing in time (doesn't follow a non linear growth path). Alternatively if you mean total debt is growing exponentially, that is implied from any linear growth path. i.e ya don't need to say "exponentially" as it just confuses what you are saying.

Yes, NZ was the first to implement an inflation targeting regime. No, we didn't really come up with the 2% target - the initial PTA defined the price stability target band to be 0-2%. The 2% target sort of evolved as inflation targeting developed in western central banking systems.

Secondly, housing costs are currently included in the CPI.

If in fact you mean residential section costs aren't included in the CPI, you are correct. However, these were included up until 1998/1999(ish)? A search on Stats NZ should confirm exactly when - iirc it was Shipley era. It was another 6 or so years before rampant housing inflation kicked of in NZ, so it's a bit of a stretch to somehow, non empirically, link the two.

Negative gearing wasn't to 'prop it all up', it was primarily a vehicle for incentivising the private provision of rental housing. Very important when trying to transition from a socialised system. It is just a relic from that time. Not a good relic, but really only because housing policy has changed significantly from when it was introduced. This alone has not been what has propped up the housing market. If you ask me, it has had only a minor effect.

The real issues arise from, as you allude, deposit subsidies (be they kiwisaver, homestart, etc), and, most importantly, land use restrictions and construction constraints. In an elastic market, the deposit subsidies would have an, effectively, benign effect on price as the WTP increase signals a commensurate increase in supply. However, in the case of an inelastic supply arising from geographic and artificial constraints (and sheer incompetence), any increased ability to pay is capitalised into land value (relative to the respective supply elasticity, of course). Could a DTI have remedied this? Potentially. However the price is set still by the marginal cash buyer (of which there were a metric s**t tonne coming from a place rhyming with shinner), which has the effect of locking out the local low income buyer.

So, long story short. If you are going to go on a white knight campaign, make it primarily against the artificial restrictions in housing supply and extortionate construction industry. The credit growth is a symptom of this, not the other way around.

An excellent riposte Mr nymad and you’re correct in much of it.

I believe that the more media debate we have on issues (particularly here) the better NZ will be.. the media generally seem to be hamstrung by revenue issues/reliance on sponsors. Mr Chaston is graceful enough to allow comments that challenge here, that’s why we visit the site.

So many journalists seem to neglect the realities of what an unregulated banking sector can create.. we moan about the symptoms, as they are in OZ as well at present and theUK too for a decade, the issues of homelessness, divorce, depression, kids in poverty, wages not meeting the bills, food parcels ( just seen Tony Alexander on channel one talking about this and million dollar properties). etc etc

all are in my view symptoms rather than the cause and yet we spend billions of government dollars ( often raised by the cause), or through the labour of people at the margin to try and fight the symptoms. Backwards thinking perhaps? The debt is our biggest issue.. in business and households... as a country we produce far more than we need to eat and consume and yet so many are really marginalised. It’s a debate about where your kids end up and mine in the future. I’d like mine to stay here!

No white knight, just understand the bollocks better than most.

Joe Wilkes

J W, and what do you make of the rising asking prices of 8, 10, 10 & 12% you conveniently omitted from you post?

Just checked out Homes . co .nz. Big drop this month in values. Some of the houses I have been watching are now down 20% since Jan 2018. Watch out below!

In markets where bugger all is selling where’s the price? Whatever the ‘marginal seller’ will take.

I noticed the same thing today.

Big drops!

You can see it on the trend graphs for each property now.

Recent prices are finally starting to filter through to their algorithm.

I had felt they were a bit behind on where the market was - perhaps they altered their calcs even.

As I have said many times on here before, a house is only worth what it says on a signed (by both parties) "Sales And Purchase agreement" - any other valuation is either "wishful thinking" and/or doesn't account for current market conditions. I take no notice of what the "spruikers" say on here - you will find they are pushing a personal wheelbarrow of their own "self interest' - whether it be in the sales of the houses themselves, mortgage broking, renovations etc etc.

Rises in Wellington, Canterbury, Otago and Hamilton though. It's not all about Auckland. Auction activity picking up in Sydney as well. The signs seems pretty good to me and don't warrant such a bizarre, scatological analogy (responding to Wilkes above).

Hello Mr Smith. I was merely questioning the language used to describe such big asking price falls.

I think that reality is probably a point that bisects Grizzly Bear Joe Wilkes and Perpetual Bull Zachary Smiths POV.

Mrs The Point

I’m not that Grizzly really.. but I do like for people to have an alternative view and some balance to consider things properly before making the second biggest decision of their lives. Mortgages these days are lasting longer than marriages so it’s important not to rush in because Tony Alexander or Ashley Church told you to.

Joe Wilkes.

But to be honest.. they are talking abut asking prices.. which mean diddly squat, its the price on the contract with the signatures on it that matters, everything else is bullpucky.

Stock on the market is far more useful than asking prices, at least it actually tells you how many people are trying to get out now.

The prices on the contracts are very unlikely to be higher than the asking prices, at least in those areas with negative numbers.

In what world are continued price increases at this point, at this speed, good? NZ is one of the most unaffordable housing markets in the world, with countless examples of the hardships people are facing, living in cars, struggling to pay for food and power, resorting to prostitution. Whole generations locked out of having a home of their own, and starting families with the security of a roof over their head that's theirs.

Exactly. For growing numbers of people, rising prices are 'doom and gloom'.

So in that sense, the spruikers here are DGMs.

Those areas will almost certainly follow Auckland down.

As house prices (continue to) rise in the smaller centres, the price platform is raised for Auckland.

Auckland is again likely to lead the next market bull-run.

TTP

yeah, in seven to ten years time

Seems about right. A return to historical affordability over the next 5-7, than some slow capital gain again between 7-10 years.

Hi fat pat,

I don’t know when the next housing market bull-run will occur - and neither does anyone else - but it doesn’t seem near.

It’s save to say, however, that while rents are rising and interest rates declining, yields for many/most residential property investors will increase. Most investors have grasped that!

TTP

What you still don't seem to grasp in your little RE brain Ttp, is that Auckland's prices can't rise again unless those homes either become affordable and to do that prices are going to have to drop quite a bit especially for central Auckland and would only rise gradually in line with peoples wages.

As far as a property 'bull run' for Auckland is concerned, that can only really happen if overseas buyers are allowed to assets strip again. Even if they could get around our Foreign Buyers ban, I doubt China, would be willing to take away their capital flight restrictions, certainly not any time soon and probably not for years if Trump is allowed to remain in power and those trade tariffs remain in place.

If any experts feel that downturn /price fall that started in last few months in Auckland, will overturn and will see boom....is plain stupid.

Any cycle be it boom or doom has to run its course.

Yes.

By the way, who are 'the experts', or at least who are the 'independent experts'?

We can dismiss the bank economists.

Maybe Bagrie?

Apparently, everyone is an 'expert' on property in New Zealand.

Interestingly, everyone is an expert in property but they don't know the first thing about economics.

Hi CourtJester,

I’m afraid few would agree with you.....

For a start, neither Phil Twyford nor Retired-Poppy have track-records to suggest they are experts!

TTP

Do you work TTP, if RTP is indeed retired and lives off interest, then I'm pretty jealous of that lifestyle, nice and easy, able to relax and enjoy life. Whats not to like.

Are the Bank Economists or Bagrie saying that prices will now stage a recovery?

No.

Not even Tony Alexander, who is the biggest spruiker amongst them.

Akld is now on the slide, lets see how far she goes....

*casually walks away concealing an empty bottle of oil..*

Vegetable, Mineral or Fully Synthetic?

Organic Halal Fair trade GMO free Coconut oil?

Question to be asked, how mant RE Agents have swithced or are trying to to switch to alternate jobs, business.

If someone can ge the that data, will know how bad the market is and what chances it has of recovery in near future.

Nope, RE agents are like the spruikers on here.. it always about to go up again.. By the time the agents get to the point they realise they need a job with a stable income, its too late. (and its the newer agents that fare worst in a downturn, the established agents have decade of previous customers to fall back on so they manage to survive.)

From my experience, many agents own multiple properties. Some of them may be pressured to sell with reduced income.

Alas, there are few opportunities for door-to-door encyclopaedia salespeople these day’s, so I’m not sure what “under-employed” real estate salespeople will do to earn a crust.

TTP

"The Central Otago Lakes region remains strong, no doubt because Aussies are not restricted from buying, unlike other foreigners."

Are there actual stats on the nationality of buyers?

No there isn't! But the purchasers in the Central Otago Lakes region, have Australian sounding names....

Biggest obvious sign of decline for outlook is the number of redevelopment opportunities which were bought in the past 3/4 years and are now back on the market in the same state at discounts to purchase price.

There is no shortage of places coming to the market only a shortage of buyers who can afford them.

Christchurch market is the most stable market in the country bar none

Rebuild continuing and with more people moving in daily, business is growing.

The property market is not just Auckland!

The MAN 2. Agreed , on a regional basis Christchurch/ Canterbury is now mispriced /undervalued.

Christchurch is hardly a "market" it's just a little village.

Cantabrians worry about falling off the edge of the Earth when they venture North of the Waipara and South of the Waitaki.

That's very unkind, CHCH is a hick town!

Agree that Christchurch is reasonably well-placed for the future.

Wellington and Auckland remain top investment areas for medium/long term capital appreciation and rental yields.

TTP

TTP, how long are we talking? Because the next 5 years or more aren't looking so hot. They could all well be negative. At least that would make the overall market more affordable in world terms.

ChCh is top investment location with positively geared property and guaranteed capital growth.

Personally wouldn’t be touching Auckland not Wellington as an investment, as returns are pretty pathetic and prices are reasonably volatile due to

The fact that young ones are heading to ChCh due to the cost of accommodation and living costs.

Got children in Brisbane, who look like they are heading back to ChCh due to cost of living, taxes and too many Ozzie’s living there!

People will only head to Christchurch in numbers if they can get employment there but, unfortunately, the ChCh labour market is weakening - while both Auckland & Wellington show relatively strong job growth.

TTP

Ahem TTP actually Waikato and Hamilton are very very going ahead and will be a top region for investment if not already. Hamilton is top for IT growth, maybe explained by being off a low base however as the article shows there are many opportunities opening up ....

Silitron Valley: exploring Waikato's tech sector | Stuff.co.nz

https://www.stuff.co.nz/technology/112880315/silitron-valley-exploring-…

1027, 4684 and 918465 are the magic numbers.

Can't find them on my lotto ticket thing.. try again?

That would be the Barfoots monthly lottery.

Ah, right, i'm playing the wrong game :)

Auckland property prices will be double in 7-10 years, the trick is to pick a correct starting point!

Starting point -40% from where we are now?

CM ~ given we already have all time low mortgage rates, that would imply real wage growth of 5%+ per annum. Can't see that's gonna happen.

Looks like a continuing trend down in Auckland to me, rather than just seasonality. There's something more for it to be -2.7% in a month. Have we ever even seen that in sliding Sydney in the past 18 months? That's quite a dip, and it's spreading from Auckland a bit. I'd say look to Hamilton and Wellington to start drifting down next, after reaching all time highs. Sure, they may go a bit further before turning. Tauranga has also had a good go in recent years, so wouldn't surprise me if it gets hit pretty hard as the market slips, with all the building that's been going on there. Certainly doesn't look like much of a shortage of housing for sale, either. Plenty in Christchurch, including those mid to lowish-priced (in this overvalued market) Kiwibuild properties that didn't sell. Yes, it's all speculation Your Honour, but that's my two cents.

The narrative seems to have changed recently from "median prices" to "asking prices".

I wonder why RE commentators want to talk about asking prices when it's the median house prices that really matter?

Probably because the May sales data isn't available yet. Personally I'm more interested in the HPI than the median price although the median is interesting too.

And even more than median prices.. the HPI, which corrects for the change in the mix of houses selling. Median price tells you what they spent, but not what they got for it. Did they get a high mileage Toyota Corolla or a low mileage Bentley for their money?

The biggest declines according to the Herald seem to be in Auckland suburbs popular with foreign investors. It is a fact that there is serious amount of overhang stock on the market, and it is fact that prices are soft. Anything else is conjecture, probably of the self-interest variety. Anybody keen to catch a falling knife?

Would it be a good buy if i manage to shave 20% off cv?

FHB looking at buying atm.

As an alternative approach ~ look at the transaction price history of every property on the street and near by streets.

This will give you an idea on price psf and I would look at transactions 2012 onwards and see how the numbers come out.

From this you should be able to gauge where u see the price should be.

Not necessarily

Some areas boomed before the RVs come out and have been selling under CV for while now.

Take a look at homes.co.nz and look at the range, alot have the last RV at the high end of the range or is even up outside of the range.

I would consider offering at the low end or under the bottom of the range at the moment as the stock is not moving, the power is ijn your hands! Lowball offers are the way to go in these times, well in Akld anyway.

The Herald must be getting worried. It's OneRoof property report was full of spruiking from the usual suspects.

What makes you say they are worried if they are just carrying on as usual?

It seemed even more spruikery than normal....

wow, didn't think that was possible.

I received 2 RE agents pamphlets in the mail this week, one said;

- I have a real shortage of listing in Ponsonby for up to $2 Mill from Ray White

the other was in the mailbox today,

- I have buyers in the $2 - 3.5 Mill bracket wanting Ponsonby intermediate zoning, from B & T

Your point?

Ask Mrs The Point if you can't figure it out yourself

And you believe every word that comes out of a RE agent's mouth, or pamphlet

Wow, that's great news. And we all know that real estate agents, that great bunch of ethically minded, morally superior professionals, always, always tell the truth.

So you think they would bother printing 100's of pamphlets then distribute them just for fun?

Yvil, if you believe such stuff then more fool you....

Of course I believe him & her, do you think they would bother printing 100's of pamphlets then distributing them just for fun? No they do it because they want to make a sale

For an architect you sound incredibly RE Agent-like.

Yvil, yet more proof you are (not) a well seasoned investor....

Dude! they are just looking for listings!

Yes they are, because they have buyers. If they had no buyers but too many listings they would be looking for buyers

They get a listing fee is why. And of course agents don’t care about the selling price too much - they still get a commission. If they can flick your property for rock bottom, they will. They want motivated sellers and cashed up buyers in their perfect 4% for doing f*** all world.

Talking of “fools”, Retired-Poppy, how are your term deposits going at present?

I note that rental property yields are climbing steadily.

TTP

REA-TTP, as expected, my term deposits are performing way better than the price of my Leafy suburbs house. Also, it's worth noting, FHB's who are waiting are watching their positions go from strength to strength :) As unemployment rises, the economy will weaken further, rents will begin to fall - property price falls will steepen. Any seasoned investor knows this.

Anticipation of the next "bull run" in 2021/22 is only the outlook of fools. It's your outlook so stop this slithering around.

of course yields are increasing as the property prices are going through the floor!

Exactly. It looks good on paper, albeit for a short time. Not unlike what happened in Ireland, when the work runs out, so will the workers - via Auckland Airport. Then rents will start falling.

"rents will be falling"

Truely one of the most ignorant, foolish and uneducated comment on Interest

You're a moron Yvil! If you had ever been a Landlord you would have known that in a declining property market this causes rents to fall. I've been through it before during the Financial Crisis in 2008, where rents dropped significantly in the UK and lots of people including Landlords lost their properties to repossession by the banks. Fortunately I managed to get through it without any losses apart for the property price declines.

I've been a landlord for 25 years and I have NEVER witnessed rents to decline. Thanks for calling me a moron, it shows you (lack of) class

Well said CJ099. Yvil, being a Landlord of 25 years, has forgotten his life as a tenant. Dangerous complacency is what I call it. Many Landlords who lost properties to banks again became tenants. The fear that ensued after the greed became an utter waste of everyone's time and resources (sigh). During the recession of the early 90s, I witnessed significant rent and property price declines. There were many vacant properties. It happened so quick too. As a tenant, I enjoyed the financial advantage!

Really Yvil I find that very hard to believe that you've never noticed rental prices declines when property prices fall. Perhaps you should take a look at what's happening across the pond from us such as Sydney for instance which has been effected by the same market forces that we have experienced: Financial Review article: Sydney rents are retreating, good news for tenants, bad news for owners

https://www.afr.com/real-estate/sydney-rents-are-retreating-good-news-f…

And before you bleat on about property oversupply as an excuse, perhaps you should also take a look around if you're in Auckland, Take note the amount of cheaply built apartments going up everywhere. Oh and the real reason why I called you a moron is that you should also realize that when people can't sell their property for the price that they're expecting in a declining market and they have to relocate, they usually decide to rent it out rather than leave it empty especially if they have a mortgage on it. This saturate the rental market and yes you guessed it - rental prices fall!

Hahaha said the person who got some RE leaflets in the mailbox and believe the market is hotting up!

Naive much?

I never said the market is hotting up

You were implying but point taken

@ Retired Poppy: Yes exactly, not only has it happened in Ireland but also around a lot of the Western world cities (Including here in Auckland) that allowed their property prices to get out of control. What people tend to forget, is that if wage earners can not afford to live in an expensive cities they simply move out. Then the companies within those city start to collapse (or move out) if they can't pay for high salaries to retain staff so they can keep paying for over inflated property prices and rents.

Take a look at Canada as an example: Better Dwelling article: Unemployment Is Rising In Canada’s Most Expensive Real Estate Markets

https://betterdwelling.com/unemployment-is-rising-canadas-most-expensiv…

Yvil, I even have one RE offering to take me out on a dinner date! You mustn't be his/her good book!

You really should stop pulling that important marketing material out of other peoples letter boxes Whyvil.

The house prices in AK have been falling since 2016 unless you were under a rock. But agree no one knows when it will rise. the cyclic patterns are not the norm , its broken,

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.