Activity ticked up slightly in Barfoot & Thompson's auction rooms in the first week of spring, but the overall number of properties being auctioned remains at their winter lows.

Barfoots marketed 87 residential properties for sale by auction in the week from 2-8 August, up from 67 the previous week and 72 the week before that.

Of the 87 auction properties, 37 were sold under the hammer, three were sold prior to the commencement of their auctions and two were sold immediately after their auctions, giving a total sales rate of 48%. That's up slightly from 45% the previous week.

The Manukau auction was the busiest of the week with 19 properties on offer and a sales rate of 58%. Things were much quieter at the North Shore auction where just 11 properties were on offer and the sales rate was only 18%.

The on-site auctions were also quieter than usual but some good results were achieved at some of the smaller auctions such as Pukekohe where the sales rate was 60%. See the table below for the full results.

Details of the individual properties offered are available on our residential auction results page.

The comment stream on this story is now closed.

| Barfoot & Thompson Residential Auction Results 2- 8 September 2019 | |||||||||

| Date | Venue | Sold | Sold Prior | Sold Post | Not Sold | Postponed | Withdrawn | Total | % Sold |

| 2-8 Sept | On-site | 1 | 3 | 1 | 5 | 20% | |||

| 3 Sept | Manukau | 10 | 1 | 6 | 1 | 1 | 19 | 58% | |

| 3 Sept | Shortland St | 6 | 7 | 13 | 46% | ||||

| 4 Sept | Mortgagee/Court | 2 | 1 | 3 | 67% | ||||

| 4 Sept | Whangarei | 1 | 1 | 2 | 0 | ||||

| 4 Sept | Shortland St | 6 | 1 | 4 | 2 | 13 | 54% | ||

| 4 Sept | Pukekohe | 2 | 1 | 2 | 5 | 60% | |||

| 5 Sept | North Shore | 1 | 1 | 7 | 1 | 1 | 11 | 18% | |

| 5 Sept | Shortland St | 2 | 1 | 3 | 67% | ||||

| 6 Sept | Shortland St | 7 | 1 | 4 | 1 | 13 | 62% | ||

| Total | All venues | 37 | 3 | 2 | 35 | 4 | 6 | 87 | 51% |

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address

.

115 Comments

Not too much to read into sales up but numbers down.

The relationship between the number of property and percentage of sales is not a direct or clear indicator of the state of the market.

As the market changes so does the best method of marketing a property changes. For example in a very hot market (as in 2012-16) when it is hard to put a price on a property an auction is the best method of marketing a property and determining best market price. Equally, when the market is stagnant (e.g. 2017-18) and one is keen (verging on desperate) to sell, then auctions are also probably the better marketing method.

What can we read into number of auctions down but sales - compared to recent events - are slightly up is that the market could be returning to more normal conditions. However, that is a little bit of a tenuous call.

Yes - it does appear that the market has recently become a little more buoyant compared with 2017-18........

But we'll have to wait and see whether this is just the Spring uplift, or something more permanent.

TTP

this is the much awaited SPRING you'll have been awaiting!!!

volumes down and sales achieved barely on half of them!!!

shivers down your spine???

The spring increase in listings seems to be delayed compared with last year, and the oversupply of Auckland properties reducing just a little. This time last year, total listings had started to increase noticeably; this year, still a slow drift down. Will be interesting to see if the increase is just late, or if something else is happening.

probably just too much rain this year...

I guess it's possible. Do sellers really wait for a good weekend forecast before pulling the trigger to list?

Well, you'd want to get the garden sorted, the house washed down and everything looking good before the buyers start coming through, so yeah, the persistent shitty weather would slow down all of that. Waiting for the front lawn to not go squish squish underfoot helps too.

The Wellington spring listings bounce is still MIA though too and our weather has been glorious at times.

Okay, interesting.

The 2017 listing uptick was later, e.g. not yet, but I put that down to the election and coalition negotiations. I don't have records further back than that.

We have had a couple of southerly blasts bring Winter back. Though glorious today (Tuesday being when most houses are listed on Trade Me) and Sunday looking fine. Still you're right, I expected more listings by now.

It usually take weeks to prepare to list, and agents don’t hold back because they need their sales pipeline. Unlikely it’s anything to do with weather. Spring selling season has started.

Was interesting to check TTP's comments this time last year:

Mon, 10/09/2018 - 16:58

"Auction clearance rates in Auckland are now commonly around 40-50% - and sometimes more than that.

Prior to June 2018, clearance rates at these levels were a rarity and - surprise, surprise - the DGM embraced the lower rates with unmitigated enthusiasm.

If the DGM dislike the re-emergence of higher auction clearance rates, then tough!"

Then over the last year the Auckland market has had one of its slowest first 9 months of the year in many years. Even Barfoot and Thompson's own figures say

Aug 2019 746 properties

Aug 2018 795 properties

August 2019 was down 6.2% year-on-year

12 months to Aug 2019 9,160 properties

12 months to Aug 2018 9,421 properties

August 2019 year-to-date down 2.8% year-on-year.

TTP, where are you getting this idea that Auckland has been more bouyant in 2019 than in 2018/17?

Certainly seems like B&T are only taking "likely to sells" to auction now (north shore excepted)

This was evident last month too where the clearance rates showed a good rise but on much lower volumes and at the end of the month B&T still ended up with its worst August for sales for 9 years

absolutely.. hence TTP's point of the market being buoyant is ridiculous....

TTP is very consistent with the nature of his comments

Ill agree with you, provided you are referring to him saying generally flat prices

Yes, I still find his posts in this thread amusing.. https://www.interest.co.nz/property/99794/lower-interest-rates-flat-hou…

Ah, I remember that. In between then and now, I found the IRD statistics on how much everyone earns (or at least how much they pay income tax on). I can now state confidently that there are a grand total of 56,110 people in all of New Zealand making $200k+. If they all married each other (extremely unlikely, at best), that would be 28,050 couples. In all of New Zealand. Not at all uncommon indeed.

Given his core point was that BigDaddies statement is wrong: "Anything much over $750K cannot be considered." Id say its a minor infraction. Nor would I consider that one of his core opinions.

I mean, BigDaddy was much closer to the truth than TTP there. I'm sure he would be happy to hear you have judged his infraction as minor, though. Is he your dad or something?

Hes been calling flat prices for something like two years. I prefer to read sensible statements like that rather than the streams of conspiratorial nonsense like 'Auckland down way more than the media is letting on', '50% correction coming', 'RBNZ cant push rates down', 'overseas funding pressures will send rates soaring', 'banks will be calling in their loans soon', 'unemployment will resemble Ireland' etc.

It was just another fine example of what TTP proclaims being complete nonsense. Many young couples on 2 x $200k. Hilariously wrong.

That FHBs can spend more than $750k.. yep, although those spending $1M+ I would expect to be pretty rare. So it all depends where your interpretation of BDs "much over $750k" lands

Where did TTP say the market is buoyant?

TTP

looking at west auckland, price achieved are well off their highs on what used to be attained on similar properties.. vendors are getting realistic...

To be fair West Auckland has a lot of dumps and benefited by the rising tide lifting all boats.

I think its fair to say that areas like New Lynn, Kelston, Glen Eden, Te Atatu, Ranui, Henderson and Massey are all at risk of large falls

cannot disagree with that!!!

Auckland overall has a lot of overvalued dumps, and the standard of new “affordable” builds doesn’t look great either for the long term. In a few years we’ll facepalm at the prices people were willing to pay for them.

https://www.trademe.co.nz/property/residential-property-for-sale/auctio… (check the interior pics). Probably structurally fine..

Sold over asking. If you aren't from(south) Auckland, Randwick Park is halfway between Manurewa and Takanini. not a highly desirable neighbourhood.

In 3 years will the new owner be patting themselves on the back for having brought well, or drowning their sorrows?

sold???

there is still an open home

Just the slack agent not taking the open home off the website(s). Sold sign on ground outside property, and spoke to agent.

so it didnt sell at auction, came on with an asking price and it sold for more than the asking price?

Yep, nothing to do with auctions, was just an example of whats out there and what its selling for in cheaper parts of Auckland. Agent said 40 groups through the open homes (x2), and 9 made offers.

Soon you can spot RE agents enjoying their organic soy lattes around Ponsonby, browsing through the latest Maserati brochure.

I suspect there are people with low debt and regular income/jobs browsing the Turners repo auction. Some real bargains were had during the GFC, mainly at the expense of REs and Developers.

Too right. I want a jetski for summer

I have added Mr Ninness's total and appear to come up with 87 properties, which would mean under 50 percent sold . Is my math flawed. ?

Looks like he changed the headline to fix that.

hats off to you.. that was some investigative work :)

good on ya

Sale prices above and below CV is what tells the story for me, a month ago it was arround 50/50. Not long ago you would have struggled to buy anything even close to CV.

House prices have dropped a hell of a lot more than the mainstream media is letting on.

I do love a good chuckle,

From a quick skim it still seems about 50/50 in Auckland?

If that slides yes we'll most likely see a higher auction clearance rate but that isn't the big story.

In Wellington and Dunedin I look at the CV and do a quick caluation of add a $100 to $150 K. It's not looking like that in Alk.

How do you conclude "House prices have dropped a hell of a lot more than the mainstream media is letting on" when sales above and below CV have remained about 50/50 over the last few months?

Hes already explained it, he does a quick calculation for Wellington by adding 100k to the CVs, butta bing, butta boom, Aucklands down 20%+

Does anyone know of a source/tool that can show daily listings across various NZ markets?

Thinking somethign which automatically tallies all new listings on TradeMe, daily.

I think you can get the TradeMe app to email you every morning about new listings, and you can set it for any criteria you want.

Working on one, will add more once I get more data http://propertylistingstats.co.nz/

"Meow!"

The numbers are certainly suggestive of ongoing weakness. How weak is the big question.

We need a couple more months of data to draw proper conclusions.

It's hard to draw big conclusions either way at this stage.

So far it’s not the spring the optimists were hoping for. It’s what the realists were expecting. No major slide yet, but I expect a slow slide down over a period of years to produce a reversion to (or below) the historical mean of price to income ratios. The RBNZ will try to throw the kitchen sink at it which might produce a dead cat bounce of sorts, and inject even more mortgage debt into the bubble they don’t even seem to see.

yeah.

The crash has been delayed. It will come though. When, I don't know, but likely in the next 5 years.

5 years is long time to wait..

Not suggesting at all that anyone should wait for a crash.

But it's something to keep in mind if you are considering buying with a 5-10% deposit....

Timing the market can be a futile exercise, but looking at long term probabilities is not. With values and price to income ratios at these very high levels, in a global comparison, it's much more likely the short to medium term future of the NZ property market is not for capital gains, quite the opposite. Yes, I'd be in no hurry to enter the market with low equity at this point. It's just asking for a negative equity situation for coming years.

Yeah. Equity is critical. If you have at least 20% deposit you should be safe-ish.

IMHO 5-10% is risky though, and I am not sure if it is responsible for the govt to be promoting 5% deposits.

Agree, I wouldn't advise anyone to buy with less than 20% deposit. If the economy/unemployment remains steady I don't see large price falls, but the precarious nature of the global economy creates a massive amount of downside risk.

My viewpoint is likely skewed slightly by living in europe during the GFC - and watching what happened to those with low equity who bought in late in the cycle. Unfortunately too many Kiwi's still don't really seem to comprehend the possible downside to over leveraging in property.

As we approach an OCR of zero there is much less future potential to buffer against recession. That, to me, is the big question moving forward.

Always a slow down leading up to the US elections. Slow down anymore and we hit stall speed and fall out of the sky.

Then Brixit, Hong Kong and all the other side shows..... it only takes one to errupt to start panic.

I'm not expecting a crash, even within the next 5 years. I suspect that a fairly high median multiplier is the new normal.

Having said that, I do expect the (Auckland) market to fall further over the next 1-2 years.

It's interesting because Auckland has had 12 straight months, starting last August, where the HPI has been lower YoY. So with the soon to be released Aug 2019 HPI figures it may be more useful to look at the 2 year YoY delta to get the true picture.

I'll be waiting until the October HPI data is in before drawing any initial conclusions about the market. That'll give time for the Spring selling season to play out. I predict that October HPI will down around 3.5% YoY, meaning it's down 4% over 2 years as last Oct was already down 0.5%. If that happens, then I'd expect the market to fall a further 0.5-1% over the rest of summer so that March 2020's HPI is down 4.5-5% over the previous 2 years.

Of course if HPI shows a significant relative improvement in October, e.g. less than 2% down YoY, then I'd probably take it as a sign the market is strengthening.

Whenever people start using phrases like "the new normal", It's time to expect a major drawdown. Do you know how many times in history this has been the case? Every. Single. Time before a major correction. Let's go way back to 1929 for instance: Two months before the stock market crash, economist Irving Fisher said “Stock markets have reached what looks like a permanently high plateau.” Every generation and every bubble seems to repeat something similar.

Perhaps. But I believe there are areas in the world where the median multiplier has been quite high for a long time. Who's to say Auckland isn't going to be one such area? Even after the recent Sydney correction their median multiplier is still very high. Doesn't mean there can't be a crash, in either Auckland or Sydney, but I wouldn't bet with any great confidence on there being one in the next five years.

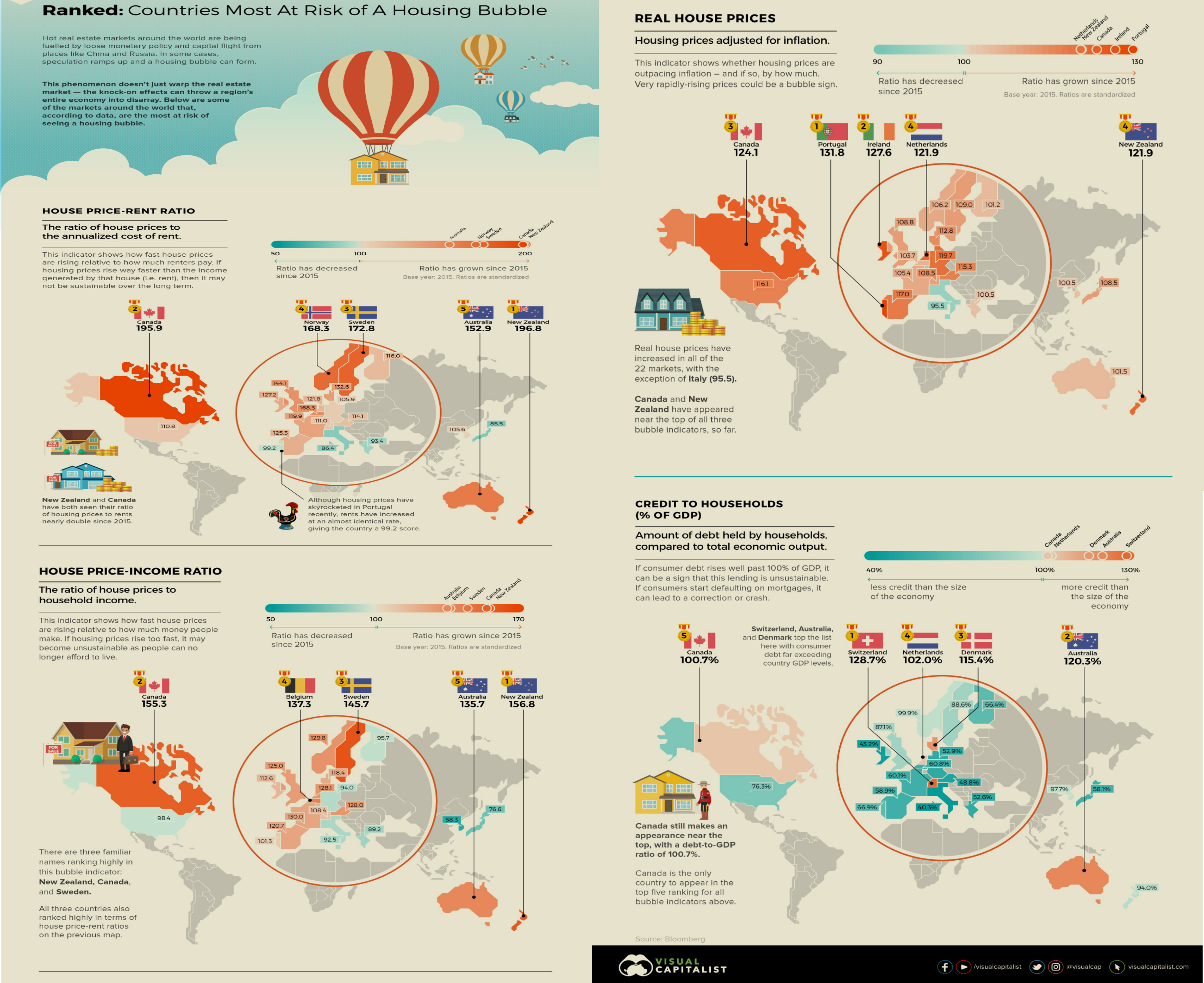

New Zealand is now number 1 in highest house price to income ratio. And number 1 in house price to rent ratio. We don't do great in the other two bubble indicators either. Here: https://miro.medium.com/max/3424/1*HViS7TYCIBfQ9ecqoF93QQ.png

{kind=link}

Sure. That's one reason why I expect prices to fall. Just not expecting a crash. I could be wrong, but so could others :-)

Common thread for 1 & 2 in both of those measures is the combination of influx of overseas capital + cheap access to credit creating the disparity. In Canada's case (particularly Vancouver), that capital influx was sustained over a longer period & a lot more substaintal than NZ.

Luxury end of their housing market (at the levels out of reach of normal working people), are way down. Circa 40% in some suburbs of Vancity.

Fair enough.

But I will put this to you. We are nearing an OCR of 0. Even if the economy improves on the next few years, it's hard to see it rising back over 2-3%.

What happens to the housing market when a recession hits and the OCR can't be cut more than 2-3%?

The only real reason I think big falls have been prevented in the past 2-3 years is because the ocr has been cut 3-4%

"Even if the economy improves...."

What usually happens when the economy improves Fritz? People buy houses.

The RBNZ have avoided the next recession by cutting the OCR to 1%, didn't you hear? ;-)

But sure, if there's a recession it'll put a dent in prices. Doesn't necessarily mean a crash though. It could be closer to a 10% dip like around the GFC, particularly if it's a mild recession. Combine that with the expected (non-crash) 5-10% drop and we're still looking at an overall fall of 15-20%. Debatable whether that's a crash. It's just one possible outcome of course.

Other than the possibility of a recession I'm curious about the flow on impact of the Fonterra debacle.

Fritzy old boy you seem to be doing a jacinda and ditching your original targets. The big property crash that was supposed to have happened by now and now are pushing the date out by another 5 years. Very open ended ...

? Stop making rubbish up.

I predicted a fall from peak to trough of 5-10% in Auckland. That's pretty close to the mark, depending on how you measure.

It's only recently I have been putting timeframes on a crash, and I have been saying within 5 years, possibly 2021-22.

It's not unreasonable Fritz but pushing a forecast out to 5 years is meaningless. I can tell you with 100% certainty that the market will crash and also that it will take off if I put a long enough timeframe on my prediction

As a property investor, you're not interested in what will happen to housing prices in the next 5 years? Do you buy and sell in a shorter timeframe than that?

Nope

Why is it meaningless?

5 years is not a long timeframe, at all. It's 'Short / short-medium term'

If I said 20 years, or if I said 'sometime in the future' then sure, it's meaningless.

And note I've said within 5 years, and possibly 2021-22. So it's pretty specific. I'm not sure how you can credibly call that a vague and meaningless prediction!

Let me ask you this - if there is a recession in the next 5 years - which is reasonably likely given we haven't had a proper one for a while, and there are a lot of headwinds - what is going to hold property prices up, when there isn't much scope left to cut interest rates?

Or are you very confident there won't be a recession in the next 5 years?

There may be a recession, there may not,

House prices may go cold or may go hot

Up or down by a little or a lot

Stop speculating and give it a shot

It is now time to cultivate your plot

"The crash has been delayed. It will come though. When, I don't know, but likely in the next 5 years."

Vague claims that could "likely" happen are completely not credible. Why do you persist with this twaddle Fritz?

Ask your mate ttp, his are just as vague.

I haven't noticed

You are really full of crap and juvenile. I actually feel sorry for you.

What's the average IQ of a property investor? 80?

You actually seem really worried.

That is a hilarious comment coming from you Fritz old boy and funny how you have no hesitation to use ad hominem against me and investors in general but have a massive paddy crying foul at the slightest hint of an insult against team DGM. You need to grow up.

Interesting to see that Housing NZ dwellings still seem to be a fairly low % of the total dwellings consented in Auckland. 109 dwellings on HNZ or Tamaki Regeneration land were consented in Auckland, out of 1454 in August.

http://www.knowledgeauckland.org.nz/publication/?mid=2945&

What I know though its that some developments are done on private land by private developers and 'handed over' to HNZ. Impossible to tell from the data how prevalent that is.

Building for HNZ is going so well that stanley group has liquidated.

On the Northshore the number of houses listing in Devonport, is really high compared to the affordable areas of Beachhaven, Birkenhead and Birkdale. When these fail to sell will we start to see a slide then? Apart from that the market is pretty hot in the affordable price ranges.

Also seems to be true further up the shore. Pretty quiet in the coastal areas where every vendor thinks they can get $2m, but most aren't yet under much pressure to sell, and so don't.

The odd motivated sale is illuminating, though. Just saw one posted which sold recently for 13.5% less than its most recent 2016 sale. Judging by the photos it hadn't changed a jot. 300k loss in three years, pretty nasty; make it nearly 350 after paying the agent.

We are FHB's hoping to buy in Devonport. There is an awful lot of junk on the market in Devonport that has been sitting on the listings for months on end. Then there is an awful lot of high end properties. Not a lot of decent stock that would be considered entry level even for expensive suburbs like Devonport. I can only assume the more expensive properties are struggling because of the foreign buyer ban? It will be interesting to see whether this brings prices down overall.

Devenport is not an "entry level suburb"

I'm well aware. That's why I said 'even for Devonport'. I'm trying to point out that the listing are skewed towards high numbers of higher priced properties at the moment.

What seems to be overlooked is that 11 proeprties were withdrawn or postponed. This almost always means that interest was so low that the vendors took the sensible decision not to proceed to auction and have a public failure. If you add these in then we have 43 not sold against 37 sold which give a failure rate of 54%

Nearly half sold under the hammer and more will probably follow in the next few days. Which means the market is evenly balanced

The market is evenly balanced? I thought auctions represented just a tiny segment of the property market nowadays. So the best we could say is that an increasingly smaller slice of the market is balanced. Whatever balanced means.

Yep, this is relevant : In Auckland in July, 14 per cent of homes sold via auction, compared to 20.4 per cent a year earlier.

from the story on Stuff about the Block auctions.

The Block auctions were a huge disappointment for viewers. A MASSIVE letdown for contestants.

Personally I found them hilarious. Hadn't watched any of the shows, just happened to be flicking channels and thought they'd be good for a laugh.

Given your vast experience in property and your balanced- rather than troll-ish - views, it's always good to hear your opinion Big Daddy.

by Fritz | 10th Sep 19, 6:44pm

What's the average IQ of a property investor? 80?

last 3m (May, June, July) residential only sales in Auckland were 4.8% above same 3m in 2017.

They were 37.5% down on 2015.

Rodney and Waitakere doing better simply because have more stuff for sale under $800k.

Auckland City apartment sales in the last 3m are 45% below 2015 in same 3m.

Yet we have substantially more being built all the time...Sales are 10% below 2018 for same 3m.

Peak listing for Auckland in last year was 14,041 in early December.

It's low point was 10,162 on September 2nd.

Market for FHB improving due to low interest rates and recent cuts.

But they risk equity wipe out next year.

Interest rate cut weapon now almost out of ammo.

What happens when economy GDP growth falls below 2%?

I find myself actively seeking out your comments more and more. No emotion. Just the numbers. I like.

I don't think The Man 2 will save you when the revolution begins

For those obsessing about a "property" "crash". There won't be one unless and until we have another GFC.

Which is likely since global debt and leverage is so much higher than in 2008.

I would expect that about October 2020 - 22 (I worst in that time frame.)

Prices in Auckland to fall 35% peak to trough, when peak was median of $900k in March 2017.

I only expect small falls in prices in next year.

Sales in 3m to end of July in Auckland were 37% down on same period in 2015

In some areas of Auckland, sales have picked up in last 2 months, compared to 2018 but that is because 2018 was a land sections and apartments sales bubble caused by front running OBB. Even that did not raise 2018 annual sale much above 2017. Sales have been falling since 2015 peak and last time affordability was a reality was 2012, since when sales are down 34% in Auckland as a whole.

Agree. That's close to my 2021-2022 timeframe.

The critical thing is the RBNZ won't have much ability by then to rescue the market.

I see small falls or small gains until then.

Fritz, does that mean then once the OCR is 0 and house prices start to falter, they will inevitably have to tank if all other factors continue on their current trends?

No not necessarily.

I only think they will tank if there is an economic shock. Which is more likely to be external (ie. another GFC) than local.

I think some parts of the economy will weaken over the coming 1-2 years, and unemployment will rise, but not enough to crash the market.

But the rise in unemployent will be a factor that limits the potential for price gains in the next 1-2 years.

Ok yea I see. So considering a GFC becoming increasingly likely, would it be fair to say house prices will come back substantially at your 2021-22 prediction?

Yeah my pick is that the NZ economy will hit a brick wall in the next 5 years, probably due to a GFC (but there could potentially be a local event, eg, an earthquake in Wellington, or on the Alpine fault. Or maybe the construction sector really collapses - a possibility - and that drives a rise in unemployment to 7-8%).

By the time that occurs, the OCR might have risen up again 'a little'. But it won't have risen up enough to give the housing market the support it needs by way of large and repeated cuts to the OCR, once the economy slumps.

Youngdumbandbroke - Please read 'Iceman' comment below, it is spot on in my opinion. It's easy to be swayed on sites like this by DGM's that are hell bent on a crash. This is a correction that happens every 9 year cycle, it is an opportunity for those who can see that. As always buy what you can afford, and pay debt down as fast as possible. In this downturn I have purchased 2 more properties and helped one of our offspring into their first home.

Many many people have been caught out as in 2008 waiting for the crash that never came, goodluck with whatever you choose to do.

I tend to agree with Fritz. (Not that any of us can be sure.)

I see prices as flat/dropping away very slightly, unless there's a global shock.

How much that shock affects us will depend on its nature. A real meltdown in the Chinese economy would have a big, big effect on Auckland prices. A sudden spike in inflation -- which could be caused by something like an oil shock -- could force the OCR up, which would cause defaults. A collapse in equities markets would probably have less of an effect of property, except to the extent that some dividend-dependent property owners might be forced to sell up.

If these kind of accidents can be avoided, and we have a long run of very low inflation/low interest rates, prices will be more or less flat for as many decades as it takes for wage inflation to catch up.

yeah, it's very much an 'educated guess'

Correction... un

"..very much un educated..."

Rather than making ad hominem attacks and baseless/ worthless comments, you could instead be more productive and constructive.

So in the interests of mature debate - rather than childish nonsense- please advise why you think the housing market will be resilient to economic downturns/ recessions in the next 5 years, given we won't have the luxury of large cuts to interest rates.

Look forward to your viewpoint.

As you know by now I don't hold extreme views either way. So I am open to *logical* arguments from bulls or bears.

"Childish"

Like the comments you make .... such as telling The Man to stop commenting in the interests of "himself and everyone else". You sure do talk bs and I intend to keep calling you out for false and wild predictions

.

BAU - Steady as she goes.

Those hoping for a crash are dreaming, the fundamentals of supply vs demand don't change.

What was the 'crash' here during the GFC? Def not 20% plus that some of the DGMs are hoping for might happen this time.

Speaking to a mortgage broker and agents recently confirm that FHBs are actively on the hunt. I've also noticed more people through open homes. Still expect weakness in prices over the 1m mark. Good properties will still be contested for and will be sold for good prices as always. Are we in oversupply territory? No. How's the Aussie market doing? Decent/Picking up. How's the sharemarket doing? Gangbusters. Bring on spring. Prices should go along the lines of steady or a slight decline before demand picks up again in a year or so. FHBs putting off buying in the hope of further declines are making the same mistake that people made after the GFC if they put off buying.

'Those hoping for a crash are dreaming, the fundamentals of supply vs demand don't change.

What was the 'crash' here during the GFC? Def not 20% plus that some of the DGMs are hoping for might happen this time.'

Prices did drop, more than 10% - even though supply and demand didn't change. Also, NZ had the luxury of being able to cut interest rates a lot from a high level. That prevented a crash. We don't have that luxury anymore.

If there is another recession, as there will be, what do you think can be done to keep the housing bubble afloat? Given there's not much room to cut interest rates.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.