House price growth remains strongest in Wellington and several provincial centres and much weaker in Auckland and Christchurch, according to the Real Estate Institute of New Zealand's House Price Index (HPI).

The HPI probably gives a better indication of market price movements than either medians or averages because it allows for changes in the composition of housing types that are sold each month.

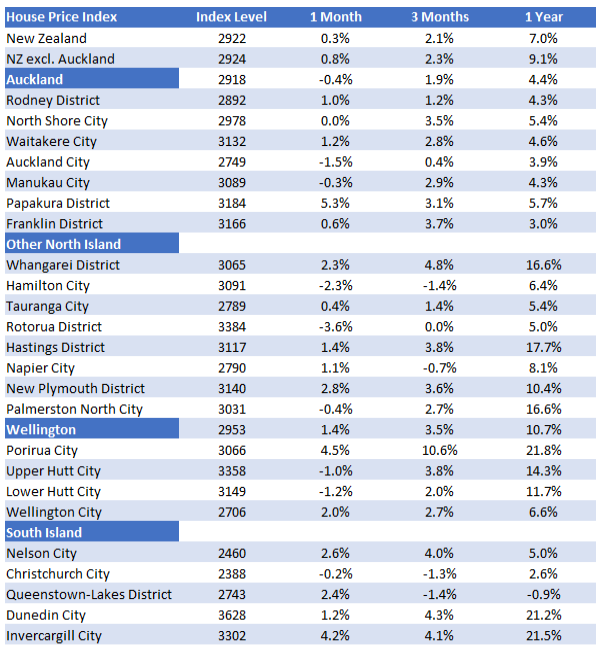

It showed an annual increase of 7% across the entire country between January last year and January this year, but price growth varied widely in different parts of the country (see table below for the regional breakdown).

In Auckland annual price growth was just 4.4% over the same period, while in the rest of the country excluding Auckland the annual growth was 9.1%, suggesting the regions are still the main drivers of price growth.

Within the Auckland region the annual price growth ranged from 3.0% in Franklin on Auckland's southern boundary to 5.7% in nearby Papakura.

Price growth was even weaker in Christchurch, with the HPI for the city increasing by just 2.6% in the year to January and declining by 1.3%.in the three months to January.

The weakest prices in the country were in Queenstown-Lakes, with the HPI for that district declining by 0.9% in the year to January and dropping by 1.4% in the three months to January.

The areas where price growth was strongest were Porirua where the HPI increased by 21.8%% in the year to January, followed by Invercargill 21.5%, Dunedin 21.2%, Hastings 17.7% and Whangarei 16.6%.

The comment stream on thsi story is now closed.

REINZ House Price Index

40 Comments

CHCH, nice place to live! NZ police recently deployed one of their patrol helicopters. Within a day, they were targeted by lasers! Obviously some didn't want Police to fly around and check on them..

https://www.stuff.co.nz/national/119607416/christchurchs-new-police-hel…

A certain grumpy old boomer has often described poor old Christchurch as the city of choice for people to shift to in future years. The words “what a lot of nonsense” come to mind.

OK Boomer

Well if 2019 is any indicator, the ol' housing train shows no signs of slowing down so consumer spending should be in great shape for 2020 as the wealth effect works its magic.

Trickling down like a golden shower.

"lag the rest of NZ"

what do you mean lag, so negative? Price stability is a good thing.

Auckland, Christchurch, and Queenstown house prices ahead of the rest of NZ in returning to affordability.

Check this graph out https://www.economist.com/graphic-detail/2017/03/09/global-house-prices

Whats driving the insane growth? NZ's standard of living relative to the OECD has declined. People feel comfortable their life revolves around servicing an inflated mortgage to fund Australian lifestyles? We have a low wage economy with poverty.

Whos the mug here?

Whats driving the insane growth?

Under supervised bank lending.

No Audaxes - that is more of an anti-bank sentiment statement.

Try RBNZ low OCR and mortgage interest rates for a start.

Banks are pretty well supervised and controlled in their lending through LVRs.

If banks were under-supervised and were lending recklessly, you would be seeing mortgagee sales which we are not.

Sadly, no regulator has asked banks to ensure they lend for productive and environmental projects – over two thirds of UK lending is not for productive purposes that creates jobs or boosts GDP, but instead for assets, causing asset price inflation. (same in NZ) Link

The RBNZ has confirmed two thirds of NZ households are mortgage free, hence around 60% of NZ bank lending is extended to one third of households (~$465,000 each on ave.) to fund leveraged residential property investment which does not qualify for inclusion in GDP - casino economics.

How many of that two thirds are renting rather than living a a mortgage free home?

I know of 4 households in my friends group who are early late 50’s and mortgage free, the rest have high mortgages because they have recently upgraded or completed renovation work that has cost them double the original quote.

From todays speech given by Adrian Orr

“Together with the Financial Markets Authority we reviewed the conduct and culture of New Zealand’s banks and life insurers. The reviews found many areas of weakness that need to be addressed quickly, so that the reputation and the public’s confidence is not irrevocably damaged. This work is ongoing and we are seeing progress in the sector

“Confidence is not irrevocably damaged” - sounds like our banks are as bad as the parent banks in Aussie.

Look up on Youtube for the live coverage of this enquiry. Particularly good watching if you like to see bank CEO’s squirming! Rowena Orr and Michael Hodge were excellent in their questioning often unable to believe what these bankers were owning up to!

The reviews found many areas of weakness that need to be addressed quickly, so that the reputation and the public’s confidence is not irrevocably damaged.

Absolutely no disclosure of these weaknesses for the public to ponder and possibly address with proactive disengagement, if necessary.

Not yet.

But when the rates rise the fun will begin.

My personal bias view? - it's all curb by the CCP about the capital outflow, then came uncle Johny from *NZ direct visit to CCP no 1 - then two months later? flurry of Chinese bidder started showing up in AKL south east. After lying dormant for quite awhile. Now, go figure where the most bank loan came from. This country is toast in the long run.

Who's the mug here?

Clearly people renting but I wouldn't call them mugs, it's very difficult to buy your first house.

BTW, do you realise that the link you posted is 2 years old? And that it warns about house prices being unsustainable? And that said house prices have gone higher since then?

We are in an interesting time regarding the housing market.

Over the past six months the drivers have meant that the upswing in the Auckland market and many regional markets have shown continued growth that was unsurprising and (e.g. Westpac) fairly predictable.

However, some of these drivers are changing - house supply, falling net immigration and especially increasing NZ citizen emigration, likelihood of stable low interest rates, increasing global slow down, election year . . .

There is likely to be increasing investor activity (as mention in Auckland by REINZ in their report) but increasing affordability issues are likely to act negatively for FHB. Increasing investor activity is likely due to CGT being well and truly buried, and the market indicating capital gains most likely; LVRs, ring fencing and increased brightline test will favour serious investors rather than speculators.

Although we may have increasing emigration by NZ citizens there is a tendency for many to hold onto their home and either rent or leave vacant in the fear of significant market increase when they return (FOMO).

Investment decisions will be interesting. With the low interest rates, assets (both shares and property) are likely to be favoured although by traditional measures highly over- valued. I think that the share market, due to the ability of investors to react quickly is a worthwhile barometer to consider. At the moment despite the Convid-19 virus and it’s wider economic implications compounding a global slow down, the markets so far have weathered the storm well (although I am expecting them to flatten in the short term) on the expectation that central banks will inject cash/lower interest rates.

So where to for 2020? Some slowing in regional growth rates and Auckland showing some continued but not spectacular growth. I see RBNZ apprehensive about further OCR cuts to save their powder, but possibly tinkering with LVRs for economic stability reasons if house price inflation is to high. As to LVR tinkering in the event of rapid inflation, that is likely to hit investors and favour FHB.

Net result is growth rates are likely to be more constrained but in the 2 to 8% range throughout different regions. Anything higher and I think RBNZ will act on LVRs for economic stability reasons where the global economy poses heightened risk.

Global economy Indicators have so many red flags it’s not funny. The FED continues to pump money into the US sharemarkets - $88 billion last night.... but hey little old New Zealand will be ok as our house prices are going up!

I get detailed house sale stats from my local friendly realestate agent..... majority of homes are selling below CV. Also looking at Realestate.co.nz there are a massive number of 2019 unsold homes in my area Eastern Suburbs).

One house owned by a real estate agent was passed in at Auction in November priced then by negotiation, went to auction again last week and is priced again. 3 New builds in St Heliers have been up for sale since September 2019. Very large houses on no land a few houses away from a soon to be built retirement village. Just a couple of examples

So, since your post totally contradicts REINZ data published yesterday, are you saying you have more comprehensive data than REINZ?

Startling landslide news, Yvil.

I was outside a Grey Power meeting yesterday; talked to three people, two of whom said that they were going to vote NZ First.

Come September, NZ First set to govern alone on 66% of seats!!!!!! Yvil, you need to accept this.

P.S. However, good to get some dialogue going on current observations and file away any anecdotal information .

There's a few of these big boxes on postage stamp sites for sale, just like those on Waimarie Street. If they aren't selling it simply because they are overpriced. Other properties like 65a Allum St are sold within days on the market.

I don't know 65a but I did view 7 Allum St. Cracking house that sold for 3.25m (at auction I think) back in Sep, 375k over CV.

For something more recent, I popped into Barfoots auction today and saw 14 Kensington Avenue, Mt Eden (CV 1.925m) sell for 2.525m.

CVs a joke. They are so far out of reality in a lot of cases I don't believe anyone can use them as a gage for value. Ive seen so many cases where the value is both well below or well above the actual value. Real estate agents that don't put a price on a property just show their ignorance in their own market. CV is just a lazy tool.

Good post printer8, I appreciate the effort put into it. Side note: your username always reminds me of the REM song "Driver 8" :-)

Interesting times for sure. For Auckland, I think we're seeing it start to transition into a "proper" big(ish) city even by global standards. I think it'd be interesting to look at what happened to property values in other cities as they passed through the 2million population threshold. My guess is that location became ever more important.

Regarding net migration, I expect it to remain moderately high. Low enough that Labour can claim to have lowered it, but high enough to keep stoking the economy.

What should really be implemented is debt to income ratios.

Brock

That has some merit for slowing house price inflation. Unfortunately a debt to income ratio is going to mainly hit first home buyers.

Mum and Dad and other investors are still going to be able to leverage against the family home and other investment properties, and although yields are low, rental income is likely to be sufficient to mean any debt to income ratio is not an issue.

I still see a 20% deposit being the biggest handicap to FHB and it really concerns me that home ownership rates for 25 to 35 year-olds have fallen from 65% in 1988 to 35% currently.

Given that many 30yo plus potential FHB are faced with young family with remnants of student loans are constraints to getting into a home. Boomers typically purchased a home by 30 and prior to a family as although interest rates were considerably higher, the house price Vs income was considerably lower (plus a lack of student loans).

While the low interest rates persist the reality is that house price to income ratio is going to remain high and the biggest hurdle for a deposit for FHB. Servicing a mortgage is likely to be a secondary issue.

There are those posters calling property a "Ponzi-scheme"; however I question how much of this negativity is based on frustration and anger.

The REALITY is that the alternative to home ownership is renting; this means paying off the landlord's mortgage rather than yours. The landlord gets to keep the house (including long term capital gains) and the renter walks away with absolutely nothing - and the landlord will have ensured that the tenant has covered not only the mortgage but maintenance, rates, and insurance plus a return on his/her investment.

It seems we have moved from a society in which there was relatively high home ownership rate to one of increasing renters. If this is not a permanent societal change, then it is certainly is a significant reality of the current 20 to 35 year-old and younger generations.

"the landlord will have ensured that the tenant has covered not only the mortgage but maintenance, rates, and insurance plus a return on his/her investment."

There are a large number of investment property owners who are negatively geared and were claiming tax losses. A number of them will be filing tax returns for the March 2020 tax year, where property losses will be ring fenced. That is when many part time property investors may realise that they're not getting an offset in their taxes (and a potential tax refund). That may change the financial attractiveness for some investment property owners.

CN

You are either kidding yourself or being a bit naive if you think landlords will be investing in property to make on going losses. Your stumbling block is that you take a very short term view.

True that many landlords will buy property that could initially - note "initially" - be negatively geared. . . and that is a loss in terms of tax purposes but is likely to be either off-set by capital gains and/or clearly going to become profitable within a very short period with rent inflation and mortgage being paid down. No landlords I know would be looking at a property that will not become positively geared within a year or two.

Landlords are not in the game of investing in properties that will be forever running at a loss.

Most Mum and Dad investors will be looking at a rental being a source of income for retirement and will plan for it to be mortgage free and well maintained - and rent will be ensuring that.

Bottom line - you keep renting, you walk away with nothing while the landlord will be looking at you paying off the mortgage and meeting all expenses related to maintenance, rates and insurance and to be pocketing all the capital gain.

In terms of losses, there is only one loser here; that may seem harsh, but it is the reality.

Just out of curiosity, which area of New Zealand are your investment properties located in?

"You are either kidding yourself or being a bit naive if you think landlords will be investing in property to make on going losses. "

Property investors never plan to make losses indefinitely, they are always unexpected. That's how property investors get blindsided. Recall the numerous examples during the 2008 / 2009 global financial crisis when many highly leveraged property investors lost money. During that period, a large proportion of sales were owners that sold their investment property below their purchase price. Some even went bankrupt ....

There were also some property investors who purchased investment property only to subsequently find out that they purchased a leaky building and which then required significant repair costs.

Then there was the landlord who found that their investment property was tainted with the drug methamphetamine.

There are lots of other cases of property investor losses which were unplanned and unexpected.

Property investors and owner occupiers buying at current price levels, in some geographical locations in New Zealand, and are financed using high levels of debt are vulnerable to risk of losing money ...

Some links for you:

1) meth damaged property - https://www.stuff.co.nz/national/89594981/family-facing-bankruptcy-afte…

2) leaky building - https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

3) tenant damage of $25,000 - https://www.stuff.co.nz/business/property/117593943/landlord-furious-af…

"Most Mum and Dad investors will be looking at a rental being a source of income for retirement"

Totally agree with you. That is the reason a large number of these investors have bought investment property, as it is seen as a form of income to supplement their pension from the government and former employer.

Remember, that being a residential landlord is being in the residential property leasing business. The residential property leasing business has business risks, some of which have been highlighted to you above.

FYI, was previously in the residential property leasing business for over 20 years, and got out in 2017. Why? The answer is simple - expected future risk adjusted returns were considered unattractive, and the funds could be redeployed elsewhere for more attractive risk adjusted returns.

Now here is an investment choice for you, which is more preferable?

1) an investment which returns 70% of your money over the next 3 years (i.e a return of NEGATIVE 11% per annum, or 30% loss)

2) an investment which returns 2-3% per annum?

Looking back at the residential property sold above, the new owners have subsequently resold the property at a lower price. If they financed it on a LVR of 80%, and a 30 year P&I mortgage, then they have lost about 30% of their investment (that's about a return of NEGATIVE 11% per annum). Alternatively, instead of purchasing the investment property, the new owners could have kept the money in the bank at 2-3% per annum.

Of course, these new owners didn't plan to make a loss, but that is the way it worked out for them in reality.

Yep it doesn't surprise me that house price growth is weaker in Auckland, CHCH and Queenstown Lakes. That's what happens when you reduce foreign buyers activity from the ponzi scheme.

Slowing the market by allowing wage earners to buy is much better and far more sustainable.

Never fear. Elect Simon Bridges and he'll do his darndest to get foreign buyers buying in droves to firmly push those houses out of the reach of young Kiwis.

Doesn’t the article title tell you all you need to know?

Speculation, speculation, speculation.

The only cure for speculation is to let the speculators get burned. Then fear will keep them in check.

This is something that the government and the reserve bank have demonstrated they are totally unwilling to allow to happen and so the speculators continue to egg eachother on and the problem gets worse and worse.

Completely outraging to see how this bloodshed keeps going on for years, wealth transfer towards the richest in form of mortgages impoverishing people with every % of housing price growth. Governments are there for a reason and obviously for many years they have been ignoring their role in controlling land prices and making affordable and healthy housing available to everyone.

The rbnz has done a great job of fueling the housing market rise with its low interest rate policies. My house value just keeps going up. Thank you!

FYI, property investors to blame for NZ's high house prices, not lack of supply, researcher says

https://www.stuff.co.nz/life-style/homed/real-estate/119511533/crackdow…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.