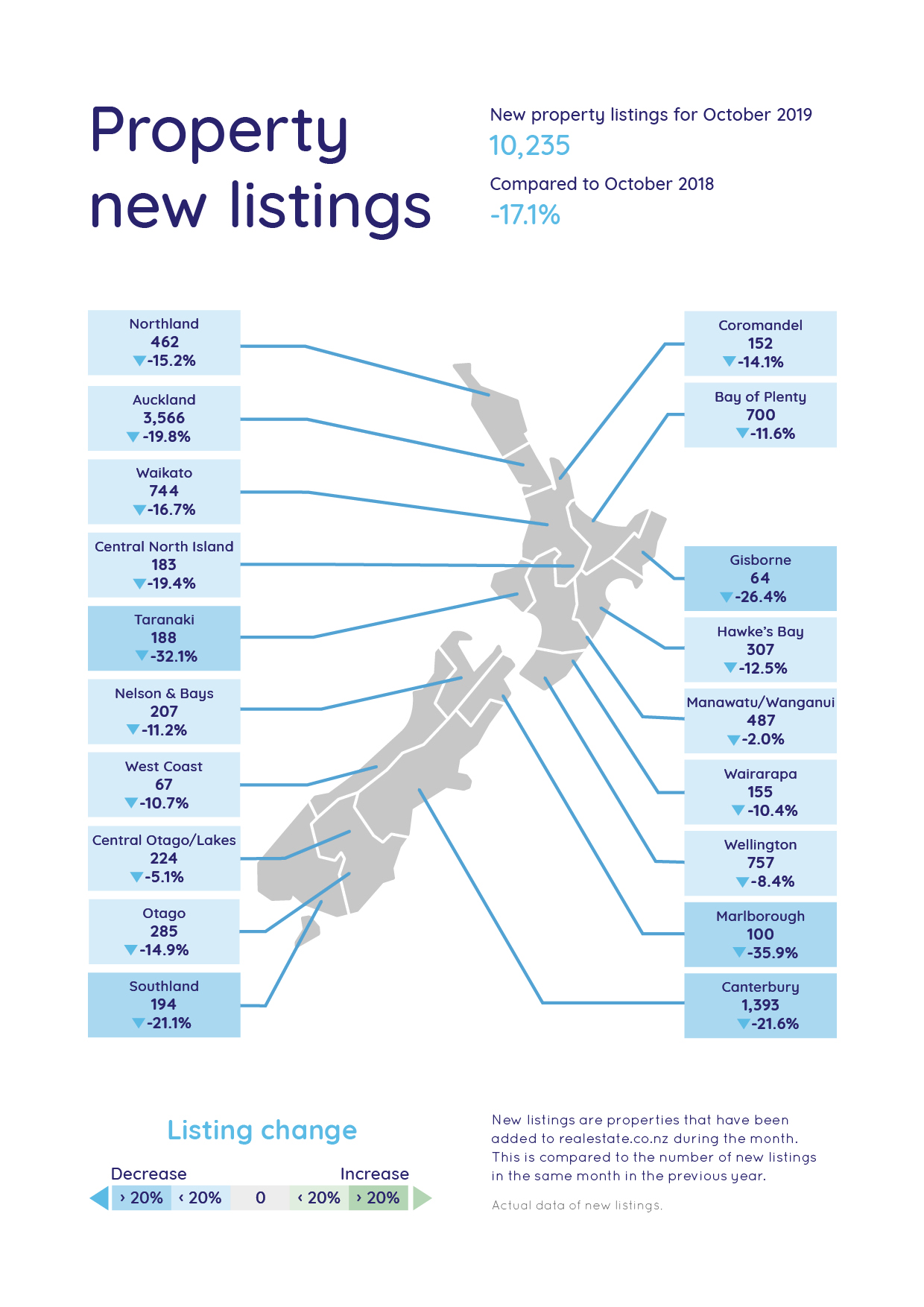

The latest figures from property website Realestate.co.nz suggest the housing market remained subdued in October with fewer vendors putting properties on the market.

The website received 10,235 new residential listings in October, up 15% compared to September but down 17.1% compared to October last year.

That was the lowest total number of new listings the website has ever received in the month of October and the downward trend was nationwide.

New listings were down compared to October last year in all regions of the country, with the decline ranging from 2% in Manawatu/Whanganui to 35.9% in Marlborough.

Around the main centres listings were down 19.8% in Auckland, 16.7% in Waikato, 11.6% in Bay of Plenty, 8.4% in Wellington, 21.6% in Canterbury and 14.9% in Otago (see chart below for all regions).

Realestate.co.nz spokesperson Vanessa Taylor said people had been late to list their properties for the spring upturn this year, although buyers had remained active with more than a million unique users on the website in October.

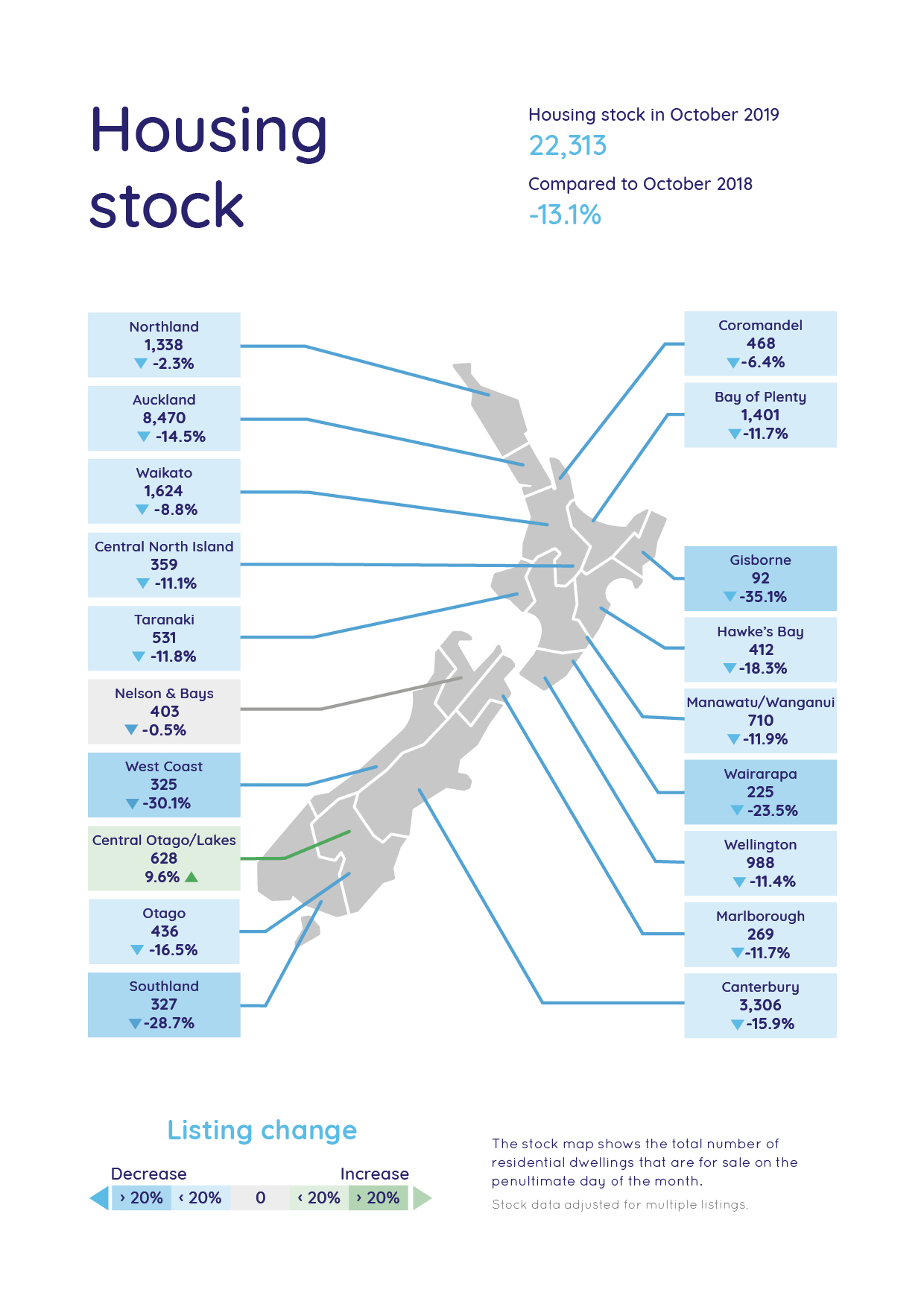

Housing stock - the total number of properties available for sale on the website, also hit a record low for the month of October, increasing from 21,174 in September to 22,313 in October. However, it remained down by 13.1% compared to October last year.

The decline in total stock was almost nationwide, with only Central Otago/Lakes bucking the trend and recording a 9.6% increase in stock available for sale compared to October last year.

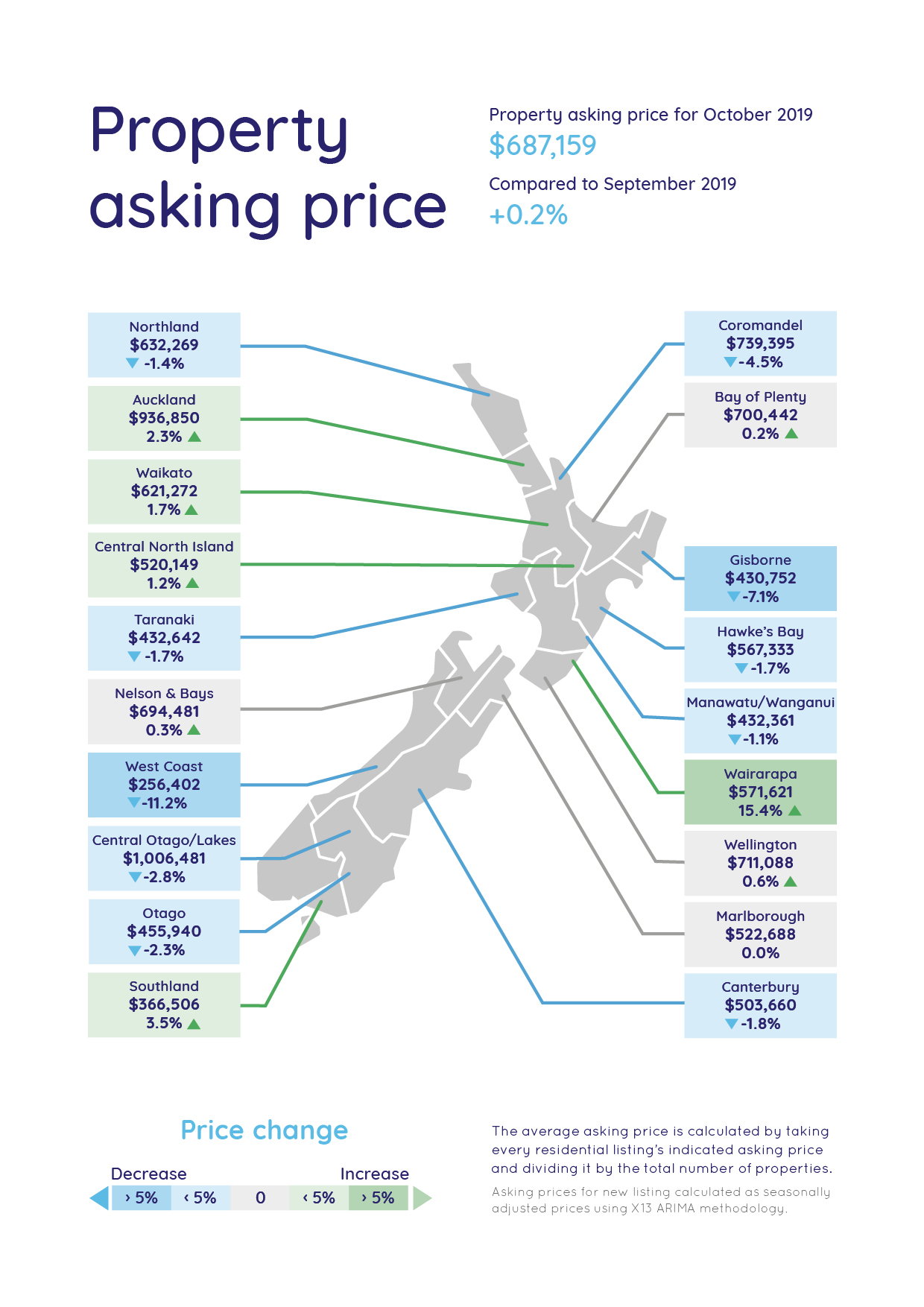

Average asking prices were flat overall compared with September, with the national asking price of $687,159 in October up just 0.2% compared to September.

Around the country eight regions (Auckland, Waikato, Bay of Plenty, Wairarapa, Central North Island, Wellington, Nelson & Bays and Southland) recorded a rise in the average asking price in October compared to September, while 10 regions (Northland, Coromandel, Taranaki, Gisborne, Hawke's Bay, Manawatu/Whanganui, West Coast, Canterbury, Central Otago/Lakes and Otago) posted declines, and Marlborough was unchanged. (See the chart below for the regional figures).

The comment stream on this story is now closed.

157 Comments

Auckland new listings down 19.8%, housing stock down 14.5%, asking price up 2.2%.

I have never put too much weight on Realeaste.co figures but another indicator that the Auckland market could be firming. Note use of "indicator", "could" and "firming".

Real estate sales work like this. If you cant séll your property for more than you paid for it, in most cases you dont sell.

There's always a small percentage that have to sell, be it because:

1. The bank forces them to sell,

2. Partnership splits,

3. Loss of employment,

4. Relocation for employment,

5. Estate sales,

6. Growing family.

I would suggest the past (larger) volume of sales can be attributed to people buying bigger houses or relocation to better areas (in an attempt to keep up with the Jones) by means of larger mortgages facilitated by the fair weather banksters. These banksters have now gone to ground, and in some cases now want their money back (or should I say their term depositors money back). In the case of the big 4, thankfully we now have a reserve bank governor who understands the risk these banks have exposed the term deposit holders to and asked them to shore up their balance sheets. Their parents are not interested in supporting them (and probably never have been), and only ever been interested in short term profit maximisation.

With less marginal lending now available, real estate transactions had to decline. Its just a question of how long will it be before an appropriate price correction is due. Labour are doing their best to keep the sinking ship afloat with home start incentives; which are only ever temporary; driven by re election appeal. I do pity the inexperienced that take advantage of these, as history has shown loan incentives can only distort the market for so long,

While interest rates are at historic lows, this is not a good sign and has more to do with keeping the banksters afloat (for a little while longer) than anything else. Take it from a seasoned investor, it is the best time to pay down debt than take some more on.

You need to add to your list: Downsizing due to ailing health/mobility etc. I suspect this is going to become a large driver of houses coming onto the market in the next decade or so as the early baby boomers move to old folks homes. You only need to see the number of old folks homes being built to realise the shift is already underway.

Good point when I walk around my suburb I see many 3-4 bedroom home with elderly which will soon look like they will need to sell I wonder how many will flood market over next 5-10 years.

Yep, I walk down my street of roughly 100 houses and can count about 30 that will be freed up in the next 10 years or so. Behind me is an almost blind 75ish year old woman in a 3 bed house who barely makes it up the drive. Next to us is a 70-80 year old couple in a 4 bed house. I know of 2 that have sold already on our street and downsized, one still working but could barely make it onto the bus (about 75yo) - they sold for good prices. Once the flood hits, I doubt such high prices will be achieved.

I notice the word sales omitted?

Lower than 2017 and 2018 in first 8m for Auckland

Vested Interest may be.

I’ll check back later in the day to see how the various camps twist this to confirm their bias.

Ex Expat

Just putting my position on the table.

In anticipation of the QV results coming out in the next few days, while I see a firming in the Auckland market, as I have previously posted, I do not see the QV results necessarily reflecting this. This is due to the the basis of their data; not only are they over a three month period, but also the considerable time between offers being made and final settlement (whereas REINZ is unconditional). So I will be looking to REINZ data. :)

Housing listings and stock down, its logical that the 'average' prices will be up, especially in Auckland...

Auckland market is still sick.... more houses being built, population down....

The usual Spring Bounce, has turned to a Spring Roll

Population down?

Yup, Aucklands population down by77.5k on June 2018 initially estimated population

So the rate of population rise is less than someone somewhere projected and you say Auckland's "population down". When the reality is that population growth has been strong and the number of Auckland residents it at an all time high.

happy for you to live in your bubble, when you chose to ignore stats that indicate numbers are lower than initially indicated...

You didn't say that Auckland's population growth is lower than initially predicted. You just said "population down", which is rubbish.

He/she doesn't understand the difference. Last week when Interest reported that Chinese house price growth was slowing, DGM also concluded that house prices are going down

Unbelievable

I'm not 100% on this as I only got up to speed on it last night but in effect, the housing shortfall calculations are based on population estimates that from 2013 to 2018 overestimated the Auckland area by 77,400. Interestingly the adjustment in population results in Auckland needing 26,000 fewer houses. That is a considerable drop.

That's good news. You'll acknowledge though that the claim Auckland's population is down is incorrect?

I can read through his words and understand what he means. He means Aucklands population estimate has been revised down substantially.

You think that saying "population down" means "Auckland's population estimate has been revised down substantially"?

Auckland's population was predicted to grow, and it did, but the rate of growth was slower than expected. Only someone with a tenuous grasp on reality or the English language would think this means Auckland's population is down, or take "population down" to mean the same thing as "estimated population growth down".

When you start to attack someone's English the argument is lost. I know what he means because he made some half-garbed statement yesterday and it caused me to hunt around. After a bit, I found the Stats NZ update; Auckland population estimate down 77,400. That's a non-trivial change and while I don't like his stunted statements, im grateful to have it pointed out to me.

Just give it up.

Anyone with half a brain can understand his point.

The latest Auckland house price index is up year on year

Not unless -0.8% has magically become UP...

Anyone with half a brain could understand that by “house price index is up year on year” I actually meant that someone predicted that the house price index would’ve dropped by more, so the HPI is up in comparison to the original prediction. Duh.

It's like saying once a teenager finishes their growth spurt they start shrinking.

I edited my comment to include that analogy only to find you beat me too it.

It's not, he's referring to the shortfall estimates which are significantly impacted by a population revision.

He didn't refer to the shortfall in estimates, or even hint at it. He simply said "population down".

You sound like a baby that needs to be spoon fed...

@DueDiligence Well, now you know what he means so the confusion has been cleared up.

Now I know what he means, but the confusion on his part persists as he still seems to think that Auckland's "population is down" and/or that this is a valid way of stating that the growth rate was lower than anticipated.

Jesus.

You sound like someone desperately invested in this ponzi scheme.

Winner winner, chicken dinner!

Buyer’s market is slipping away in front of your eyes sunshine, best hurry up.

And on an LVR basis I’m confident you’ll be more heavily invested in this Ponzi scheme than me if you finally follow through on that pre-approval.

Ah, back to your stalking behaviour. something about leopards and spots.

And we are in no rush, house prices going sideways, cheap rent in a good location, deposit growing at a healthy pace, interest rates dropping..

guess you don't understand the meaning of DROPPED

from your comments we know how much of a scholar you're..

words from stats nz.. "were revised down with the largest revisions to Auckland (-77,400)" ... revised down, is a DROP

Hate to break it to you mate, but you are flat wrong on this one.

If someone says "the estimate was an increase of 100,000, then we had to revise it down by 50,000", that still means an increase of 50,000"

Auckland's population is growing, its just growing less than originally thought. Still growth though.

To reiterate; 'revised down' absolutely does not, under no reasonable interpretation, equate a drop.

I hate to break it to you mate.. There are many ways to skin a cat..

"the estimate was an increase of 100,000, then we had to revise it down by 50,000", ..that still means an increase of 50,000 or a drop of 50,000 from the 100,000 that EVERYONE built their model on housing shortage on!!!

What does it mean for a housing market that's potentially reactive to population numbers? It's like booking a table for 100 people at a restaurant, and only having 50 people turn up.

Dgm

This is annual, YOY, spring on spring.

To make it clear - this spring's results are better than last year spring's.

Annual, YOY, is not comparing current results with winter results.

Pretty simple to understand.

Glad you understand that, hence I highlighted the fact that volumes are down

No Dgm

You comment "The usual spring bounce"

When one compares one spring with another and there is a difference, one can't brush it off as simply as "The usual spring bounce". :)

What's better?

Across the country asking prices are up 0.2% YoY

Volumes are much lower YoY

If you're a RE agent volumes down is worse

If you're a buyer or seller flat prices is all the same

The correlation or more accurately causation you describe of lower volumes = higher prices would be different to most historical trends. Lower stock and hence sales volumes typically put downward pressure on prices.

Except he/she doesn't say lower volumes = higher prices but less stock for sale = higher prices which is correct if you assume the number of buyers is about the same

Well into spring and very low interest rates. Is this the best that the property market can do?

The Great NZ Stagnation has arrived.

We shall see Fritz, I believe fewer vendors for the same amount of buyers (combined with low interest rates and upcoming lower LVR?) will lead to higher prices by March 2020

Maybe. Won't need to increase much to get to all time highs.

As you know I have predicted the market to flatten out over the next 1-2 years. This could mean small gains (2-3%) or small drops (-2 or -3%).

I've just looked out the window and seen the weather has changed (again!). And I have just read your comment and found your predictions have changed (again!) At least theyve been revised upwards this time.

Do you ever update your predictions based on new evidence? If not, why not?

Yes, but I am not a cynical person prone to making wild statements and then retracting them when the obvious is staring back.

Stop misrepresenting the positions of people. It would be good if the editors took misrepresentations seriously.

I have said several times over at least 2 months that the market is likely to be flat for the next 1-2 years. I have said that flat could be somewhere between -3% and + 3%. Aligned with that I said I think there will be a recession in 2021 or 2022, which will result in price falls which could be very significant.

Is that clear now?

"same amount (number" of buyers?"

Pardon?

Sales were higher in September than last September.

One month. In Jan-Aug period they were lower.

October 18 was mania of off-loading pre OBB

So, October 19 will revert to (2017) figure.

November will be same.

I repeat, sales in last 32m have been LOWER than they were in 2009-11 for same 32m period.

Prices will go down, after February reveals no Spring or Summer "bounce"

By the way, "bounce" in my definition means "higher than year previous" not higher than winter.

We will find out by April 2020 (for the March figures)

- new all time high prices as I predicted

or

- 25% drop in prices as you predicted

His 25% drop prediction is for the end of 2021. Are you so desperate to win the prediction competition that you're trying to put words in his mouth?

Ok then, he said just above,"prices will go down after February"

One of us will be right, one of us will be wrong, we shall see in April (for the March figures)

Why are you pretending you can't read? He said: "Prices will go down, after February reveals no Spring or Summer bounce".

He didn't say "prices will go down 25% by March".

He's not pretending. As I say up above, full time property investors are not the most intellectually gifted people.

They may have commercial savvy, but they certainly - in general - lack intelligence.

Fritz, think what you want about professional landlords!

Reality is that a thick financially wealthy landlord will have a far better lifestyle than you Fritz, that haven’t taken the opportunities available and have ended up financially unsuccessful!

CourtJester, I didn't know you were Mike Kirk's mum, is he not old enough to speak for himself?

Quoting you: "Prices will go down, after February reveals no Spring or Summer bounce". Indeed I admit understanding that prices will go down after February. Since you think I cannot read, would you mind explaining to me from what date MK predicts prices to fall?

"As I say up above, full time property investors are not the most intellectually gifted people.

They may have commercial savvy, but they certainly - in general - lack intelligence."

Wow you really know how to pull out the flattery Fritz. So dont get upset the next time someone insults you, or start crying foul like what I have witnessed you do. It's funny how you seem to be a property expert without ANY experience and without study - unless you count study to be an ENGRISH teacher

The beginning of the move towards all time record prices in March 2020 (which will be reported in April)

Today's column by Gregg adds to the weight of evidence that the housing market is beginning to move again - and notably in Auckland.

Indications are that we may see significant increases in average/median prices over coming months.

TTP

News, Data, So Called Experts - One day will come up with how the market is Up and the very next day, how it is Down. One can argue if the housing market may or may not go down (Everyone needs something to talk about and run their show/ business)But what is defenite is that it is not going up soon despite low interest ( Interest rate being so low in itself is an indicator of state of ecenomy).

Low interest may slow the process of correction but cannot avoid it specially in Auckland for how many on NZ wages afford a million or 1.5 million house. Also many houses that are being sold for a million just because Auckland council shot the RV by 50% or 60% worth the price tag. Market was so hot that it will be a while before sense prevails and buyers thinks logically in their best interest without the fear that is been created of losing out.

Property market stirring eh Westpac. Ha.

Funny the decline in listings is just what I am forecasting sales to fall by year on year in Oct: 17%

Mikekirk

Your postings have been claiming a collapse in market prices.

The above suggests that you don't seem to grasp a basic market 101 facts. Sorry to have to spell it out but clearly needed.

- An abundance or increasing number of properties - a buyers market. Bad news for sellers as greater pressure to get a sale so downward pressure on prices.

- A shortage or decreasing number of properties - a sellers market. Bad news for buyers as greater pressure to get a buy so upward pressure on prices.

Keep doing that historic analysis of data and a year after a turn in the market you will be able to identify the turn. :)

Partly right, but not that simple.

Quantities aren't exogenous. Likewise, neither are prices.

Owners, being risk averse, react to market conditions. If the market is soft (i.e. they cannot list/market their property for more than they paid for it), their propensity to list is reduced.

In other words, you assume that causality flows from quantity to prices when in fact the two are endogenous.

So, essentially, you're both as wrong as each other.

Exactly.

Risk aversion and confidence are of course directly related.

Confidence is not rising. Quite the opposite.

Owner are with-holding and buyers are waiting for prices to fall further.

Deflationary mindset is setting in and this is why RBNZ is taking drastic measures.

Exactly.

Re the Auckland property market

In 2015/ 2016, recall the rapid property price rises which then caused a fear of missing out (FOMO) which then attracted more active buyers to the market? Recall the frenzied bidding at auctions? Property price expectations were of higher prices due to the recent pattern of price changes, so active buyers were willing and able to pay.

Now that there has been flat / slightly falling prices in Auckland since March 2017 (so for 30 months), this has influenced the future price expectations of many. As a result property price expectations for more people are now flat or down. As a result, many potential buyers are taking a wait and see and not actively putting in offers to buy at current prices. Those who have expectations of lower prices are just sitting on the sidelines waiting for opportunities. That has resulted in fewer active buyers in the market (despite the fact that there is continued population growth and an underlying shortage of housing in Auckland as estimated by the Auckland Council economist). Buyers are less willing to pay current prices, hence the decline in active buyers. Some active buyers are making low ball offers, but these are either not being passed on by the real estate agent to the vendor, or simply being rejected by the vendor (as the vendor has higher price expectations).

A relative has been trying to sell their house for 10 months They have listed the property with different real estate agents. Yet their asking price is unchanged and they still have expectations based on price levels of 2017. Since they can hold on, they can wait for acceptable offers. There will be other vendors out there who may be unable to wait or hold on.

Forecast, as I have said ad nauseam (yet continue to be misquoted) is for a $670k median in Auckland by end of 2021. NOT a crash.

That is 25% lower than the peak median of $900k of March 2017.

Now that is out of the way: a buyers market is where more people are buying I would have thought (logically)

They are not. And not surprising when 20% fewer listings to buy.

ACTUAL buying is different to potential for buying, just as RE NZ CEO saying lots of interest online from buyers , is not actual buying.

Confidence is crux and that is in decline.

Speak to people on doorsteps and examine what are constituent elements of listings and you will see that there is a shortage of what people want to buy and where they want it.

Also, a lot fewer sections listed than a year ago, for obvious reasons.

Also, it is not a buyers market if fewer people can afford to buy them: hence 34% lower sale snow in Auckland than in 2013: with higher stock by 6.5%

So, lecture over. Try again

" it is not a buyers market if fewer people can afford to buy them"

Just to clarify, so that you are understood correctly, and that readers are all on the same page, and to reduce the risk of miscommunication and misunderstanding here.

Most people define the phrase "buyers market" to indicate which party in the property transaction has more relative bargaining power.

The phrase is not used in reference to buyer affordability.

Mike, given you're a RE agent, I'm surprised by your claim that: "a buyers market is where more people are buying I would have thought (logically)".

A buyers market is a market in which there are more sellers than buyers, therefore giving more choice to the buyers, not a market "where more people are buying" as you claim

No quite Yvil

A buyers market is where the buyers have all the choice and time at their disposal and backed by fundamentals that encourage buying.

Almost all of these things are true at the moment except buying isn't increasing from the doldrums of the last 2 years because there are a couple of important elements missing... Affordability and credit availability (which unsurprisingly is restricted by affordability or risk).

In a true buyers market the opposite of a sellers market applies, where sellers are chopping prices and doing all the can to move the item for sale.

We are more at a stalemate at the moment, we have removed the buying segment that pushed the prices sky high with the FBB and the OCR is allowing sellers to hold and wait.

I suspect that when the new builds have to substantially discount to gain cash for the next project, mixed with job lossed from the coming recession then we may see competition to sell and a buyers market.

Thank you glc. And that is why I am expecting prices to drop more after Feb

Strange theglc, you agree and expand on my point, yet you start by "no quite Yvil", just say "agreed" and then expand

Kindly give a solid idea for us of what a "turn in the market" will mean so we can look out for the evidence.

I am interested in feedback on another indicator of the state of the market.

I have found that with a shift to a sellers market, one tends to get more letter box drops from agents seeking property listings. This tends to be for "more desirable" properties (read, properties likely to be in demand by buyers).

Are those living in Auckland finding this?

Be honest :)

Not seeing that. I live in Meadowbank, quite a few properties are for sale in surrounding streets, but no leaflets.

Not seeing any letterbox mail drops or door knocking by agents. Auckland Eastern Suburbs.

Some in Remuera, but they are a constant since I moved here about 5 years ago, so no real change.

Biggest impact on Auckland housing market in last 6 years: China money in and China money restricted.

This is what is beginning in their banking system:

https://www.zerohedge.com/markets/chinese-bank-verge-collapse-after-sud…

Yes exactly and that is a huge problem for NZ and in particular Auckland's housing market. Everyone here got so addicted to dodgy overseas money pouring in from China, and now that that money is gone, we're trying to make residents and FTB's make up the huge short fall to maintain prices by getting themselves in to massive amounts of debt that they can't hope to repay.

Also keep in mind that Hong Kong is also on the brink of recession since they are not willing to tolerate an oppressive Government. The HK people won and got their Government to withdraw controversial extradition bill after much protesting.

BBC How protests pushed Hong Kong to the recession brink. https://www.bbc.com/news/business-50204696

I believe HK was officially in recession as of last night. At least that’s what I seem to remember reading on Bloomberg.

Mikekirk

You seem besotted with the notion of the importance of Chinese involvement in the Auckland market.

The "biggest impact on Auckland housing market . . Chinese money". Where have you been?

The biggest impact on the Auckland housing market have been the low NZ mortgage rates and in more recent years as far as Auckland is concerned, issues related to both affordability and future of the market. As for low mortgage rates - don't look to Chinese money but rather RBNZ and OCR.

Note that RBNZ introduced LVRs not to control Chinese money but rather every NZder and his dog speculating by going out and buying property.

Like Auckland, prices have risen throughout most of New Zealand as a result of the low mortgage rates. Those Chinese property investors wouldn't know where Gisborne, Palmerston North and even Hokitika were, let alone buying property there to influence those markets.

From memory, some official stats indicated that the number of overseas sales was estimated to be 3% and then, while many, the Chinese were less than 50% of total foreign buyers.

You are hanging onto a modern-day version of "reds under the bed".

Cheers

Printer, we were trying to buy a house on the shore 5-6 years ago and pretty much all of the auctions we went to had an 80/20 split, and that 20%, they were white fullas like me.

I'll give you absolutely zero guesses who ended up buying most of those houses...

That tap is obviously (and thankfully) turned off now but to say that Chinese money has had no influence on the Auckland market sounds like it's coming from someone who hasn't tired to buy a house in auckland in the last 5-6 years.

Interest rates have dropped in those years but the initial damage was done by that massive influx of money and punters selling now are still clinging to the dream of the last few years.

Lets see where we are in another 2 years. (i've no idea but it'll be an interesting ride)

Hi muzzled

So you checked all their residency status are absolutely sure that they weren’t “us”.

Unless of course to be a NZder one needs to be a “white fulla” as you note.

For those that have argued prejudice doesn’t exist on this site, then note muzzled’s comment.

Get real! We know where that money come from over the last few years, so go pull the other one printer8. That dodgy money has GONE!!!!!!!!!!!!!!!!!!! And I agree with other commenters here, that it's a good thing that money tap has now been turned off. Now we can get back to building real our economies instead of allow our cost of living to be pushed sky high. Article: China's Home Invasion https://www.aljazeera.com/programmes/101east/2015/01/china-home-invasio…

So CJ1099

You know where all that money really came from.

Care to state a reputable source to back that up or it becomes just another wild assumption.

If you stand by your comment and want credibility, back it up with the data source.

Hardly an assumption, surprised this is in any way news to you? Perhaps you should watch this NZ documentary from an award winning documentary maker Bryan Bruce and read more articles on the subject to educate yourself, I've got heaps more evidence on the subject if you want more links. Documentary: Who Owns New Zealand Now? https://www.youtube.com/watch?v=HzSAmOQuyjU

Wasn't actually trying to be prejudiced at all P8, but your question about residency status is as ridiculous as they come.

Maybe I should have added in that a lot of those buyers had interpreters.

Does that mean they're not residents, no it doesn't, but...

Cheers muzzled

Your comment was prejudice. If you care to look up the definition of prejudice you will note that it means having a preconceived idea or view about a group or particular person.

In the context of the discussion regarding foreign buyers you made the assumption that the 80% of Asian buyers as you claim

That assumption and statement is prejudice.

As to checking their residency status; well you were making the statement and you need to ensure that such comments are factual or subject to scrutiny.

Out of this you seemed to have reflected on your preconceived ideas and the statements you make.

I agree that just because “they” have an interpreter that doesn’t mean that they are necessarily a foreign buyer. A legimate resident for who English is a second language could well want and wish to have an interpreter in such a stressful situation.

Cheers

muzled, say if you are a white guy who can speak pretty good Mandarin. Go to to an auction in China, I can bet you will need an interpreter!

haha, thanks for the explanation P8, I feel so much more enlightened now buddy.

None of which takes away from the fact that you seem to think that 'Chinese' money had nothing to do with changing the landscape in the akl market which you seem to have skewed the argument away from quite nicely. (lets replace Chinese money with foreign money and your argument is dead in the water). You prob don't want to go down that track though as that would get back to your original assertions that it's low interest rates that have driven the market here through the stratosphere.

Do you have any thoughts on the market in Vancouver for example? Or is that just low interest rates as well?

What about China clamping down on getting money out of the country?

Cheers muzzle

Clearly there have been issues with money laundering and activity of foreign buyers. I haven’t seen any published material with the detail of what has been happening but the fallout has been significant. Buying and selling a property, or opening a bank account, has just got a further layer of bureaucracy and double that for a trust. A trust taking a mortgage has become horrendous. There is a growing movement that those with family trusts are winding them up.

If the disappearance of 'hot' Chinese money hasn't flattened the market in Auckland, then what has?

Interest rates have been cut and cut and cut, but the market has not resurrected.

So why hasn't it kicked back in to life?

The only meaningful policy changes have been the foreign buyer ban and the extension of the bright line test. This suggests that one or both of these policies might have had some effect.

And that would suggest that foreign buyers were much higher than 3%. How much higher, I don't know, but I have heard estimations of 10-20% at the peak of the boom.

In 2015-2017 I was working as an English language teacher for adults, with >50% Chinese students. Middle/upper class migrants. All were mad keen on buying property, most already had bought both property for themselves and investment properties. They openly discussed with me the means used to 'smuggle' money in despite capital restrictions etc.

Were they nice people? Yes. Smart and funny.

Were they citizens and permanent residents with every right to buy property? Yes.

But where did their money come from? It came from China. It's money they've made in China, or borrowed from Chinese banks, or from relatives and friends who wanted 'in' to those sweet sweet capital gains.

So just looking at what percentage of sales went to foreign buyers vastly understates what was really happening in Auckland, because economically it's not just about where the person was from, it's about where their money was from.

Printer, we were trying to buy a house on the shore 5-6 years ago and pretty much all of the auctions we went to had an 80/20 split, and that 20%, they were white fullas like me.

I'll give you absolutely zero guesses who ended up buying most of those houses...

That tap is obviously (and thankfully) turned off now but to say that Chinese money has had no influence on the Auckland market sounds like it's coming from someone who hasn't tired to buy a house in auckland in the last 5-6 years.

Interest rates have dropped in those years but the initial damage was done by that massive influx of money and punters selling now are still clinging to the dream of the last few years.

Lets see where we are in another 2 years. (i've no idea but it'll be an interesting ride)

You were obviously in the Land of the Wrong White Crowd!

:) I do wish we'd bought 18 months earlier...

muzuled you are absolutely correct.

Now with foreign speculative money/money laundering gone - will be interesting to see how many can buy million dollar ot 1.5 million houses on NZ wages.

Low interest rates may slow the process but ultimately house price have to match with what they are worth.

Interesting time ahead.

Yichuan Bank in China is on the VERGE OF COLLAPSE!

This is the 4th Chinese bank that has been in MAJOR TROUBLE since May 2019!

The Chinese economy is more fragile than most assume. It's just been propped up repeatedly, a bit like Japan was in the late 80s / early 90s before it all came crashing down.

I don't think communism is immune to financial crisis.

Speculative interest gone, returning to normal house sales volumes of people needing to move for practical reasons. Price don't enter into it, thats a separate argument when prices are still detached from reality.

Yes, price doesn't really enter into it for existing home owners, buying and selling in the same market is effectively house swapping with a bit of change here or there. Prices could be double what they are, and it'll be business as usual.

It's when there's an imbalance of those trying to exit the market vs trying to enter the market that creates an issue.

Yawn. Listings down as people wont sell without gain upside, and low rates are making it easy to hold. Buyer yields are out of wack with price, and there is no spec gain on the horizon. So why buy...?

All it's going to take is one large bank somewhere to crap itself and the king tide of cheap debt washing the world will recede. Then we will see who is naked. How are those banks in China and Germany looking?

Meanwhile the usual suspect are back printing cash to protect the asset ponzi. Extend and pretend.

Well said. One comment that says what 78 others were trying to .... even if they didn’t know it.

This is probably the best comment I've ever read on this site. Sadly most of the other comments here always devolve immediately into who's predicted what, why they are wrong and X is right and personal attacks. Almost all of them are dominated by the same usual suspects and anyone that disagrees with their rhetoric is either a "DGM" or a "Spruiker".

*yawn*,

Asking prices, which doesn't mean diddly when most of the lower priced listings on realestate.co.nz are by negotiation or Auction.

And of course it misses what is currently a huge factor in the auckland housing market (and maybe elsewhere too), all the housing NZ and community housing provider builds that never get listed, but are being built and taking people out of the hunt for mostly rental houses, which in turn destroys demand from investors for more rentals. Hence the recent slowdown in rental price growth.

Month to month 5 regions with upsides, 10 with downsides with the remaining 4 regions stagnant seem pretty bearish to me with a further risk ofdownward trend further into the year.

Year on year the housing stock on market fell 13.1% but the asking price ironically fell 17.1%. This divorce in relationship suggest that there is little real demand for the current housing offered in the market,this I suspect was likely due to the gap in price expectations between vendors and purchasers. In addition, if the number of housing consent remains strong like the 30.8% we'd seen in September for the same kind of housing stock, I think we're simply engineering ourselves a hard landing.

The buy and hold 'strategy' for property investment is precarious at the moment as it is highly dependent on flexibility of the banks, taxation rules, rent income and interest rates which are all subject to factors beyond any individual's influence or forecast ability.

I cannot see any kind upside in the property market in general at the moment.

I seen to recall record numbers of completion certs being issued. Where be all these new houses and flats ? If they aren't listed are they being held back ?

Biggest building efforts round our way are housing NZ and community housing providers, builds that never hit the open market.

Probably cheaper for govt to continue to intensify hnz land (aka Panmure) than continue to pay loads of accommodation supplement year on year to landlords/banks.

yah but stats show they are only about 5-10% of the new builds occurring in Auckland at the moment.

It's an excellent question Glitzy.

Apart from the minority which are Housing NZ, I assume there are lots of very small townhouse / house developments spread all over Auckland region, plus a few chunky developments eg. Hobsonville, Auranga, Milldale where you will regularly see 10 -20 homes for sale.

There will be some retirement units.

Then there will be new build houses that are being built by owners of land, rather than built to sell on the open market.

Then as you say some might be being held back.

But yes it does seem that there aren't as many on the market as the building stats would suggest.

One person says I am wrong to define a buyers market way I did ( people buying more not fewer)

Person says in fact it is when are more sellers than buyers. Depends a little on time frame selected. Also if you look at what is actually being sold. Listings in Auckland in last year are down 20% and sales 11% for residential only. However apartment sales are down 26% in last year and apartments OTM are only down 10%. Also how can you define a buyer? Perhaps what is meant is someone looking to buy. That is entirely different as any open home will demonstrate! Yes buyers have more to choose from but what are they being offered? And at what price. Overpriced shoebox shacks for instance does not look like a good buyer choice to me

There are still opportunities out there for those that want to pursue them and become financially independent.

Purchased a near new property today which will give a return of over 6% and undervalued

Moan and groan as much as you want, but the doom and gloom merchants should start doing the business or you will be left further behind.

"and become financially independent".... you mean with a crippling 30 year mortgage?

Congrats for your new purchase.

You really show your lack of financial acumen once again The Boy. You say you bought something yesterday undervalued. I beg to differ. If it was undervalued how come some other sucker did not buy this house? You obviously had very little or no competition because after all it is poor old Christchurch which has performed badly forever. Earthquakes, shocking weather, poor work and business opportunities, isolated and hence it has a small population. You set the market price yesterday for future registered valuations. You bought at current market price. You need to read some basic economic and financial material and get honest with yourself.

Indeed, I said a buyer's market is not defined by more buyers buying but rather by more sellers selling as this gives more choices to the buyers and pushes prices down as a result. I stand by this.

Spruikers close your ears now!!!!

I am reading the latest Verve magazine.

Sylvia Lund of 'Just Rentals' one of the main rental agencies in the eastern suburbs says on page 151:

'Not only is there gloomy weather, but there is gloom in the rental market too. Not much is happening. Properties are slow to rent and Trade Me enquiries are down'.

Spin that one spruikers!!!!!@!!

What's with the "spruiker" obsession? It states the same as in the article above, which is low volumes which does not equate to low prices

Sentiment, Yvil, sentiment. You know that thing that has a big influence on markets. Even a rental agency calls the market 'gloomy.' Because...it is.

Gosh why don't people on this site not understand RE, it's unbelievable.

A RE agent makes money through sales (same applies to a rental agent with tenants). So yes if there are FEW SALES or Rentals, for them it's bad. This does NOT mean that the values are down. How can so many on this site not understand this basic principle

Sales are down because demand is down. Simple.

A property owner can pull their house from the market or not list it. With minimal impact.

But for a landlord every week without a tenant is damaging. Which means there is more likelihood that rents will be reduced, compared to prices.

Pretty simple.

Yes it is simple yet you don't understand it Fritz. Your post above shows that very clearly, you start writing about sales then you move on to rents and then prices. You very clearly don't understand they are different components and you get them all mixed up. For example read the article above, why are sales down? Not because there is less demand as you say, com'on read the article it's plain to see… Do you get it? Yes it's because there are less listings and less stock, that means less sellers.

Maybe it's better you post on items you understand, so you can add value to the forum

You know NOTHING about markets. Zilch.

You got lucky with timing that's all.

Anyone who knows markets knows that in times of low demand, supply is lowered. That is one of the fundamentals of a market.

I am not going to ever bother responding to you again.

You are clearly dumb or deluded. Or both.

I hope for your sake your reliance on your portfolio doesn't get destroyed by a market correction.

Merry xmas.

Ouch, it sounds like I hit a very fragile nerve. It's OK if you don't understand RE well, just refrain from making comments that show everyone your lack of understanding and focus on the "markets" you say you know well. I've made millions through RE over the years and I don't need to work anymore (although I do), yes and sorry, it's "showoffey", but I just state that in reply to you alluding I don't know the markets.

The spruiker obsession? Well spruiker is what several of your mates are. You guys call us DGMs, we call you guys spruikers. Fair enough.

I don't have "mates" on Interest, I come here for the business value (the articles anyway). My "mates" are real people that I see face to face and I can have a drink with in real life. But yes, I can see how some here see this forum as nothing more than "everyone can share their opinions, their 2 cents worth" even if one has no expertise or experience in the field discussed. Yes for some, I presume, this forum is about getting as many upticks from their "mates". Easiest way to achieve this is, of course, by sarcastically criticising everything and everyone. Not my thing though, I prefer my mates to be real and in in front of me

One thing to note Fritz, is that if you get the better of Yvil, he'll report you to interest.co. there is a good ole name for such folks.. mamma's boy...

Houses Overpriced… LOL

The article goes on 'We have lowered rents and put new photos on Trade Me but, as I have said before, there is no sense of urgency'.

You shouldn't be too worried surely Yvil? I am sure as a seasoned investor you are in it for the long haul. So a period of stagnation shouldn't worry you.

Personally in ChCh We are not finding that at all.

What I will say is that the property rental market is just not AucklAnd.

Secondly, private fulltime professional property investors tend to be far better at finding good tenants than paid property managers as they have more time to concentrate on the business.

Good for you The Man. I can only speak for Auckland, and it's look pretty flat, and a bit vulnerable.

Good on you if you are still making buys in ChCh that provide good yield. Very rare to get 6% in Orcland these days.

Fritz, I do not consider property that won’t return us at least 6% as it gives sufficient margin to make it worthwhile.

This is my point that I continually try to make on Interest.co.

This is a site to discuss things I regard to making financial decisions rather than a pro property against those that are negative towards property.

Everyone knows that Auckland provides very poor rental yields generally unless you have owned the properties for a long time.

We achieve absolutely nothing by debating the same thing in Regards to pro and negative whenever there is a topic in regards to property.

Everyone has a choice as to where they invest at the end of the day.

Thanks The Man. Good to see that you agree that Auckland property investment (buying today) is a poor one. Agree that some people have done well by buying in the past when prices were lower and yields better.

Maybe a good time to list before everyone else decides to pull the trigger and more competition lists.

I think it is dangerous to wait because the market may just drift along or fall of a cliff and people will be kicking themselves for thinking this market will rise like has in the past if they just wait a few months.

I agree. It seems like vendors might be holding in order to not take a lower price, or even to manage supply. But how much stock is building up to be released? What impact will a flood of supply have on prices? And what kind of events could trigger them to be listed?

This is the key question. I believe there are a lot of investors with Auckland properties who are effectively losing money on their investment.

But what could prompt them to sell?

There aren't great gains to be had elsewhere.

I believe events in China will be crucial. The question is, would economic problems there lead investors to repatriate cash to China (because they need it urgently there), or to cling even more tightly to their relatively secure investment in NZ? I honestly don't know. (And, in Auckland, the 3% figure is absolutely a delusional fraud...)

Very good question. I guess if it got bad enough there they will be more likely to repatriate. But it would have to get pretty bad for that to happen.

MW: "But how much stock is building up to be released?"

You may be guessing about new builds, which is nothing but speculation, the answer to your question we do know is: Today stock is DOWN 14.7% in Auckland, not up. Read the article

And yet prices are still going sideways.. demand must be dropping in unison with stock on the market if you want to stick to a supply and demand narrative.

if you are more savvy, you will notice that there are other forms/media that enable properties to be listed.. so properties are up for sale, demand is dropping and hence prices for now is stagnant, just marking time

Or would they keep it here in a nice safe offshore holding where the chinese Govt can't easily grab it? If they were planning on fleeing the country I think it'd be safer over here.

"investors with Auckland properties who are effectively losing money on their investment"

Under Minsky's Financial Instability Hypothesis, this would meet the criteria of "ponzi" financing. Refer https://www.mauldineconomics.com/editorial/the-market-is-headed-for-a-m…

"I believe there are a lot of investors with Auckland properties who are effectively losing money on their investment."

This is the reason, that property prices in Auckland have become increasingly vulnerable - there are a LOT of investors who are losing money. If there were only a few, then the vulnerability to Auckland property prices would much lower. If there are a lot of investors who are losing money in Auckland property, there is a higher chance of causing an imbalance in the Auckland property market. Does anyone have any statistics on this?

"But what could prompt them to sell?"

If these property investors are highly leveraged, how are these loss making / cashflow negative property investors financing the cash shortfall on their property?

They are typically financing it from household incomes. So

1) businessman - cashflow stress on their business could cause them to sell.

Here is an example of a businessman who sold some of his investment properties. He had ownership in 9 properties - his own home and 8 investment properties.

https://i.stuff.co.nz/business/property/116378021/ecohouse-businesses-i…

2) employees - loss of income could cause them to sell, so their employment status is important.

Will any of the employees in the above bankrupted business a) own their own home b) be highly leveraged c) be unable to find a new job in reasonable time d) have sufficient financial resources to maintain mortgage payments before being able to find a job or will they be forced to sell?

I heard about a guy who got made redundant during the GFC in 2009, unable to find a job and was unable to continue debt repayments. He ended up selling his home and 2 investment properties.

If the NZ economy goes into recession, how many businesses and employees will be affected?

Also recently heard of a property investor who sold 15 properties due to the expected high cost of meeting the Healthy Homes Standards.

Inability to service debt. Job loss. Rate rise etc.

All is well, people have employment = income, there's no hardship, lots if work in the pipeline. Enjoy your weekend, life is good. :-)

"people have employment = income, there's no hardship, lots if work in the pipeline."

Yes, agree with you that that is the current situation.

That same statement above could have been made in 2007. Then look what happened ....

The real question is what are the chances of

1) status quo continuing for the next 3-5 years.

2) improved economic conditions for the next 3-5 years

3) deterioration in economic conditions for the next 3-5 years.

And the magnitude of these outcomes.

There are leading indicators to watch which can provide a potential guide. Some commenters on here can see them, others miss them.

The useful value in the weather reporter is not the information provided in reporting yesterday's weather, or the weather conditions right now. The most useful information for most people is in their future forecast.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.