By Greg Ninness

Auckland house prices may be at an important turning point but whether that turn is up or down is anyone's guess.

Conventional wisdom has it that a fall in prices is usually preceded by a drop in sales volumes and the number of homes being sold in Auckland has been soft for some time.

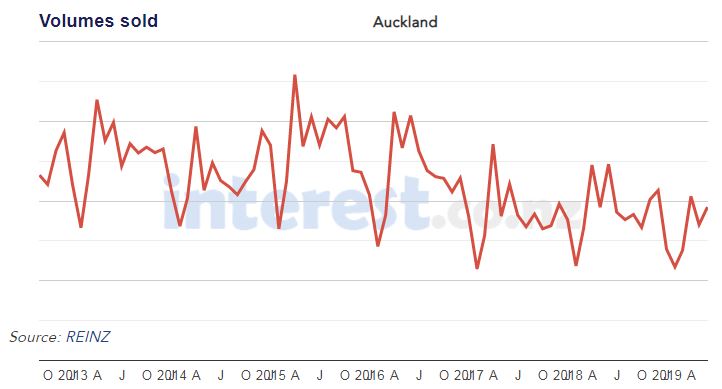

The chart below shows the number of homes sold in Auckland every month between August 2012 and May this year (REINZ data) and an interactive version showing the same information for all regions going back to 1992 is available here.

What the chart clearly shows is a fairly regular seasonal pattern with the annual peak in sales occurring in March. What it also shows is that the number of homes sold each month in Auckland has been steadily trending down since March 2015.

In May the decline in sales was particularly steep, with just 1925 sales recorded by the Real Estate Institute of NZ, down a whopping 22% compared to May last year. That followed a 12% decline in sales in April compared to a year earlier and a 16% decline in March. And compared to May 2015, sales in May this year were down by 37%. Normally such a sustained fall in sales volumes would have heralded a significant a fall in prices, but so far that hasn't been the case.

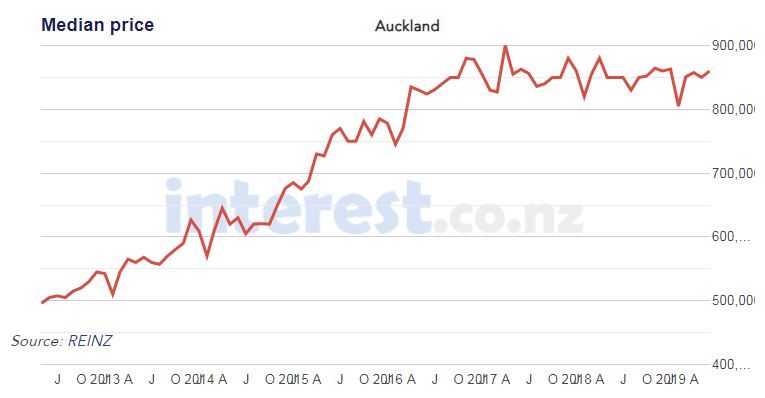

The second chart below shows the REINZ's median selling price in Auckland for every month from April 2012 to May 2019, with an interactive version available here.

This shows that the median price was steadily rising until August 2016, but since then there have been relatively small monthly movements either side of $850,000, with the overall trend since August 2016 being flat as a pancake. And it's not just the median price that's flat.

The REINZ's lower quartile price for Auckland hit its record high of $680,000 in March 2017. Then from April 2017 to January 2019 it stayed within a fairly narrow range, moving up and down each month between $649,000 and $675,000. And then it hit $680,000 again in February this year, stayed at that level in March, dropped marginally to $676,000 in April and then hit $680,000 again in May. Which means that although the lower quartile price is also flat overall, it is testing its upper limits.

So at the bottom end of the market prices have also remained flat, but may be poised to start edging higher.

No doubt the recent stability in prices has been helped by lower interest rates, with interest.co.nz calculating that the average of the two year fixed mortgage rates offered by the major banks has dropped from 4.80% to 3.95% over the last two years, while the recent scrapping of a potential Capital Gains Tax wouldn't have hurt either.

However if the number of sales being made in Auckland continues on its current downward path over the remaining winter months, it will severely test the market's ability to maintain current prices.

But at the moment the market is not following the usual rules and there's not enough evidence to say prices in Auckland will move one way or the other.

We will just have to wait and see.

The comment stream on this story is now closed.

125 Comments

Certainly, Auckland house prices have proven resilient - far more so than many people here predicted 3-4 years ago.

TTP

All the factors add up for Auckland. A gateway city into an economic region. A sea port and an international airport. A well known city with high immigration level. British heritage with all the good things that entails for personal freedom and secure investing, English speaking, very cheap personal transport with Japanese imports at rock bottom prices for quality vehicles and cheap associated costs. A good level of medical and educational institutions. Low crime although we could do better. Good weather, not too cold, not too hot, plenty of rain. Many parks, beaches, a very attractive city. Relatively cheap to travel to anywhere else in the world - okay takes a few hours more but that's hardly a big deal.

High employment.

It's hard to see things changing dramatically anytime soon. Zachary Smith prediction - prices will hold and increase with inflation.

You must try to stop living in denile, reality is difficulty to accept that sales are tanking, QE credit experiment and neoliberalism is unwinding, but locals are left with massive debt based on self serving property industry compulsive lies, basicly the industries corrupt and have turned a basic human need / right into a speculative investment. Government must brake this anemic cycle, thats costing the tax payer and damaging communities.

An Auckland house is not a "basic human need/right". Much the same way a DGZ property is not. The problem is with greater migration flows desirable property expanded to include entire cities - the Global Cities mostly. Cheap travel and the freeing up of migration created a plethora of global cities of various tiers.

Not a basic human need/ right?

I agree if you are talking about ownership.

I would 100% disagree if you are talking about access to decent rental ( social or private) housing.

You're absolutely right 2 Tooth Bora, NZ has allowed it's property market to become corrupt, thankfully at least we have a Government in power that is trying to fix this major issue with our economy, through enforcing Anti Money Laundering regulations and Foreign Buyers Ban. Which have had a very big impact on our cities property prices.

Unfortunately some Boomers (And Real Estate Agents) are not willing to acknowledge how property prices got so out of control and are now so scared and desperate that they're willing to say anything to maintain their million dollar plus property price which is currently deflating before their eyes.

So CJ099, have foreign buyers and money launders have been buying up big time in Whanganui, Timaru and Westport and all those other rural centres throughout NZ big time also forcing up house prices in these centres over the past decade?

So low interest rates, historically high immigration rates, housing shortages and lack of skilled trades people, and a little bit if greed on the part of local property speculators have had nothing to do with it?

No, probably not, but those who benefited from the "largesse" from said money launderers have, so now people who live in Whanganui are now being displaced just as people have been in Auckland. We are using any means we can, mainly rampant immigration (or sky hooks in other words) as it would be considered too disastrous to let prices settle back down to values that better reflect that which can be paid for with earnings from near to where the houses are located.

You could be describing Sydney in 2017! And prices just kept going up there as well... right?

Any analysis/prediction on house prices that doesn't even mention the role of credit/debt is just laughably simplistic.

The concept of an interest rate led debt bubble is predicated on 'return to mean' interest rates. The flaw is that there is no real and stable natural rate of interest over long time scales. Interest rates are not a solved complexity. It could very well be the case that rates of 6% or 9% percent are not justified by natural economic forces at play these days. How high should they be? Well if its perfectly reasonable to ask how high, then its perfectly reasonable to ask how low. And thats the failing of the interest rate led debt bubble theorists. They are simply bias to rates going up.

Not really resilient in the upmarket sector. If you have the cash you can get a Mansion for a bargain

Agreed TTP, and those predicting a bubble burst were advising FHB to put their lives on hold until the market bottom out. The charts show that the Auckland market has been relatively stable since the peak and trends currently do not show signs of a significant correction. The main drivers currently providing support for the Auckland market are continuing low and falling mortgage interest rates, historically high immigration rates and shortages of skilled tradesmen - all of which seem likely to continue to be significant in the medium term.

Risk to the market would seem most likely to come from off-shore but that is unknown and always a factor in life.

In terms of prices, currently buying well - such as in the winter slowdown - is probably a far more important factor for FHB than the future of the market.

P8, you say "risk to the market is mostly from offshore and is (ALWAYS) a factor of life"

Lol! Is it really? I feel blessed to be provided with such entertaining (comical) Spruiker material to read. Keep up the great work, it's a timely omen of the prevailing risk.

FHB's will do well to wait, watch, sacrifice and save. Refraining from becoming the biggest fools yet in this epic housing ponzi will be rewarding. Savings in the bank also provides security and freedom. Consideration should be given to the risk of being trapped underwater. It is a prison sentence.

When at the crossroads, sometimes the right thing to do is sit still and wait. Ignore the heavily indebted Spruikers shunting you from behind. The Auckland HPI is indeed falling YOY. Many property bulls have found this difficult to digest.

printer, do you really think there are a large number of people "putting their lives on hold" at the moment?

It would seem to me that deposit requirements and stress-testing at 7% are two good reasons for the low volume of first home buyers at present, more than any "putting on hold". Why investor activity is also so much lower than it used to be is another matter.

We do tend to look at NZ's property market perhaps with rose-coloured tines, given the lack of major crashes in the past. It's certainly interesting times at the moment, though. We've never seen this sort of monetary pumping of the market before (both central bank driven, and from China), have we? So we've never had to face the possibility of being a Tokyo, let alone a Spain or Ireland.

"Why investor activity is also so much lower than it used to be is another matter."

Gary Lin, a high profile property investor of Auckland based property, & in the "property mentor" business, stated in a recent video that he is constrained by financing due to the bank application of the stress test rates at 7.25-7.35%. He needs them lowered in order for him to have more borrowing capacity.

Also the fact that property prices in Auckland have not risen in the last 3 years or so, means that there has been little or no capital gains on property prices, and hence no equity gains for buy and hold investors. The lack of equity gains thus results in an inability to undertake equity release / deposit recycling techniques where property investors borrowed against the unrealised equity gains to use as deposits for more property purchases. That self reinforcing upward price cycle has stopped for the time being.

Not sure about property traders (i.e. buy, renovate and sell strategy), trading in Auckland residential property and whether they face financing constraints. However there are a few stories of property traders in Auckland residential property getting caught out and some are currently in an unrealised loss position at current market price levels.

Given financing constraints, and reduced borrowing capacity, it looks like property traders and property investors (buy and hold strategy) might be more active in residential properties in Auckland at the lower price points - apartments.

Gary Lin...I recall that fellow. Got a 40% first home deposit as a handout from his wife's daddy then castigated Kiwis for not working hard enough, whilst also proclaiming Chinese to be the master race.

Seemed like a good, down to earth fellow.

Yes, Rick, WTF have we done. We’ve exported our homes and jobs in return for cheap plastic crap.

TTP you have been criticised over time for a view which is proving to be sound. Sadly contrary views have been personal in their criticism of you.

Such attacks have not been supported by reason but rather baseless wild assertions. RP comment above falls into that category.

RP is nothing but a Narcisist pushing his own agenda. I would like to see such commentors who focus on criticism of others removed from this site please Editor.

Shoreman, you can't resist humouring me can you :) Begging the editor to remove each and every commentator that threatens your ideology with sound argument is not the solution. Perhaps by tuning out or venturing somewhere else is?

The bulls seem very sensitive today. Like Don Corleone you have so many influential people in your back pocket, ... politicians, central banks are working overtime to support your investments, yet RP has you rattled. RP has always shown broader concerns, he is not a Narcissist.

Resilient TTP? Depends on how much people are prepared to lose on the top end (artificial foreign money price that encourages them to borrow on the family home) that the banks will fully encouraged, against the small gain on the leveraged property investment.

A few bank economists (debt salesman at seminars) should go to jail at the end of this unwinding.

JW

Headline photo is from Dunedin Baldwin St, but report only covers Auckland! Is it possible to have a similar overview for the remaining 2 thirds of properties, those areas outside Auckland. Interesting numbers and questions put

Agree. For those who know it stands out like a sore thumb.

Hi Houseworks, if you click on the links in the article they will take you through to interactive charts where you will be able to see the sales and median price trends for all regions.

Subtle foreshadowing that Auckland's median might go down to meet Dunedin's at $450k or so?

Thanks for a well balanced article Greg

Underlying trend is prices should have been falling, but excess immigration and falling interest rates have propped it up. If the govt actually slows immigration down watch it plummet. And construction is on the boil (for now), so supply issues are being addressed too.

Agree. And not much life support left in terms of lower rates.

Perhaps we are seeing a divergence in separate segments of the Auckland market.

The lower end being supported due to folks being able to afford these places and interest rates being cut. (Let's say that's at or below NZD median price).

Then we have the market from the median price to 2mm which appears to be slipping a bit and has some weakness in sales.

Finally we have the 2mm and above which in places has shown more significant falls in volume and price.

Greg, perhaps this is worth exploring in a further article ? It would be really interesting to analyse volumes in these three price buckets over the period and also the cut the data between houses and apartments. The latter cut may be necessary as whilst we know the sales volume of apartments is down yoy we also know that the FBB specifically excludes this type of housing.

The FBB only excludes apartments in NEW developments of (I think) 20 or more units. Resales are still captured by the FBB.

Thanks for the clarification Greg, I was unaware of that distinction. What do you think about cutting the data by price bucket to see if there are divergent trends ?

We looked at the trends in lower quartile and median prices. Unfortunately REINZ doesn't publish upper quartile data. However UQ data can be more difficult to interpret because there is greater diversity of homes in that sector and bigger variances in prices. If you were to plot ALL sales on a distribution curve it would be bunched up at the lower end and very spread out at the upper end. But if there was a significant shift in the UQ price band I would expect to see a little more movement in the median.

Understood. Thanks Greg, appreciate the detailed reply.

@ Greg: Well that's a huge gap in REINZ data don't you think if we're only being presented with trends in "lower quartile and median prices"?

We really need to see the effects on the "Upper quartile and median prices" too to get a full picture on what's happening our property market.

Even looking at the "Housing sales - market price segments" That data is capped and is only tracking those at a maximum of $600k, which in Auckland would be classed at affordable. Is the REINZ not fully tracking and able to present property data for those sold unaffordable price levels such as over a million dollars?

The reason why it's important to see the UQ data, is that we (Local Investors) need to see that the effects of Money Laundering in NZ, and to see that it is declining otherwise as Investors we would be investing in a very risky unstable market if it's still going on within our cities.

Here's an article for you from Better Dwelling: How A Little Money Laundering Can Have A Big Impact On Real Estate Prices

https://betterdwelling.com/how-a-little-money-laundering-can-have-a-big…

To Greg's point 're the new apartment sales & FBB ...

The first link provides an explanation of which developers can apply to have an exemption.

The next link shows the exemptions granted ~ this is quite interesting as many developers have gone for the exemption where they can and provides some evidence that developers are still pushing apartments to foreign buyers.

https://i.stuff.co.nz/business/109117400/apartment-developments-seek-ex…

https://www.linz.govt.nz/overseas-investment/applying-for-consent-purch…

Thanks for the links. But what I'm actually looking for is the data on sales prices for 'existing housing stock' that the AML and FFB were meant to make more affordable. So this is why I think we should be able to see this data because I know that both of these legal measures have had a big effect on property prices in the upper price brackets +$million mark, I can see those prices reducing in the auction results. And yes I know that most of our new builds in area like Auckland are still be sold off to overseas investors via back door Trust companies etc.. But it should be very easy to filter out that data in a spreadsheet by simply by removing those that do not have 2017 RV's, which allows you to see the existing housing stock which makes up the majority. But as Greg mentions "Unfortunately REINZ doesn't publish upper quartile data". Sorry if that sounds a bit long winded.

CJ, understand your frustration. Some data it seems is less than transparent.

Re your point that Trusts and company purchases are being used to usurp the FBB... I was under the impression (perhaps wrongly) that now all purchase by trusts required all trustees and beneficiaries to be residents. I'm not sure if the same is true re the majority shareholders in a company also being resident ?

Any thoughts on these points appreciated as I'm still getting to grips on whether there are sufficiently large loop holes in the FBB for foreign folks to still purchase landed property.

I think you'll find there are plenty of loop holes on new build property sales to overseas investors.

CJ, I had a look at the REINZ and I think I now understand why they are pushing the use of median prices.

By way of a little background I ran a trade association in financial services for a while so I understand first hand how stats are used to tell the story the association wishes to sell.

In this case REINZ is the trade association for real estate agents. They owe no allegiance to anyone other than their members as these folks pay for everything * including the stats which are released.

The median price is the 'middle price' of all the data in a transaction set.

If nothing else changed you would expect a few things to be true of the median.

1. The median price should rise roughly by wage inflation each year as wage rises make property more affordable

2. The median price will rise with lower interest rates again as affordability increases

3. As the higher value transactions in a data set are relatively small in number a change in their frequency or value will have little effect on the median value

So the question is what stat would be useful to review ?

I'm guessing the mean value would tick down slightly quicker than the median as higher value transactions reduce in volume but its use would still be limited to a broad indicator. I can't see how the HPI is calculated so I have to reserve an opinion on this stat.

Bottom line though is that the only way to adequately analyse the data is an analysis by all transactions grouped by value bucket.

This could include numbers of transactions by price range, % over / under RV by price range etc. If you could also exclude / separate properties which had substantial spend on renovations and improvements you'd have a much purer data set.

There are several real estate agents that provide this information in their monthly updates, but it is based on their working area not an entire city or region.

So obvious that the upper end has collapsed because of the lack of Chinese money. The RBNZ C5 data shows that housing credit growth and credit impulse are both positive. Interest rates have been lowered. The market should be booming but it isn't.

Hi fat pat,

That's arrant nonsense.

The market boomed during 2013-2016.

Nobody in their right mind would assert it should still be booming in 2019.

TTP

TTP, yawn. You need to provide an argument.

Fat pat hasn't proved that the upper end of the market has "collapsed". No doubt some people who paid a million too much for a four million dollar property will get burned if they want to sell only a year or so after they purchased it however we are still seeing three million plus properties selling for greater than their RVs in Auckland.

Around my area all seem to sell except for the odd and obvious exception. Currently down to just eleven listings. I'd say those that bought big sections at premium prices are having the hardest time. Yet we Aucklanders all know that you can rarely buy and sell within two years and hope to make any profit. A loss has nearly always been more likely.

Let's see the data that backs this up.

28 Picton Street, Freemans Bay RV 2,950,000 Sold 3,150,000

24 Kenyon Avenue, Mt Eden RV 4,550,000 Sold 4,600,000

39 Maungakiekie Avenue RV 5,500,000 Sold 6,200,000

10 Armadale Road RV 3,100,000 Sold 3,800,000

40 Upland Road, Remuera RV 3,750,000 Sold 3,600,000

Well I can certainly see property prices declining in the expensive areas of Auckland, here's a random selection from recent auction results.

12 View Road, Campbells Bay RV $3,900,000 Sold for: $2,758,000

43B Kenneth Small Place, Remuera RV $1,180,000 Sold for: $800,000

2/632 Manukau Road, Epsom RV $1,120,000 Sold for: $865,000

2C/9 Victoria St East, Auckland central. RV $1,160,000 Sold for: $883,000

Albany, 8 Red Oak Pl, Schnapper Rock RV $1,300,000 Sold for: $976,000

4/76 Vale Road, St Heliers RV $1,340,000 Sold for: $1,000,000

Browns Bay, 71 Glencoe Road RV $1,125,000 Sold for: $915,000

33 The Glen, Remuera RV $1,800,000 Sold for: $1,615,000

1/6 King George Avenue, Epsom RV $1,060,000 Sold for: $973,000

7 Aberfoyle Street, Epsom RV $2,375,000 Sold for: $1,950,000

631 Remuera Road, Remuera RV $1,950,000 Sold for: $1,790,000

165 Grand Drive, Remuera RV $2,100,000 Sold for: $1,852,000

60 Campbell Road, One Tree Hill RV $2,175,000 Sold for: $1,830,000

631 Remuera Road, Remuera RV $1,950,000 Sold for: $1,790,000

Browns Bay, 658 East Coast Road RV $1,125,000 Sold for: $915,000

14 Hillsborough Road, Hillsborough RV $1,430,000 Sold for: $1,200,000

This is like canon fire from two ships of old which are facing each other intent on destroying the other. So far CJ099 has fired more shots but had less hits.

You're making less sense than usual Houseworks. But it's understandable that your getting more desperate to put a positive spin the AKL market.

Not sure if you noticed that Zachary included a price decline in his limited gains list. Can you sport it?

CJ099, within a short time, Hamilton will be sporting a similar list. I hear from my contacts that without vendor discounting, it's near impossible to shift Hamilton listings $750k and above. Weakness starts at the top, gravity does the rest.

Yes quite agree with you RP, Which is why I would like REINZ to publish the data from property prices above the +$million mark on existing housing stock (Not new builds after peak 2017 valuations) so we can see whether the recent measures for AML regulations and Foreign Buyer Ban have had the desired effect on upper price brackets. This would also effect regions as you mention Hamilton, also Queenstown and Tauranga.

CJ099 you say "I would like REINZ to publish the data from property prices above the +$million mark"

Greg Ninness has already answered this question, today in fact, of why that info is not available.

Then hilariously you go on to say "This would also effect regions as you mention Hamilton, also Queenstown and Tauranga." in answer to (try hard) retired poppy. He has long been discredited and the term poppy-cock fits him perfectly.

I commented earlier that your stoush with ZS was like a war of attrition. That comment has obviously set you off in pursuit of me for an explanation of million dollar prices and what drives them. You clearly have missed the point that lower quartile Auckland homes are "poised" to go higher, so that now might be a worthwhile time for at least Auckland fhb to make a move. Last I heard lower quartile is well below one million even in auckland.

And btw if indeed you did sell any auckland investment property in this cycle at the height of the AKL market, what did you do with the proceeds if any? Please dont try to wow us and say you invested it all in the regions because I can tell you didn't do that.

Your really come across as rambling now Houseworks. You should reread your comment above. Making random accusations and pulling things out of context makes you real tiresome and very boring with you trying to make things personal. Bottom line is that I provide actual evidence to support my points of view and you don't. Now stop trolling people and trying to intimidate them in to not commenting.

CJ099 Your self awarded accolade of selling "off my property investments at the height of the AKL market" is a fabrication. Not only is it a vague claim but anyone who had the insight for the reasons you gave would have put their funds into the regions and made the massive gains since then and still continuing. Fabricated to make a point that's all

....look whos envious of the one whos gains are actually banked? Well timed CJ099, smart move.

Cheers RP, These Real Estate Agents are really getting desperate aren't they. :)

Trolling Houseworks, you're very desperate. You obviously did not like the fact that I provided a list of evidence of the upper price bracket prices falling. It's just a fact deal with it, I've already provided the evidence, so where is yours to claim otherwise. And yes I do notice the trends on what's happening in a market it's not difficult to figure out.

Unreferenced numbers on a page do not mean anything CJ. You might need to do some more work on that I think. Btw I made one comment and as a result of losing the argument with ZS you have got your knickers in a twist and demanded I explain whys and wherefores to you and how prices and markets work. Printer8 has asked you a question above. Please be consistent of your own standard and go and reply.

CJ99 Your problem is you don't understand much which is why you can't get anywhere in the property market....please try not to reply with a self-righteous speel

You really do sound desperate to stop people from commenting on what's actually happening in our property market. And I sold off my property investments at the height of the AKL market because I recognized how it was being over inflated by overseas investors and money launders. So explain to me how I don't understand the market? Also please explain to all of us Houseworks, how the Auckland property market is going to increase in the +$million plus price brackets because I can clearly see it deflating and I've provided evidence of that price decline.

Dp

Funny how you play the man and then deflect back criticism of putting others off from commenting. And nice try to claim Guru status by way of a vague reference

Oh you do make me giggle! Come on actually give us a real explanation to support you arguments. So I ask again: Explain to me how I don't understand the market? Also please explain to all of us Houseworks, how the Auckland property market is going to increase in the +$million plus price brackets?

...cm'n Houseworks, don't be like REA-TTP and go silent. Address CJ099's questions!

Thanks RP, But he/she is to busy trolling me on another thread. :)

There is a question waiting for you above CJ from printer8....why haven't you answered it yet and what's taking you so long? Get to it!

Ahh the envious poppy with no inheritance! How does putting a few numbers on a page explain anything? Time to do some homework and then continue the war with those who care. Btw you have been elusive not acknowledging the fact that fhb and investor housing is poised to go higher. (Poppy: Let's sweep that under the carpet and keep quiet about it)

"fhb and investor housing is poised to go higher" It hasn't yet so why are you hyperventilating as though it already has? I'm already on record as suggesting that cheaper money will be supportive to a degree in the lower quartile, just not in the higher. Sorry to break this to you but FHB's raiding their retirement funds to scrape together deposits on 30-year mortgages at the top of a market isn't going to be your sustainable market panacea. Think about it.

More to the point, why are you dodging the questions that CJ099's put to you?

You are incorrect (whats new?) prices have gone up $31000 which is faster than anyone can save over a short period. If prices break $680 and form a new high then what will you say then?

I made the mistake of commenting on CJs war with ZS. Frustrated that he was losing the argument CJ tried turning his guns on me. Let it go retired poppy, it's not good for your blood pressure and aging heart.

Hi Houseworks,

When CJ099 fires his canon, he succeeds only in shooting himself in the foot.

TTP

REA-TTP, I'm struggling to visualize any primate attempting to shoot themselves in the foot with a canon. Your comment serves as further proof you often experience these bazaar visualizations.

I think its time you ducked for cover....

Hi R-P,

You’re right for once........

CJ099 is one of very few people who know how to shoot themselves in the foot with a canon.

And by the way, R-P, you’re another.

TTP

REA-TTP, if someone suggests you duck for cover - THEN DUCK!

You commented"Certainly, Auckland house prices have proven resilient - far more so than many people here predicted 3-4 years ago"

Since it was you that made the following post just over two years ago, it can only be interpreted that you are criticising yourself - lol!

by tothepoint | 24th Feb 17, 10:00am "A fall of a mere 12% over the next 3-4 years would be a soft-landing, given the spectacular gains of the recent past. So, hardly a forecast to get too uptight about. But the fall could be more pronounced than that - shouldn't rule that out. Auckland property prices are in decline now. Unless there's a compelling personal reason, why would one buy a house in Auckland at this juncture? Better to "buy low and sell high" than the other way around - every Joe & Jill Bloggs knows that"

BOOM!

Retired Poppy is it also time for you to retire from interest? For the last two years your forecasts have been wrong! Your predictions are entirely due to your predicament so I wouldnt recommend anyone puts any faith in what you say. You change your biased argument just to suit your situation.

Houseworks, financial freedom is a predicament is it? If so, it's a nice one to be in. Its irrefutable that Auckland based FHB's who followed my advice from day one are much better off against a backdrop of sliding prices. It's such early days of what (barring a shock) will be a prolonged Spruiker disillusioning slump.

Face up to the glaring fact that you've had your short time in the sun. Now, be humble and celebrate that first time buyers will now enjoy theirs (at your expense of course)

I'm raising my glass!

There has been no slump or start of one in this market that you love to hate so you are right out of luck. And it looks like the auckland fhb segment is "poised" to go higher according to Greg Ninness...did you miss that point in your haste

...there's your achilles heal right there. It's not about luck. It's time you stopped gambling at the Cassino and pay more attention to the next generation of FHB's you left sitting in the car with a bag of crisps.

Its true that Spruikers biggest fear is a falling market. Its also true that those with real skill will still derive a decent living from it.

It is you that keeps telling fhb to stay sleeping in their cars a bit longer until property prices reach nirvana. So without your flawed advice they could already be in homes, resting back on their lazyboy, watching the auckland lower quartile increasing in their favour like the morning sun rising on a clear spring day.

...savers really do irk you don't they. Its like some new movement that threatens to flatten your out of date and dust covered ideology.

Anyway, don't you have some dusting to do? You'll be surprised what rot lies beneath all that neglect.

Enjoy your week :)

houseworks

People that have to sleep in cars don’t have a deposit to buy a house... the minute they have a few quid they don’t want to live in a car , but they xan’t Buy, now stop posting idiocy.

There will be a lot of names on a list that spruiked this bubble.

It’ll Be interesting to see what the disclosure is when the government goes to The platforms to check email addresses and identities. . A Few celebrities no doubt. Hisco sacrificed already

Who’s next?

What a banker mess... because of greed.

JW..

Bit cold last night but not as bad as the night before that eh. How's your car?

Hi R-P,

Your quote of me (above) is well over 2 years old [24th February 2017]. It's way out of date.

As you well know, I abandoned that position and my current position was formed in early-April 2017.

As it transpires, my revised position has proven to be exactly correct - spot-on - over the past 27 months.

There’s no point you continuing in your attempts to mislead and deceive people, because you are always exposed.

TTP

....and the award goes to REA-TTP, the worlds most entertaining FLIP-FLOPPER :)

Hi R-P,

Your quote of me (above) is well over 2 years old [24th February 2017]. It's way out of date.

As you well know, I abandoned that position and my current position was formed in early-April 2017.

As it transpires, my revised position has proven to be exactly correct - spot-on - over the past 27 months.

There’s no point you continuing in your attempts to mislead and deceive people, because you are always exposed.

TTP

Still getting abusive and personal TTP, still not providing any foundation or evidence to your ridiculous sad comments.

10% to 20% below CV is the trend with few expectation and anyone who is not ready to meet the market is unable to sell.

Do not know much about other areas but Pakuranga, Howick, Bucklands Beach, sunnyhills and near by can vouch for it.

Anyone interested can check the houses listed in trade me for those area with asking price, and than the price that they are being sold. Trend is initially most ask expectation are near around CV - example a house with CV 1050000 will have an expectation between a million and 1.1 million nut after few weeks will change to mid 900s to million and most profit will be sold in mid/high 800s to early 900s and some not even fetching that as in today's market buyers have decent choice to choose from and not in a hurry to buy.

Another trend that have noticed is that since last month even low price units have started to come down so the process is well under way and their is NO IF or WHAT DIRECTION MARKET WILL TAKE.

Housing market is dead for some years to come and it happens world over and whenever the cycle changes to boom or doom is for a sustain period of time and not for a short so now the downside in housing market is for long hibernation.

28 Picton Street, sold for a fraction more than it did in 2016 (which was more than its 2017 RV also), and the photos suggest it may have been extensively renovated, would need to see the listing photos from 2016 to compare them.

24 Kenyon St " no expense spared contemporary comfort is this supreme and exquisitely renovated four to five bedroom", yep, how does it do against RV when you deduct the $$$ pumped into renovations?, oh it sold $50K above RV, so unless Bayleys "Exquisitely renovated" means a fresh coat of paint it did go backwards.

39 Maungakiekie: yep, same deal "A unique opportunity to purchase an outstanding, generous 1198m² freehold property on the park that has been completely rebuilt to the highest standard by our current owners for their family." It's been discussed on here before.

10 Armadale- "A voluminous family living extension was added with a skylight creating an exhilarating sense of light, bright and airy space. Incorporating an office..." yep. again.

And Upland road sold below RV in spite of renovations..

Freshly renovated properties should sell above RV.

Pragmatist, good post. Your facts come as no surprise at all.

Nitpicking that's all Pragmatist is doing. I was merely pointing out that there are still some buyers for 3M+ homes.

ZS, for as long as there exist 3m+ homes, there will always be buyers for them, as long as the prospective buyer perceives there exist real value for money. I think Pragmatist presented a good counter argument that houses sporting renovations win over those not. In a well announced buyers market there simply isn't the competition amongst buyers. This is causing vendors to rethink their pricing expectations. It's all looking rather vulnerable, especially in the upper quartile. The last thing this market could deal with is an imported shock. For example, I know my villa no longer sports the latest renovations therefore I cannot reasonably expect to fetch a 2016/17 RV when one day I go to sell. It is what it is.

My observation about the 3m+ segment is that the really nice places are selling if "sensibly" priced, but there's a lot of unrealistically priced stock that has either been on the market for a long time or has been removed from the market. It feels like buyers are able to be more picky, and take their time. I'd say that prices have fallen 10%, maybe a bit more, over the last year. E.g. Kenyon probably sells for 5m+ a year ago.

Overall, I wouldn't say this market segment has "collapsed" but it has definitely weakened significantly.

From the article:

But despite reports warning of price collapses we aren't in the Endgame. Far from it.

Perhpas you missed this bit:

"Houses in the higher price bands in Auckland have not been selling in the numbers they used to, and that hole has dragged down the median price in many central Auckland suburbs.

The number of buyers able to afford home in the top end of the market is much smaller. A year ago, 7 per cent of all sales in Auckland came in at $2 million and above. That's dropped to 4 per cent now."

REA-TTP, you say "nobody is expecting it to be booming in 2019"

You're already on record as saying it could be booming (bull run, substantial upward lift) as soon as 2020 on the reasoning the FBB would have zero impact, low interest rates, high immigration. That's quite a commission rich summer of 2020 you're predicting right there.

On the night of the election you also said National would be forming a Government the very next day!

The problem with the bull hypothesis is that it is dependent on some positive external forcing. I don’t see this happening because those forcings are already maxed out and were one off. From 2008 to now interest rates dropped from 10% to under 4%. Are interest rates really going to go lower? Is immigration really going to go higher? The only factor I can see helping from here is wages, but if wages move significant so will inflation and in real terms that is a wash. House prices will of course rise some time in the future, but I don’t see Auckland doing another surge in the next ten years unless one of two things happens first:

• a big rise in wages

• a big decline in prices allowing for a big boost via recovery.

Hardly, well said. For employers to be able to raise wages on a broad basis, it has to be supported by the ability to raise prices. In a low inflation/highly competitive environment, the extra funds have to come from stored fat (hay in the barn), trimming staff numbers, increased efficiencies. As there's very little fat in the system, raising more debt at lower rates seems to be the way forward, whether it be public or private. This is a short term band-aid that is sure to serve up longer term consequences.

Barring an imported shock, I also think house prices are more likely to remain in the doldrums for at least another ten years. Either scenario, the Spruikers lecturing to FHB's that houses are a risk free road to financial freedom will be snuffed out for some time to come.

For FHB's over this timeframe, expanding wealth by way of saving is also a pathway to financial freedom, more house for the money and/or less dead money paid out in interest.

You missed the point. LQ prices are poised at the top end, not "in the doldrums" as you say but rather the median "is TESTING ITS UPPER (emphasis added) limits ... at the bottom end of the market prices ... may be poised to start edging higher." Quoted Greg Ninness

Hi Misleading-Poppy

My position for a long time has been that there will be no significant increase in Auckland house prices until 2021 - at the earliest.

However, some recent events (e.g. further falls in bank lending rates; higher than anticipated immigration; rising rental yields & the denouncement of CGT) suggest that there MAY be some lift in prices before then. I have acknowledged this.

I have made NO forecast whatsoever on the timing of the next housing bull-run.

TTP

Fat Pat is right TTP we can see that prices are declining in the auction results for the Upper price band property. At least she understands how that market was driven in the recent boom years and how banks are doing everything within their power to encourage price growth, so far the market has been very tepid to say the least.

Some of us have long maintained there will be a small-moderate correction in Auckland. It doesn't have to be a binary scenario of boom or bust. I have maintained for a couple of years that Auckland would drop 5-10% from peak. It's down 4%. I maintain that the fall will be 5-10%.

Greg, again you insist on ignoring the HPI. You say that sales volumes falling with prices holding means "the market is not following the usual rules ". Yet falling sales slowly translating into falling prices does seem to follow general expected patterns - The HPI shows exactly this.

I don't understanding why you continue to ignore a higher quality dataset, particularly when it is showing a pattern far more consistent with what you'd expect from falling sales volumes.

Yeah, that's one very strange omission in this article. Greg says that the decline in sales numbers has not been followed by a decline in price, because look at the median and the lower quartile. Yet the REINZ HPI - the golden standard of measurement - has indeed declined in price. By 4.4% in April and 3.something% in May, before inflation.

I agree. clearly Greg is trying to bait the spruikers.

Hook, line and sinker! comes to mind

I see many of the Baby Boomers who had money tied up in a nice Investment Property will see their nest egg evaporate considerably and the younger generations are still wishing prices to fall further to be affordable. If we follow Australia by one year, then I see prices falling further no matter how much the RBNZ alters the cash rate and banks lower interest rates. Lowering Interest rates is just a move to get borrowers through the door, if a more organic approach, prices can come down to meet the borrowers demand. If manipulated, we are heading for recession territory. Young people are increasingly concerned about negative equity in this current market.

When houses are million dollars plus and borrowing in 700s to 900s a slight fall in interest rate does not matter much (Though is good) instead of paying $850 or 1000 per week will pay $820 or 800 or $950 which in itself speaks the level of debt UNLESS interest rate drops to 2% or 2.5% and start offering 10 years or 15 years fixed term as any loan borrowed is mostly for 25 years or 30 years.

Prices through most parts of New Zealand are very reasonable and represents value!

NZ is a great country to live in, although the current coalition government is not travelling very well at all!

The property negatives that keep commenting about house price drops need to get real and appreciate that if they don’t own their own home by now then they probably never will!

Forget about what the property market is doing and buy a property that is good buying, improve it and you will build up equity and go from there.

This is what most successful property people have always done and it is a winning formula!

Not negative for long term (few years) but Yes for now it is falling and this downward trend is here to stay and anyone looking for long term should invest but should wait and watch as house price has to catch up / fall and by waiting more chance of getting more for your $$$$$$.

Hi THE MAN 2,

What you write above is a simple, sensible, well-proven/time-honoured investment strategy......

But still the DGM lack the wherewithal to implement it.

Instead, they come here moaning and groaning, whinging and sniping - but never making any progress.

TTP

I agree with you completely about other parts of NZ. I was blessed to have shares in property in the North and South Island in my early 20s, then when the Global Economic Crisis hit in 2008 I waited until it bottomed out and purchased again in 2009, just North of Auckland.. So glad I did buy then as I probably would not be able to afford the same today. My tiny cottage up here is RV over half a million. It's nuts, I don't think it's healthy for our future generations... Can't help but think that opportunity to buy low again is not too far away though. Maybe next year or 2021 there will be another chance for more young working people in Auckland to purchase their home. Love life, learning, legacy ;o)

It wouldn’t be a comments section without the ad hom filled squabbling between camp spruiker and camp DGM.

We need a points board that tallies up the number of likes spruiker and DGM commentators receive on an article.

Prices will continue falling

As you know Greg, asking prices have fallen about 7% in Auckland, on RE NZ, in last 3 months alone.

That is in peak selling season.

Median is not best measure of what is happening NOW.

Prices will be further hit when developers and builders stop waiting to list property for sales and have to list it due to needing quick money due to revolving increases in debt servicing costs, at same time as revenue is falling. That increase in supply on top of a rapidly ageing stock for sale, will crash prices.

Expect Auckland prices to fall to median of $670k by end of 2021

yes a big drop in asking prices is an indicator of what is to come.

Doesnt matter how much you drop your asking price if you still cant sell it. Pressure will be rising for a lot of the overpriced dumps out there.

Watch and wait..

I’m seeing a few more advertised mortgagee, and fairly desperate sounding real estate ads in Auckland now. Quite a change from a few years ago. Still, prices are very high on a price to income level, and certainly in world terms. Odds are prices will give way, just like they did in Australia. If they set off upwards, it’ll only add to the overall NZ bubble and unaffordability. Interesting to see the ANZ shenanigans in the past week too. Something seems to be going on there, beyond the little we know.

It is real simple Auckland land prices have been falling since 2017, meaning:

- There are less sales as the capital gains of 3-8 years ago no longer occur and flipping is not profitable.

- The top end has fallen, because the top end price is mostly land value.

- The middle/bottom is stabilised by an increase in supply.

Which part of the NZ property market is not just Auckland do people not understand.

We are all aware that prices have grown remarkably to what they were 10 years ago fueled by overseas buying.

Houses are extremely affordable and represent great value in most parts of NZ if you are motivated enough to buy.

Whinging on and hoping that prices will crash will not improve your own circumstances, as if you haven’t bought in the last few years then chances are you probably won’t in the future.

Interest rates are low and Banks are keen to lend.

You can buy property around NZ for less than the cost of renting if you are intelligent enough to see this!!!

The challenge is finding jobs in a lot of these areas in the career paths that a lot of First Home Buyers might be heading. I guess people could always throw away their career prospects, get a job at a small town supermarket and buy themselves a cheap house.

But I agree, you can buy property around NZ for less than the cost of renting. I've been a home owner for 2 years. My combined Mortgage/Rates/Insurance is 15 - 20% less than the market rent for a lower quartile equivalent. I also have a fairly decent commute to the office.

NZ Housing market has largely been pushed by investors and overseas buyers for years. Unless you are an ostrich with your head buried in the sand, the world economy is heading downward. Overseas buyers are almost gone, investors with steel balls are still there in the game but only few of them. Up talk of buying properties in CHCH, Timaru, or even Palmy North (don't know what the attraction is in PN) will be just noise.

https://www.abc.net.au/news/2019-06-24/ian-verrender-analysis-awful-eco…

Chairman, I only buy in ChCh as I beleive it is the most sound rental market in Nz and the upside in property values in the next few years is huge.

There have been several reasons why the CHCh market hasn’t boomed but hasn’t dropped either and there have been great buying opportunities!

ChCh the most desireable city to live in going forward!!

"ChCh the most desireable city to live in going forward!!" yeah nah...

Chairman, have you ever lived in ChCh?

Have lived in Oz and it is overrated!

Too many taxes !!

Ah yep.. 4 years, our house was in Marivale (around Holmwood Rd) and it was pretty crappy!

Also lived in Palmy North for 2 years..

You are right a lot of crappy cold homes in Merivale.

More money to be made in Christchurch in property than Oz!

Better relaxed lifestyle as well, although Oz good for holidays,

FYI, re Auckland property market

Days to sell in May 2019 was 45 days.

This is the highest for the month of May since 2008 when days to sell was 49 days.

This is similar with Jan 2019, Feb 2019, March 2019, April 2019. The days to sell in these months this year were the highest since the 2008/2009 period for the same month in those years, so we are reaching 10-11 year highs on this metric. That metric indicates that the Auckland residential property market is currently a buyers market.

So in Auckland, there are:

1) stable, slightly falling property prices, (definitely not rising)

2) and longer days to sell residential property located in Auckland- the highest level in 10-11 years.

Also note that in 2019, we have an economy with positive growth. In 2009, the economy was in a recession.

Note in 2019, the unemployment rate is about 4.2%, whilst in 2009 it was rising and peaked at over 6% unemployment in 2010.

What is going to happen in the Auckland property market if the economy goes into a recession? The RBNZ has already made one cut to the OCR, suggesting that their economic outlook is definitely not optimistic.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.