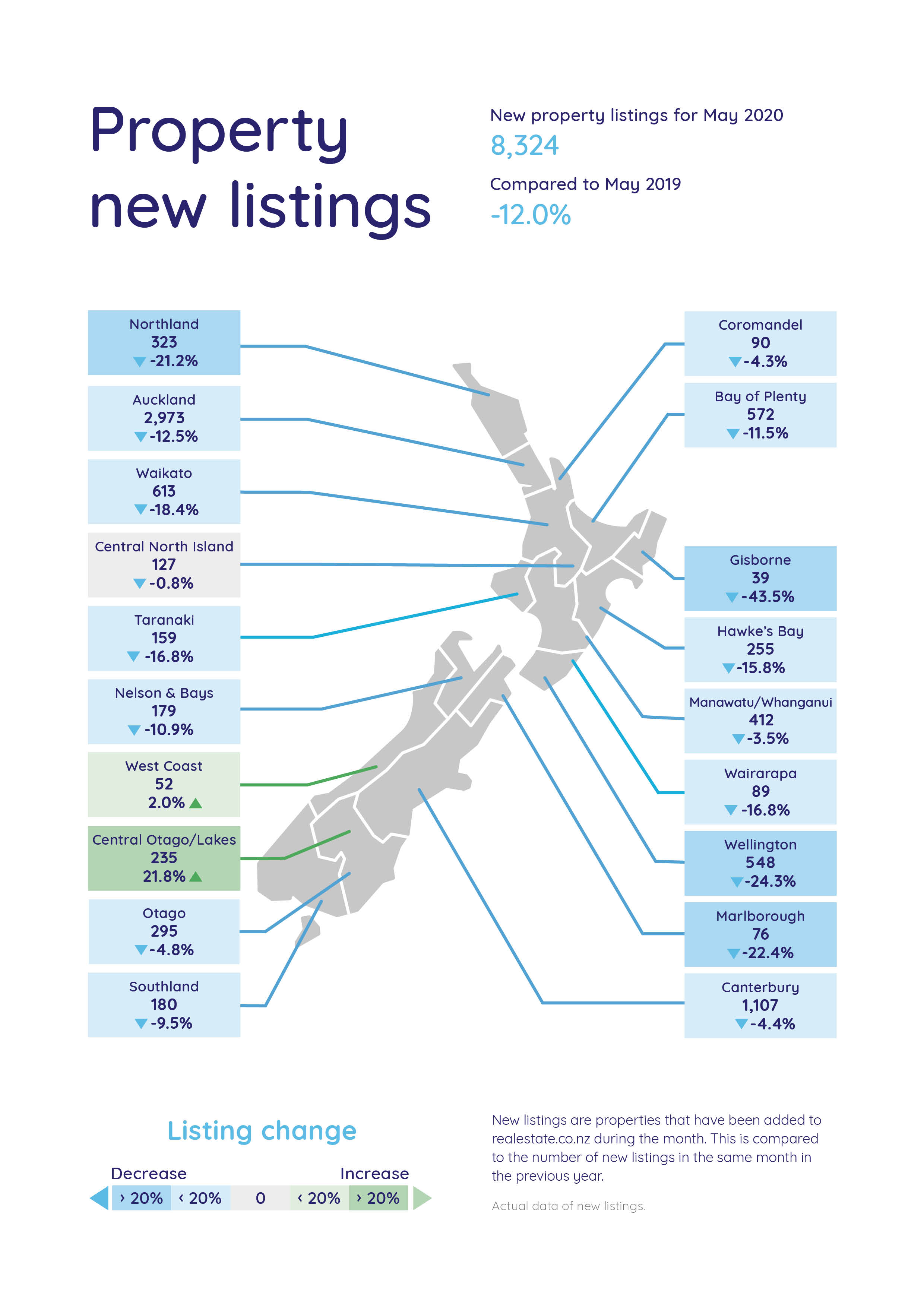

There was a substantial number of new residential property listings in May, suggesting market activity could be heading back towards normal over winter.

Property sales website realestate.co.nz received 8324 new listings from throughout the country in May, down just 12.0% compared to May last year.

That was a substantial jump from just 2962 new listings in April, when the country was mostly in Level 4 lockdown.

The jump in new listings was strongest in the Queenstown-Lakes District, where May's new listings were up 21.8% compared to May last year.

Around the rest of the country, the strength of new listings varied widely, from being up 2.0% compared to a year ago on the West Coast, to being down 24.3% in Wellington.

In Auckland new listings were down 12.5% compared to a year ago and in Canterbury they were down 4.4% (see chart below for the full regional figures).

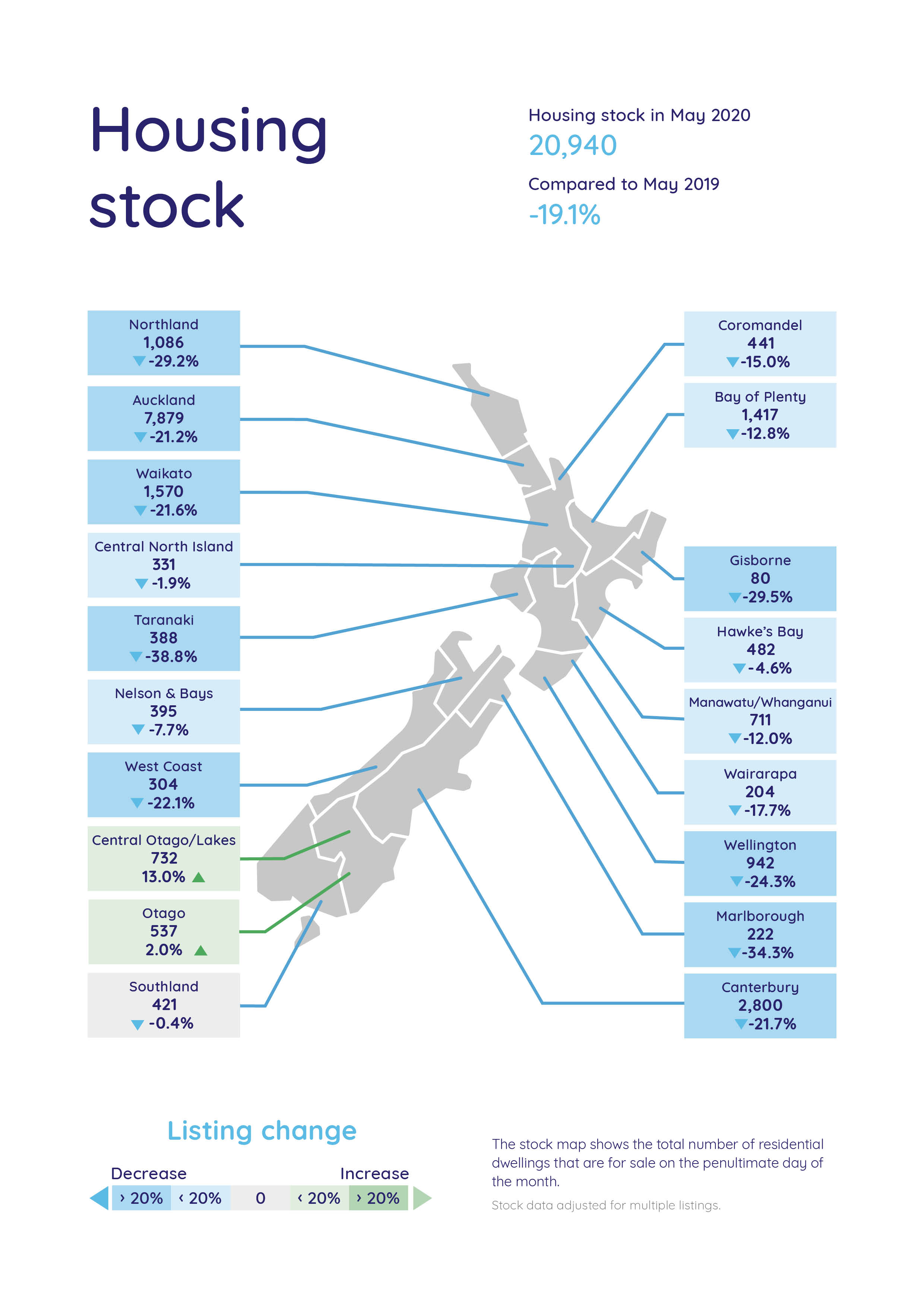

The total number of homes on the market is also bouncing back, with realestate.co.nz having 20,940 properties in total available for sale on the website at the end of May, which was the highest number since November last year.

However, that was still down 19.1% compared to May last year.

The total inventory levels in May were lower than May last year in all parts of the country except Central Otago-Lakes where they were up 13.0% compared to a year ago, and Otago where they were up 2.0% (see chart below for the full regional figures).

The national average asking price fell back sharply in May, dropping from its record high of $874,886 in April to $729,002 in May (-16.1%), but that was still up 10.0% compared to May last year.

Although sales activity was seriously reduced in April there was substantial settlement activity from sales that occurred earlier in the year, and April's prices reflected the buoyant market in late summer.

However, although the national asking price dropped sharply in May, around the country asking prices were down in May compared to April in nine regions Auckland, Bay of Plenty, Gisborne, Wairarapa, Wellington, Nelson Bays, Marlborough, West Coast, Central Otago-Lakes and Otago, and up compared to April in nine regions, Northland, Coromandel, Waikato, Hawkes Bay, Taranaki, Central North Island, Manawatu/Whanganui, Canterbury and Southland. with record asking prices being set in Waikato, Hawkes Bay, Central North Island, Taranaki, Manawatu/Whanganui and Canterbury.

Perhaps not surprisingly, during a period when the country was still in partial lockdown and many people were working from home, 1.2 million users visited the realestate.co.nz website in May, compared to 1,.1 million in February.

The comment stream on this story is now closed.

128 Comments

Ex Air BnB in Queenstown start to hit the market is no surprise. No income and lots of debt is a bad combo in anyone's books. Those that have no debt will will yawn, and be happy that the frantic pace of Queenstown backs off a bit.

Those that have no debt will will yawn, and be happy that the frantic pace of Queenstown backs off a bit.

As long as they're comfortable being 'all in it together.' Having no debt is a positive step. But being exposed to depreciating asset markets can have serious psychological impacts.

I think Northland and Coromandel will also see prices shifting downwards due to major loses in international tourism making it very difficult for Airbnb's to keep going etc.

Northland prices are ridiculous at the moment, their REA's seem to be trying to sell homes for double or at least adding a several hundred thousand on top of the properties 2019 RV, which is lunacy considering there is little to no economy in these areas. How do they think people are going to forking out over a million for a $400k batch stuck in the middle of no where!??

Just been to the Coromandell and baches in good spots selling fast as returning expats want holiday home to escape Auckland in the weekend. Bach next to ours been on the market for over a year and "sold" - owners could not believe it.

Who are all these rich returning expats? You know any? Sure, there might be a few here and there...

Data shows a large chunk of returning kiwis have gone on the dole.

Rental listings are dropping now Fritz. Was over 10100 now under 10000 across the country. Those returning kiwis (rich or poor) still need somewhere to live

I'm sure you are right. Auckland is well above 5100 still.

I think auckland as a proportion probably has too many

And countrywide rental listings were 8,027 on the 21st April 2020 so it pays to look at the bigger picture....

Yes I wonder that too Fritz. I've recently seen kiwi friends return from the US who lived out there for over a decade, they sold property over there and had good incomes. Only to find that returning to NZ they're now on lower salaries and can't afford to buy a home here in Auckland even with a sizable deposit.

CJ, you would’ve thought that the would’ve had the foresight to look on the Webb to see how much houses were in Auckland wouldn’t you?

Believe it or not, there are far better places to live than Auckland and far better house buying price wise!

Everyone knows that Auckland is expensive and if you want to live in Auckland then pay the price!

Yep they have looked outside of Auckland, and the bizarre thing is that most of NZ is now getting as expensive as Auckland. Even though there's not much economy to support those prices. So either people are getting in to huge amounts of debt that they can't hope to pay back or so there's external influences. Or which is what I suspect, most of these properties with unrealistic prices are just sitting there unsold.

CJ, fair enough, personally I wouldn’t be wanting to pay the prices for homes in Auckland as it is not a particularly desireable place to live, despite the increasing population.

Bearing in mind ChCh population is growing quicker percentage wise than Auckland.

Yes I realise many are probably over committing and potentially putting themselves into vulnerable positions particularly if a couple lose their job or career.

What I have always consistently maintained is that you need to be buying at the right money and in essence I have maintained that Auckland and some other places are overpriced but if that is the market, then that is what you will need to pay, but always buy right!

We have made a successful business in ChCh from buying right with very good cashflow and always with upside and this is what I have a,ways maintained.

At the end of the day people have the choice to do what they want within reason.

Have helped several people to improve their lifestyle thru property investment done well.

Most people can improve their own financial position by getting advice from the successful people and what I can guarantee is that sitting on your chuff moaning will get you nowhere.

From what I'm hearing, most younger generations and in a lot of cases older as well (Returning kiwis) are now moving back in with their relatives to wait for prices to drop and save for a better deposit which is why we're seeing a lot of properties just sitting on the market unsold.

Lets face it you only need to look at the latest auction results to see that housing stock isn't moving that much. ¯\_(ツ)_/¯

Teach them the no dig method to grow their own veggies CJ

Yep they're already in to wanting to grow their own veggies, just they can't afford the land in their own homeland (Pardon the pun). :)

The exchange rate is pretty good for them bring in money from the US. But NZ house prices are just way too high compared to incomes.

That's one of the things about this market. It's just so damned expensive. It seems backward that Auckland, a relatively small city surrounded by plentiful land that doesn't pay well, is miles more expensive than much bigger cities in the U.S.A that pay a lot better.

It’s winter now. That combined with the Covid-19 crisis is not good news for the housing market - and various other consumer and investment markets.

I anticipate that house prices will weaken - and that’s been my position for several months now.

But any falls won’t be of the magnitude that the DGM are parroting. The wise among us will ignore their scaremongering.

NZ house prices have proven resilient in the past - and will remain resilient in the future.

TTP

I dont think so Tim

The resilience you talk of is based on a giant band-aid by the RBNZ lowering the OCR to all but zero

Care to predict how much prices will weaken???

For a long time I believed low interest were inflationary. In the long term they are deflationary. If people belive their retirement will be more problematic or that they can buy big ticket items more cheaply in the future, they will defer their purchase.

TTP = Take the piss ?

Hmmm name calling, classy!

Do you think it's less or more classy than gloating about a large property capital gain in an economic climate where thousands of kiwis are losing their jobs?

TingTP ? Its a verb not a noun.

Its an accurate behavioural description.

And you should talk Yvil. I’ve been on the receiving end of your vitriol...

TTP often called me Motor Moa so he's not exactly a saint.. his medicine really.

Rich NZers going home to make pesos and buy overinflated prices for weatherboard houses, sounds like what rich people do. Not.

Likewise poorer NZers going home to make pesos and buy over inflated prices for houses, not sure that's gonna happen either.

I would rather use my money from my house and savings to buy a business in NZ, and buy a cheaper house in a location that is cheaper to live. Lifestyle is what I'm after, by the beach. Whats the point of going back to NZ and get in the rat race and get into debt to pay off a huge mortgage for the rest of my life, sitting behind a desk.

About time

This article makes excellent reading and analysis:

https://www.zerohedge.com/markets/here-stunning-chart-blows-all-modern-…

This means that the lower (and more negative) central banks push rates, the lower (not higher) the spending, the higher (not lower) the savings rate, the lower the inflation, the higher the disinflation (or outright deflation), which in turn forces central banks to cut rates even more, to add QE, yield curve control, buy junk bonds, buy ETFs, or pursue any of a host of other monetary policies that are even more devastating to consumer psychology, forcing even more savings, resulting in even more disinflation, causing even more intervention by central banks in what is without doubt the most diabolical feedback loop of modern monetary policy and economics.

Said otherwise, monetary easing is deflationary. Let that sink in.

In effect, what the chart above shows, is that once trapped by NIRP, there is no way out, and the more central banks pursue inflation to offset deflation via monetary policy, the more pronounced the deflationary outcome resulting in even more central bank deflationary "stimulus"!

Meanwhile, as central banks spark even more deflation with their policies, the one place where all those trillions in liquidity they conjure out of thin air ends up in, is what was once known as the "market" and is now, in the words of BofA the "fake market" or as DB calls it "administered markets", leading to ever higher fake asset prices, and ever greater wealth and income inequality, which ultimately tears the fabric of society itself.

Anyone who has followed Japan should realize that monetary easing doesn't necessarily revive bubble economics.

Talking of bubbles, looks like Australian property market is starting to deflate as well despite the huge lowering of mortgage rates. The Business Times article: Australia house prices fall in May as shutdowns hit property market, "AUSTRALIAN home prices fell in May for the first time in almost a year as the impact of the coronavirus shutdown rumbles through the economy."

https://www.businesstimes.com.sg/real-estate/australia-house-prices-fal…

"Property values across the state and territory capitals fell 0.5 per cent last month."

Hardly newsworthy.

The news for Canada's property market isn't that rosy either with at least -11% falls. Perhaps they haven't been pumping the mortgage drops as much as here and Oz.

Better dwelling article: CMHC’s Canadian Real Estate Price Forecast Shows Big Drops In Ontario and BC. "Prices are expected to start falling later this year, and don’t find a bottom for a year or two. Depending on the market, the forecast runs out of time before seeing a recovery."

https://betterdwelling.com/cmhcs-canadian-real-estate-price-forecast-sh…

Family in Canada say LVR has increased from 5% to between 10 and 20%

For young Canadian's that is rosy news.

Perfect analysis. I agree 100%.

I looked at Japan's data. What point to note is that their average income has been on a declining trend since 1990s, despite all the QEs. People who talk about this never mention this point. off-course if your income is reduced, you will spend less. To say when deposit rates decrease and there is aggressive monetary expansion going on, spending decrease is misleading unless you look at the impact of the monetary policy on actual earnings at corporate and family level. Saving up when income is down does signal that the money has ended up with people who do not need it and who are not willing to risk it when investment prospects are so dim.

Great link, thanks RCD

This is such a great article thanks

Pricing in Tauranga in the over $1m bracket is rapidly dropping back to RV. Offers are now for RV or below. There may be a bit of a Mexican standoff for a couple of months but if you really want to sell and there are now plenty of reasons why you have to sell, prices are going to keep falling.

Our daughter had a look at a Ngatai Road starter that went to auction last week.

Bought as a Deceased Estate 2 years ago for CV of $520k; 2 years worth of renovations ( badly needed!) with no tenant ( no income) and the financing costs associated. Needed pretty much everything doing ( bathroom, kitchen, electrics, plumbing, enlarged from 2 bedrooms to 3 to 'maximise' sharing with a flatmate, wreck of a garden/fences/garage, complete repaint walls and roof, driveway rebuild, internal cladding from an accumulation of 10 years worth of rubbish not taken out - Council had to send 3 trucks and a fumigator to get it ready for re-habitation etc) and it went for $659K.

Now that looks good, and the stat will say a "25% Rise in value!". But 2 years at 5% financing = $50k; reno costs couldn't have been less than $50k; selling costs/legal fees = $20k.

So all up ( IF they got away without paying any Income Tax!) that's a net result of $20k, or 4%, not 25%.

But it will show 25% !

Took 2 years to complete the renovation.. Tax avoidance I would say if bought before the BL extension.

That's exactly what the RE agents sales pitch said" Oh. They bought this to live in but changed their minds'

However, with the new 5 years Bright Line test it will be interesting to see how far back the IRD actually look at such obvious cases as this. ie: Sold just over 2 years from the original deadlines.

After all, the BL test isn't the 'be all and end all' of IRD surveillance - it's just the starting point.

Easy for IRD to prove too. We bought beach bach a week after the change and our lawyer remarked it was a pity we hadn't bought before.. that was the last thing on my mind as not our intention to sell. Been two years now and loving it even though empty most of the time. Just haven't got round to doing air bnb

Bright line tests are not susceptible to tax avoidance. For example, a person with no personal place of abode in NZ will become a NZ tax resident if they reside in NZ for 183 days in any 12 month period. Many visitors will stay outside of this bright line test often staying for 180 day blocks a year for several years. IRD have and never will take a tax avoidance case in such circumstances as the law is clear that all that matters is whether the bright line test is met.

Cough splutter ...Houseworks claiming tax avoidance?

Excuse me? Tax planning is perfectly legal... dont worry I pay far more than my fair share. And yourself?

You're definitely supposed to lodge tenants' bonds though eh.

Haha lol you have a long memory Rick

No I didnt think that you would volunteer any information

Two years... 4% with all those hardwork... That's why I'm always saying that investing into property is not attractive at the moment at all. We won't have those 2014-2016 moments anymore that you can just sit there and wait for a capital gain. Investing into stock gets much better return. People who have invested into shares two months ago, they should easily get a 10-12% return at the moment. If you are good investor, and invest smart, you could get at least 20% return. I dont understand why people are so obsessed with properties.

Er, let's think about why... cos of leverage, cos of tax incentives (although admittedly way less than used to be), cos it'll still be there even if paper assets go into a slide (although if tenants burn house down, maybe no house left but even so at least have the land so long as no sink holes/ land doesn't get blown up), somewhere to store crap, inflation wipes out debt... that could be why.

RBNZ to reinstate LVR to investors with immediate effect. Reserve Bank is mandated to provide soundness and efficiency of the financial system, not the other way around. Rising investor participation tends to increase financial stability risks in severe downturn conditions.

I seriously fail to see how an increase in listings is any indication that the market could be 'heading back towards normal'. Just anecdotally, I have two friends who are considering listing now so that they can sell before the sh*t hits the fan. I suspect they're not the only ones.

They may be too late. My mate and his brothers sold their place in Papamoa just before the lockdown. The panic is due to start very soon.

Watching keenly. So far no rush of listings, at least in Akl and northland.

Canterbury listing numbers down show no panic at all!

Record asking prices is validating that Christchurch prices are not going to be dropping as people are wanting to live in the most liveable city in NZ with the most stable real estate market in the country.

Those that hesitate will be costly as with interest rates so low, this is your best chance to own in paradise

TM2, drink that (property) Kool-Aid.. It's good stuff!

"So far no rush of listings, at least in Akl "

Has anyone been monitoring inner city apartment listings in Auckland? - that would be an interesting statistic to watch.

Currently 617 listed for sale.

Some have been listed for sale since August - October last year - so that's well over 6 months and still unsold at the vendor's desired price.

Here are some examples -

i) Listed 29 August 2019 - https://www.trademe.co.nz/a/property/residential/sale/listing/189150235…

ii) Listed 15 November 2019 - https://www.trademe.co.nz/a/property/residential/sale/listing/259727332…

iii) Listed 13 June 2019 - https://www.trademe.co.nz/a/property/residential/sale/listing/166458056… (this one is leasehold and ground rent under review)

It will be interesting to see how long price reductions are staved off.

Historic and current evidence seems to indicate that there's usually a few months of standoff before prices plummet.

There is currently a window of opportunity for fhb. Why after buying your own home would you try to discourage others.

Because the situation has changed since covid-19 hit the scene, and throwing his fellow FHB under the bus is not a nice thing to do..

I really, really don't understand you most of the time.

My point is there is likely to be a significant drop in prices in a few months time. Why is that discouraging FHBs?

It's not.

As I have said before, it's a good time for FHBs to be looking if they have job security, but that the deals might get better in a few months time.

Never mind

Yes that's what happen after a few years of price stagnation in larger cities. Now that tourism has gone there's nothing to support property prices in holiday areas.

CKahawai

Why do your two friends propose selling?

What do the two friends propose doing after selling? I assume renting.

Both are in Auckland, and in each case, their proposals have been to sell at today's 'premium' prices, move in with family members, then re-buy (and upsize) down the track when prices have reset. I think it's a smart option. Neither are desperate to sell and won't if they don't get a price they're happy with.

Sounds like a logical thing to do with shares, but with the house you live in? What a pain in the butt. I can only assume they are planning to sell privately (as most people should), but even so, moving and storage costs later, and just the overwhelming annoyance factor of moving on the chance you get a step up the ladder... They are clearly significantly more exuberant than I have ever counted myself as.

Solve_it

Good that you see beyond the rhetoric. Sounds great bit of casual comment but the reality is a little bit more complex.

Lesson also in that lots ditched out of exposure to shares (especially KiwiSaver Growth funds) thinking that they were being smart proposing to get back in once the market bottomed. However, the reality is that the market bounced back so, so quickly they have missed the boat and taken a very big hit.

What is the basic strategy of long term investments? Hang in there for the long term and accept short term volatility.

My wife and I experienced over 10% drops (based on RVs) on three investment properties in the GFC - however within a year or two we were well ahead again.

I agree timing the market is a fools game as this cat seems to be made of high dense rubber

Damn i wish i was a baby boomer

I'm no boomer mate

I would tend to use a typical intersection of the supply and demand curves to suggest a downward trajectory in prices but the NZ property market in NZ doesn't seem to follow theoretical price discovery. In other words, an excess of supply pushes the price down. Is there an excess of supply right now?

Yes and it will increase each month

"Property sales website realestate.co.nz received 8324 new listings from throughout the country in May, down just 12.0% compared to May last year.

That was a substantial jump from just 2962 new listings in April, when the country was mostly in Level 4 lockdown."

Comparing m.o.m to april is a waste of time

so those regions with fewer listings can expect a rise in values if the number of buyers remains the same, right ?

Why? Do the buyers suddenly have oodles more cash to spend, and the willingness to spend it to push prices up?

Is the forcaste by everyone / experts that house price will fall wrong :

https://www.newshub.co.nz/home/money/2020/06/new-zealand-house-prices-r…

OR is the current data mostly made up of houses sold earlier at high / pre virus prices and went unconditional in May / after the lockdown

OR is it come what may house price in NZ will never fall

Will know with data in October / November, what is the status of housing market in NZ.

Had commented in other article the same and had a feedback which too was possible as below :

May be the house price rise was much higher earlier and has come down from much higher rise and was caught on its way down at a percentage of rise at that time and if touched a falling knife.. will have to wait till November to get clear picture.

Firstly, average prices are much less reliable than medians, especially in the current situation (where higher value properties seem to be selling much more than low-mid value).

Secondly, too early to draw conclusions. Need another 2-3 months of data.

Yeah by October/November will not only know the direction (Should be South) but also the extend of damage(fall) that has and likely to happen.

Correct is too early to draw conclusions.

Most intelligent people realise that economists mostly predict wrong!

The experts were predicting tens of thousands of people dieing from Covid19 in NZ and yet no one apart from resthome patients did in reality.

Experts were predicting interest rates to go to 9 or 10% a few years ago and they are a third of that!

If you follow economists the. You are mostly misled, you would be far better off taking advice from people who have been financially successful than those that make predictions!

I'm assuming you're claiming that experts claimed that tens of thousands of people would die of Covid-19 even if we implemented the lockdown, because to claim that experts who predicted that many people would die if we didn't lock down were wrong because we did lockdown and people didn't die would be pretty silly.

So, can you give us an example of this? An expert who claimed that tens of thousands of people would die, even if we imposed the border restrictions and lockdown?

There would be a lot dieting as well due to the virus!

Covid19 is not a killer virus inNZ there hasn’t been a single death to anyone semi healthy and the claim that Nz could lose 28,000 lives is clearly a load of rubbish.

The so-called killer virus had next to no one in hospital throughout Nz and in fact is going to kill so many more due to the so-called cure to the virus.

You're right that there hasn't been many deaths. But I don't think anyone predicted that *even if we went into lockdown and imposed border controls* there would still be lots of deaths. Those predictions were about what would happen if we didn't do anything to prevent it. If you have any evidence to the contrary, by all means present it.

As for it being a 'so-called' killer virus, tell that to people in the US, where they've had 100000 deaths and counting.

TM2 gets his fact checking from Trump university, he has a good handle of things in his head. Don't you know hes a successful business man, he doesn't advertise it I know, so its hard to guess.

28,000 lives in NZ would be around 5,600 per million inhabitants. Here are some current statistics for you - and note that this is not over by a long shot.

Spain - 6,133 deaths per million

USA - 5,620 deaths per million

UK - 4,072 deaths per million

Sweden - 3,746 deaths per million.

NZ could very easily have lost 28,000 lives if we hadn't locked down so effectively. Note that all of the figures above are just the first chapter in the story (~10% of the populations of UK and Spain have been effected so far), and are despite fairly strict lock downs in many cases.

edit: forgot to add a source https://www.worldometers.info/coronavirus/#countries

I think you are reading off the wrong column there - cases per million. Deaths per million in the States is 323. But if we had that death rate it would be around 1600 deaths.

@THE MAN 2 | 2nd Jun 20, 10:41am

"people dieting from Covid19" so Weigh-watchers would be very happy!

Chairman, their were plenty of people who have dieted through Covid19, and the fact is that NZ people are about the 3rd most overweight country in the world, it is well overdue!

"there" and "plenty".

TM2, stop adding whisky into your coffee.. you are drunk!

Chairman, Lol, flippen changing my words!

Maybe I should have another one or two

Are you up for a bit of property investing advice in ChCh, home of the skinheads according to you!

"Are you up for a bit of property investing advice in ChCh, home of the skinheads according to you"

Next time I am in CHCH, may be we should catch up for a beer.. I will listen to your sound investing advice, and then we can cruise around in your Range Rover to a skinheads hot spot..

Social distancing Chairman or we be ok?

Haven’t seen any skinheads or white supremists for over 10 years

You obviously do not know Chch.. let's have beer and come with me!

He certainly shows us his age and intellectual prowess on a regular basis.

Geez Gordon, what is this love affair with “the man”?

I think you have a love affair with yourself.

THE MAN 2 in love with THE MAN 1

I recalled he said he got a model material wife so no time for him to have a love affair with himself..

Mind you there are lot of model materials in Thailand but under the bonnet they are something else!

I suppose you could be right Fritz!

Certainly don’t hate myself that is pointless when I am providing a valuable service for people.

Geez Newshub taking "the glass full and spilling over the top" approach...

Yes life is so much better with a glass half empty attitude...

Yvil, what are your plans for the proceeds of your Ponsonby sale? Half full or half empty choice?

Mitigating the disaster of his slummy motel and Air B and Bs

gn made posts two weeks ago about stalking you be careful

Hahah. I just said his wife was hot. Anyway, he found me on FB last year, not the other way round. No one stalked anyone.

I missed the post about you stalking me… We found each other through a FB post from another poster here, remember? I asked you, given the nature of your comments on FB, if you might be Gingerninja…

PS, my wife being hot is nobody else's business on Interest

Ha. fair enough. I can't remember the exact context, but someone suggested you were a creep/loser/Casanova type and I disagreed and said you appeared happily married to a very attractive woman and wealthy. But you are right, it's no ones business. All the name calling just does my nut in sometimes. I have never in anyway doxxed or leaked your identity though (nor would I).

Thanks Ginga, much appreciated that you defended me on here. X

Of course I remember. The comment was me defending you actually not sure why HW refers to that as stalking. Je n'ai pas de mauvais sentiments envers Yvil. Je ne suis juste pas toujours d'accord avec lui.

"actually not sure why HW refers to that as stalking"

Based on the context of All of what you said here two weeks ago on 15 May GN. But I dont feel the need to reproduce it here so maybe we could just leave it there. If it's not stalking then I apologise but I think you should be careful discussing others and divulging their personal details.

HW, I can assure that GN is not a stalker, originating from Interest we got to know each other through FB and Messenger, she's one of he smartest person I know and I appreciate her intellect as much as her uniqueness, she's very far from bland. Whenever I go to... where she lives, I might even message her to meet up in person

HW, i totally agree on being careful not to divulge personal details. However, I don't believe I did divulge any about Yvil (nor would I) apart from saying that he appeared to me to be very successful and happily married or whatever it was I said, when others suggested otherwise. Yvil and I have known each other now for 18 months and neither of us have divulged personal info about the other. A lot of mud gets thrown around on here and even though I don't always agree with Yvil, I didn't want people making up some fantasy about him being some sleazy, wannabe loser. He really isn't. A lot of people take lot of flack on here and we all sometimes stir the pot too. That's just the nature of online comments sections though eh?

18 months... that's getting serious. Forgive me I didnt know that. There is alot of spiteful envy here on this website and I have been the target for some of it as has Yvil. So was thinking about his interests that's all thanks

You're being a total egg Houseworks, I remember those comments and GN didn't disclose jack. She was just checking someone who was personally attacking for no particularly good reason.

Say what you like moron there's no need to get on my case with your mindless name calling. I think I know what I'm talking about and could repost various comments here but if someone wants to go back and check they can. I have given the date. To add to that around the same time there were insinuations around a couple of other people too and gingerninja was right in the thick of it. My earlier comment to Yvil was with all that in mind and looking out for his interests. If someone posts here that Yvil has "a model looking wife (I know because I have seen her)" without any reference to personal contact that sounds pretty bloody dodgy. How could I have known about his personal messages with her eh genius. But now we do. Or "that he looks rich and successful" and we all know about the egotistical and spiteful envy here. Being stuck inside hasnt done you any good. Please reply.. I dare you....

You keep saying you won't repost her comments but yet you are doing so in such a way - very selectively - to paint them as being significantly more sensational than what they were. And to be particular, I wasn't name calling you, I was name calling your actions. You are BEING an egg. And I stand behind my name calling in that respect! Lol

Go and refresh your memory you brainless loser.

Wow

Hibiscus Coast listings 24% below where were a year ago. In 2017 the drop cf prev year was 32%. So this is no surprise. Bear in mind that around a third of RE NZ listings listed as “house or townhouse” ARE NOT any such thing as they are not built yet. These sit on market for 12-24 months or more til are finished. A useful exercise is to calculate % of stock OTM at any one time. And whilst doing so remember Auckland stock is up 13% in last 7 years whilst sales are down 32% in first 5 months of 2019 cf 2012. All this despite cont falling interest rates and rising immig. Simple: too expensive

FYI, New Zealand house price index for the last 46 years ...

Many house buyers get confidence that:

1) there is low historical volatility of property prices (say compared to shares)

2) property prices have not fallen by much historically, and when they have, they have recovered in a few years and

3) there has been a seemingly consistent historical growth in property prices.

As a result, many residential real estate property buyers are willing to use high levels of debt to finance that purchase, which may result in high debt service ratios.

i) From 1974 -2020 (46 years) the house price index went from 91 to 2,843. (i.e 31.2 x the original index value in 46 years). FYI, that is 7.79% per annum.

ii) So many choose to extrapolate this historical rate of growth of 7.79% per annum into the future. If that were to eventuate, the house price index in 2066 (46 years from today) would be 88,839 (i.e 31.2x today's value).

iii) to put that into context, that would mean:

- that the median house price in NZ would rise from $680,000 currently to $21,246,637 in 46 years

- that the median house price in Auckland would rise from $925,000 currently to $28,901,676 in 46 years

a) does that seem reasonable?

b) if so, what (if any) are the limitations from the house price index reaching this level in 2066?

(Note: for sake of reference, some property promoters frequently espouse that property prices double every 10 years - that is equivalent to 7.18% per annum.)

https://www.interest.co.nz/charts/real-estate/qv-house-price-index

Interesting to see the amount of well-read readers on this site who are certain about what will happen next.

If anyone were making such certain predictions about the stock market, price of gold, or anything else, everyone would see them for the fool they clearly are, but when people do the same for property, there is an echo.

If anyone were making such certain predictions about the stock market, price of gold, or anything else, everyone would see them for the fool they clearly are, but when people do the same for property, there is an echo

That being said, it would not surprise me if the gold price went up.

The governor of the Reserve Bank of NZ said last year the future of banking in NZ depends on those willing to step up and borrow. So, let the greater fool step up and borrow at these ridiculous prices to support the banking system. If you fall into negative equity, they will not support you!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.