By David Norman and Shane Martin

• Housing affordability remains a challenge for many in Auckland. Land use regulations such as the Rural Urban Boundary (RUB) are often blamed.

• But until now, no studies had looked at whether the RUB distorts land markets.

• Pre-RUB studies also underestimated the cost of infrastructure to develop greenfield (or undeveloped) areas, and in some cases ignored the value of location or mis-attributed amenity value.

• Our reviewed analysis shows the RUB accounts for at most between 0.6% and 5.2% of the price of the average developed residential property that has land and is inside the RUB.

• But market prices do not include the social impacts of more expansive development on things like congestion, emissions, viability of public transport and optimal use of existing infrastructure.

• We should evaluate whether these social impacts justify the RUB before bold recommendations are made on the RUB’s future.

The RUB debate

With housing affordability still a challenge for many in Auckland, the finger of blame often points at land use rules, such as the old Metropolitan Urban Limit (MUL) or current RUB, both of which have limited development outside certain areas of the Auckland region. If a growth boundary results in a land price premium that materially increases the cost of housing, then given Auckland’s housing affordability challenge, there would be an argument for removing the boundary.

The facts of this matter are fundamental to the shape of Auckland in terms of its growth, infrastructure provision, and economic and social outcomes. This means any policy to contain or expand development should be based on even-handed, defensible evidence.

The view that the urban boundary imposes a substantial premium on land is universally based on studies done on the obsolete MUL. On 15 November 2016, Auckland’s Unitary Plan became operative, consolidating the different zoning rules in the various legacy plans of the councils that amalgamated to form the new Auckland Council in 2010. It replaced the MUL with the more flexible RUB, which includes around 30% more land.

The Unitary Plan was the biggest change in zoning rules in New Zealand’s history, and increased physical development capacity in urban areas by around two million dwellings. This is several times Auckland’s projected housing demand over the next 30 years. Within the RUB, allowance has been made for around 137,000 new homes in greenfield areas. These significant changes render previous studies on Auckland’s MUL obsolete.

As our full technical report points out here, previous studies also had a number of other limitations. They generally underestimated or ignored the cost of infrastructure to turn greenfield (undeveloped) areas into residential-ready areas. As a result, they overestimate any price premium on developed residential land.

One often-cited study, which estimated the cost of land use regulation under the MUL at up to 56% or $530,000 of the total price of an average property (not land) in Auckland, also excluded proximity to the CBD as a determinant of property values in Auckland. Yet practically every study that includes this variable finds that proximity (especially to the CBD and/or jobs) matters.

Previous studies have dealt with the value that amenities add to properties with varying accuracy and detail. One study accounted for amenities by using a dummy variable for each suburb, but then assigned the value of this variable to the cost of land use regulation. It effectively assumes the difference in land prices in Ponsonby, with its proximity to jobs, the water, hairdressers, supermarkets and coffee shops, and rural areas near Pukekohe is overwhelmingly the result of land use regulation. But land is not geographically identical. Location matters.

Other gaps in previous analysis that we wanted to overcome included:

• selecting an appropriate way to compare parcels of different land sizes inside and outside the RUB

• using real-world sales data rather than property valuations (to avoid modelling a model)

• accounting for net useable land when converting farm or lifestyle land into residential sized sections

• considering natural hazards such as risk of flooding in determining property values.

The question we posed

Put simply, we ask if converting farm or lifestyle-sized land outside the RUB into infrastructured residential sections similar to already developed land inside the RUB would deliver land to the market more cheaply. If there is a material premium on land inside the RUB, it would imply that the RUB is inflating land prices inside it.

We define the RUB factor as the share of the price of the average developed residential property that has land and is inside the RUB that is attributable to being inside the RUB, if any.

We provide a brief summary of our approach later in this article but recommend the interested reader tackle our full technical report. In short, we built a standard hedonic pricing econometric model to explain property prices as a function of the dwelling, land, and location. We gathered screeds of information about the nearly 37,000 farms, lifestyle blocks and residential properties with a land component that sold in and outside the RUB between 15 November 2016 and 31 March 2019. This allowed us to explain much of the variation in property prices depending on property characteristics and location.

What we found

Our goal was to isolate the un-amenitied, a-spatial value of land in farm sized (four hectares or bigger) and lifestyle sized (0.4 to four hectares) land outside the RUB, and compare it to the un-amenitied, a-spatial value of developed residential land inside the RUB (less than 4,000 m2 in size).

The “un-amenitied, a-spatial land” value is what remains once we strip out other things that add value to property (such as proximity to jobs, the water, parks, or “good” schools; or the size and condition of the house, views, and contours of the land). We then estimate the value of un-amenitied, a-spatial farm or lifestyle land outside the RUB of the same size as the average developed residential property inside the RUB (618.7 m2 ) without these confounding factors. Here’s what we found.

Figure 1

Un-amenitied, a-spatial value of 618.7 m2 of land, before accounting for net usable land and infrastructure

| Farm-sized | Lifestyle-sized | Residential-sized | |

| Outside RUB | $1,069 | $7,447 | $67,164 |

| Inside RUB, Inside FUZ | $21,594 | $28,695 | $99,203 |

| Inside RUB. already developed areas | $70,098 | #37,000 | $132,665 |

This figure does not say that the average residential section in Auckland costs $132,665. It says that once you have removed almost everything that adds value to a property – its dwelling, its location and amenities, and other characteristics of the land – this is left over. The figure for farm-sized land outside the RUB is $1,069.

But it would be a mistake to stop the analysis here.

First, when farm or lifestyle-sized land is converted to residential use, a large share of that land will be converted into roads, stormwater run-off, parks and other uses from which no financial return will be made by the developer. This means the value per square metre of raw land needs to be adjusted upward based on an assumption about how much of the land will be used for non-recoverable purposes once converted to residential use. Recent Auckland structure plans suggest around 57% of land becomes unavailable, meaning the cost of the land must be recovered from the remaining 43%. To err on the side of conservatism (i.e. overestimating the RUB factor, if any), we assume 65% of farm and lifestyle sized land is available for cost recovery.

Second, and far more importantly to the results, the major difference between farm and lifestyle land on the one hand and developed residential land on the other is access to infrastructure – running water, flushing toilets, roads, power and the like. It stands to reason that the cost and value of that infrastructure would add massively to the value of land. Yet only one previous study we know of in New Zealand has made an explicit attempt to account for some of these infrastructure costs.

Figure 2

RUB factor using various infrastructure cost scenarios

| Property location | Higher estimate of bulk infrastructure costs |

Average estimate of bulk infrastructure costs |

Average estimate of bulk infrastructure costs, 15% of subsidy priced into land |

Average estimate of bulk infrastructure costs, 30% of subsidy priced into land |

Lower estimate of bulk infrastructure costs |

No allowance for infrastructure costs |

| Farm sized land outside RUB | -$77,580 (-8.1%) |

$15,820 (1.6%) |

$27,220 (2.8%) |

$50,380 (5.2%) |

$58,420 (6.1%) |

$131,020 (13.7%) |

| Lifestyle sized land outside RUB | -$87,391 (-9.1%) |

$6,008 (0.6%) |

$17,408 (1.8%) |

$40,568 (4.2%) |

$48,606 (5.1%) |

$121,208 (12.6) |

The Future Urban Land Supply Strategy (FULSS), which sets out the sequencing for an estimated 137,000 new dwellings in greenfield parts of Auckland inside the RUB, provides an insight into the likely bulk infrastructure costs. Our full technical report provides detail on how this work was used to estimate the cost per dwelling in greenfield developments outside the RUB. For a number of reasons we list there, the estimates we use for bulk infrastructure in this analysis are likely to be far lower than would be the case outside the RUB, but again, we err on the side of conservatism.

The cost for bulk infrastructure, notwithstanding they are lowball estimates, is eye-watering, ranging from $72,600 to $208,600 per dwelling. The average estimate per dwelling inside the FULSS area is $115,200. We would also note that even these figures do not include all of the infrastructure provided by central government or other costs of subdivision, including surveying, resource consent, legal and Land Information New Zealand fees that would be incurred in cutting up a farm or lifestyle land into residentially-sized sections.

Applying six different estimates of the possible cost of bulk infrastructure to develop farm and lifestyle land outside the RUB into useable developed residential properties similar to those inside the RUB, yields the RUB factors in Figure 2. The most defensible upperbound estimates of the RUB factor are in the dark grey boxes. We have pointed out the absurdity of a view that no infrastructure costs should be allowed for, but present that result too for the sake of completeness.

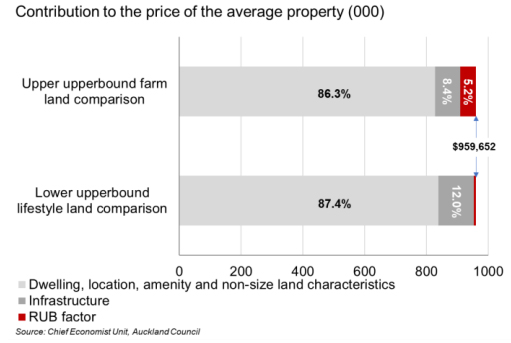

The most likely upperbound range of values for the RUB factor is 0.6% to 5.2% of the value of the average developed residential property with land inside the RUB (value of $960,000). We label this an upperbound range in large part because of the low estimates of infrastructure we have used throughout, and our exclusion of other subdivision costs altogether.

We ran numerous sensitivity tests on different model specifications, many at the suggestion of our external reviewers. None of the tests changed the modelled results in either direction by more than a few percentage points.

This last point is important. At higher infrastructure cost estimates, or different model specifications, it is possible that properties outside the RUB actually carry a premium. This would likely be because often two-thirds or more of the cost of bulk network and social infrastructure in greenfield areas is not borne by the property developer. Assumptions that this will continue to be the case may be encouraging land prices to be bid up outside the RUB, with the anticipation that the RUB might expand or disappear altogether.

What does all this mean?

Our analysis shows that the RUB factor, if any, is massively lower than previous work on the MUL had suggested. The reality of what the Unitary Plan has seemingly done to land markets, and accounting better for infrastructure and amenities matters significantly to how we think about the impact of the RUB.

Figure 3

Role of the RUB factor in the price of the average property

What about the social costs of sprawl?

Further, market prices do not include the relative social impacts of more expansive development on congestion, emissions, viability of public transport and optimal use of existing infrastructure, for instance. Our work provides a starting point for an informed debate on whether a RUB factor of up to 5.2% is justified given the social costs that may be part of more expansive development that would come with relaxing or removing the RUB.

A thorough analysis of whether these social impacts justify the RUB should be completed before bold recommendations are made on the RUB’s future, given the impact keeping or removing the RUB has on the shape of New Zealand’s largest city, its infrastructure needs and community outcomes.

How we did it

The interested reader will want to read our full technical report. But in summary, we used hedonic price models with spatial error disturbances to explain prices in farm, lifestyle and residential properties. We tested numerous models, but settled on a three-model approach with separate models for farm, lifestyle and residential sized properties, all of the same specification. This allowed for different values to be placed on amenities or the value of an additional square metre of land by property size category.

We did not use a “difference in difference” modelling approach, as we were not asking how the RUB affects land market prices relative to the MUL, but rather how the land market operates today, since the Unitary Plan and RUB were introduced. Further, the results of a difference in difference analysis could almost certainly not be meaningfully interpreted. Land that was outside the MUL but is now in greenfield areas inside the RUB would be expected to increase in value given the promise of infrastructure, but how much would be largely a subjective interpretation.

We are confident in the reasonableness and explanatory power of our preferred model, but we ran numerous sensitivity tests. These tests included using spatial error and lag models; a number of different spatial weights; models with and without median income; with and without zoning; with and without additional RUB, or RUB and FUZ dummy variables; with different thresholds for setting size categories; using log forms for estimating the value of an additional square metre of land; using capital value instead of actual sale prices; and using one combined model instead of three.

* David Norman is chief economist at the Auckland Council. Shane Martin is a senior economist at Auckland Council. This article was first published here. It is here with permission.

65 Comments

"But until now, no studies had looked at whether the RUB distorts land markets"

That's no-one except urban economist, Arthur Grimes and colleagues at Motu who published this in a refereed journal as well as this earlier working paper

Read them all and make up your own mind.

The MUL and RUB are technically different things.

And they do cite that Grimes paper in the technical report..

But this is an excellent example of a rubbish empirical model conveniently producing the results you want. Probably 95% of the covariance in house price models comes from like 10 key characteristics. Always be dubious of the intentions when you see a 3 page table of coefficient outputs.

I especially like the argument where they try to argue land area should not be measured in log form. Dunno how much precedent that approach would have in the literature..

Don't know how it was under the Town and Country Planning Act but under the RMA there is definitely no such thing as a MUL or a RUB. They are pure inventions of the former Auckland Regional Council. When North Shore City took ARC to court to set aside the MUL/RUB they won. And they won basically because the RUB/MUL do nothing to implement the s5 purposes of the RMA.

So, when you say the MUL and the RUB are technically different that may be true but only in the minds of Auckland Council. It doesn't really matter for the purpose of the argument because as Grimes points out there is a long history (pre-dating the re-organisation of local government and the introduction of the RMA) of the Auckland urban area being constrained to prevent sprawl. Whatever name you give it.

Yea, I 100% agree. There is very little tangible difference between the two. And as you say, a growth boundary is a growth boundary.

I was more pointing out that the statement was technically correct and they had cited Grimes in the technical report.

Standard DN parlance is to try and make things sound more novel than they really are in his bulletins. I must say, though, although he won't have done the empirics, the standard (although still low) is better than the standard spurious correlations he normally presents.

Yeah, ridiculous (and totally untrue) comment from the council's chief economist spruiker.

Who may earn a pay rise to be funded by ratepayers paying higher levels of rates set by a monopoly?

When was the last time anyone experienced a fall in rates in Auckland? Wasn't that the rationale of Supercity?

In 2016 the Rural Urban Boundary was introduced expanding the buildable area by about 30%. Sounds good except population growth in 2016 was 2.8%. At that rate Auckland's population will have grown by 32% before 2026.

The conclusion looks flawed.

The RUB can only affect the land price component. The dwelling,concent and infrastructure costs are roughly fixed.

The "non-size land characteristics", e.g. amenity and excess demand though excessive immigration again only affect the land cost component.

Assuming the dwelling, consents & infrastructure are 50% of the total value, leaves the other 50% due to the land price component of which 5.2%x2=10.4% is the effect of the RUB.

These authors have obviously read a lot less than me and I am not an economist: I am merely a concerned citizen who lobbies and makes submissions on this issue.

There is one principle that completely wrecks these authors main hypothesis. That is, under conditions of rationed land supply and "extractive pricing" of land, the cost of infrastructure, now recovered in the form of development contributions, represents a SUBTRACTION from the equilibrium market price for greenfields land, NOT AN ADDITION! The price inside the boundary would go up if DC's were abolished. Even for the infrastructure that developers put in themselves, this is something they SUBTRACT from the price they are willing to pay for land. The cost of infrastructure only LOOKS like "an addition to the price of land".

In the absence of a boundary, and developers paying true rural value plus a premium for capitalized transport cost savings, the price they pay and then add infrastructure costs to, is FAR LOWER.

Numerous economists who should know better, are stupidly ascribing to "amenity value", what is actually a form of economic RENT of the monopolistic or extractive kind. Differential economic rent (which is what exists in the absence of a boundary) is merely a premium that reflects cost savings on transport and potential share of higher incomes. This is only ever a few percent, NOT AN ORDER OF MAGNITUDE! The "order of magnitude" inflation that follows imposition of a boundary, represents monopolistic or extractive economic rent; people now being price-gouged for "the maximum they can stand" rather than a fair "better value" because of location alone.

Next important point: "supply of land". Planners (and economists who should know better) are assuming that "the land inside the boundary" represents "X years supply of land" with "X" being "the total quantity of new land inside the boundary, divided by the rate at which the market is requiring land". But this assumes that ALL THE LAND IS ACTUALLY FOR SALE!!!! In reality, so little of it actually is for sale, that the whole dynamic changes to "developers entreating owners to sell" and the owners price expectation changes by an order of magnitude within a single property cycle after imposition of the boundary. Inflation begins within 3 or 4 years and is explosive - witnessed again and again in every urban area that imposes a boundary. The denial about this is a disgrace. Besides the reality of little of the land being up for willing sale, developments take years, and developers also like to acquire their "next site" before they finish their current one. This means that around 8 years worth of land supply on average, needs to be "already in the hands of developers". Real urban economists studying this issue conclude that the boundary with sufficient supply inside it to not inflate prices, would have to be so large there might as well not be a boundary.

"Splatter" development is a necessary feature of a housing market that is affordable due to the absence of land rationing. I can cite several studies that concluded that "splatter" development is efficient, not a "necessary evil". This is because splatter development becomes an initial guide to the market and to planners, what is the most efficient potential use of the as-yet-fragmented land. The incremental contiguous "carpet" growth insisted on by planners, foregoes the evolution of numerous efficiencies including the formation of new agglomerations. More than one study in Britain has concluded that "nothing like Silicon Valley is possible" under these conditions. Clusters are of multiple types, and the great majority of them studied by economists formed during periods when land was cheap and there was affordable space for new participants including the workforces. This is the main reason that commuting times and patterns are so inefficient in British cities in spite of 6 decades of "growth containment" planning and densities sustained that are on average double those of Western Europe, three to four times those of Australasia and Canada, and 5 to ten times those of US cities. There is in fact no evidence from commuting times that there is greater efficiency in cities that have grown by forcible cramming inside boundaries. Similarly, there is no evidence that density in lieu of expansion, results in anything other than exponential inflation in economic rent, to such an extent that housing costs always increase with downsizing of housing units. ALL the median-multiple-3 cities in any data set have large-section houses as their average or median "new housing unit". The land cost for these houses is exponentially lower than the land costs in a boundaried city.

What Phil H said.

To quote:

'land is converted to residential use, a large share of that land will be converted into roads, stormwater run-off, parks and other uses from which no financial return will be made by the developer. This means the value per square meter of raw land needs to be adjusted upward based on an assumption about how much of the land will be used for non-recoverable purposes once converted to residential use. Recent Auckland structure plans suggest around 57% of land becomes unavailable, meaning the cost of the land must be recovered from the remaining 43%.'

Wrong.

If the land has to be put aside as a park for example, then that is providing an amenity value the developer can add to the price of the remaining sections. if that Park was not allowed for, he would have been able to develop more sections, but they would have less value.

If a situation arose where the developer could not recoup the costs for parks or roads etc. within the developed section price, then he would factor this in on the initial offer he made on the raw land, ie he would offer less for the raw land, NOT upwards as you claim.

Not sure I agree entirely with you there, Dale. But the quoted argument misses the point. If a developer is converting land costing $30K/ha instead of $2m/ha then they can afford to build the Taj Mahal as a playground and still charge less for sections than those in modern developments where the local park is a 100m2 patch of scrabble with three dead hebes and a see-saw.

Yes, agree, the report does not even seem to wonder why in other jurisdictions that land can be purchased at tens of thousands rather than millions of dollars per hectare.

And this is after taking into account dwelling, location, and amenity, and non-size land characteristic costs.

In a competitive, less restrictive market (which NZ used to be up until the early '90s), in a hypothetical subdivision financial model, the land cost is what is left over after you have deducted all other costs. Some of these costs might have been needed to mitigate land issues, so naturally accounted for raw land that might need extra work to bring it up to a 'developed' level.

The fact that they have a FUZ within a RUB, is really just another name for a MUL with a FUZ attached.

The RUB is just a MUL on steroids.

'We did not use a “difference in difference” modelling approach, as we were not asking how the RUB affects land market prices relative to the MUL.'

How about trying the difference of having a RUB, with the difference in not having one?

IE a non-competitve land market vs a competitive one.

Incredibly, it seems that the author's very methodology should have arrived at the conclusion that the RUB makes no difference at all, because their formula is essentially "circular". Their conclusion that it is responsible for between 0.6% and 5.2% of the price, is really just accumulated noise in the data. I mean, they start with prices under the status quo rationing arrangements and look at all the other cost inputs and find a mismatch, so this mismatch must be "the effect of the RUB". This reminds me of one of those "think of a number, any number" show tricks.

It's a bit more complex than that and your broad assumptions about noise are incorrect. This is a generally correct approach to identifying the effects of interest. But they just do some weird things within the empirical framework.

Of course land use regulation is never truly exogenous from price, but given that they are studying it post AUP sorta mitigates many of these such issues.

So the article heading is incorrect; the study was about the effect of interest rates on a property market inside a growth boundary, not about "the effects of a growth boundary on the property market" at all.

"The effects of interest" did not refer to the the effects of interest rates.

Surely you didn't interpret it as such. That would just be too embarrassing for you as it shows you didn't take the time to even read the technical report. Even worse, if you did, you didn't understand it..

Poor old David Norman , he is a brilliant economist in my view , and is a very competent analyst , and his scenario planning is excellent ,

That said , he has the unenviable task of telling the motley bunch of fools running Auckland the truth , and cannot simply say that we have too many people in Auckland to cope , too many new arrivals , money is too cheap causing asset price inflation ( houses ) , and the Urban planners are asleep at the wheel .

Why can't he tell them that?

And is this report then, his cognitive dissonance behavior because he can't tell them, ie something that is not true but that they will believe?

I don't get how, having made provision for 137,000 new homes in greenfield developments inside the RUB, demonstrates that urban planners are asleep at the wheel?

As the Special Housing Area fiasco showed, its one thing to draw a plan showing where 137,000 dwellings could be built even to consent subdivision in a whole lot of places it's another thing to actually develop and sell those sections.

The realities of a council's ability to fund extension of infrastructure let alone the economics of buying expensive undeveloped land and making a profit off subdividing it tends to get in the way of the dreams of planners.

You kind of make my point - planners make plans - they don't own land, nor determine when it will be developed. So I still don't know what the actual criticism of planners, or the AUP is here?

I read an article once where the author suggested that planning has become the scapegoat for the failures of neoliberalism (in other words, where the market has failed to deliver, planning gets blamed). It is worth thinking about - we just did not have these housing problems prior to our major reform period.

No, the planners are responsible for the failure, not "the market". You understand that the planners don't own the land or determine when it will be developed. So take a step back and try and understand why median-multiple-3 housing markets are possible when there is no growth boundary or proxy for it. Nobody is "planning" sales of land or development of it, but "the market" works THEN, doesn't it? It stops working when planners impose a boundary, and you conclude that "the market" is what "failed"? Incredible!

The median multiple in NZ is where it is for a simple reason: immigration and capital inflows outstripped our ability to construct new supply, particularly in AKL - and where that boat rose all others rose with it.

"Our ability to construct supply" - funny, but the reports I've read on this say that we built a lot more houses in the 1960's and in the 1980's than we have since the land-rationing policies became fashionable. I think I already described in another comment, how the industry suffers from the distortions created by the rationing of land. This is a familiar story from Britain and everywhere else these policies are imposed. The construction sector gets lumbered with risks and delays and "game playing" to survive (and many firms go bust right when they are needed) then the planners claim that "because the industry didn't respond as fast as it should have, that must be where the constraints are, not in our regulations".

People attracted to central planning, as economic history shows, are clueless about real life and economics. In so far as they use arguments from economics to try and evade blame, they use shallow ones that are wrong.

I am reminded of Winston Churchill's comment about 20th century communism conducting "the world's most expensive remedial lesson in economics" but the modern urban planning fads must be a close second, historically.

There is something nonsensical about this report. Expensive lifestyle block land is $250,000 per hectare. If 10 to 20 twenty houses are built on this then the raw land costs is less than $25,000 per house. If infrastructure costs is between $100,000 to $200,000 then why are new houses in Auckland the better part of $1million?

Because those that control the market - landowners and developers - price according to what the market can/will pay.

To do that they must have monopolistic type pricing power. There must be restricted competition... Few sellers, many buyers, restrictions on new entrants supplying the market... that sort of thing.... sound familiar?... do we think Auckland Council is doing a good job as the land use market regulator?

Monopolistic pricing power would mean there is a single market owner of all the available land in that 137,000 new/developable sections. That is just is not the case.

Instead, large scale greenfield developers conveniently inflate land prices in unison and set their own development controls by way of covenants to ensure those prices remain inflated through the period of the phased development.

The government has attempted to force them to build a percentage of "low income housing" (typically terraced houses) - to my mind the government would have been better to force a percentage of sections to be sold at cost, plus a reasonable margin, with no covenants attached. In other words, to take the control regarding the build out of the hands of the land developer and into the hands of the section purchaser.

It's is the raw landowners that inflate the price, not always deliberaltly, all they have to do is wait and others will outbid each other to buy it. Some of these people then develop it, but most don't, they are only selling it onto developers.

But this means that already too much has been paid for the land, then councils have their own monopoly in supplying infrastructure. Councils delay bureaucracy is a cost to the developer but is revenue to the council.

Then the sections go to the market in undersupply to be finally bidded up by the buyer to their limit.

The whole system is designed to extract maximum money, irrespective of the quality on offer.

Having no covenants does nothing because most people what some rules to protect the value of their overinflated investment. If there was a market for no covenants, then developers would offer that.

And if there was a benefit to having no covenants, then the $ value of that benefit would be capitalized into the land price so it would not make a difference to the end-users total expenditure. That is what happens when you have a restriction in the system, all the benefit gets captured by the restriction.

You don't understand "monopoly rent". It is not necessary for a single monopolist to control the entire resource. There are widespread misunderstandings of what constitutes “market freedom”. We are constantly told “capitalism has failed” or “privatization has failed” or even that “free markets have failed”, without an understanding of the level of market freedom that actually existed.

Consider a government monopoly of the kind that has existed in many countries — for example, in telecommunications. Supposing the government “privatizes” that monopoly — sells it to willing capitalist buyers. But they retain regulations that perpetuate the monopoly, and the new capitalist owners simply keep price-gouging and offering poor service. This is not a “failure of market capitalism”, it is a market distortion for which government was and still is responsible.

The next potential level of “market freedom” is where the government “licenses” another applicant to “provide competition” to what would otherwise be a monopoly. Now even without collusion between these enterprises, the prices and service levels always remain sub-optimum compared to a market where there is no barrier to new suppliers. There was an economics literature decades ago regarding “monopolistic competition”, which actually held (with strong evidential basis) that even a multitude of “suppliers” who nevertheless held a “license to supply” that was not available to new entrants to the business, would end up providing sub-optimum value for money for consumers.

To be a truly effective “free market”, a market has to have freedom for new entrants to “supply”, and the resources available to these potential new suppliers must be super-abundant. Most resources in the world today are super-abundant. That is, the demand for those resources over a given time period, is only a fraction of what could be supplied in response to higher-price signals. This is the miracle of free markets and trade; nothing short of that would have achieved the same thing.

Urban land is an excellent educational example to learn from. Median multiple 3 housing markets do have freedom for new entrants into the market for supply of land, and relative to the requirement for land for growth, the resource is super-abundant. Saying that there is "competition" therefore growth boundaries can't be the cause of the inflation that commences every time one is imposed, isn't coherent. There is no coherent explanation where some other convenient factor can be blamed that "just happened to coincide with the imposition of a boundary" in every single case everywhere in the world that a boundary got imposed. Of course there can be "proxies for a boundary" which don't disprove the case.

It also makes no sense to blame "developers", as you do, for price escalation, when the biggest killing of all is being made by the original land vendors. If developers are wating for prices to rise to something even higher than what they paid for the land, often this is because they paid too much in the first place to actually make a profit. Development under these conditions is extremely risky for developers; they must out-bid each other for sites in the first instance. It is common for the rate of attrition among developers to be high, cycle after cycle, when there is a housing affordability problem, and this is why. If "house prices" fall ten percent, that means something like a 50 percent fall in the price of the land in projects in progress, which the margins on actual development and construction are in no way capable of covering.

Without these distortions and volatility, developers can get on with competing to make honest money on actually supplying the market, not having to play strategic and gladiatorial games. The development industry in Britain after decades of this kind of planning, has ended up concentrated in the hands of fewer and fewer larger players, with legal departments and political connections. Britain is a case study that economists ignore in their incompetence or dishonesty.

Brilliant explanation.

For a theoretical policy wonk following the machinations of some overseas trending expert.

Ties in exactly from my practical experience

Sez the person trotting out one excuse after the other that does not fit with reality across the full set of historical data. Actually this is a big problem; it is "sun rises in the west" analysis from people who claim to be economists, that is tending to prevail, almost certainly because it suits the agenda of vested interests. The people who are talking sense tend to be marginalized, because all the work for fat commissions requires "conclusions written to order".

I own and have read, several text books on urban economics; but for people who need to be experts on the subject, just one would do: "Economics and Land Use Planning" by Alan W. Evans. Evans is grounded in real life outcomes and the need for "theory" to be able to explain them.

Phil, it seems you decry economic analyses in one argument and then use it in another. I take it you have a preferred economics world view - the one that says that no constraints on development is good; any constraints on development is bad.

We have a similar problem with freshwater pollution - capping cow numbers by soil type/characteristics is the simple, pragmatic solution given our current technology/knowledge. Just as with urban development, in hot spots of congestion, capping new development is the simple, pragmatic solution given the state of our current and aged infrastructure (AKL and WGN in particular).

And moreover, the full set of historical data is in many ways irrelevant. One cannot equate Houston to Auckland. Different topography, different cultural/geographic values, different topography, different capital markets, etc.

In answer to your second question: do we think AC is doing a good job as the land use market regulator, my answer would be no. There was a time when traffic planning findings would be sufficient to refuse consenting of major new developments and/or expansion of existing developments. Clearly, AKLs traffic congestion is just so, so, so bad that few if any new developments should be added. A moritorium on greenfield development in many areas should be in place until roading infrastructure catches up. That, to my mind would equate to good planning.

If greenfields development should not be consented without adequate road capacity, then the whole experiment in intensification should be cancelled, because nothing is creating dire congestion like that does. The road capacity expansion that should be done, is prohibitively expensive because the areas concerned are "built out" and either massive acquisitions and demolitions of property are required, or tunnelling or "overhead" highways.

It is nonsense to assume that mode shift foregoes congestion under conditions of intensification because a significant majority of new residents use cars. You might get "only" 90 percent more cars on the road by doubling density, but what does 90 percent more cars do to congestion? The outcomes are not even merely linear. Flow breakdown makes delays exponential, and then there are tail-backs onto streets that shouldn't even be congested.

The only intensification that makes sense, is "articulated density" or spiky density; very dense home units at specific locations adjacent to obvious major PT routes, and no provision for car ownership at all. Everywhere else should remain low density, sufficient that road flow is sustained. Flow breakdown is such an evil that it does more harm than the gains from mode shift achieved in the process. As long as you can get there at a sensible speed instead of stop-start, there is no net harm compared to our mistaken-assumption approach.

Auckland got several paras in a UN Habitat Program study "Streets as Public Spaces and Drivers of Urban Prosperity" because Auckland is so outlier-low in street space; something like half of the average in first world countries. I don't know how to describe the "story" that we have "overinvested in providing for cars" because it is so utterly false. It may be an assumption "honestly made" but the people making the claim are certainly not basing it on any honest analysis. They believe it because they want to. It is next to impossible to get the UN Report recognized by the agencies that matter - their heads explode and they go right on doing the wrong thing.

The solution (suggested by the brilliant urban economist Alex Anas) is sprawl, properly planned and taking advantage of low land acquisition costs and ease of access for building all infrastructure. It is a dishonest claim that costs are saved by intensification; they are much more expensive in reality because of all the disruption and the very high costs of land and demolitions etc. But the planners are so incompetent that one of the first things you would assume "PLANNERS" would do, is designate corridors and rights of way and public spaces ahead of any development. But they wait until after developers have paid millions of dollars per hectare and then waste bucketloads of ratepayers money "buying space for parks" etc!!! And they ensure that it will be impossible to expand capacity in the future because they insist on structures being crammed on every spare inch of space.

Presumably you also subscribe to the absurd assumption that sprawl means "everyone travelling even further" to their CBD jobs. If employment is not dispersing at the same rate as the population, there is regulatory interference preventing it from happening. Did you read my comment earlier about how clusters form and co-location efficiencies occur?

Intensification simply does not add the big bang numbers that greenfield development does. And I'm sure the planners would love to halt development until such time as they had been able to "designate corridors and rights of way and public spaces" for such development to then/subsequently go ahead.

The argument about sprawl vs intensification isn't the issue - the issue is being able to say no. Something that planning has lost the ability to do under this neoliberal planning regime.

Nonsense. The CRL tunnel is a big-bang number, as are all the tunnels under existing built areas. So are the costs of property acquisitions and demolitions. Then there are the costs of disruption, as we are seeing. Greenfields infrastructure is cheap. It might look like big-bang numbers because massive amounts of new housing and commercial land are being enabled.

You repeatedly miss my point. No-one should have to "wait for designations" made by real planners worthy of the name, the designations should be there already. I can remember properties along certain arterials in new greenfields developments all being substantially "set back" because there was space designated to widen the road to four lanes in the future. This was common practice. There is now hardly a single example of this kind of thing being done anywhere in NZ.

Central Park in New York was designated long before New York city even grew onto that part of Manhattan Island. The street grid for the whole island was designated back when almost the whole island was still farmland. This is "planning". What we have is obstruction and sabotage, not planning at all. Planning, to adjust for potential market failures, should be done to enable markets, not to sabotage them. The market failure that was the main reason for urban planning, was the possibility that private developers would not set aside space for parks, highways, road widening, schools and public facilities, etc. So these things were designated on greenfields decades before the urban fringe even got there. Developers could work around these things, and it made their job easier, not more difficult. "Planning" as it is now, is definitely making their job more difficult and imposing "waiting on planners" on them.

Agree that since the RMA, TLAs have not made use of designations well at all. The utilities companies did a much better job of it. They were much more widely used by planners under the TCPA and earlier.

Here's a good example, where the development was consented as a cart before the horse. In a properly regulated land use market, the Southern Motorway congestion issue would have prevented this development going forward;

https://www.stuff.co.nz/business/property/111994244/paerata-rise-provin…

A large rest home complex would have been a better land use at this point in time, given most of that traffic would have been into Pukekohe, as opposed to AKL.

I disagree that congestion on the roads should be a cost imposed on the property owner by restricting land use The rightful place to impose that cost is on car owners by;

1. Removing car parking minima plue ensuring car parking spaces are priced to prevent car circling to search for a car park.

2. Congestion road pricing ensuring roads are free flowing.

To do this city spatial planning needs to be multi-modal so that people have non driving mobility options.

Oh for goodness sake. People need to get to work and kids need to get to school and shopping for groceries needs to be done. In the absence of more than adequate public transport, people have few choices. Why should car owners be further taxed for completing the necessities of daily living?

Your blinkers that are set on build, build, build - and property owners should have no restrictions whatsoever on doing what they want with their property - totally perplexes me. It was the nirvana line that the RMA effects-based legislation was built on - and look where it got us.

I think what Brendon is talking about is not merely "taxes" but using price signals to help infrastructure provision and the efficient utilization of it. But part of this would have to involve market freedom to "develop elsewhere" if the prices were showing that the existing locations were unable to be furnished with more infrastructure because of the cost of providing it in already built-out locations.

We should REPLACE the existing TAXES with these more efficient market-guiding mechanisms for raising funds.

By the way, road pricing that sustains FLOW is a no-brainer. People imagine drivers being "priced off" but if flow could be maintained at 1400+ vehicles per lane per hour instead of collapsing to 700 because of stop-start, this is the opposite of anyone being "priced off". Rush "hour" could be a lot shorter. The trick is to avoid the spikes in usage that collapse the flow and impose stop-start conditions for the next three hours. Flow collapse is occurring earlier and earlier as more and more people try to "beat the rush". A fee should be set for each time slot, that keeps the demand below the spike level that collapses flow. If hundreds more people get a quicker trip over the two or three hours following flow collapse being averted, that is not "pricing off", that is providing fair value for money in the form of a quicker trip.

price signals to help infrastructure provision and the efficient utilization of it.

More economic theory coming through there. I've heard it all before - alongside the theory that resources should be allocated based on price mechanisms, given the highest bidder is likely to make the highest value use of the resource.

Now consider that economic theory (highest bidder = highest value use) in light of the latest trend of 'ghost houses' and 'land banking'. Terms that did not exist in our vocabulary 30 years ago.

It's only economic theory to you because you have not looked outside of your NZ centric view to observe it happening elsewhere.

And the only reason ghost houses and land banking exist today is because we have created the conditions that support their existence ie non-competitive markets via RUBs as one issue. We have got everything we have planned for.

If the conclusion is there is very little difference in land prices between one side of the RUB line and the other, why have a RUB at all?

I assume the RUB is an attempt to direct capital investment into areas where (some modicum) of infrastructure exists. But the thing is, AKL is at over-capacity and has been for some years now.

When you say over capacity, you are meaning people, not infrastructure?

Next question is, why do they think you need to direct capital? No developers going tp build a subdivision without a road and services to it.

But if that is their reasoning, what it does is automatically signal to the land banking market the next sequence of development by virtue of council monopoly, ie the council wants you to hook onto their infrastructure. So the land quadruples in value and money that would have been available for infrastructure falls into the few private hands.

Many other jurisdictions have very affordable housing by the very reason they don't have RUBs land can't be monopolized and land banked, other private infrastructure providers can also compete with the council and provide more affordable and better quality infrastructure, and they don't need to direct capital to make all this happen.

Too many people for the existing infrastructure.

If land banking of already residentially zoned land is a problem. we should be using land banking to our cities' social advantage via a vacant land tax. Ring fence it for infrastructure replacement and upgrade.

Land banking is mainly on land that is not yet zoned residential but is expected to be in the future.

And yes, they could have a tax but they don't, because those owners have already paid above the competitive supply rate and any vacant land tax would force them to develop even if the market did not allow them to recoup their price.

And of course, this tax is a cost to them but revenue for the council, so council is biased to that end. The general rule of thumb is you don't make things more affordable by adding cost to the system.

If we wanted more affordable housing we would introduce systems that reduce non-value-added costs because of non-competitive markets.

You lost me on the last sentence. Need concrete examples, as opposed to theoretical explanations.

Non-value added - 'A non-value added activity is an action taken that does not increase the worth of what is delivered to the customer. ... For example, a process might include a review or approval step that does not add value to the end product; if this step can be redesigned or eliminated, the efficiency of the organization is enhanced.' So on land, this would be the increased monopoly capital gain value a land banker achieves by just owning and doing nothing with it. If this cost (waste) is removed, then there is a lower input cost but no loss in amenity.

Value-added. 'Value-added products or services are worth more because they have been improved or had something added to them.' IE you buy the land with no rentier price increase, obtain consents in a timely and true value manner, can buy infrastructure services via a competitive market, add your margin, and offer the final developed section to the market at a competitive price.

I'm sure I don't have to define competitive markets to you.

If we were allowed to do this in NZ, then sections would be approx. 1/2 the price they are today. I've run the numbers and it is possible if it was allowed.

And in having some sympathy with you regard to the theoretical language, land economics has its own language, and my background was more practical land development, and it took me a while to get my head around it. But once understood, it helped me understand what I was seeing on a daily development basis and the right from the less right. I mean if people want/like paying more for something than they need to, then all power to them, But if I want the same for less, then I should be allowed to buy that as well.

I would suggest you re-read Phil Hayward's comments, which can be heavy to read because of the subject matter but are 100% correct.

The RUB in Auckland is designed to direct capital investment away from areas with existing infrastructure.

Takanini/Ardmore is adjacent to an electrified rail line, existing bus routes, a core cycleways network, excellent linkage to an up-gradable waste water plant and a 6 lane motorway - therefore AC has it placed outside of the RUB. Huapai/Kumeu is down a 2 lane road, with a railway station that cannot take trains, a half hearted bus service, no good pre-existing linkage for waste water and is much further away - therefore AC places it inside the RUB.

The other point the authors miss is that prices are set at the margin. The last price transacted in a given context sets the floor for the next comparable one. Plus prices for land and houses are notoriously sticky on the downside. A ratchet effect. There's a need for some education in behavioural economics here....

Yes. The way we 'blanket' revalue properties against market prices every three years is a dumb, dumb idea.

Check out the timeline

1, One often-cited study, which estimated the cost of land use regulation under the MUL at up to 56% or $530,000 of the total price of an average property (not land) in Auckland - was undertaken prior to 2016.

2, In late 2016 Auckland almost doubled the amount of land supply available (and did some sketchy stuff).

3, Then Auckland carries out this study of post 2016 data and arrives at a much lower cost.

The sketchy stuff is also important to this study. In late 2016 Auckland created within its RUB a land category called the "large lot" where development is prohibited until at least 2040, this has had the effect of suppressing demand for these sites. So Dr Norman is correct to observe that lifestyle blocks outside the RUB trade at a premium. If you want to purchase a lifestyle property you can purchase inside or outside the RUB, buying inside means a "large lot" with more restrictions and paying much higher rates.

Our work provides a starting point for an informed debate on whether a RUB factor of up to 5.2% is justified given the social costs that may be part of more expansive development that would come with relaxing or removing the RUB.

Those social costs are not "given", the Auckland RUB planning is incompetently bad to such an extent that it causes more pollution than it prevents. If the RUB was expunged the development of Auckland would be substantially more compact, because large areas of land closer to the city than land within the current RUB would be open for development.

Exactly, these social costs that they assume happen, is on the assumption that everyone wants to go to the CBD, so the further away you are then more congestion, use of vehicles getting there, etc.

This does not take into account that many people are forced to the fringe because they can't afford to live closer in, and then there are those that prefer for their own social benefit, not to be near the CBD, and like most Aucklands do not need to go to the CBD for work or leisure.

The report does not explain why Auckland has some of the most unaffordable housing in the developed world. But if it is not the land price as they are suggesting, then what is it? Hint, the very organization he works for.

What is it? We open slathered our residential housing market to all comers - the amount of money laundered via NZ was immense, and it will largely go unreported. But think back a few years ago, the CCP released its 20 most wanted nationals for extradition - and 4 of them were residing here in NZ.

That is a completely different issue, namely the type of oversea investor or immigrant we invite in.

Other jurisdictions have just as high immigration numbers, lower interest rates, and their house prices are only 3x median income.

Their competitive markets, ie no RUBs, actually ensure that new speculator money does not go into real estate because there is no non-value added speculative capital growth.

Any asset growth comes about by actually adding value to a development which has still to be competitively priced (because of more potential competitors). This only attracts professional longer-term property investors.

There is such a thing as institutional settings that can cope with any amount of population growth, immigration, cheap money, and even money laundering. Some of the median-multiple-3 housing markets in the USA have grown even faster than Auckland, including from immigrants. The cheap money and the dirty money looking for a haven get soaked up by the infrastructure bond market and actual new houses get built downstream from the funding stream for new infrastructure. It is like a completely different world. Everything merely turns into "economies of scale" instead of zero-sum price inflation. Fortunately some experts in NZ have studied this and have "got it". Institutions that send study tours to places like Britain and Oregon to "learn how it's done" just aren't even interested in anything but perpetuating the racket. It's like sending a study tour on "Democracy" to North Korea instead of Switzerland. If you want to study housing supply, study somewhere that supplies a lot of housing in response to demand, not somewhere that fails to.

There is a very interesting calculation by Saiz and colleagues, of "housing supply elasticity" by city in the US, where "1" represents elasticity that at least matches demand. The problem cities score below 1. But the median-multiple 3 cities score a wide range of levels above "1", some of them going over "4". That is, their supply is so elastic that it is four times as fast as it needs to be to sustain price stability. It is entirely typical that after an identifiable "shock" like an interest rate cut, the number of new houses being supplied is higher within FOUR WEEKS. That is a "market" responding. In the most dysfunctional markets, there is no identifiable pattern of relationship between demand shocks, and supply. There is no incentive at all for developers with sites, to attempt to capture customers before some competitor does.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.