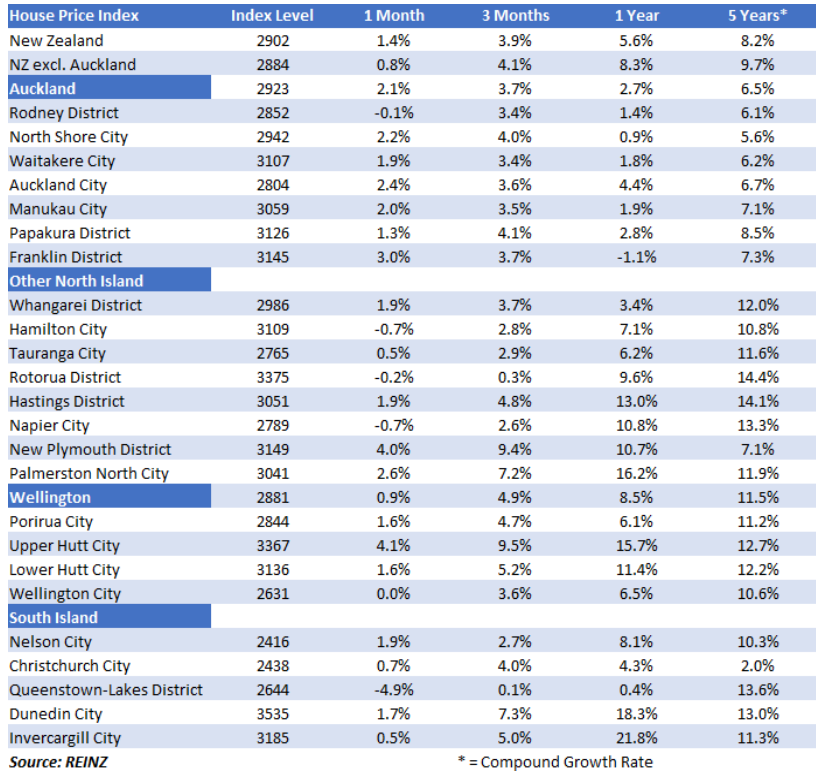

House prices are on the rise again in Auckland but appear to be flattening out in most of the rest of the country, according to the Real Estate Institute of New Zealand's latest House Price Index (HPI).

The HPI tracks the movement in prices around the country and also allows for changes in the mix of property types sold each month when calculating price movements, so is seen as a more accurate reflection of price movements than shifts in median or average prices.

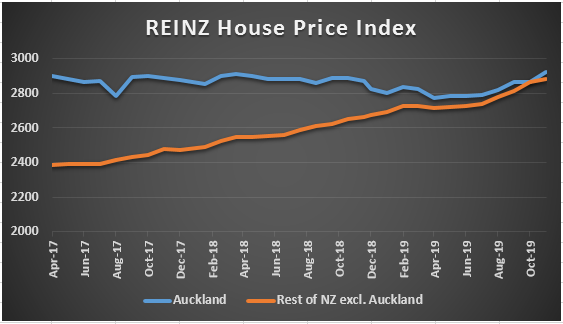

One of the most significant trends in the November HPI was a turnaround in the Auckland market, which went from having a 0.1% monthly decline in prices in October to a 2.1% gain in November.

Within the Auckland region, price gains were recorded for all districts except Rodney which posted a 0.1% decline, whereas in October, North Shore, Waitakere, Auckland Central, and Papakura all posted monthly declines.

On an annual basis, prices in Auckland were 2.7% higher in November than they were a year earlier.

That suggests upward price movement in the Auckland market after a prolonged period when prices have been flat at best.

But around the rest of the country it's a different story.

For the rest of New Zealand excluding Auckland, prices are still rising at a faster rate than they are in Auckland, but the rate of price growth is slowing, suggesting prices in many regions are starting to flatten out.

According to the HPI, the rate of price growth in November compared to October was lower in 11 of the 17 districts outside of Auckland, which suggests slowing growth even though prices are still rising in most centres (see table below).

The biggest turnaround has been in Queenstown-Lakes, which went from showing 4% monthly growth in prices in October to a 4.9% decline in November, although price movements in the district can be volatile because of its relatively small size.

In the Wellington region monthly price growth declined form 2.6% in October to 0.9% in November and in Christchurch it declined from 2.2% to 0.7%.

Even in Dunedin, which has had some of the strongest price growth in the country over the last year or so, the monthly price growth declined from 2.7% in October to 1.7% in November.

The comment stream on this story is now closed.

REINZ House Price Index

101 Comments

"On an annual basis, prices in Auckland were 2.1% higher in November than they were a year earlier."

The table says 2.7%.

Auckland leads and the rest of NZ follows........

This pattern is not new - but it is disconcerting for first home buyers in Auckland.

TTP

What the disconcerting part? The bit about Auckland property prices having risen a compounded 6.5% in the last 5 years?! Shouldn't we be at least 65% by now if we're going to get the traditional doubling every 7 years, or maybe it's 10? But at the current rate, it's going to take another 40 odd years to get the next doubling!

Well think of it this way, at least property price growth has significantly slowed down and Auckland is still below the 2017 peak price. Even if our house prices start to double every 10 years that's still too fast to for wages growth, which for most people has remained frozen for quite some time.

If we see a property price double in less then 3 years that should send up a "big red flag" and we know were back to good old money laundering.

Article: North & South: Taking us to the cleaners. https://www.noted.co.nz/money/money-property/taking-us-to-the-cleaners

And at a ~1% p.a. Auckland property price rise over the longer term ( the 6.5.% Compounded over 5 years) then stability/affordability has a shot at being reinstated - again, over the longer term. I don't have an issue with that. But that should have been done in 2012 and just look at all the debt that has been assumed since then, and how pointless it has been at the community level ( I know, we are where we are! But, hey, "Better now than never!")).

I think you're misunderstanding what the compounding means. You have it backwards, I'm pretty sure. It went up so much between 2014 and 2017 that, on average, it went up 6.5% per year over the last 5 years.

Correct, so at that rate it will take 11 years to double, very close to the long tem average

The doubling in house price on average over a 7-10 year period is accurate however it’s over the long term and it’s not linear. It may very well take 15+ years for the first 100% uplift, then the compounding effect takes hold and it reduces. I have a rental I bought in the 90s that is doubling every 3 years on the original purchase price at the moment. That will eventually fall to doubling annually at some point. That’s the inflation compounding affect. It pays to understand it.

.

OK pedant, it increases by 100% of the original purchase price. And while we’re on pedantry it’s “that is a weird definition”

.

I was using the vernacular of the earlier poster. You come across as quite a sad and petty person. Life passed you by?

bw - This what I see, we are at the starting point of the upswing/cycle in Auckland, this is the 6th cycle I have witnessed in Auckland in my adult life. Many on here think that talks of cycles is madness, I have seen and learned to trust these cycles and planned property transactions around them.

The current pattern is 9 years, 5 years up,1 year limbo, 3 years flat to falling, have a look at any chart for Auckland house price movements over the last 40-50 years and it is quite obvious.

The doubling is not quite correct, generally the gain is more in the 70-90 % range.

My opinion looking forward is the gain this cycle will be less for a number of reasons that would bore everyone.

My pick is 40-70% but history can only confirm in the future.

Being aware of such cycles at play can greatly assist anyone interested, and help build a comfortable lifestyle.

Many complain on here about robbing others of the ability of home ownership but the fact remains we don't make the rules but understanding the big picture allows us to confidently participate in the market.

Not everyone will own a house thats always been the case for multiple reasons, so why not aim to be the Landlord and not the tenant.

Seasons greetings.

Great post, Shoreman.

Really good to read such a well-informed/considered commentary.

TTP

Brock Lovett: (In reference to the captain of the Titanic)

"Twenty six years of experience working against him. He figures anything big enough to sink the ship they're gonna see in time to turn. The ship's too big with too small a rudder. It doesn't corner worth a damn. Everything he knows is wrong."

Global debt is the ship that is too big.

Interest rate maneuverability is the rudder that is too small.

The first and last sentences apply to you.

Nasem Taleb has put a few books out around these lines - like Foold by Randomness and the Black Swan.

I find it hilarious that people seem to fully buy into the concept that past performance almost 100% predicts future outcomes!

Great post Shoreman. It's that simple

I would certainly not count on another doubling from the previous peak in the next 5 years. Sure, that cycle you stated has been fairly usual over decades but you have to take account of the current situation, and exceptions which happen when credit and price-to-income get as out of whack as they are now. ~$1.7-1.8m for average Auckand home price by 2024 would be pretty crazy stuff. In terms of cycles, check out Ray Dalio’s recent book on larger cycles, as well as the smaller ones. Every so often, the bigger cycle bites. I own NZ property, but I’m not expecting much more capital gain, if any, over the next 5 years.

House prices of $ 1.8 million for Orc Land in 2024 will be perfectly acceptable if average family incomes rise to $ 600 000 .... matching the long term trend line of house prices being 2 to 3 times household income...

Yep and then we'll be a banana republic with hyper inflation.

Shoreman - do you also sell snake oil?

IO - Why do you need to make such a comment ? If you don't follow or understand cycles move on. As with all things the results over time are the only thing that's relevant. In my case I have made 12 million dollars over 4 decades, how is your money machine coming along ? What were you going to do with the snake oil again ?

I make my comments for the same reason you make yours! You feel your opinion is truthful and worth sharing, and so do I. Happy with the theory of cycles - do you follow Ray Dalio? Short vs long cycles?

Great work on your returns. You've done very well and I'm sure the renting class of NZ admire your success. Congratulations.

I prefer to avoid snake oil, it irritates me terribly.

BW, the current growth rate of 6.5% takes 11 years to double prices, not 40. That's very close to long term averages

bw - regarding your comment on the future of the market based on 6.5% in last 5 years.

Your comment was not a very insightful one.

Clearly over the past five years we did not have a consistent market. Following a long historically unique boom, with a peak in March 2017, then followed by a period of falling prices and, only in the last three months some upswing.

To extrapolate the last five years out as likely to be consistent for the future short to medium term is being a little naive.

It is anybody's guess; but if you want a basis go by RBNZ comments that they would be comfortable of annual increases of 2 to 3% pa - and they have some control on the market. Are we likely to see a similar boom as we saw 2012-2017? Not likely as RBNZ - for economic stability purposes - don't want to see a similar boom as we have just witnessed and what is different is they now have the tool - LVRs - which they didn't have for much of the last boom and was used to slow that. Again, for economic stability reasons - RBNZ are likely to try to control any significant falls in the market.

A conservative estimate of 2 to 3% pa is probably what most experienced and successful property investors will be factoring in. Any experienced and successful property investor will be laughing at your assertion.

Quite conveniently you seem to have omitted the period 2008-11 from your "boom" period.

There was not a boom in that time, in sales or in prices.

So?

What is your point in relation to my posting and the point raised?

Factually it was not a long boom as you said.

Boom is not definable but a 40% price rise in 4 years is to me a mania. New Zealanders did not suddenly get flush and buy loads of houses at inflated prices.

Only Auckland had a mania and only Auckland is 30% Asian. And magically the mania died in the v six months China stamped on the hose pipe of money flooding into foreign RE. Also only Auckland had up to 40% of its sales being made to “investors” who take lots of houses and hence are fewer for younger buyers to buy at ridiculous prices.

Great leap in belief there mike.

Clearly you weren’t noting comments on this site between about 2012 and start of 2017 when every man and his dog in excellent English were raving about investing in property and how it was going to go up and up and up. That was local activity driven by falling interest rates. Everyone was talking about it at work. Reminded me of the NZ sharemarket boom in the mid eighties.

Oh, and mike if you don’t believe me, talk to a long term member of your local Property Investors Association - they will tell you of the sky rocketing numbers of increasing membership. But then doesn’t fit with your conspiracy theory.

Mike

Re your comment: "New Zealanders did not suddenly get flush and buy loads of houses at inflated prices".

No; but do I need to spell it out. The key was that interest rates were much lower, so instead of being 8 or 9% they were able to borrow nearly twice the money and hence houses - like shares - saw a sustained period of rapid growth. Cheap money in NZ was the main driver.

Everybody accepts that it was cheap interest rates and your assumption that it was all to do with "Chinese money" is a leap of belief and has all the hallmarks of a conspiracy theory. (Look up the definition)

Dp

Just another comment

Catchy title

Nice art deco...

... yes ... after all these years , art deco still looks pretty cool , funky ...

Mind you , I wouldn't pay a million $ for it !

Cheap debt is boosting confidence. Leverage up.

House price in Auckland rise...

Anyone and everyone knows.......Important is will it sustain and if yes what may be the level of price rise.

FHB who were already struggling are finished. Bad news for them.

Bend the stick as much as but not stretch far enough to break it.

This is what has happened with FHB in Auckland if this Price rise continues will break many FHB in Auckland.

Some may argue that anytime is good enough to buy but than with another boom round the corner what will happen to affordability. Wanting to buy a home is possible only if one can afford and definitely FHB in Auckland will have to give up unless wants to pay a premium for shit hole and ready to compromise in house (Am not talking about luxury house) as well as lifestyle.

No wonder election results world over are surprising. This time if opportunity party play their card well may be who know - may be king maker.

I feel obliged to make some comments after attending the Barfoot and Thompson auction at Shortland St this week.

My first observation was that two thirds of bidders (at least) were of Asian descent.

Second observation was that current RV or recent sales prices in the area seemed not to be a factor in how high they bid - they were determined to get the property at any price.

The final factor that marries with the above was said to me by an Asian Real Estate Agent who was surprised at the level of inspection that we undertook. She said that if an Asian buyer liked a property they would just buy it without that level of inspection.

My conclusion is that this sector of the Auckland buyers market is what is driving up prices in the lower quartile.

Probably mostly kiwis with NZ passports. Immigrants from Asia, South Africa, UK and Australia very often earn good incomes and can afford to pay a lot for houses. People seem to think they are all Uber drivers or kiwifruit pickers.

Are you trying to buy a first home or apartment framan? I think the reason for the comment of buying without intensive inspection hinges on the verb "liked". In other words the property has to suit them, they will not buy just any property only those that meet their criteria whatever that may be. An experienced buyer whether asian or caucasian will know what they are looking for and can make quick assessments just by looking and getting a feel as well as do background checks. The agent probably was getting sick of lots of questions and wanted you to bugger off.

You may be right about b------- off. Yes I am assisting my son - a FHB.

My surprise and dismay is that the prices being paid were so far out of line with prices paid in recent sales in the same street / similar home.

I hope he finds what he is looking for in the area he wants. I looked at 2 recent auctions. First in golflands 2/12 the green. Lots of buyers and onlookers. Sold 1040000 far higher than the homes.co estimate and the sellers had bought in 2015 for 880000. The second at 45b west st pukekohe. Sold 598000 for quite a bit less than RV and homes.co estimate. Only one phone bidder and the other couple dis not bid. The sellers lost money, bought 2016 for 655000. Both large b&t standalone homes on approx 600 sqm. The golflands one was a back section. As so often is the case the market varies from area to area. If it was me I think the pukekohe one could have been the best value buy.

So framan, being someone with a bit of experience in property and getting a current understanding of the current market trend when assisting your son you have noticed that houses are going for much more than similar properties recently.

Wrong! This is contrary to what many who have been posting over the past three to six months. They will be strongly denying your assertion - but there again you are in a position to know and I give your comments credibility.

May be this Asians are kiwi proxies of their friends, relatives or finanacers overseas that was being commented by few earlier.

Most FHB will check and pay as is hard earned money but most money comming from overseas is unaccounted money looking for safe tax free countries like NZ.

So national party friends are back in action.

Maybe they were us.

P.S. Heard about the anti-money laundering legislation and FBB and the extensive multi-layered checks by real estate agents, lawyers and banks?

Just goes to show that the doomie gloomies who have infested this site haven’t got a clue. The only bubble I see is the DGM bubble that is the interest.co.nz comments section.

Well that was a complete waste of key punches. But hey, if you're going to call people out for entertaining the idea that houses prices are in some kind of bubble, why not have a dig at people who buy gold? Considering gold is a hedge against the supposed madness of monetary largesse and bubble economics, people who invest in gold as some kind of protection represent a quintessential DGM.

https://finance.yahoo.com/news/gold-high-net-worth-wealthy-hoarding-phy…

And sure, there are people in Auckland who think they've hit some kind of jackpot because they've personally benefitted from the bubble. But trust me, bubbles are ultimately destructive, either when they pop or when they're being propped up. Nobody in NZ seems to want to openly discuss this (maybe because talking about such things is seen as "DGM"), so they gravitate to the steady line of empty patter delivered by The Hosk and Leighton Smith. They're not really doing themselves any favours.

Personally, it wouldn't bother me if I were called a DGM and cut off from some kind of suburban groupthink. Right now the Fed is engaged in pumping $500 billion of liquidity in Dec alone. While 95% of NZers might be blissfully unaware of this, some people will be aware. They will understand how asset markets have now become manipulated beyond recognition. To me, that's something people should be concerned about. And yes, if this all blows up, the fake economics of NZ will be exposed and possibly ravaged. If saying so earns me the DGM t-shirt, that's fine with me.

. . great post ... the property bubble has expanded beyond any rationale , beyond our wildest expectations .. .. so much so , it'll be a blood bath if it bursts ... not a problem for debt free long term owner / occupiers ... but a massive hemorrhage for banks and speculators... and that'll flow on , to infect the entire economy ... our house prices are now in the dangerous " too big to fail " basket...

not a problem for debt free long term owner / occupiers

Well my DGM hard hat is tightened firmly and I will say to you that these people are not immune. Let's say Trevor and Sally run their own business providing supermarket chains with those "nice to have", high-margin food delicacies that NZ supermarkets are famous for (they even have their feet in the online space too). Oh, and the villa in Kingsland is mortgage free. Life is good.

Now, let's assume not even a DGM scenario. Say house prices in AK fall 10-15% over a few years. Any idea what it does to people's choices at the supermarket and Trev and Sally's revenue? Chances are business will suffer. Now let's assume a full-bore DGM scenario. Loaves of bread, cartons of eggs, and Watties baked beans sell well. The whole "nice to have" categories and businesses crumble. Mark my words. This is a global phenomenon. Witness the rise of Dollar Tree in the U.S. and Daiso in Japan.

GBH. Catastrophising again?Just take a nought off the price of everything. 1m becomes 100k. Simple solution easily fixed overnight.

... call me a categorizing old boomer if you will ... but I still believe that houses are an essential asset for citizens , and ought be neither in short supply nor a speculative plaything for the idle rich and foreigners...

JC. We can "openly discuss" what you call a problem as long and loud as we care. Will it change anything. No. Unless you are Jesus Christ. So who can change the status quo and do they want to? I think the pollies and the rbnz CAN do something about what you call a bubble but they dont. Either 1. They agree with you but it must be in their interests to do nothing or 2. They dont agree with you and market cycles are a norm as long as it doesnt overextend. The Auckland market has been in a holding pattern for 3ish years now so that is not overextended. Is it?

One of the causes of a bubble is human psychology - we humans can be quite irrational (observe the history of financial markets.....read Irrational Exuberance by Robert Shiller if you haven't yet...and focus on the real estate section).

To say that Government or Reserve Bank can control human psychology is a bit far stretched - if that were the case there would never be booms and there never would be busts right? We'd have perfect levels of growth and inflation, no greed, no fear, just rational investors making sound decesions as a result of perfect policy settings, and returns perfecly weighted to the risk taken.

In this case the government and reserve bank have affected our psychology, just over a longer timeframe than you might think. Introducing inflation targeting and forever intervening to make sure house prices always increase has caused most to think that house prices always go up when it wasn’t previously the case and probably won’t be in the future once our current Ponzi scheme runs its course.

Great post and I am completely on the same page as you.

One of the interesting things that people don't get is recency bias. "This is the way it's worked for the last 5 years or so, so this is the way it will continue to work forever". It is a complete mistake, particularly when we have nearly tapped out monetary policy, productivity dropping in many first world economies, on track for $400tn NZD of debt by the end of the year (in excess of 3 or 4x the GDP of the world), massive derivatives markets bigger than the last GFC, corporate and local government debts looking to be in big trouble, gold looking like its going to go higher etc etc. We have created a situation where a hedge fund managers can ring up their central bank and ask for more money to be printed to push their asset prices a wee bit higher.

If nobody sees a problem with any of this and their obvious link to asset prices, particularly land and housing, you are living in a real "rose tinted" reality.

Incidentally we just had a visit from our neighbour, a young couple, one in IT and another a physiotherapist. They are leaving NZ in February - why? Because they cannot afford housing in Wellington. This follows from another 4 couples that I know have left for the same reason, 2 to Australia, 1 to the US and another back to China. All highly skilled professionals that cannot stay in a country due to high house prices.

You can't eat house prices. When the economy has no skilled people left to work in it, guess what? A low wage economy is bad for everyone, the old folk who are demanding it will be damned by it eventually. It's just a pity they can't see past their own greed to think about their own future 10-20 years out or the future of their country.

Spot on and well said.

NZ I am afraid has v little idea anymore that it is very vulnerable to international money system of money flows.

Wholesale market for banks is going to get v tough next year as world recession arrives.

The last down leg of housing market will then fall into place, as forced sales result from need to meet revolving rising debt costs.

Notice Auckland according to REINZ is now 44% of sales for NZ.

With 36% of the population.

Meanwhile sales falling in Wellington, Nelson and Christchurch as prices have gone up too much.

Thanks Mike for all the info.

Fair call DD - but are you willing to eat these words if you get it wrong (say over the next 5-20 year period)? Or are you just gloating because of this short term data point?

I'll happily eat my words in 5-10 years time if NZ housing turns out to be the best investment class. But I think we should equally acknowledge that prices are pretty high and history would suggest markets that have done what we've seen here in NZ have often fallen and fallen significantly. So I don't think we want to say for certain that this or that will happen because we just don't know. But if it does fall it has the ability to take the entire economy down with it - and that may cause wide spread suffering for a lot of people. Now you need to ask yourself whether you woul want to be one of the causes of that risk because of the negative impact it could have on other people.

I’m almost certain there will be another recession in the next 20 years, probably two of them. We would be well overdue if there isn’t one (or something close to it) in the next 5. Property prices will almost certainly fall when this happens. Wouldn’t be at all surprised to see recovery within 18 months.

I’m also confident that property prices will nearly double every 10 years.

I’m certain property is not “the best” investment class. But for the average kiwi, banks won’t lend as much to invest in the better ones in comparison to what they will lend for property investment.

Your account of the history of NZ’s property market is way off.

Infested? Getting a little Trumpian aren’t we?

Refusal to join in chorus of cheerleaders is not “gloom” etc. it is questioning. Which some of choir seem to really despise judging by language. Acidity does seem to be unnecessary and merely makes the site unpleasant

DD ...I'm not a DGM ...just a "realist" with the view that "past performance is not an indicator of future performance" ...also concerned about the debt bubble, just have a look at Aussie and what the rest of world thinks of that situation .....to say DGM's haven't got a clue, just illuminates your ignorance and arrogance ....have any of you "property bulls" ever run other businesses ?

Thought this was interesting:

https://www.infometrics.co.nz/chart-of-the-month-will-nz-housing-follow…

Prices are up about 2% in Auckland year on year.

This may be connected to the number of sales being made in Auckland City, especially above $1.5m

In Jan-August these sales were running 20% below the level for the same period in 2018 (1184 v 948)

Then, in Sept-October, this drop disappeared and sales were marginally up (286 v 288)

One might speculate how and why this surge has occurred , especially as it is not replicated in other price brackets.

Overall, REINZ said sales were 8.7% up in November 2019 compared to previous November.

A lot of those sales were made in Papakura. The median sale price down there is about $680k and the sales this year are up by about 35% on 2018.

Mortgage rate cuts have certainly improved things for FHB on repayment costs but the rise in lower quartile price is slapping them in face all the time.

Prices are not rising as fast as they were in regions and total NZ sales are well down on 2018 figures, inlc I notice, in Wellington.

The Auckland median in last year appears to have risen from $860k to $885k

Total Auckland sales in first 9m of 2019 were 11.2% lower than in 2018.

Consents of about 12,000 mean that stock available rose about 2.3%

RE NZ listings are now below 10,000 and 20% lower than a year ago.

I do not think the median will rise much further.

Extra money is arriving in Auckland for purchases above $1.5m.

This needs explanation, given the OBB.

I suspect that nervous investors are seeking safe havens for their money and that money is leaking out of Hong Kong, since this uptick comes on heels of severe recession there and chaos on streets.

Money leaking in from HK and China makes sense. There are probably plenty of duel HK NZ residents who can shepherd money from close friends and relatives. Or just people who will write side agreements to buy and hold residential property on behalf and believe they wont get caught.

Looked at other price brackets for sale sin Auckland City.

In Jan-Aug the user 750k bracket was down 17% in 2019 compared to 2018.

In Sept-Oct this improved to - 12%

In the 750 - 1.2m bracket the Jan-Aug 2019 figures were up 2% on 2018 and in Sept-Oct were up 6%

Contrast over 1.5m which were down 20% in first 8m of 2019 but up 0.006% in Sept-Oct

Biggest improvement in highest price sales....

Mikekirk

Do you ever look beyond your narrow statistical crunching and look at the wide range of real time and real world factors influencing the market - such as immigration, housing shortages, low unemployment, low interest rates, low housing stock . . . .

A few months on the basis of your number crunching I think I recall you were talking of a collapsing (price) Auckland market.

Printer8, read three posts up this very page and yes he is doing that.

Sorry printer but you don’t seem to have realised that my major focus is on macro political economic effects on Auckland REA. And lower interest rates of course mean can borrow more. Crux however is that due to amount now need to borrow there are a third fewer buyers than 6 years ago. So price is not good where it is and needs to come down and will after April

Hi Printer,

Mikekirk only checks sales volumes to justify his value position. A valuer only checks comparative prices. I wonder who is right.

You do not know, in fact WHY I do sales total checks.

Simple, it shows demand and ability to pay.

Debt I am afraid, cannot go up forever. The piggy bank offerings of lowering costs of interest to allow ever increasing mortgage borrowings is approaching end game. Then what? Prices will then not be supported by banks ability to lend fro buy at that price.

Price will then start declining.

November, October and September rises in prices in Auckland are suspiciously coincidental to need of HK rich to get their money out.

To you and your fellow back-slapper, I look forward greatly to April too.

You have very limited records Mike from July so you have no insight into what has gone on before then.. there are some pretty wild statements in what you say

I have access to REINZ figs back to 1992 in fact.

So no idea what u mean

I stand corrected but why did wilkes say it was more recent? I stand by my statements you draw wild conclusions and you hv no insight. You have been calling for falls in price of 15 to 40 percent, do you think that will happen by April, April 1st?

My forecast is and has been all along that cycle will bottom at €670k end 2021. Drop will recommence in April. Median going up and down due to variation in number of more expensive properties sold.

€670k, is $1.34m nzd?

My mistake : I meant $670k

Hi Mike

I eagerly wait for April.

I have a good memory.

Earlier MK said prices will drop following February 2020… In March 2020 he'll probably say prices will drop starting June 2020… then in June he will vanish from this site, like so many others

Interesting to see the big increase over 1.5m. Are you able to break it down any further than that? For example how about above 2.5m?

Imop houses have reached the upper limit price. That is the price a FHB or investor can and will pay in the lowest interest rate environment.

Whereas you can always buy fewer shares at a higher price houses cant be split without serious compromises.

If im right I expect house prices in the main centers to be flat or fall for decades. Think Japan. Elsewhere they may plummet.

In absence of Foreign money, hard for another major price in Auckland on Kiwi wages.

If house price would have stabilized (not falling) could understand but rise again and with this speed -Question to be asked, How foreign /Chinesse money is finding its way to NZ.

Is authorities not aware and seriously believe that 0.3% fall in interest(from already low rates) is the reason for this jump in million dollar range - just like national believed that no foreign buyers were responsible in the housing ponzi.

There's still a whole 1-2% (yes leaving us in negative territory) for the OCR to go!

Of course they will claim it will result in huge increases in business spending and pump up the economy heaaaaps, just like the last 10 or so drops have done (sarcasm). It won't lead to higher house prices like the past 10 or so drops have done (sarcasm).

The patients are running the asylum.

Someone said Auckland prices double every 10 years.

This of course depends on what year you start.

Also, stats only see to stat on REINZ in 1992

I do not think it at all likely that they doubled in 1984-93 for instance??

The primary manias were 2002-06 after China entered WTO and 2013-16 when Chinese rich were sending their money out into RE anywhere they could in world.

No mania is coming and prices are unlikely to do much more than rise by inflation + 2-3% pa for next 4-5 years.

"Also, stats only see to stat on REINZ in 1992

I do not think it at all likely that they doubled in 1984-93 for instance?"

Hi Mike Why did you choose those dates? Bit of a no brainer, and I am not old enough to remember what the figures might have been. First, there was the highly popular Lange govt and there was the bull run of share and property markets until 89 with a recovery from 92

I can recall an extended period from the late 1980's into the mid 1990's when the GV of the family home did not budge.... stuck in a rut ...

... oh , for those halcyon days when houses in NZ were affordable , when they were just somewhere to live , not someplace to speculate ..

Go on GB

Last century we all loved selling our home for more than we bought it. It is just that we didn’t know the word “speculation” or what it meant. :)

P.s. My wife and I have bought and sold eight homes over 45 years and always sold for more than we paid.

Highly popular?! No doubt you think so due to it being first neo liberal privatising NPM government?

No. They got a second term with a BIGGER majority, it was the heyday. You missed that fact by a mile mike.

22% interest rates. 1987 crash. Big unemployment increase. Decline in real income for half pop. Halcyon days

Simple Economy 101 for the 7% annual growth:

You have the vast population of middle class kiwi families with poor finance management. The ones who buy lotto every week, hoping to pay off CC and the hire-purchase loans. This result in a stable market of renters with no collective bargaining power. They will pay whatever sky-high the market rent is. Even if rental yield is higher than the interest rate, they cannot buy.

In a market with guaranteed rental return, and investor friendly interest-only loans with revolving credit, it is just a math game. Whenever the gap between rental yield and interest rate is low, it's time to accumulate via leveraged buy and hold (even slightly negatively geared, cap growth justifies it).

It's a low-income-earner myth that most properties are bought by rich Chinese, 100% cash. We'd be pretty bad at math to not utilise the loans here.

The 7% is the combined result of the amount of mortgage being issued by the bank and the increase of rental yield due to inflation.

Welcome to the world of free market.

The same clique of ideologically blinkered commenters furiously empleasuring themselves over a blip in seasonal noise.

Could replace them with a fairly unsophisticated bot and nobody would be able to tell the difference.

Absolutely insane - 8.2% nominal compound annualised growth rate across NZ, circa 6.2%+ real cagr.

Governments are meant to be by the people for the people, i.e. total welfare.

Not by the home owners for the home owners.

Some of its driven by worldwide low interest rates, but the immigration rate, taxation & RMA reform are in the Governments hands.

Christchurch gives a perfect example where there was no population pressure (re earthquake & proxy for sustainable immigration) and 2 commuter catchments (Selwyn & Waimak proxy for RMA changes) to soak up the growth.

Today, some price info as this might be informative for all readers.

All relate to November: All info from REINZ

1992: Auckland median $140,500. Index was 413

1998: Auckland median $230,000. Index was 693

2004: Auckland median $355,000. Index was 1150

2010: Auckland median $480,000. Index was 1414

2016: Auckland median $878,000. Index was 2880

2019: Auckland median $885,000. Index is 2923

Hence prices did indeed double 1992 to 2002.

Price rose 92% between 2002 and 2012.

Since 2012 they have risen 62%.

Since 2016 the price index is up 1.5% and median has risen from 878 to 885 (0.008%)

Median price rose 83% between November 2010 and November 2016.

The 3 year rise from 2013 to 2016 was 40%.

Those are the facts.

Population and dwellings have risen of course, and interest rates have fallen a lot since 2011.

But pop continued to rise 2016-19 by about 50k net pa and about 30,000 of them went into Auckland.

In those 3 years interest rates continued to fall. But price has not risen and sales are well down.

Thus, attempts to connect these two variables to price rises are not reliable.

By the way, median price in November 2007 was $450k and in Nov 2011 was $491k: a 4 year rise of 8.35%

The last 3 years (2016-19) prices have risen 0.008%.

So, for the boom to resume and get back to the 2010-16 rate, a hell of a large price rise is going to be needed up to 2022. This seems highly improbable

MK quoting yourself:

"1992: Auckland median $140,500, prices did indeed double 1992 to 2002"

so $281'000 in 2002 (according to your figures)

Quoting you again "Price rose 92% between 2002 and 2012"

so $539'520 in 2012 (according to your figures)

So that means $1'079'040 by 2022 to keep the doubling going every 10 years, quite possible, despite your conclusion

Quoting you "a hell of a large price rise is going to be needed up to 2022. This seems highly improbable"

Do some maths and start with price in 2016.

2012 to 2022 could double yes but still requires 23% rise above current level of $885k. In 3 years. Please explain why you feel it will so rise, given last 3 years being flat?

6%/year increases would take 2012 to 2022 to about 93% (1.62 * (1.06**3)) which is similar to the previous decade. I'm not predicting whether or not it'll happen, but we did just see a pretty high monthly increase so I wouldn't totally discount it.

Don't blame me, I'm just using your own figures, you're the one who decided to start with 1992 and end up with 2022, not me. So by the data you chose, starting at $140k in 1992, if house prices double every 10 years, then 30 years later they should be 8x higher so $1'120'000 in 2022 which is not that unconceivlable

As with any time series the result depends on start point. If you start at bottom of cycle ( say Janauary 2009) then prob is not a doubling by Jan 2019. Or could start at top of cycle about 2004-5 and compare to next top about mid 2015? I will report back on both

Auckland land supply restrictions were tight between 2011-17 and in 2017 these were then loosened. The land supply constraints caused Auckland house prices to rise faster than the rest of NZ market due to cost inflation. The loosening of the constraints caused Auckland house prices to stall due to Auckland land cost deflation. We have now reached the point where the Auckland index has fallen to meet the rest of NZ and everything should behave in a similar manner.

Correct with property prices almost doubling every 10 years, however this time around you will find it be different, there has been a lot of recent changes, from the countries economics to the new restrictions that have been put into place. Apart from the lending restrictions that have put off the foreign investors the gap between wages and rising property prices has widened significantly.

To see the property market rising in value you need to have the right driver factors behind it, low interest rates and rise in population is not necessarily a significant force. You will find other issues will rise with population increase and low interest rates.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.