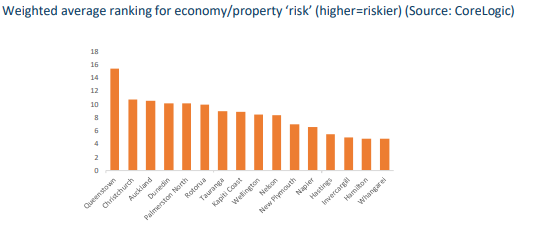

Queenstown, Christchurch and Auckland could be the centres most at risk from a property downturn in a post-lockdown recession, while Invercargill, Hamilton and Whangarei may be the least riskiest centres, according to property data company CoreLogic.

The company considered four risk factors that could impact on how property markets in 16 cities throughout the country might be affected in a downturn, and then applied a weighted average to rank them from highest to lowest risk.

The four risk factors CoreLogic considered were how much of a contribution the accommodation and food services sectors contributed to each centre's economy, the recent percentage total of property purchases in each area by investors compared to the long term average, the percentage of all dwellings in each area that were listed on short term accommodation website Airbnb, and the percentage of total guest nights in each area that was due to international visitors.

Perhaps not surprisingly, Queenstown's property market was seen as most at risk from a downturn, by a considerable margin over other centres.

It was followed by Christchurch, Auckland, Dunedin, Palmerston North and Rotorua, which were the other higher risk centres in the rankings.

In the middle with moderate levels of risk were Tauranga, Kapiti Coast, Wellington, Nelson, New Plymouth and Napier, while the lowest risk centres were Hastings, Invercargill, Hamilton and Whangarei (see graph below for the rankings).

"Queenstown doesn't look good on this system and that supports the popular perception amongst commentators that its property market could be in for some major problems." CoreLogic said in its report.

"Rotorua is another candidate often suggested as being vulnerable, but on our measure it doesn't look any worse than some other parts of the country such as Christchurch, Auckland and Dunedin."

That's because Rotorua is not entirely dependent on tourism and had other industries underpinning its economy, the report said.

"Elsewhere, most of the main centres and a number of other main urban areas look to be on a par in terms of their vulnerability to a property market downturn, but Invercargill, Hamilton and Whangarei stand out as more resilient property markets in our basic weightings system."

CoreLogic admitted its rankings weren't an exact science and said other factors would also affect property markets in each area.

However the factors it had looked at would likely have a substantial impact on the property market's performance in a downturn.

.You can read CoreLogic's full report here.

The comment stream on this story is now closed.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

269 Comments

That's not what the ONE ROOF sponsored NZ propaganda Herald thinks.

You couldn't make the headline any more ridiculous unless you said "Post nuclear apocalypse, NZ house prices may be steady". What a joke that paper has become.

https://www.nzherald.co.nz/property/news/article.cfm?c_id=8&objectid=12…

The employment damage from the GFC was quite narrowly and intensely focused. The damage this time is much wider.

The 'recovery' will also be vastly different. Unlike post GFC we don't have the ability to make large and repeated cuts to the OCR, unless we go way negative (a possibility but a remote one).

I expect once we hit the bottom of prices there will be flat or only minor growth each year for many years.

So much for 'double every 10 years'.

This is the kind of content that Granny Herald relies on to be a going concern.

One Roof is clearly of the LOB school of forecasting (Always look on the bright side of life).

That's because it's effectively sponsored posts by real estate firms. The Herald's biggest advertisers write what they want.

Would be interested in thoughts on the journalistic integrity of this.

For me, OneRoof is not clearly delineated from the rest of the Herald's content. Sure it's got 'OneRoof' branding, but...

I don't think the herald has any thoughts about "journalistic integrity".

The Herald thinks integrity is a type of Honda

The NZ Herald paywalls all of its "premium" content. On a Saturday, nearly 80% of all articles are paywalled

Except One Roof - have yet to see a One Roof article paywalled

Yeah, but I bet half of NZ Herald Premium articles will be about Harry and Meghan.. opinions from Mike Hoskings and his missus..!

It concerns me that someone like Mike Hosking has free reign to extoll his obvious bias unfettered.His radio show doesn't take callers,so can't take him to task,he is all over the Herald as well, expressing his views as if they are fact,with no right of reply.

His total disrespect for this elected government is obvious and he is so hypocrytical with some of his rants.

The other day he was going on about how poor the rest of the media is compared to him,he complained about the using the term 'liquor barons' in a story,saying it was just emotive language showing bias against rich people.Then every day he uses terms like 'that lot' for the government,Jacinda,Aunty Jacinda,Taxinda,apparatchiks etc,then when he refers to others its Simon Bridges,The National Party,always trying to drag out some has been from the past to support his theories.He asked the gentleman who is looking into the legality of the lockdown various questions,Mikey was ebullient as he started talki g,but when the legal expert disagreed that the govt could be taken to court for financial losses,as it was done in good faith and that he was looking at it from more of a academic & future policy angle,Mikeys mood changed and he quickly ended the interview.

It's a shame no one is given the opportunity ask Mikey some difficult questions.

The "host's" delivery is a bit painful but it shows up Hosking's hypocrisy brilliantly and is quite funny... https://youtu.be/vyNds3DIbd4

That is brilliant,thank you to both of you for sharing...I'd love to see that go viral,that is one virus I want everyone exposed to lol...

Ha ha that's gold. Hosking's a politically biased intolerable know-it-all. In his defense though, the correct course of action has changed as the understanding of the virus has changed. Initially it was though that the CFR=1-5% and R0=4-7. Now we know that the CFR=0.1-0.4% and countries like Taiwan and South Korea have taught us that the R0 can be lowered right down by, among other measures, wearing masks in public. Unknowns remain like ADE and long term health effects. I wouldn't be so critical of the government when my own opinion of the virus has changed.

This is the only Mike Hosking I've watched or heard in about 5 years.

https://www.youtube.com/watch?v=vyNds3DIbd4

(edit - that's not correct, made sure I watched his first night on 7 sharp or whatever it is he does at 7pm, never has their been a face so sour, Caroline Robinson was sitting beside him and literally struggling to contain her glee, it was a thing of beauty)

I have disliked him forever. However, occasionally (maybe 25% of the time) I would find myself nodding in agreement to his views.

Disturbingly, I find myself agreeing to most of his columns now, re: his criticisms of the government. But I am an open-minded enough person to just go with that, and not bear grudges.

In a ridiculously fawning media, we need Hosking right now.

To be fair Mike Hosking does state it the way it is, without beating around the bush.

Current journalists that put questions to Ardern are pathetically soft!

"states it the way it is, without beating around the bush" = "confirms all my factually incorrect beliefs, while being a smug d*ckhead towards people who know science and maths"

To be really fair he tells it the way he sees it.

Did you not see the link above,the way he sees it changes regularly.

He had some opinion this morning that if property went down by 15% it would only be back down to last years levels lol.

Here's Mike telling it as it is, saying the amount of people died here is laughably small.... im not sure its anything worth laughing over, regardless how small.

https://www.newstalkzb.co.nz/on-air/mike-hosking-breakfast/video/mikes-…

The no.of deceased at 21 and all elderly with issues is pretty low when you realise that there is generally around 700 plus people die each and every week in NZ and therefore nearly 5000 over 7 weeks and yet nothing is said about this!

Nothing needs to be said about it because people who passed 6th form maths understand why it's a non sequitur.

https://www.rnz.co.nz/national/programmes/mediawatch/audio/2018741210/m…

See above for the many hypocritical positions he takes. Regardless the disrespect shown to Labour politicians by MSM is mind boggling. You tube how they fawned over Key, never asking the obvious questions, never stopping him and saying "that's not right PM" when told an obvious lie.

Re MH he has such an obvious Nat party bias as per all msm I suspect theres a bit of folding involved as per the Sky City rumble that was disclosed. This bias will rear its head again at election time if he comperes a debate. Funningly enough at the last election I think he did very well, pulling Farmer up on a couple of obvious bending of the facts. I believe he felt that there had been such a groundswell of dislike to his bias he had better drag it in for a while on the big gigs.

Yep lots of historical revisionism going on in these comments lately. I lost count of the times Key got away with easily disprovable casual lies but suddenly the Nats are watchdogs for government accountability.

As for the Hosk, did you see this one: https://www.youtube.com/watch?v=RP2S-IzLoWo

Very droll is that you sl

When you deregulate the f-k out of media ownership this is the logical endpoint.

Hosking wears lifters

"yet to see a One Roof article paywalled"

Just because both NZ Herald and OneRoof are owned by the same group of companies, they serve entirely different purposes. People should avoid confusing the two. OneRoof has a different revenue model from NZ Herald:

1) NZ Herald is subscription and advertising revenues

2) OneRoof is attempting to compete with Trademe.co.nz, Realestate.co.nz on property listings for sale. OneRoof's revenue model is based on properties for sale listing revenues (like its competitors). They will unlikely paywall the site as they want to attract a larger audience of potential property buyers for their property listings.

Everyone should consider OneRoof as a property for sale listing website first and foremost, with property marketing, property sales, property promotional material. (need the audience to believe that property prices are going up to entice buyers to buy. Fewer people are likely to buy if property prices are expected to fall)

OneRoof is an property focused advertorial website. No independent viewpoint whatsoever on real estate. CAVEAT EMPTOR.

Here is the disclaimer from OneRoof

"This Platform has been developed in an effort to help you make your property decisions easier. However, in presenting you with available properties from Real Estate Agents and other service providers and listers (together, “Agents”), OneRoof is not recommending that you choose a particular property or Agent– it is a platform to facilitate engagement between independent third parties."

In the short term, we could not be in a more deflationary environment for property. Soon to be large scale unemployment, mortgage holidays end in September, low migration, consumer confidence way down & no room to move on the OCR (which has been a key driver for property price inflation since 2008). It's going to depend on how many people need to sell, or if they can do what they generally do in a downturn, hold/stay put.

In the long term, we're going to either have to pay back the $ we borrowed, or undertake QE to make the kiwi peso more worthless. Which would be inflationary for assets.

Hate to be a central banker right now. Nightmare.

Loads of room on OCR, -2% by July.

Really?

Sure it's a possibility but it hasn't seemed like there is a huge amount of enthusiasm for it.

I think there's a better than even chance, it's the least costly way to shock the economy back into life.

Michael Reddell advocates for it, but if I have read him correctly he thinks it's quite unlikely.

Yeah because negative rates have worked so well everywhere else they've been tried.

How do you know they haven't worked? (don't quote the recent articles on Sweden)

Okay in which country with negative rates has the economy been "shocked back into life"?

There is a wealth of empirical evidence that lower interest rates stimulates the economy, ergo deeply negative rates will stimulate the economy. No one has gone deeply negative yet. Happy now?

You're talking about empirical data on lowering one positive rate to another positive rate. I'm talking about negative rates. It's not that simple because the relationship between rates and inflation is non-linear. It's not like

2% to 1% --> X inflation, therefore

0% to -1% --> also X inflation

https://www.youtube.com/watch?v=HmM01J-nrno - 0:00 through to 5:20 (there's even a dig at Millenials in there for ya)

I'm not saying he's right, just saying there is really no reason to assume negative rates will do what you're expecting them to do.

My brother lives in Sweden, he bought a house there in 2016. Probably the only reason he could afford it was because of their basement bargain interest rates.

Always made me quite jealous.

The banks computers don't have a minus sign on their keyboard apparently, according to Mr Orr.

The Herald has become unreadable. They clearly have an agenda, and not just with houses.

Dare I say Stuff has more credibility now.

I thought I used to like Simon Wilson but I'm not so sure now. I like the place he's coming from, but his writing is quite waffly and I'm not always sure how robust it is.

Matthew Hooton's articles are great.

Maybe I am turning to the dark side?

The thing with Hooton is that he is very clever, and usually quite balanced and non-partisan. In terms of the latter, I've found he's improved a lot over the last few years. He's clearly of the right, but that world view does not dominate his writing - it certainly strongly informs it.

Yes that's right, there are still some good journalists amongst them, and I don't mean to run them down. It's just the overall tone of the site, is more a kin to a gossip mag now. It's seems to be only interested in clicks and content quality and journalistic integrity be damned.

Completely agree on Hooton - he's definately become a hell of a lot more balanced then he used to be. As a result, his articles are now great.

newsroom is preferable to stuff or nanny H

What I like about Hooton is that he is actually right wing and is against corporate welfare

I don't read 99% of Stuff articles when they're free, so what hope of implementing a paywall? The general day to day journalism makes the Daily Mail look like it's written by Ernest Hemmingway.

Totally agree on NZH, trash bag! They call themselves Journalist, they are not better than trash bloggers or Twitter commentators

May be this is what Trump refers to Fake News

Puts me off subscribing

Usual suspects of the housing lobby on that video, just missing some Ashley and Tony guys, they must have been busy making sound investments.

Haha very good . Ashley has no property credentials whatsoever to promote himself as an expert on the subject

"Ashley has no property credentials whatsoever to promote himself as an expert on the subject"

FYI, Ashley has property industry experience, yet no formal property qualifications.

His work experience is in the area of sales, property industry promoter. Certainly no formal property valuation qualifications. No formal qualifications beyond School Certificate from what I can determine.

Ashley has been high visible in the media, as a property market commentator, property price forecaster. Even though he has been allowed to espouse his thoughts on platforms with large audiences (such as national television), it does not make him an expert on property valuations. Remember people should not confuse a bull market with genius.

1) work experience: https://www.linkedin.com/in/ashleychurchnz/

2) formal education / qualifications - "My formal education never progressed beyond School Certificate at Tamatea High School" - https://www.oneroof.co.nz/news/ashley-church-do-you-need-to-be-born-ric…

FYI, here is his website - https://ashleychurch.com/

Gee bloody boring interviews, sounds rehearsed. And this from one who would usually enjoy such discussions.

After growing up in Whangarei, I can vouch for the fact that there are some lovely homes and there used to be some real value for your dollar in the city. However, as the bubble became the primary focus of the NZ economy, many of those homes have commanded hefty price tags. Nowhere near as ridiculous at Auckland (where banks have taken things to a whole new level of stupidity), but Whangarei is not necessarily "cheap". Furthermore, if you were able to benchmark prices against the income levels of the locals, it would not surprise if the place were as bad as anywhere in terms of overpriced property and value for money.

It would also not surprise me if Whangarei is whacked as badly as anywhere else. Anything I see from Corelogic I expect to be overstated on the way up and understated on the way down.

Yeah I was a little surprised by that. They look too bullish on regional cities.

Tauranga and New Plymouth to be included in high risk centres.

Thought the ban on gas exploration had kept New Plymouth a bit quieter during the last few years, so less downside.

Thats on new extraction, the current licences are still operating so in the short-medium term there has been plenty of growth potential in the region. However, covid has dumped cold water on the energy industry and many that work in it are feeling it big time.

Don't forget Hawkes Bay. One of the lowest avg. income by region, many are reliant on international visitors (wine, high-end restaurants, tours etc.)

Apparently a lot of hot money from Auckland too, some of which may reverse.

Yes and it's that massive over pricing of property in regional areas that will prevent them from recovering, since the locals are sure they can squeeze out the million bucks retirement fund out of a basic property that they bought less then 5 or 10 years ago.

See if no wage earner can afford to live there, then who is going to setup a business and rebuild the economy? And don't say Overseas Investors from Asia, we all know that's a false economy. They'll just asset strip and leave their properties empty, hollowing out our economy in the long term.

Hollowing out is the master skill of the COL as they hollow out rural communities. The tree planting looks like it will be a major disaster

Whangarei and indeed Northland will only grow economically once there's a 4 lane highway connecting it with Auckland.

Time to setup some companies to mass purchase.

Once in a life time opportunity.

Black swans are no longer an endangered species.

Chinabot predicting CCP grab for control of more of NZ? I await Ximon Bridges advice on how we should proceed.

What's the problem? We give them our water for free?

I have never understood why NZ's right claims great upset over oil and gas yet wishes to give away other natural resources for free. Donations?

I agree, I only point out the contradiction. I have never understood why people claim great upset when cunning individuals take advantage of our relaxed approach to foreign ownership of strategic assets - houses included. If we're open for business, don't be complaining when people buy the merchandise.

Its because NZ has always had ample freshwater so we don't value it the way we should. Only once it dries up will we realise how valuable it is.

V perspicacious.

And they get paid for these sage-like deductions.

Meanwhile they are making out that market won't fall (ie prices and sales) and not get back to prev levels for years

Not independent I am afraid. If need advertising, not independent

mike

Wot are you on about????

Core Logic is not a real estate company, nor does it have a vested interest in seeing properties either falling or rising, nor in need of advertising which compromises their position.

"Not independent" - utter rubbish.

The are an independent company (formerly part of the government's Valuations' Department) who simply track property prices, and in doing so are contracted to provide independent information to councils on RVs.

They also provide valuations for buyers and sellers - and as valuers can not have any vested interest.

"They are making out that market won't fall" - nowhere is this asserted. Read the document - the opening sentence is "In the coming months, all parts of the country are likely to feel some degree of property pain".

Core logic appears to be now part of the propaganda problem I am afraid.

They exist by selling valuations to various parties, they certainly do have an interest in rising house prices, and maintaining housing sales volume. When prices are falling how many people are going to be asking for new valuations to extend the mortgage and buy a new boat/car/whatever? Last thing most people will be interested in doing is putting a new lower valuation in front of their bank manager.

Corelogic's core business is corporate - including banks, insurers and developers. These parties want valuations in a falling market. For the exact same reason private owners don't.

And they have major shareholders blackrock and vanguard capital. Got to be mindful of those American pensions.

You omitted real estate agencies for some reason.. falling values, and falling volumes of sales are bad for corelogics bottom line.. that is the crux of the argument.

Not independent: where do you think they get funding?

I have paid for many valuations done on properties over the last 40 years. Not once have I felt I was given a "low" valuation because that is what I wanted, or a "high" one for the same reason. Each and every time I feel the valuers have applied their formulas and come up with a valuation based on those rather than on what the client, being me, wanted. Which of course is what I want really. I suspect others have had experiences with dodgy valuers, rather than the honest ones I use.

Sit23

Agree with you; valuers need to provide unbiased and justified valuations. To provide a biased valuation leaves themselves to being sued and stuck off. Yes, there has been instances of “dodgy” valuers - where known they have been likely prosecuted and struck of.

Printer8

Like any professional discipline, there's 'unbiased' and then there's 'unbiased'.

I've seen it all my career, among engineers, architects, planners, valuers etc etc.

Most of the time professionals will seek to provide the 'right' answer for their client, in a way that still appears credible and unbiased. But which still does actually have some bias.

That's simply how the world works.

Mike

They get their funding as they are contracted by councils to provide RVs.

They also get their funding by providing private valuations.

As valuers - a professional role controlled by a legally enforced code of ethics - they must be independent and free of any influence.

To suggest that they are anything but independent is a baseless slur. They are required to retain registration to practice as a valuer - just like most professionals such as lawyers, teachers, engineers . . .

You clearly do not understand the role of valuers.

Interesting to note that the directors for Corelogic are listed as being from Australia and California on the companies register. Not that this rules out any conflicts of interest but does suggest higher likelihood of being unbiased.

Nzdan

What is your justification for that suggestion?

And the directors job is to return maximum value for the owners.. not sure how the fact they are American/Australian makes much difference?

The implicit bias of virtually all in RE world and living off its scraps I am afraid is:

Prices up good, prices down bad.Plus everything is always getting better and will be more so in 3, 6 and 12 months.

A perspective that only sees increase and never decline is not one I can give respect to, because it ignores cycles.

They are half owned by an American data collecting entity doing their best to control NZ property information

You are wide of the mark. Core Logic do not carry out professional independent valuations by registered valuers . They carry out online assessments they choose to confuse and validate by naming valuations . Quotable Value carry out valuations by valuers but then I understand they are half owned by Core Logic which is another matter in itself

Just when you thought Christchurch couldn't get any cheaper?

Don't be silly, TM2 assures me Christchurch is on the up.

Yep as reported Christchurch is on the up with skinheads hassling Asians about Convid-19

Bring it on!

Any bargains and I will be Buying if people are fearful.

Look forward to 10% returns when I can get money at 3%, great opportunities!

Yesterday there was an article forecasting a 5.49% percent drop here there and everywhere. I thought that quoting to 2 decimal places was hysterical.

When I hear that the BOE has this as looking like the biggest recession ( ?? surely depression) since the Great Frost in the 1700s I really believe there could easily be 2 figures before the decimal point and the first won't be 1.

After the decimal pt -who gives a stuff?

If one is going to be wildly wrong it's important one does so with precision.

Lots of opportunities to buy well under true market value for those who know how to use debt wisely!!!!

(Edit: Oh god I didn't even see his comment above before I posted this, his self-parody is better than my parody.)

In a significant recession the locations with the biggest separation in prices to incomes will have the biggest risk exposure. Add in where speculation was accelerated with factors outside the normal economy, and you have a MASSIVE risk exposure for sure. Awk foreign cash and loose lending bubble, CHCH earthquake cash bubble, and Queenstown (see Awk). I would add Taupo, Rotorua, Wanaka into those category as their main source of commercial income is dead. The massive layoffs that are happening in the big operators already underline this. Then consider Kiwi/Aussie holiday houses, do you sell the holiday home, or do you sell the family home where hopefully your job still is?

Those with protected income and a pile of vulture fund cash are going to do well, very well. Those leveraged up the a**, and experiencing or facing loss of jobs/income, you are, or are about to be the contact patch where "the rubber hits the road".

Bring it on, it is about time the conservative were rewarded and the wasteful over leverage brigade finally learn that leverage can work in both directions.

It's amazing that none of the spruikers have acknowledged that literally ALL of the supposed growth drivers they kept citing just disappeared from the market all at the same time. They have jettisoned any attempt to rationalise the bubble and are now just openly running on pure delusion.

What percentage of total NZ properties does Auckland, Christchurch, Dunedin and Queenstown make up?

By what measure?

Population wise, about 44%.

Residential dwellings by count, probably a little lower (guess 40%?) due to higher than average occupancy.

Housing $ value.... I'd say over 50%, maybe 60%?

Food and accommodation biggest weighting!?

Because in a recession people stop eating and no longer require shelter?!

Macca's did 4 weeks worth of business in first week re-opened - so yes, food sales dead for 4 weeks, but the bounce-back has been dramatic. Can you say the same for tourism? No. Rotorua and Queenstown are stuffed - Rotorua's small population doesn't have bugger all professional services unless you are classifying the local gangs as professionals??

Good to have overseas hotel nights and Airbnb considered - but appears this isn't weighted as high as a general 'food and accommodation' category as this area, along with 'overseas tourism' is the one that is dead and buried long term, not food.

Investor impact is also questionable as negative sentiment and bank lending standards will impact owner occupiers just as much if not more (I know many who have cash ready and waiting, and we don't buy on feelings we buy on numbers, 2.99% rates making the numbers better as of today).

You miss the whole point of these resets. Rotorua and Q'town are not "stuffed", we will just have to adjust to the new normals of the next few years, whatever those are. Maybe the new normal will mean that beneficiaries will be able to afford rent in QT, which has not been the case for many years. Businesses will force the people they deal with to lower their prices so they can afford to provide goods and services to the new market. Some will do so, some will go broke. That's life.

The tragedy of all of this is - we brought it on ourselves. (as did other countries)

It has been blindly obvious for decades that we have priced housing out of the equation for many ew Zealanders - unless they took on ever more debt. ( tie up more and more of their future earning and spending capacity)

Regardless of what happens now to nominal prices, the biggest question is:

"What do we do about it?"

Do we 'stimulate' the property market back into life and continue to load Kiwis up on increasing amounts of debt?

Or do we bit-the-bullet this time, and set about rebalancing our property market and society?

My suggestion is that the 'more debt' scenario has overshot it's capability, and Covid19 has been the final nail in that coffin.

But one never knows!

We'll all be the wiser in a year or two's time. The other big question is:

"Do current distressed owners ( and their bankers) have the amount of time available to them to 'ride out the storm'?"

I doubt they do.

Agreed. Many have brought into endless debt, but many haven't. When those that havent attempt to point out the risks, they get berated and attacked on this site as negative. Bottom line without endless price appreciation the math/risk balance hasn't stood up for some time. Personally I'm in favor of an Icelandic like reset.The Govt has the ability to make this happen, or to just continue to protect bank profits by doing all to maintain the asset bubble through more and more debt. So far it looks like the second option thru lower and lower interest rates and elimination of the minimum equity requirement.

Will be interesting to see what, and should make for a very interesting election. Save the banks/speculators vs. save tax paying kiwis. Pretty sure the latter is actually the Govts job, but like Nat's, you never know.

So true. TM2 berated me on here last year because I bought a home without needing a mortgage. He was appalled that I hadn't utilised my capital by leveraging up or buying sooner. The way he spoke on the topic was as if to infer that there was no risk at all in taking on debt.

Take out big mortgages in a city that is built on mud that shakes alot. What could possibly go wrong?

Ginger, there is no risk at all with taking on debt if it is profit making debt.

When you are averaging 10% return and 3% money borrowed and fully tenanted properties, anyone should be able to work it out that it is a very profitable exercise.

Let your equity work for you, it is the ones that have invested in wrong business that will be feeling it.

The Man has been stating this for years.

TM2

1) "there is no risk at all with taking on debt if it is profit making debt."

That is the same assumption that many highly leveraged property investors made.

2) "When you are averaging 10% return and 3% money borrowed and fully tenanted properties, anyone should be able to work it out that it is a very profitable exercise."

That is the same assumption many highly leveraged property investors made. What happens if the underlying assumption(s) is incorrect? (can you identify the underlying assumption that has caught out many highly leveraged property investors this time?)

CN, I would suggest to you that if investors were highly leveraged on their properties, that they would not be profitable especially in Auckland.

If you buy permanent material property well that are returning you in excess of 6% and under market value then you won’t go wrong.

If you are paying too much in say Auckland for $700k and getting $500 per week then you are not buying well enough to make it worthwhile.

Example bought a 5 bedroom plus self contained sleep out 3 of years ago for $380k and it returns $595 per week so 8% gross return.

We have a commercial property that returns 15% net return on purchase price.

I have maintained over many years that I generally wouldn’t be touching anything that couldn’t return 6% per annum gross.

Investing is about profit and return and the capital gain on paper takes care of itself.

Folks, have you ever looked at a chart of the 1929 stock market, or the Japan Bubble, or the Tech Bubble, or Spain, Ireland, US etc housing market bubbles and said to yourself, "How the f-k did anyone rationalise buying at the peak of this thing?"

^ This guy.

I would not trade places with someone who is highly leveraged right now, thanks!

"There is no risk at all with taking on debt if it is profit making debt".......... WOW JUST WOW! I am left speechless by the naivety of this comment.

NZ's new normal ?

That's the origin story of my username

The Man is a total crack up! Surely must be a parody profile?

This is how he "buys under true market value".

I suspect that the printing press will be rolled out and we will attempt to inflate the debt away as our currency slides to oblivion. Of course this will also inflate away savings and result in lower standards of living.

But the piper must be paid one way or another

The real estate market will rebound and probably quite well. Reason being all the printed money has got to go somewhere. They key of course is remaining tension from under-supply

Then what?

"Do current distressed owners ( and their bankers) have the amount of time available to them to 'ride out the storm'?"

That is the key question. Answer depends on

1) is the household experiencing difficulty meeting debt repayments? - these statistics show up in the number that have requested mortgage payment deferrals (as an indication of cashflow stress). There are currently over 105,000 applications with a total loan amount of $37.1bn outstanding.

The key one is those that are unable to even pay interest only, and have deferred all their mortgage payments (52,691 as at May 8 with loans of $19 bn outstanding - https://www.nzba.org.nz/consumer-information/covid-19/consumer-lending-…)

2) how many of the above households will continue to experience cashflow stress after the mortgage payment deferral period ends and payments normalise?

3) what is the LVR on the property? If the LVR is high and the borrower is unable to meet normalised debt payments, then some action may be required by the bank.

Agree - those are the key figures to watch.

More unemployment/government income cover and it could only get worse.

The rate of recovery of the economy is also a variable to monitor. The slower the economic recovery, then the higher the probability that unemployment rate remains high, causing more highly leveraged borrowers to face financial stress.

But if you are caring landlord and buying in CHCH below market value, then rent them out to professional tenants with a stable income. You'll be sweet!

Hello, TM2!

With interest rates below 3 and LVRs gone it's better to buy than rent and Chch house prices are good value. Renting longterm in chch is like putting a match to your money when you could so easily afford to BUY the same home for less than the cost of rent. Probably deserve to be taken advantage of.

Yeah right, because everyone has $100k lying in the bank doing nothing. Bloody idiot poor people, why don't they buy a house?

"Probably deserve to be taken advantage of."

Theeere's the social Darwinism. Knew it was in there somewhere.

You forgot to describe him as a caring "professional" landlord CM. I warned him constantly but he says he kept buying instead. He knows better than anyone in New Zealand and of course property is different as you are in complete control compared to equities. That would be one of his most naive comments to date.

In all seriousness, I think TM is a RE Agent.. Just got the right sorts of vibe of being one, That's all.

he reminds me of another poster here "Chris CJ" he came and looked at our house a few years ago when we were moving to Brisbane.

Or TTP.

I think you are right, TM2 is an agent.

TTP it turns out is very wealthy and successful. He's the Managing Director of Property Brokers. He's been an REA since the 80s.

So only knows falling interest rates and rising values.

Yeah but in his defence, it would cause an almighty confirmation/recency bias after all that time, wouldn't it?

We don't 'really' know how wealthy he is.

Ha. Okay. Fair point, you can never know. But he appears to have donated quite a lot of money to charity over the years so that suggests he's comfortable. But I guess maybe he's not? His business has 700+ staff and he has built that himself over several decades, so whatever my own reservations are, i'm inclined to think he's achieved some success.

He definitely has a very clear bias on property though so he's been quite naughty and disingenuous on here over the years. But equally, we're all mostly anonymous so that might be the norm?

Judging how much TTP desperately tried to bully people on this site including me when they pointed out stagnating property prices, So logically he's up to his eye balls in debt. And hats off to you Ginger for outing him. ;)

He really looks like a bully too.

This quote explains why most property promoters, real estate agents, property mentors, property industry participants etc have difficulty seeing the opposite to their beliefs

'Most good sales people believe their own baloney' - Warren Buffett

TTP should be ashamed, where are you TTP? Tumblewwweeeeed

If that's true, he is also a pathological liar. He stated many times that he doesn't own a house, as he was still saving up money for a deposit.

I referred to him as Tim the other day and then he wrote back and signed off as Tim, so from my perspective he confirmed.

But yes, he did say that he couldn't afford to buy a house. So he may have been winding us all up the whole time. I shall wait and see if he has an explanation because I have heard from several people that they have met Tim Morduant and that he is a very good person, so I am trying to stay neutral.

TTP has also done his share of mudslinging. And I won't deny that some of the comments here get heated and even nasty sometimes, but I think a lot of people have been guilty of that too.

He has also said several times he doesn't live in Palmy. Which might be true, maybe he lives in a lovely lifestyle locale nearby like the delightful Feilding.

Re TTP: He's just an REA and an unsuccessful one at that.

No, if TTP is indeed who we think he is, he lives in Palmy, Nice house, tennis court and pool on ~2/3 acre. Bought for $600k under RV back in 2013.

So either he's not who we think he is, or he's a liar. I'll leave that call up to you.

He might be a she

You can identify as anything you want these days. Today I choose to identify as a pineapple.

Yes I have said previously I was a sales person for many years!

Rentals are a far more profitable business for us without the stress and it gives us the freedom to do what we want when we want.

When you are a real estate sales person you are only as good as your last sale.

With our portfolio of properties, the rent comes in week in and week out without us being around.

Yep that explains the BS!!!!!

Yeah we know you were a "REA sales person" The Boy 2, your mate Gordon (nice chap) outed you a while back.

Just quietly, I think he still is.

Na, don’t need to be!

Came back to Dunedin last September absolutely stunned and disgusted by the price of houses here and the lack of well paid jobs.

All my family and friends kept saying it will only get worst, it can never go down so we got pre-approved and have been looking since. I thank my lucky stars we didn't buy one before the music stopped.

I have noticed a lot of the houses on the market now are the ones that were sold in the last year - speculators getting out. Already seeing lots of 300-400ks appearing which there were none of prior to March.

I will start looking again after September, but I feel like a weight has been lifted from our family's shoulders. We no longer need to take on a life-time of debt and we will enjoy many more memorable experiences with the extra money and time that we save. Fantastic news for first home buyers.

Nice one. Patience will definitely pay dividends for you, and not the bank this year. Good luck.

..........and the parasitic spruikers will call you a DGM..... Go figure?

A lot of tradies packed up and went to Q-town for the big bucks. Guessing they will be heading back to Dunners and looking for rentals as their Q'town house has devalued a lot.

The clifftop has been found :)

Dunedin did become too expensive for what you were getting when you compared it to Christchurch.

How is that eye patch TM2?

Glad to hear that, it did become unreal. I have seen a lot of young Dunedin couples move to Christchurch to get into the property market. Dunedin cannot afford to lose even more of its young adults. See winners and loser through the lock down however those still in a position to buy property are still going ahead..not interested in waiting, shows how much of a emotional choice it is.

It is plain as day light that the houses lost a significant amount of their economic value when it became clear that COVID 19 is a global pandemic. However, how the house prices in NZD (as opposed to their already reduced value) will behave in monetary terms, largely depends on the actions of the RBNZ and NZ Government. If the increase in money printing going on continues, NZD will be devalued. If capital flow restrictions are introduced (as already contemplated by some), this will devalue bonds and holder of debts will try to convert it to something other than the worthless paper.

You will then have economic depression with Monterey inflation. So you have a house that you cannot sell, as effective demand is all but gone, but it monetary price holds up because NZD is losing its value.

Actually the RBNZ printing wont devalue the NZD because almost all other major currencies will be printing and devaluing at the same time haha therefore no one is actually devaluing

Yeah, the whole "floating currency" solution only really works when the whole world isn't fuc%&d at the same time.

Ninja...mind your language. There are men present on this site :)

Bahaha. Yes, no vulgar language around the penises. I wouldn't want to frighten them.

Too many vinos GN. Just quietly I am well on the way....

Sssshhhhhhhhhhhhhhhhh

They are very easily startled

It might not devalue it against other currencies. but it does devalue it in terms of anything denominated in NZD, unless there is external demand for NZD (i mean by parties outside NZ) greater than the money being printed (e.g. Europe, China, Australia where ever is willing to get NZ bonds and given us goods and services).

Yeah but the current printing of NZD is still only just filling a hole to replace all the NZD that is no longer being created via productivity or services and the NZD that will disappear because of debt defaults and bankruptcies. There will be such overwhelming deflationary pressures across NZ that the devalued NZD will still probably buy more in the shorter term than it did last year, things will be priced to sell. Inflation expectations are falling and the demand just won't be there for anything.

That is true. I.e. if total money printed is less than total money destroyed, then you will end up with less NZD than before printing. But when large scale bankruptcies happen, the RBNZ is very likely to come to the rescue of the banks (and their savers) by increasing the velocity of money printing.

Under this scenario you end of with a real deflationary economy (real activities and supply down, real demand down etc) but money in circulation is greater than before. This excess money will end up somewhere eventually. Economic deflation coupled with monetary inflation.

Yup. This is my best guess too. But I think the monetary inflation will take awhile because the scale of the destruction isn't yet known and will also take time to show up. Sadly, this kind of economic environment will be negative dominoes. One business failing will eventually lead to another business failing and so on, for awhile until sanity is restored. There has been a whole lot of froth feeding on froth.

Ireland 2.0? The rock star fisherman is going to become a broke lad fishing for spotties at the rocks.

What happen to the conventional common argument that housing prices will continue to rise due

1) to population growth?

2) housing shortage?

Those justifications for rising property prices may prove to be flawed thinking.

Reminder that these are some reasons given in the mainstream media, property market commentators, property market promoters, bank lending promoters masking as bank economists, real estate agents, property market mentors & other sources as to why property prices in Auckland will not fall by much and that there is a low probability that property prices will fall dramatically:

1) during the GFC, house prices in Auckland fell only 7-10%

2) over the past 50 years, house prices in Auckland have averaged 7.2% per annum (or commonly referred to as house prices doubling every 10 years). This trend can be expected to continue into the future - https://youtu.be/Agp9xFWoBX4?t=172

3) there is a shortage of underlying housing in Auckland, so property prices won't fall by much - https://www.interest.co.nz/property/97513/auckland-councils-chief-econom...

4) there is a growing population which means that there will be more demand for houses - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but-...

5) we have inward immigration which means more demand for houses

6) Auckland is an attractive city with an attractive lifestyle - that makes it desirable and attracts foreigners to move to Auckland and hence raise the demand for houses

7) lower interest rates are supportive of rising house prices

8) lower interest rates make debt servicing easier for borrowers

9) Low interest rates were also forcing retirees and those nearing retirement to look for investments that would produce income, such as rental property. "Plans of the baby boomers to retire and live off a conservative yet well-yielding portfolio have evaporated with low interest rates," he said. "[They] are seeking assets and buying investment properties. They are also seeking assets they can hold and live off of for three decades in retirement rather than just 15 years given advances in health and medicines." - https://www.stuff.co.nz/business/84322204/all-predictions-of-an-auckland...

10) we mustn't forget either the vested interests in ongoing stability. No government, central bank or trading bank with mortgage exposure wants materially lower house prices. Nor does an incumbent Beehive want falling house prices going into an election campaign https://www.stuff.co.nz/business/110499233/think-house-prices-are-going-...

11) the economy is doing well, with low unemployment - https://www.stuff.co.nz/business/110499233/think-house-prices-are-going-...

12) there has been insufficient construction of new builds to meet the housing shortage - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but-...

13) there are high construction costs to building a house. House prices cannot fall below their construction cost. - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but-...

14) people don't sell their houses at a loss - https://www.stuff.co.nz/business/106883553/house-prices-have-fallen-but-...

15) continued inflation means that house prices will continue to rise in the future

16) The fact is, debt levels have barely changed from the beginning to the end of those 10 years, compared to GDP levels, compared to household assets, compared to household disposable incomes. And much more importantly, debt servicing is very much easier now, an item that is almost universally overlooked. We are not pushing out to unsustainable levels now, and even if they creep up a little, we are far from that point. https://www.interest.co.nz/opinion/95894/if-you-think-new-zealands-house...

17) in aggregate household debt servicing is low in New Zealand - currently at just under 8% of disposable income of households - https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-household-debt

18) property market participants & commentators who have been correct in their predictions about recent property price trends have more credibility and hence their predictions of upward prices are believed by a wider audience (such as Ashley Church, Tony Alexander, Ron Hoy Fong, Matthew Gilligan, etc). - https://www.stuff.co.nz/business/84322204/all-predictions-of-an-auckland...

19) previous warnings about a house price crash have been wrong - property prices have continued rising upward significantly since these warnings were given, so there is little reason to believe these warnings.(such as Bernard Hickey) - https://www.stuff.co.nz/business/84322204/all-predictions-of-an-auckland...

20) its unlikely Auckland prices collapse. I think the main two reasons though are:a) Affordability has been this bad, and worse, in the past and it only resulted in about a 10% drop. b) The number of homes built over the last decade has been too low and will take some time to recover - https://www.interest.co.nz/property/100670/housing-market-continues-hibe...

21) returning New Zealand expats will buy houses in NZ -

22) NZ is a safe haven from COVID-19, etc - expats will buy houses in NZ - https://www.theguardian.com/news/2018/feb/15/why-silicon-valley-billion…

A good list of what MSM is saying.

I am incredibly skeptical. The idea of it actually increasing seems laughable.

To get a price bubble in any asset / object, there has to be widespread belief by the general public that:

1) prices are sure to go up

2) prices do not go down by much

Also see a large number of new entrants

It is interesting to hear the rationalisations for continuing price rises by market commentators (and those with a vested financial interest) tell to the general public and that the general public believe.

There is a large element of high confidence and greed. Little or no focus on downside risks. Confidence quickly disappears once prices start falling dramatically. (look at recent Kiwisaver asset allocations from aggressive to conservative after the rapid price falls in March)

Having witnessed firsthand quite a few price bubbles (and studied quite a few more) they can be easy to spot at extremes when price risks are high (however one never knows how long the music continues to play before it stops).

And whats your prediction CN?

No price predictions to give - you can see some really extreme and unexpected stuff happen in markets. (who could have ever have imagined that oil prices could become NEGATIVE $37 / barrel?, or negative interest rates before they happened?)

Property price risks of median house price levels are high in some markets in NZ.

Also when there are anecdotal stories of mortgage fraud, it does make you wonder how prevalent it is, and could be endemic.

Typically these types of fraud get discovered when market prices fall. Look at Madoff. Look at Enron.

I think it's gone beyond anecdotal now CN (this is Australia, but can't imagine NZ is that different): https://mozo.com.au/home-loans/articles/-liar-loans-on-the-rise-1-in-3-…

Ha! They really do produce a prodigious amount of spin.

My favourite is "house price won't fall cause GFC." I must have forgotten the part of the GFC where a virus shut down the entire global economy and NZ had no tourism for 2 years.

Wanted to capture many of the narratives being told that lead people to buy when there are elevated price risks.

Across the four indicators (I1-I4) for Christchurch:

I1 Accommodation & food services sector: CHC not ranked

I2 Difference in investors’ % share of purchases Q1 2020 vs. average: CHC <1%

I3 Airbnb listings as % of total dwellings : CHC <1%

I4 International as % of total guest nights: CHC ~45%

So CHC ranks 2nd on international guests nights (I4), yet that is 45% of nothing (I1) or 45% of <1% (I3) and therefore CHC is 2nd "riskiest" market on balance.

What wonderful analysis! It makes total sense!

ChCh prices will hold up just fine, and what it means is that if people aren’t buying then there are going to be plenty of tenants around!

We had plenty of applications for the properties we had to relet at the beginning of the year and don’t see much different next year.

If first home buyers can’t get mortgage money then there may not be many sales and prices won’t be dropping.

Personally don’t care what prices are doing as we don’t generally sell and if I see something that I like and is under priced giving a great return then why wouldn’t you be in?

So youre predicting prices wont drop in ChCh?

"A turkey is fed for a thousand days by a butcher; every day confirms to its staff of analysts that butchers love turkeys 'with increased statistical confidence.'"

- Nassim Taleb

honestly, I just feel so sad that greed has taken over this lovely country we live in

C.R.E.A.M

Meanwhile, on reddit new zealand

https://www.reddit.com/r/newzealand/comments/gfmbp6/this_time_it_will_b…

Low student numbers could potentially effect the lower end of the Wellington market.

Might be some uptick though as some people retrain, or go on and do a masters?

Maybe. Although, Masters students don't tend to live in the big old houses, flatting with other students. There are a lot of big old student digs type houses in Welly, owned by investors. Welly's rental market is massively reliant on big student numbers. Not the whole sector, but a goodly chunk. I live quite near Vic uni and i'm just surrounded by student houses. They've all been gone the whole lockdown and its been like 28 days later! Really quiet.

Students, Government and the movie industry. I had heard of potential Government job losses within the next few months but ironically Covid seems to have stopped that. As for movies, Wellington has Avatar 2 on the go, but I'd expect there to be a job hit within 6 months. Just my speculation (as someone working in the movie industry).

We have friends in the movie industry who have already been made redundant. The ones working in CGI are busier than ever though for now.

We've not had any redundancies (Weta Digi), as far as I'm aware. Just contracts not being extended. So far, it's 20% hour cut and pay freeze for 1 year. Compared to our Canadian, American and British counterparts, it's remarkable resilient. But there will be a lag in the pipeline before there's no new shots to be working on.

Yeah, its my friends at WetaD who have plenty of work on ;-) I imagine WetaD can price themselves pretty competitively compared to other English speaking competitors too?

Yeah depends which part of Weta. Post Production (Digital) have got enough to keep them ticking over, it's the set locations which are a bit on hold at the moment.

I turned down a job at WETA a couple of months back. They usually pay about 70% of market rate to contractors because they argue the job is "long term and secure". Pretty happy with that decision right about now.

Nahh Wellington has Weta and Tech industries that moved down from Auckland to keep you going.

It may.. although the sector and government believe with first moved advantage on covid-19 they can enhance the level of international students.

Maybe its time to go back to when rental properties were based on yield rather than speculative driven capital gains.

New reset eg, Property prices fall by 25%, rents fall by 15%, then legislative changes are made to remove monopolies so speculation incentive removed and prices and rent would only go up by the general rate of inflation from that point on.

If you want yield to be the driving factor for property then a 75% drop in price would do that. At 25% a lot of properties would still be marginal to losing.

"rather than speculative driven capital gains"

Many people believe that property prices double every 10 years. This belief has been widely perpetuated by property mentors and property promoters.

As a result of this essential underlying belief, many property investors have borrowed heavily and willing to invest for capital gains (and negative cashflow)

No, prices doubling has been perpetuated by reality. You can close your eyes if it's unpalatable. FWIW, the doubling is on the original price and not the compounded price. The first 100% can take as long as 12-15 years, the next 100% 8-10yrs, then 5-7 and so on.

Yes that has BEEN the reality. Was never going to guarantee that would be the reality moving forward.

And it's clearly not going to be.

So basically, "When we repeatedly said 'doubling every 10 years' what we actually meant was 'doubling the original purchase price every 10 years give or take'"? Classic.

Why don't you ask someone who bought in Tokyo in 1990 how many times their house price has doubled in the last 30 years.

You actually thought house prices doubled exponentially every 10 years??? Oh dear.

Tokyo is an extreme example, there are so many other examples of rapid house price inflation.

Clearly I didn't think that because I'm not one of the idiots on here spruiking buying leveraged property at the top of a bubble. Your crowd most definitely did think that and repeated it over and over again with great confidence. I appreciate that you at least have the self awareness to back pedal from that particular absurdity in light of the data.

Do you want some more price charts to look up?

Any city in Japan

Dublin

Madrid

Las Vegas

Phoenix

Let me know if you're getting bored...

I haven't back-paddled from anything, in major NZ cities you have 100% return on your initial investment (not compounded) every 7 to 10 years over the long run. The cities you cite above (Japan aside) all experienced significant over-supply in the lead up to 2007/8 - ground zero for the GFC. Have you looked at Wellington house prices over the long-run rather than cherry picking cities in US deserts?

You come across very bitter, like life has passed you by. It's none of my business where you choose to put your money, it would never occur to me to do so and I couldn't care less.

Here's Dublin for you, House prices are up 50,000% (500 x) over 115 years. Shall I check your other ones???

https://www.eh.net/eha/wp-content/uploads/2015/05/Lyons.pdf page 10.

Te Kooti,

Thank you for the link.

That is a great outcome for the property buyer in Dublin in 1900 and held onto their property for the next 115 years (assuming that they didn't use deposit recycling / equity release financing methods and maximised their borrowing capacity all the way until 2007).

Let's take a look at the situation for an owner occupier buyer in Dublin in late Jan / early February 2007:

a) Property prices in Dublin have been rising from 1900 to 2007 - that's 107 years of historical data of house prices rising. Based on that, the owner occupier believes that property prices will continue to rise, or not fall by much

b) They read that property market commentators are saying that there is a housing shortage in Dublin and read the following article in the local newspaper on 25 Jan 2007 - https://www.irishtimes.com/news/dublin-housing-shortage-to-continue-1.8…

c) They proceed with a house purchase in 2007 using high amounts of leverage.

Details of purchase:

i) Property price: 162,000

ii) Mortgage @ 80% LVR - 129,600

iii) Equity value saved and used to buy the house - 32,400

Value at 2020 (13 years of ownership)

i) Property price: 137,000 (fall of 15.4% from purchase price - AFTER 13 YEARS of ownership)

ii) Mortgage @ 80% LVR - 129,600 (assumed to be interest only for illustration purposes)

iii) Equity value - 7,400 (77% decline from original equity to buy the house)

House price data - https://tradingeconomics.com/ireland/housing-index

That 7,400 in equity may be used to either:

1) upsize (into a bigger house by younger owners for children), or

2) downsize (into smaller house for retirees)

(Remember that there still payment of sales commissions which would reduce the 7,400 equity value even more - say 3% on 137,000 sale price or approximately 4,100 in sales costs which would result in net equity of 3,300). Haven't even included interest costs in any of the above calculations.

Now how is that 3,300 going to be sufficient for a 20% deposit for a new house (either for the upgrader, or downsizer)? That 3,300 is now only 2.4% of the median house price of 137,000 in 2020.

The owner occupier's financial security had experienced a real set back. These people will have less to retire on. All because of that one decision to purchase a property in 2007.

Now that scenario assumes that the owner occupier was able to hold on. What happened if they were unable to continue debt service payments (such as lost their job, experienced lower weekly wages, etc) and were forced to realise those losses?

This is the potential situation that owner-occupier buyers today are facing. I don't believe that hard working owner-occupiers buyers who have taken years to save their deposit to buy a house should be potential collateral damage as a result of a large presence of speculators in houses. Owner occupier buyers should be fully informed of potential property price risks and make fully informed decisions, rather than accept blindly the highly promoted viewpoints of those with huge vested financial interests.

Imagine if that potential owner-occupier buyer was your loved one.

^This. Thanks CN for taking the time to illustrate that.

Te Kooti look at page 11 of your link. BY YOUR OWN DATA it is very obvious that the bubble growth trendline is NOT the real long term trend. The long term trend is the slow gradual increase from 1900 to 1995. Then there is a massive spike from 1995 to 2007 followed by a crash and partial reflation of the bubble. Still well off the 2007 peak in real terms to this day.

Property should be viewed in real terms as well. Even the graph in the link by Te Kooti on page 11 shows that for 100 years, prices in Dublin had zero real growth! Then boomfa...bubble time and collapse. 1995-2007.

Check out the inflation adjusted US and Aus data. Note that Australia has gone higher since and that NZ follows more or less the same price/inflation trends as Australia. We've got a bubble on a bubble from about 1995 onwards!

https://www.whocrashedtheeconomy.com/blog/2012/08/never-a-better-time-t…

My understanding is that historically a price/income ratio for afforadable housing is around 3. With the average household income around $85,000 (https://www.stuff.co.nz/business/114647486/new-zealands-money-how-do-yo…) then based on that historical measurement of affordability, the average house in NZ should be worth between $250,000-340,000. Approximately 50% less than current values between $600-700,000.

So if Te Kooti wants to use historical data to see if houses are over priced or not, we need to look at it from all angles - and this one would say we could see falls of 50% - all it will take is some inflation and interest rate reversion to mean. Unless of course the tail wags the dog now (house prices set interest rates....but surely we aren't that mad!) but if we use inflation targeting on the way down to zero interest rates, then we must to the reverse on the way back up - otherwise the last 20 years has been an economic lie!

https://www.whocrashedtheeconomy.com/blog/2012/08/never-a-better-time-t…

In real terms, NZ and Aus (and Can) have the mother of all real estate bubbles on our hands.

For potential owner-occupier buyers, they might be interested in following this Irish couple who were mortgage prisoners who were unable to upgrade.

I recall a story of a young couple who bought a one bedroom apartment. Then they had a couple children, and the property was too small for them all. However due to the fall in property prices, they were effectively in negative equity, and were unable to upgrade to a larger property as they had no equity or insufficient equity to upgrade. So they were forced to rent a place that was big enough for them all, whilst still paying the mortgage on the one bedroom apartment in negative equity.

1) https://youtu.be/J4XrOGuAdWo?t=414

2) follow up https://youtu.be/J4XrOGuAdWo?t=2166

3) follow up - https://youtu.be/J4XrOGuAdWo?t=2507

Also note the mental toll it has taken on the couple.

Note that this documentary was made 9 years after the property prices peaked in 2008 and property prices have still not recovered to their previous peak levels. The couple have owned the property for 11 years and are still in negative equity.

A reminder for all potential owner occupier buyers - choose your scenario and act accordingly.

Which will the owner occupier regret most:

1) missing out on future potential gains in equity?

2) potential loss of their savings invested as the initial deposit for purchase of the house or even potential negative equity?

For owner occupiers, a reminder of the impact of leverage (it amplifies property price changes both on the up and down):

Scenarios of financial impact of leverage on equity, assuming an 80% LVR for owner occupier, for a recent $1,000,000 property purchase, $200,000 initial deposit, mortgage $800,000. (simple round numbers used for illustration purposes)

A) Scenario - property price rise:

1) property price rises 5% to $1,050,000, mortgage $800,000, equity $250,000, so 25% gain in equity value from $200,000.

2) property price rises 10% to $1,100,000, mortgage $800,000, equity $300,000, so 50% gain in equity value from $200,000.

3) property price rises 15% to $1,150,000, mortgage $800,000, equity $350,000, so 75% gain in equity value from $200,000.

4) property price rises 20% to $1,200,000, mortgage $800,000, equity $400,000, so 100% gain in equity value from $200,000.

5) property price rises 25% to $1,250,000, mortgage $800,000, equity $450,000, so 125% gain in equity value from $200,000.

6) property price rises 30% to $1,300,000, mortgage $800,000, equity $500,000, so 150% gain in equity value from $200,000.

7) property price rises 35% to $1,350,000, mortgage $800,000, equity $550,000, so 175% gain in equity value from $200,000.

8) property price rises 40% to $1,400,000, mortgage $800,000, equity $600,000, so 200% gain in equity value from $200,000.

9) property price rises 50% to $1,500,000, mortgage $800,000, equity $700,000, so 250% gain in equity value from $200,000.

10) property price rises 100% to $2,000,000, mortgage $800,000, equity $1,200,000, so 500% gain in equity value from $200,000. (i.e if they believe that the property price doubles every 10 years)

Remember, the owner occupier must be able to hold on under ALL economic environments (including any potential significant reduction in household income).

B) Scenario - property price falls:

1) property price falls 5% to $950,000, mortgage $800,000, equity $150,000, so 25% loss in equity value from $200,000.

2) property price falls 10% to $900,000, mortgage $800,000, equity $100,000, so 50% loss in equity value from $200,000.

3) property price falls 15% to $850,000, mortgage $800,000, equity $50,000, so 75% loss in equity value from $200,000.

4) property price falls 20% to $800,000, mortgage $800,000, equity is ZERO, so 100% loss in equity value from $200,000.

5) property price falls 25% to $750,000, mortgage $800,000, equity is NEGATIVE $50,000, so 125% loss in equity value from $200,000.

6) property price falls 30% to $700,000, mortgage $800,000, equity is NEGATIVE $100,000, so 150% loss in equity value from $200,000.

7) property price falls 35% to $650,000, mortgage $800,000, equity is NEGATIVE $150,000, so 175% loss in equity value from $200,000.

8) property price falls 40% to $600,000, mortgage $800,000, equity is NEGATIVE $200,000, so 200% loss in equity value from $200,000.

Here is an actual example for owner occupiers to learn from (if they choose to) from New Zealand

A) Purchase: December 2006 purchase price $164,500

B) Sale: December 2019 (after 13 years of ownership) - sale price $140,000 or 15% below their purchase price.

https://www.qv.co.nz/property/56-romilly-street-westport-7825/1055725

Some mathematics

A) December 2006 purchase

i) purchase price $164,500

ii) LVR 80% mortgage $131,600

iii) Equity deposit $32,900

B) December 2019

i) Sale price $140,000

ii) Mortgage $131,600 (assumed to be interest only for illustration purposes)

iii) Equity value $8,400 - loss of 74%. (which excludes the payment of interest and sales commissions of say another $3,000 -$4,000)

Now they look to upgrade or downsize - what can they buy using that $8,400 (less after sales commissions) to use as a 20% deposit (assuming no other additional funds)?

That one purchase decision has potentially severely jeopardised their future financial security, and their ability to upgrade. (or in the case of downsizing, resulted in a vastly smaller amount for their retirement funds)

The owner-occupier would have been better to have not bought (and rented) and kept their initial equity in the bank earning interest for 13 years.

Are you serious, Westport, that's your example??? Oooh look I scoured NZ and found a house that went down in value. Do you know how many publicly listed companies have blown themselves and their shareholders up, there is risk in every investment, there are always pockets that perform poorly. What did the general NZ house price index do over the same period of your example?? Napier, Wellington, Hamilton - what did those house prices do?

Embarrassing.

Have you had a bad experience on the share market?

No actually, the contrary. My point is, property as a market has an industry make-up like stocks - growth, dividend, high beta etc etc. Choosing Westport is like me choosing CBL insurance as an example of how stocks are rubbish and ignoring Xero. Also, 450% above inflation over the last 60 odd years looks pretty good to me. That's an average real yield of 7% (crudely).

"My point is, property as a market has an industry make-up like stocks - growth, dividend, high beta etc etc. Choosing Westport is like me choosing CBL insurance as an example of how stocks are rubbish and ignoring Xero. "

Remember, that owner occupiers buyers don't buy a housing market index to live in. They buy a single residential dwelling to live in, normally financed with a mortgage.

"Are you serious, Westport, that's your example??? Oooh look I scoured NZ and found a house that went down in value. Do you know how many publicly listed companies have blown themselves and their shareholders up, there is risk in every investment, there are always pockets that perform poorly. "

Te Kooti,

I was unclear in the points that I wanted to highlight with the Westport example. Let me clarify.

How many of these comments have owner-occupier buyers been told?

1) you can never lose with property

2) you never go wrong with bricks and mortar

3) house prices always go up / never go down

4) rent is dead money

5) people should own their own home over renting

6) there is population growth so property prices don't go down / will always rise

7) everyone needs somewhere to live so property will always be in demand and property prices will rise

8) there is an underlying housing shortage so property prices will not go down by much

I have heard these phrases frequently repeated by property market promoters, and real estate agents to persuade inexperienced owner occupier buyers to transact (so that real estate agents can earn their commission).

Then these historical price charts are shown to support their point - https://www.interest.co.nz/sites/default/files/styles/full_width/public…

{kind=link}

The point with the Westport example, is that after 13 years of ownership, most owner occupiers would expect to have made some gain in the value of their house, (and increase their equity) and that is clearly not the case. Most owner occupiers would not expect that they could lose 75% of their initial deposit after 13 years of ownership in property.

For most owner occupiers, the house is the main asset used for upsizing, or the main source of funds for retirement (due to downsizing). The house is the main source of wealth creation. If the purchase decision is made poorly, the future financial trajectory for owner occupiers can change dramatically, and can have a significant impact on the quality of their retirement.

The Westport example illustrates to owner occupier buyers that property is not a risk free one way bet and that owner occupiers can lose a large chunk of their initial equity deposit.

There are numerous more examples available located all over the country. Look at the example in Freeman's Bay, in Auckland of the purchaser in March 2020.

People are free to choose to ignore the lessons in the above example. People however are not free to choose the consequences of choosing to ignore lessons in the above example.

"What did the general NZ house price index do over the same period of your example?? Napier, Wellington, Hamilton - what did those house prices do?"

For an owner occupier buyer today, (who is using high levels of debt to finance their purchase), the key question is: are those historical returns, a useful and relevant guide to future returns?

For some people, they like to use the rear view mirror approach to develop their future return expectations by using historical returns. That is their choice. That is also how many people get caught out at extremes.

Using this approach, buyers would have lost significantly in the following instances:

1) Ireland property circa 2006-2007

2) Internet shares circa 1999-2001

3) shares circa 2007 / 2008

Owner occupier buyers are free to use historical property prices, and historical returns to develop their future return expectations and buy at today's price levels using high levels of debt. They are however not free to choose the consequences of their choice.

Now, let's take a look at the situation for a recent owner occupier buyer in Auckland in early March 2020:

A) at purchase date

a) according to the RBNZ, house prices in New Zealand have been rising (in nominal terms i.e non inflation adjusted) from 1965 to 2015 - that's 50 years of historical data of house prices rising. Property prices have doubled every 12 years on average. That is a 5.95% growth per annum for that 50 year period.

https://www.rbnz.govt.nz/research-and-publications/reserve-bank-bulleti…

b) furthermore since January 2016, the median house price in Auckland has risen from $720,000 to $888,000 in February 2020 - that is a 23% increase (or 5.2% per annum).

c) they read that there is a property market cycle and that property prices double every 10 years from high profile property market commentator Ashley Church

i) 27 January 27, 2020 - https://ashleychurch.com/have-we-seen-our-last-property-boom/

d) they read the latest newsletter of a well regarded property market commentator Tony Alexander saying that there is a housing shortage in Auckland

i)- 20 February 2020 - Tony Alexander - http://www.tonyalexander.nz/resources/TV%2020%20February%202020.pdf

e) the economy is strong, there is low unemployment, a housing shortage in Auckland, and inward migration.

Based on the conditions and information above, the owner occupier believes that property prices will continue to rise, or not fall by much.

f) They proceed with a house purchase in March 2020 using high amounts of leverage.

Details of purchase:

Address: 11 Wood St, Freeman's Bay, Auckland

i) Property price: $3,710,000 (vs CV of $2.625mn so price to CV of 1.40x; vs homes.co.nz estimate $2.89mn so price to valuation is 1.28x)

ii) Mortgage @ 80% LVR - $2,968,000

iii) Equity value saved and used to buy the house - $742,000