Housing prices may have peaked in March and begun a slow decline, according to the Real Estate Institute of New Zealand's House Price Index (HPI).

The HPI for the whole of NZ peaked at a record high in March and then declined in April and May and is now 2.4% lower than in March.

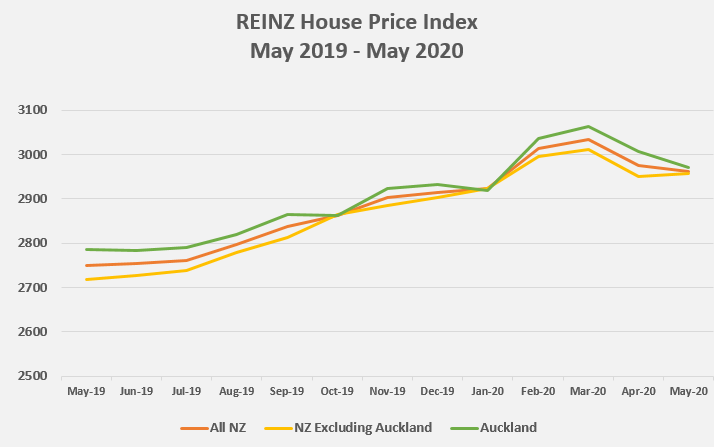

The graph below shows the monthly trends in the HPI for all of NZ, Auckland, and all of NZ excluding Auckland, from May last year to May this year.

The three sets of figures all show a remarkably similar trend, rising steadily from August last year to January this year, then rising strongly in February and peaking in March, before declining again.

The HPI was developed by the REINZ in association with the Reserve Bank and is considered a more accurate overall measure of housing price trends than either median or average selling prices, because it adjusts for differences in the composition of housing types that are sold each month.

The table below shows the movement of the HPI for cities and districts 28 districts throughout the country, from its peak in March until the end of May, and the percentage change in that time.

Of the 28 districts recorded, only four registered a gain between March and May: Papakura in south Auckland +0.9%, Rotorua +1.9%, Lower Hutt +0.2% and Invercargill +2.0%.

The remaining 24 districts all posted declines, with the biggest decreases occurring in Queenstown-Lakes -5.8%, Waitakere (west Auckland) -4.3%, Palmerston North -4.1%, Auckland City (the central suburbs that previously fell within the boundaries of the former Auckland City Council pre-amalgamation) -4.0%, and Upper Hutt -4.0%.

However, although the figures suggest a reasonably consistent trend, it should still be treated as a tentative one.

The real estate market was severely affected by lockdown restrictions in April and May, resulting in sales numbers that were well below historic norms.

It could take another month or two before it becomes clear whether the decline in prices evident in April and May was a temporary blip or part of a longer term trend.

Commenting on the HPI figures in a Home Truths newsletter, Westpac Chief Economist Dominick Stephens said the decline in prices was expected.

"New Zealand is staring down the barrel of a severe recession and house prices always fall during recessions," he said.

"We expect house prices to decline less severely than during the Global Financial Crisis, but more severely than the early 1990s or late 1990s recessions."

The comment stream on this story is now closed.

| REINZ House Price Index | ||||

| March - May 2020 | ||||

| March | April | May | Change March-May | |

| New Zealand | 3034 | 2975 | 2962 | -2.4% |

| NZ excl. Auckland | 3010 | 2951 | 2956 | -1.8% |

| Auckland Region | 3063 | 3006 | 2970 | -3.0% |

| Rodney | 2919 | 2987 | 2882 | -1.3% |

| North Shore | 3119 | 3088 | 3017 | -3.3% |

| Waitakere | 3247 | 3111 | 3108 | -4.3% |

| Auckland City | 2949 | 2855 | 2830 | -4.0% |

| Manukau | 3192 | 3181 | 3154 | -1.2% |

| Papakura | 3181 | 3297 | 3209 | 0.9% |

| Franklin | 3206 | 3098 | 3187 | -0.6% |

| Whangarei | 3114 | 3077 | 3108 | -0.2% |

| Hamilton | 3277 | 3138 | 3231 | -1.4% |

| Tauranga | 2851 | 2899 | 2846 | -0.2% |

| Rotorua | 3622 | 3584 | 3692 | 1.9% |

| Hastings | 3218 | 3049 | 3168 | -1.6% |

| Napier | 2917 | 2800 | 2878 | -1.3% |

| New Plymouth | 3222 | 3049 | 3153 | -2.1% |

| Palmerston North | 3223 | 3090 | 3092 | -4.1% |

| Wellington Region | 3039 | 2992 | 2971 | -2.2% |

| Porirua | 3126 | 2887 | 3080 | -1.5% |

| Upper Hutt | 3534 | 3402 | 3394 | -4.0% |

| Lower Hutt | 3320 | 3389 | 3325 | 0.2% |

| Wellington City | 2739 | 2733 | 2661 | -2.8% |

| Nelson | 2468 | 2541 | 2437 | -1.3% |

| Christchurch | 2480 | 2436 | 2426 | -2.2% |

| Queenstown Lakes | 2731 | 2737 | 2572 | -5.8% |

| Dunedin | 3740 | 3704 | 3649 | -2.4% |

| Invercargill | 3312 | 3349 | 3379 | 2.0% |

297 Comments

Can't wait for a certain commenter's (not so)humblebrag, for the 20th time :)

Also, any particular reason for Rotorua and Invercargil to be positive, or is that just noise?

Im going to say, all these figures suffer from low volumes over April and May.

We will see what happens over the next few months and then once the mortgage holiday ends, if its still heading down after all that, youre probably too late to get out unscathed

I can’t talk about anywhere else, but in the Hutt here in Wellington, property is going for insane prices. Friend of mine put an offer of 590k on a house, CV 420k September 19, in Stokes Valley. It went for 620k. Open homes are like a six60 concert, no room to move.

Before y’all start yelling at me... I would love nothing better than prices to do a massive drop. I think they are ridiculous. It just ain’t going to happen here in Wellington. Clearly there people with huge amounts of money/leverage who teams in unaffected by the mayhem of the black bat event, that is COVID19.

Just out of interest - what was the size of the section that the house was on?

Have seen property developers bid up properties in Auckland where there is a large section which can be subdivided.

You make a good point -

https://www.trademe.co.nz/a/property/residential/sale/wellington/lower-…

These property developers / landbankers buyers have very different economics, and hence are able to pay the highest prices - certainly higher than owner occupier buyers, and higher than long term tenant landlords.

Compare that to stand alone houses on smaller land sizes of say 400 sq m, or apartments. Property developers typically aren't interested in those as they are unable to make the economics sufficiently attractive.

So potential owner occupier buyers or long term tenant landlord buyers (and pre-COVID19, Airbnb landlords, and landlords to foreign student accommodation) of those properties are not competing with property developers. In the categories of remaining potential buyers, Airbnb landlords were the group to pay the highest price - thereby outbidding owner occupier buyers, once again.

If an Airbnb landlord was not interested, then the next highest bidder would be long term tenant landlord buyer or landlords to foreign students. Once again outbidding owner occupier buyers. Typically owner occupier buyers can only afford to pay the least.

It's only when a property is financially unattractive to

1) property developers / infill developers

2) Airbnb landlords

3) long term tenant landlords

4) buy and add value property traders

that is when there is less buying competition for owner occupier buyers. Owner-occupier buyers may be able and willing to pay more than property traders (renovators)

I'm a buy and hold investor. Your comment doesn't reflect my purchasing experience. I can only afford to purchase once every 5 years or more. When I make a purchase, the property has to meet a number of my predetermined rules, or I move to the next opportunity. As this is a business decision, I don't have the same emotional attachment to a property as a young couple looking to buy their first home. I avoid auctions, as I will always be outbid by a first home buyer who is bidding based on emotion. I generally have to find a run down property in need of renovation that is less likely to have the dream wow factor when purchasing. It would be interesting to hear from a first home buyers experience. I wonder if the houses they have missed out on were actually confirmed as purchased by an investor, or that was simply an assumption? Being outbid by investors certianlly makes for great click bait, but it would be nice to see some actual data on the subject.

Every time FS, every time. First was the wave of money out of PRC, then by what appear to be NZ investors, after that wave broke with the FBB.

How do I know they were from the PRC, the REs said they were.

FS,

Thank you for sharing your experience with us.

Your points are very valid. Totally agree that at some price level, cashflow oriented investors may be outbid by owner occupier buyers, if the rental yield is too low and the numbers don't make financial sense.

This is common in areas where rental yields are low.

Or a buy and add value investor where there is a major fit out cost.

Fully agree with your point about owner occupier buyers developing an emotional attachment to the property and willing to pay higher prices.

I was unclear - the two types of purchasers I had in mind above were:

1) a first time buy and hold investor who is capital gains oriented (who is using deposit recyling / equity release financing from their home and hence uses 100% debt financing & willing to purchase a negative cashflow property), and the property is kept in its existing state (i.e minimal renovation or improvements) with

2) a first time owner occupier buyer who is financed with an 80% LVR

Yeah - that's my thinking towards Wellington. There's still a frustrating low levels of listings. I just don't see prices being affected here. But I would love more than anything to be wrong.

That said, things are still being propped up and listings are typically low here in Winter (because you need some belief your home isn't dark/damp). We'll see what happens come Summer. We're giving it until start 2022, if there's no change then it's time to leave.

I reckon you guys are bang-on the money.

If there’s any “recession” in the Wellington housing market, it’s destined to be “short and shallow”.

Generally, the closer to the CBD (in both Wellington & Auckland) the higher the capital appreciation and rental yield of the property - except for “shoebox apartments” which are a trap for the uninitiated.

Best wishes with finding your ideal property!

TTP

That's rubbish. At least in Auckland, yields on expensive inner suburb properties are usually pathetic, 3% or lower.

I suggest you stick to what you know ie. The Manawatu.

FYI, on a property investor forum, just saw a comment by a property investor asking about Property Brokers in the Manawatu who are offering rental guarantees to landlords in their property management business ...

Would any potential client of that business like to made aware about the consistently disrepectful, name calling, belittling & toxic behaviour of a certain individual rumoured to be associated with that business? Is the character of the business owner relevant in assessing whether the guarantee promised would likely or unlikely be honored if required?

If that potential client asked for payment under the promised guarantee, would the business owner possibly engage in name calling, belittle the client, and behaviour that is disrespectful? Should that potential client be fully informed and be able to make a fully informed decision?

Isn't it funny how Karma works in mysterious ways? ...

Will be interesting to watch what feedback that questioner gets ...

A interesting response to the questioner ...

"I'm with PB .... Not impressed. At all."

Sorry but not sorry TTP, every time when I see your higher rental yield of the property based on location. I just feel that I have to post this link here:

https://www.tvnz.co.nz/one-news/new-zealand/change-landlord-s-tenant-ma…

My theory is simple, it all comes down to affordability. If tenants couldn't afford, landlord rental yield will fall. If their salary can not keep up with rental price, option 1: find another property. Option 2: if they can not find another property, they will move to another city.

We will do the same, but are looking at end of this year to mid next year. If we can leave at that stage and Wellington prices aren't at semi sane valuations, we will be heading back to China, most likely. At least there you have an economy with oppourtunities and no shortage of houses to buy. Sure valuations are a bit batty, but my few 100k of deposits I have here can buy me a relatively luxurious apartment there in a lower tier city pretty easily. Just a pity NZ would miss out on the 100k+ of tax per year us as DINKs are providing. But as the tax and welfare systems here are completely broken, there ain't much point staying...

Another guy I know in IT (and his wife a top Business Analyst) moved back to the US in Dec because of the lockdown... this follows another couple who moved back to the US last year too and another guy that moved to Aus. All top flight IT people who couldn't get a house in NZ... none of them going for OE's either, in their 30's and 40's, frustrated at NZs lack of progress on pretty much any "crisis" we have. All of these people were replaced with young immigrants, mainly from Eastern Europe or Asia, all of which (having worked with them) are of dubious quality, but are a lot cheaper, I am sure.

This country is going backwards so ridiculously fast, it's not funny. I am advising many of the young people I know to get the hell out of here, no decent jobs, no hope of a future, it's basically been stolen by the old, rich, conservative incompetents who can't see anything wrong.

"stolen by the old, rich, conservative incompetents"

You've got that wrong bobbles, good jab although I dont fit the label. You need to open your eyes wider

Of course it is. Overwhelmingly old people have voted for the current mess. They refuse anything that will not result in lower house prices, have no idea how to grow productivity, are quickly burning the environment down at the expense of the young. When this is presented to them with objective evidence, you are met with a barrage of irrational arguments that try to distract and divert the issues away from themselves. Zero leadership, a lack of real world skills, narrow minded, parochial numpties who can't understand that building a better world for the next generation is actually helping themselves.

Having lived in quite a few different countries in Asia and Europe, my eyes are wide open. I have seen things done right, wrong, upside down and backwards. This country stands so still for soooo long, then wonders why everyone else in the world is in front of them. And it's clearly certain generations benefiting at the expense of the young. All so they can retire nicely with their 1-50 rentals, have debt slaves running all their services for them, crow about how amazing they are at being born at the right time, drive their Audis around and then blame everyone else when they don't get what they want (like a good healthcare system/environment/respectful society etc).

I suggest you open your eyes, there's a reason more and more sites like this are popping up: https://e2nz.org/

You did your research beforehand so why did you come here ?

I was born here, I have an automatic right of return.

Doesn't mean this is a great place to be, unless you are one of the cohort who has benefited from the current regime, it is most certainly not a place to have a good life if you are young to middle aged and are highly skilled.

One of those who left to see their fortune.

"it is most certainly not a place to have a good life if you are young to middle aged and are highly skilled."

Complete bollocks, as far as I'm concerned you can go back today and find other greener pastures

Have you lived outside of NZ, Houseworks?

Blobbles - "certainly not a place to have a good life if you are young to middle aged and are highly skilled"

Wife and I are in that position, and completely agree.

Why would I want to live outside of godzone. Family in aust are no better off actually worse off than the family members who stayed on this side. We have family in Europe and we talk to them all the time through SM and can visit anytime we like. I suppose you think you have to live overseas to get a perspective of what it's like.

"I suppose you think you have to live overseas to get a perspective of what it's like"

In my experience, there is a huge difference in mindset and perspectives on the individual between:

1) travelling abroad for overseas holidays

2) living abroad for a period for more than 12 months or more

Many commenters who are in category 2 above are more likely to understand the differences on a person's sense of perspective. There are many of this category in this community.

But apparently those of us in category two "have to open our eyes".

Our eyes are wide open. It's the parochial ninkumputs in this country that are blind to the outside world because they haven't experienced it. They don't realise the effect it will have as more and more highly skilled people leave. Which goes to show you how blind they really are...

"I suppose you think you have to live overseas to get a perspective of what it's like"

Well it helps.

Especially when you're telling others to open their eyes.

Of course it is to you. Let me guess, you own multiple houses so have enjoyed the ride of the last few decades?

I doubt I will get an honest answer to this.

We are planning some property developments so are in actual fact increasing supply. I also have a trucking company and it's a good life getting paid to look out a window :) yes I'm mid age but not a boomer but sometimes call myself one as it's better than being an X

Sorry blobbles but if you are highly skilled and no doubt spent time overseas earning the big bucks then I find it surprising that you are not able to have a comfortable life in NZ now. Blaming a different generation for your perceived difficulties just closes your eyes to other opportunities. Are you able to replicate what your parents did? Probably not as times have changed, but there are many other ways to build an asset base that fits yours beliefs. Totally agree that past and current leadership regardless of what party has been in power has been totally lacking in vision but whining about it does nothing to change the future

I find it pretty astonishing that nearly every time a poster on here explains just how much they have been affected by the rapid increase in house prices and what it has done to them and their plans and their family, they get accused of 'whining.' I suppose it just makes people pretty uncomfortable to have it pointed out that something that has benefited them has actually come at huge cost to the generation of kiwis coming up behind. They'd rather not face that fact.

This is why I've been attempting to warn older generations that there could be a time that they regret their self interest and lack of humility on these matters. They are slowly losing control, despite owning most of the assets. The riots in the US should be a warning of change in the air and the 'have nots' willingness to change the system. And you can't lock them all up for not continuing the play the game that is rigged against them. They want the rules changed.

Isn't the difference between

1) the people who are multiple property owners who have large amounts of equity and

2) those that are not in the category above

I know people who are older who do not own property and do not have financially secure circumstances. There may be more older people coming into this category as a result of COVID19 and loss of job (with a high mortgage), or a highly leveraged business owner who will be shutting down their business (e.g in Queenstown)

That's very interesting Blobbles. I think there is something rotten about NZ as well, but this isn't the place.

We had to move back to Perth Blobbles... we saw so much poverty in NZ it wasn't funny. People couldn't afford rent let alone mortgages. I made half the wages then I did in Perth, but everything was double the price to just live. Trying to save $150k for a deposit was absolutely ludicrous..You wonder why professionals like myself and many other of my Uni friends are having to cross the ditch... we are priced out of the market by greedy huias... its truely a society of the the have mores (top 1%), the have nots (99%)....

Yes and you might be able to explain to people that house prices don't always rise BacktoPerth.

I understand houses there peaked there a long time ago and have been stagnant or falling ever since? (like at least 10 years)

https://www.macrobusiness.com.au/wp-content/uploads/2013/05/04.gif

{kind=link}

Completely agree Blobbles. Your observation lines up with my own. I've a lot of international friends/couples, in their early 30s and also DINKs, all looking at leaving within a year or so. All becoming increasingly frustrated. Housing being the number one issue. I wonder if Wellington will be a victim of it's own "success"over the next two years (if you can call it success). Each of these couple all turning over around $100k tax (plus gst) annual.

I monitor house listings back home (in England), in particular areas we like. Every day I'm seeing more and more listings and more and more "reduced price"tags. Good warm solid homes.

I’m in the same demographic and share your frustrations. In fact we had already arranged one-way tickets out of Wellington (and NZ) prior to C19 for this very reason.

Whether we stay committed to Wellington (and NZ in general) hinges entirely on whether we see a correction in housing.

You’ll likely see similar conditions in most open market economies.... all the printing has, and will continue to, drive up asset values

Until inflation appears and interest rates regulate under a period of stagflation

There has been a disconnect happening in prices for a while. Houses in the typical FHB price range (largely outer suburbs and satellite cities) keep going up, but properties in a slightly higher price bracket (more central) have been pretty flat, and have now started declining from what i've seen.

Interesting point... I'll pay closer attention to the next higher tier.

Now let's just hope the free market do its thing.

Let's hope the RBNZ/Govt lets the free market do it's thing. They haven't seemed too keen to let that happen so far.

I don't know. All things point downwards, but then we see the stock markets. I want to believe, but I find it hard the market is free at all.

The likelihood is that house prices will fall by a much lesser amount than certain individuals here wish/hope.

The long-term trend for house prices in NZ will remain upward - as it has done since reliable house price statistics were first collated (well over a century ago).

Some people seize the opportunity to buy into the housing market during periods of price weakness......

But, alas, as we have seen here, others lack the initiative/wherewithal...... and suffer from terminal disaffection. )-;

TTP

Are you talking in real terms? House prices provided zero real returns for about 100 years.

Don't let facts get in the way of his narrative

Hi Independent_Observer,

Not when you combine capital appreciation with rental yield. :-) Given your affinity for boasting about your property acumen, I'm surprised that you would "overlook" such an obvious (and critical) factor.

Housing has proven an excellent investment - especially for those who are in for the long haul.

Go chat with any retiree/senior who's invested in housing through the years/decades......

TTP

Precisely TTP.

Any retiree/senior who has invested in housing though will have had what is likely an exceptionally lucky run through the housing market. It's not at all obvious that someone investing in housing now will experience the same. To take an example, one retired couple I know bought a house in 1980, and the house is now worth 10x what they paid for it. In order for the same house now to be worth 10x what it was bought for if sold at today's prices, it will need to sell for $8M in 2060. This is a fairly ordinary 3 bedroom house is well, and it's not in a spectacular location or anything. That seems highly unlikely.

Exactly - a long period of declining interest rates has been the main driver. In the absence of rising incomes this is the only way anyone has been able to pay ever increasing amounts as houses are traded back and forth. Interest rates now have limited room to move further downward, so I can't see real estate being a great investment in the coming decades.

Declining interest rates would have had very little effect on prices if, at the same time land, consenting, and infrastructure restrictions had not increased.

This can be seen in general in that lower interest rates did not cause car prices to increase, and especially in other jurisdictions where interest rates were lower than in NZ BUT they had few restrictions, housing remained affordable.

If you can remove the restrictions at the bottom of this bust (whatever that goes to) then houses will become far more affordable going forward, although won't be great investments for those that bought prior and their debt exceeds their equity.

Any return will be on yield rather than capital growth.

You can't compare cars with land.

Yes, you can as they both follow the same principles of supply and demand, and they do in practice when the same marketing conditions exist.

In NZ not too distant past, cars also followed the same restrictive price increases when we had quotas and import supply licensing.

Right - we'll agree to disagree on that one. I can claim depreciation on my business vehicles (i.e. they lose value with age), but I can't claim depreciation on land (because generally speaking it inflates in value in line with money supply - but within constraints of lending and interest rates) nor buildings now. That is because they are different types of capital assets. Companies can always enter the car market and compete to build cars at the market equilibrium point. Companies cannot enter the market to build land. Unless we're going to start building new islands or land masses for real estate? But the price would be far to high so return on investment would be bad - and where would the land come from? I'm assuming you would need to bring it up from under the water. Perhaps that is the solution - underwater housing communities...I have read articles about that before! If the land bankers don't want to release their land, just start building 30m down in the Hauraki Gulf.

Well, then you are also disagreeing with Evans, Cheshire, The NZ Productivity Commission, etc.

But I see by the end of your comment you agree with me. 'If the land bankers don't want to release their land.' So you acknowledge that land banking occurs (an artificial restriction) which means higher prices, cause other more expensive options to be considered like you are suggesting, 'just start building 30m down in the Hauraki Gulf.'

You will find it far cheaper to just remove the restrictions land banking causes. Housing will be far cheaper and interest rate falls won't feed into house price increases.

This is the reality in other jurisdictions where they have lower interest rates, land prices are not only lower, but the price of land overtime is not affected by the interest rates.

Where there are restrictions eg land banking, then any savings that interest rates give people is captured by the restrictions within the system. That is why we see the price of sections within months of an interest rate cut increase by at least the price of the interest rate saving, if not its LVR multiplier.

You don't even need more land than we have, you just need to stop it being drip feed out at the rate that is less than the market needs it.

Ok cars and land is like comparing chalk and cheese. One is a depreciating asset with a short life. The other has an infinite life period and generally speaking, appreciates in value (even go ask your accountant or the IRD - no land or property depreciation). Every car I have purchased has depreciated in value every year I've held it, regardless of interest rate movements. The land that I have owned has generally appreciated in price - although I did live through the GFC so I know that property prices can fall if the market becomes irrational!

If your cars haven't been falling in value each year you own them, you must drive around in collector cars. I'm very much jealous!

Property prices go up more based on irrationality than they go down. And as both Ex-expat and myself point out on adjoining comments, car prices have gone up on even second-hand cars vs new, all because of restrictions that are man-made. And what makes collector cars increase in value is their scarcity relative to demand.

The improvements on the land depreciate, whether you can claim it or not, is another man-made regulation.

Your argument about price increases is solely based on the low-interest rates. The evidence shows that low-interest rates do not matter if the land is supplied at the rate of demand, and the only reason it is not, is restrictive regulation.

And the issue is not about the land per se. If the land had fewer restrictions, then the council can also apply restrictions on consent processing, infrastructure supply, or it could be the availability of nails.

Or the interest rates, as all they represent, is a saving. The saving could be labour time (less cost to build) with more efficient building systems.

In multiple component systems, any saving on one of the components will be captured by the other restrictions.

And this is why house prices in NZ continue to rise, while the quality is falling relative to other countries.

Ok our understanding of supply and demand differs - all good.

We also had restrictions on car financing. In the early 80s, it was not unknown to pay more for a used car than a new one (Hondas in particular), as supply was limited and the finance deposit requirements were far higher for a new car. I think it was 66% deposit for new, 50% for used and 33% for commercial (Mazda 323 station wagons were popular as they were classed as Commercial). Imagine having free motoring where you buy a new car, then trade it in a year later and get another new one for little/no money. The dealer makes the money on the used car sale. Japanese used imports blew that situation out of the water.

Yes, the same market forces are at work as to how we supply (limit) land. And even today, the price of our cheap Jap imports is directly related to how the Japanese have more restrictions on their car owners the older their cars are so they are devalued at a rate that makes them almost worthless in Japan, but can still find a market in a country like NZ that has no local car manufacturing industry to protect.

Car prices, like land prices, are simple supply and demand dynamics. With the biggest limiting factor being manmade regulations, not the actual resource.

Yes exactly. Would the usual suspects care to comment on how they expect this to continue?

If you push them hard enough, they can't answer you . The key drives for property appreciation here have been driving interest rates to zero, high immigration and banks allowing people to use equity in previously purchased property in order to buy even more properties!

Its not wages, if it were my salary would have been doubling every ten years, but it hasn't been - and in the end its peoples wages that must pay the debt - either via rent or directly to your own mortgage. Property has had a dream run the last 20-30 years - I'll absolutely admit that, but the wise generally know when something starts to become too good to be true.

Incomes do rise though?

Wages doubling every 7-10 years for the same position and experience? What industry is that?

wages dont double that often and I didn't say they do? effectively, assuming interest rates remain stable, over very long periods of time housing should grow in line with nominal gdp.

This is where the 2% inflation targeting does my head in as we push interest rates down to avoid deflation, but means lending rates drop and house prices, not included (thoroughly) in the CPI basket go through the roof. We're creating our own demise. If house price inflation was included wholely and as a significant factor in the CPI basket, rates would have been going up the last 10 years, prices would have stabilized, debt levels would be much lower and we'd be in a far healthier position than we are. Its like a blind person tapping around the room looking for a door, but don't realise they're standing outside and there's a cliff nearby. Painful to watch.

This is a critically important point IO! Very rarely is this mentioned by analysts or commentators. The only tool (the CPi & OCR) used to control inflation is artificially constructed with a major fault in that it actually inflates accomodation costs.

Maybe not so much in our new reality.

Absolutely - but if you compare the house price to household income ratios over the last 30 years, the two lines are getting further apart and the only thing that has allowed that to happen is driving interest rates to zero. We're there now....i.e. we're at zero. What allows the lines to get further dislocated for prices to go even higher? (nothing is the answer to that question if you didn't figure it out).

Wages should absolutely be rising, particularly for the vast majority who are not fairly compensated at all. But we have been loaning wealth into existence from nothing, among other things that contribute to this insanity. Wages are not going to be able to catch up to the current housing prices. We've allowed them to balloon beyond all reason, and somehow expected to be able to continually hand this mess down to the majority of income earners, whose wages cannot support it.

A number of leading economists think we're heading towards stagflation. I.e. rising price level/inflation but stagnant wages.

Well put.

al123, Stuck@home, Quiet desperation

When I first bought my house ($59,000) average houses at more than $100,000 were incomprehensible.

My parents bought their first house $9,000; they felt for me at $59,000.

My grandparents built their first house for £250 ($500). They would not be able to comprehend houses at $700,000 - fourteen hundred times that.

Don't get hung up in the present; open your mind up to possibilities. :)

And oh, right up to the 1970s mortgage rates were around the 3% so go figure what my grandparents thought of a house my parents bought at $9,000 - 18 times what my grandparent parents paid only a generation later.

I'm trying to open my mind up to this possibility, as you put it. I would still like to know, how exactly do you see this continuing? Pointing at the past only does so much to help one envision this continuing infinitely.

If you talk about property with anybody in NZ in the 50-70 age bracket, who hasn't lived overseas, they appear to suffer from severe hindsight, recency and confirmation bias.

If you have the same conversations with people from the likes of the UK, Ireland, Spain, USA or Japan they understand the real risks of elevated property prices. Not here.

Very true.

"If you have the same conversations with people from the likes of the UK, Ireland, Spain, USA or Japan they understand the real risks of elevated property prices."

Because they experienced a significant drop in property prices firsthand recently.

For most people who have never experienced a significant property price fall firsthand, the thought of a significant property price fall occurring is outside the realm of possibilities.

If you had those same conversations with people in the US, Japan, Ireland, Spain, etc BEFORE property prices subsequently fell, the thought of property prices falling significantly was outside the realm of possibilities. That is how property prices reach levels with such elevated price risks.

Cause of the housing and credit bubble in US

From the May 2010 FCIC interview with Warren Buffett, a reknowned investor and Chairman and CEO of Berkshire Hathaway

MR. BONDI: As I mentioned at the outset, we’re investigating the causes of the financial crisis. And I would like to get your opinion as to whether credit ratings and their apparent failure to predict accurately credit quality of structured finance products, like residential mortgage-backed securities and collateralized debt obligations, did that failure, or apparent failure, cause or contribute to the financial crisis?

MR. BUFFETT: It didn’t cause it, but there were a vast number of things that contributed to it. The basic cause, you know, embedded in psychology –- partly in psychology and partly in reality in a growing and finally pervasive belief that house prices couldn’t go down and everyone succumbed –- virtually everybody succumbed to that. But that’s –- the only way you get a bubble is when basically a very high percentage of the population buys into some originally sound premise and –- it’s quite interesting how that develops –- originally sound premise that becomes distorted as time passes and people forget the original sound premise and start focusing solely on the price action.

So every -– the media, investors, the mortgage bankers, the American public, me, my neighbor, rating agencies, Congress –- you name it -– people overwhelmingly came to believe that house prices could not fall significantly. And since it was biggest asset class in the country and it was the easiest class to borrow against, it created probably the biggest bubble in our history.

Yes for anyone here who wants to understand market psychology have a read of Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters for Global Capitalism by Shiller and Akerlof. It will help you make sense of what is happening - who is acting rationally and who is not. At this point I'm not sure if I can include central banks in the rational camp any longer which is a real worry.

you cant read a book and expect to know anything accurate. books are a closed forum, where you get to access the reader free from opposing views. There are strong mitigants to animal spirits, efficient markets for example. I mean i love shiller but just pushing shillers argument is bias and shiller has often himself been incredibly wrong. There are studies freely available from these guys and you can see them go back and forth and fight maths with maths. Books are lazy.

I don't subscribe to efficient markets hypothesis (EMH). Here is one such example.

https://markets.businessinsider.com/news/stocks/hertz-stock-price-sell-…

These are called anecdotes. Efficient markets is a model, and models are not perfect. But in order to defeat efficient markets you must produce a forward-looking model that outperforms it. please only post journal articles, I do not care for tabloids. Shiller has not been able to produce a functioning model that defeats Efficient markets and, of course, Shiller teachers efficient markets.

Ok. I'll leave you to EMH. Good luck.

Laminar - yes agree the efficient markets provides a good basic understanding how market markets should function. I've watched Fama and Shiller argue it out and each makes their point. I've watched Shiller and Taleb discuss markets as well. Again each has their point. I think its about pulling it all together.

The requirement that humans are rational for the efficient markets model to be true is probably its greatest downfall in my view. I think the behaviour financial (the psychology) plays a much greater part in markets than what Fama acknowledges.

Fama freely acknowledges the issue. What bothers fama so much is that he understands psychology is a factor but can not create a model that demonstrates this. Shiller is not happy about it either. And it's not a basic understanding, efficient markets is probably the most accurate and well developed working market pricing model in existence. That's why it's so fascinating that it is both clearly wrong but yet no one has been able to touch it in terms of a superior model. My point is that you shouldn't push books as they are a closed forum.

Ok your view on books differs to mine (again that is fine). I think they can really expand peoples thinking. Obviously its important to read multiple sources on any given topic to get all perspectives - its what you don't know that will hurt you more so than what you do know. Books help with blindspots for me.

If you have any suggested readings I'm always looking for new things to look at. I'm just finishing up on Benjamin Graham by Walter Isaacson. Very intersting to get a founding fathers take on what America should be, compared to what it is today.

Sure. I think the most interesting stock debate taking place today is the value premium:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3525096

Thanks for the link - will have a read tonight.

That's why I read lots of different books there Laminar.

And remember Shiller has a nobel prize for his work on asset pricing - but if you want to dismiss his views that is fine.

I personally don't assume I know better than a person with a nobel prize in a given field. Most of the property investor types in NZ think they do however. I think a test of intelligence is knowing what sources to trust. If its NZ herald or OneRoof fine, or if its the likes of Taleb, Akerlof, Shiller, Kahneman, that is also fine. It will just give very different levels of perspective on the same topics - e.g house prices.

You shouldn't put words in my mouth. I openly stated that I love Shiller. You should not push books in the same way you should not push tabloid articles, you should push studies and debate. You were pushing Shiller without note of Fama, that's misleading.

Fair point.

What line of work are you in? I'm just interested because, by and large, I agree with, or am intrigued by your views. I, however, am far less well-read, and I work in the medical field. I'm just wondering if this is a hobby of yours, or if you work in... I don't know... finance or something.

Yes, I guess the prices themselves aren't a particularly good measure - what matters is not so much the sticker price, but cost relative to income. To use the same example case, the house I am thinking of was 4x a single professional income 40 years ago, and is now at least 8x. If the same trend continued, in 40 years it would be 16x a single professional income. That seems pretty unlikely. Of course any of us could be wrong about this, but it seems a lot more likely to be that the past 40 years have been an anomaly with regards to house prices rather than a reliable guide to the future.

Affordability index is a much better indicator that median income. Another factor worth including is lower income tax rates. Also think household incomes have grown exponentially since then. You're wasting your time if you ignore the full picture

Houses at more than $100,000 were incomprehensible until inflation kicked in and everything tracked up at a rate of knots.

Excellent summary P8. Correct me if wrong, from those prices I deduce that you bought in early to mid eighties, your parents early 1970s and therefore your g-parents in the 40s or 50s. Though the exact dates arent important, these prices show a clear increment from the previous generations level going back decades. What I dont understand and perhaps you can enlighten is why interest.co commenters talk about capital gains only occurred since the 80s. I assume its because that's the extent of their recollection or otherwise it suits their narrative

As discussed above, the prices themselves don't really show anything. What does matter is the buying power afforded by income. The reason I started with the 80s is because that's when the people talking about how housing is such a good investment usually start. The reason (I assume) that they start there is that the 80's in when house price to income ratios started going up and up. From the 50s - 80s house price to income ratios were pretty stable. I don't think we have good data prior to that.

I have seen many property investors develop their future property price growth expectation by extrapolating the past property price history. This is similar to Printer8 's approach above.

That is how Ashley Church developed his property prices double every 10 years.

They are effectively using the rear view mirror to drive their future property price expectations. This may prove to be incorrect when property price risks and property valuations are elevated.

My question was to P8 if you like you can answer my question to you at 2.05 al123

Sure - but you also asked why 'interest.co.nz commenters' start in the 80s, which I just had above, so explaining why seems to be a relevant contribution.

With regards to your 2.05 comment, of course you're right - it's tricky working out affordability, and there are lots of considerations (student loans vs higher tax rates, higher interest rates vs. lower sticker prices, etc). One that always particularly annoys me is that house price to income ratios are often done based on household income. But whether that household income comes from a single earner (as was pretty common in the past, but is very uncommon now) matters a lot, because if it's from two earners there is a very good chance that a large part of the second income is going to go on childcare for a decent chunk of time.

Stop it - al123....Houseworks wants somebody to reaffirm his hindsight, confirmation and recency bias a bit further.

"Housing has proven an excellent investment - especially for those who are in for the long haul" when rental yield is dropping?

https://www.tvnz.co.nz/one-news/new-zealand/change-landlord-s-tenant-ma…

lol, retiree/senior didn't have covid during their time...

That's because of what's just happened here - not what could happen in the future. Its been a dream run the last 20-30 years, I completely agree. But between 1900 and 1990'ish weren't fantastic - sure recently they have been - agree with you on that point.

Just be cautious about your hindsight, recency and confirmation biases on the subject is all I'm saying. If I were reading a university text book on biases/heuristics (and yes I've read a few) you (and a few other posters) fit the classification perfectly. And its those biases that get people burnt - assuming the future will look like the past.

Yes, residential property prices have provided good returns in recent years. And that may have resulted in the formation of return expectations for the future by many residential property investors - many use extrapolations from 50 years of property price history (such as this https://www.interest.co.nz/charts/real-estate/qv-house-price-index).

The key question is can these returns be expected to continue into the future from current house price levels? Future returns should not be based on looking in the rear view mirror but focusing on the windscreen and what is ahead. What has been good in the recent past, does not necessarily stay good into the future - that is the nature of cycles.

Some real estate markets to note :

i) note how prices prior to these periods showed a seemingly consistent upward direction - many people used these and extrapolated historical price changes into the future to develop their future price expectations.

ii) then something unexpected happened

1) residential real estate in Ireland circa 2005/2006 - then house prices fell over 50% (and still haven't recovered to their previous peak over 14 years ago) - https://tradingeconomics.com/ireland/housing-index

2) residential real estate in United States circa 2005/2006 - then house prices fell 27% - https://fred.stlouisfed.org/series/CSUSHPINSA

i) residential real estate in Las Vegas circa 2005/2006 - then house prices fell over 60% (and still haven't recovered to their previous peak 14 years ago) - https://fred.stlouisfed.org/series/LVXRNSA

3) residential real estate in Spain circa 2005/2006 - then house prices fell 26% or thereabouts (and still haven't recovered to their previous peak 14 years ago) - https://tradingeconomics.com/spain/housing-index

4) residential real estate in Hong Kong circa 1997 - then house prices fell 55-60% - https://tradingeconomics.com/hong-kong/housing-index

5) residential real estate in Singapore circa 1997 - then house prices fell 40% - https://tradingeconomics.com/singapore/housing-index

6) residential real estate in Japan circa 1991 - then house prices fell by over 45% (and still have recovered to their previous peak almost 30 years later. They are still at least 30% below their peak almost 30 years ago) - https://fred.stlouisfed.org/series/QJPN628BIS

Yip I look at charts like that and simply crap myself and the potential downside risk. As a country we could get absolutely smashed by this. There's the 1975-2000 trend in nominal price appreciation - then there is the hysteria 2000-2020. Its the growth of the last 20 years I'm worried about, as its about a 50% fall to the longer term trend.

The gold bug is at it again ... "real terms?" His gold graphs he shows unadjusted

I'd just like to point out to everyone that I'm not a gold bug. I'm a diversifited investor that includes cash, bonds, shares, commercial property and yes a small amount of commodities including gold and silver. EDIT: forgot foreign currency!

Houseworks - quit with the BS narratives that are false, in an attempt to belittle people and dismiss peoples views.

Respectfully..

Struck a nerve! And good sidestep

Ouch yes you got me....just off to find the panadol...the pain!

You will remember for next time then that apples go with apples and oranges with oranges. In other words dont tell BS about the unadjusted gold price and then insist others show real prices.

Please take my apologies for not providing you with the data! But please share it with me if you want to. You can always help by providing links to charts etc if you want to make a point.

If you make a point at least be consistent

You can always do some research and send links if you have a point to raise. I'm here to learn as well so if you have something to share please do.

IO

Even if house prices are only increasing at the rate of inflation for no net real return, have you considered the significance of equity leveraging against mortgage ??

Equity leveraging is often overlooked.

Inflation 3% and house prices up 3%; however if one's equity is 40% then one's house equity increase is 7.5%.

And . . . yes, short term house price falls equally accentuated but as seemingly accepted we are talking long term . . . and, yes, there is mortgage interest and rates, maintenance etc but that soon falls well below equivalent rent.

The alternative is to rent. However it is very, very simple: landlords do not invest in property for social housing reasons. Your landlord does not love you enough to provide social housing, they love you just because you will be providing a return on their investment, paying their mortgage off, and they walking away with that CG.

You continue to assume house prices always go up. Leverage works in two directions.

IO

if you are, then keep renting. Your landlord loves you. :)

You're right they do - because I pay, don't do drugs or turn their property into a p-lab.

IO

I understand that it the past few years have been frustrating for potential FHB.

As I post below (albeit it long post), there is currently significant change and there is need to adapt and look at one's future.

For those potential FHB who are frustrated, then the future of house prices may provide an opportunity in terms of affordability issues.

Potential FHB need to be looking to seize the opportunity and should be looking and working towards that. The decision to buy a home is - and never has been - a spur of the moment decision that takes a month or so to implement. It is a decision that may take a year or so to achieve and it is important to put factors that are mental blocks aside and focus on how and when one can achieve that.

Something I learnt playing rugby; when preparing to play a strong side, one never got bogged down about how strong they were, rather one planned how to beat them. Soppy I know, but a principle I try to apply.

Don't we all live the same country though P8? You would appear to be saying that there are two sides to this...like FHBs vs investors for example.

Those with the wealth should be humble in their approach and providing fair opportunities for future generations. Instead they've trying to suck everything out of the system for themselves and leave future generations with all the risk and debt.

How and why is that fair? Shouldn't they just all revolt and change the rules of the game if the game is rigged. This is why I think we're at risk of some form of revolution away from this neoliberal capitalist system that your generation thinks will last forever...it won't.

Yes, that's why I dislike this 'game' analogy that a lot of posters seem to be using. The whole point of the rules of a game (like rugby) is to ensure that the competition is reasonably fair: if the rules clearly favoured one team, it a. wouldn't be very fun to watch and b. the other side just wouldn't play. But if housing is a 'game', then it's obvious the rules weren't put in place to ensure fairness, and it's one we're all pretty much forced to play, rather than one we can simply walk away from. Given that, there's no reason why anyone should simply accept the rules and get on with it, as a lot of posters seem to be suggesting.

IO

Some good philosophical points there.

Life is about personal opportunities - so yes, I suppose one can consider life much like a game in which one makes the most of opportunities open to them.

You seem to be well educated person and hopefully no doubt in a good paying and clean comfortable job. You seem to have made the most of your opportunities so far - and I admire and don't begrudge you that and wish it for my children and grandchildren. However, are you sucking more out of the system than the cleaner on the very minimum wage and hours that cleans your office and toilet? Is that fair? Is it morally wrong that you (or others, if necessary) who have worked to become educated to have the comfortable, clean and well paying job?

Yes, house prices have seen rapid inflation resulting in affordability issues for FHB. But FHB are not the only current casualties of the low interest rates; equally those retirees who planned on a certain level of income from the safety of term deposits have also suffered having their income severely impacted upon.

These consequences are the results of the RBNZ and other central banks trying to maintain (whether to be proven to be eventually successful or not) economic stability; their actions were primarily meant to provide support for businesses and consequently jobs. Should the RBNZ and government not have taken the action it did post GFC and Co-vid? So what was it to be - low interest rates with housing and equity inflation or jobs losses and a slow down in the economy??? That is not a cop out - rather the fundamental reality of what has and is happening.

So is Co-vid current support fair? Are you providing fair opportunities by leaving future generations with all the risk and debt?

Yes, home ownership rates for 25 to 35 year olds falling from 65% to 35% over the past 30 years is not the NZ I knew or want. So yes, if life can be considered a game, there is need for change but it is not about the young and old, the me and you.

And for heavens sake please stop saying that older people own all the property - there are many retirees on the bones of their bum renting, and there are also many retirees who don't own investment properties. Those who own rental properties - or have other investments - are the ones who were prepared to work and take risks for the opportunities that they now have and benefit from for a comfortable later life. Is that morally wrong?

I'd just be careful assuming that the future will be a repeat of the past. Many people don't want that and they're growing in numbers. And more that central banks (and to an extent governments) do to preserve the wealth of the minority, the most likely the system will come apart.

Oh but it does....history repeating; albeit in slightly differing versions.. we are predestined to make similar errors

Maybe our lot comes down to luck and timing?

Good point - yes. The wise generally know when something is or has been too good to be true. They are humble and cautious.

P8, shaming someone for renting is really twisted man.

Laminar - not shaming anyone at all.

If one thinks that there is too much risk in owning a home, then fine, just keep renting.

I was actually going to wish IO the best just as I saw your response.

Not offended by your comment there P8 - all good.

IO

Thanks

On point P8

One word: Unemployment

Two words - mass unemployment.

TTP, I agree with you about the long term. I’ve been saying for a few years on here that NZ housing is way overpriced/inflated. In the long run, it’ll be fine, especially if/when prices drop to a reasonable or even bargain level. After the GFC, in the US there were some extreme bargains to be had. Similar could happen in NZ and Oz this time. If not extreme, we could well see at least reasonable prices in the coming few years. It’s about time.

On RNZ yesterday, some interesting comments on stock markets. 1) there is nowhere else providing any return, so many have piled in 2) sports betting has been shut down, apparently a lot of sports betters have also piled in 3) this is very us centric, of private investors there, 84% of the market is owned by the top 10% of earners, 40% of the market is owned by the top 10% - this speaks to inequality more than anything else. Doesnt include institutional investors. 4) Amazon and google (I think) between them employ 280k people, in the 70s A T and T and GM employed 1.2m people, this comparison based on the same inflation adjusted market capitalisation.

There was more, thats just what I can remember

That's exactly what I was thinking about ;)

Hi b21,

Good on you!

Clearly, you're a smart cookie!

TTP

You obviously didn't hear of the word "sarcasm"

Wait for it, names calling process is about to kick in.. 3,2,1

The free market was praised on the way up. We were told that the market will do its thing and find the right price. Now that the time has come for the market to find the right price *below* the current one, banks are doing everything to control the market, with support from govts and reserve banks.

LVR restrictions, foreign buyer ban, ring fencing of rental losses, capital gains tax on residential rental properties hardly epitomise free market.

No it wasn't was it. But its getting closer...if only the central banks would stop fiddling with interest rates and governments stop paying landlords via accommodation supplements...House prices are basically being held up by monetary and fiscal policy! So perhaps still far from a free market! Imagine if they were just held up by current wages, no welfare, no interest rate drops (i.e. use a historical rate of 5-6%).

Easy answer then, scrap rent subsidies.

We absolutely should once we have the support of the democratic society we exist in and people can afford to live based upon wages! (which landlords don't understand because they live off other peoples wages...leech like...). But until then, we as a society have the heart to support people who are trying to get by, to only give to those who are trying to 'get ahead'. Yet they do not understand the damage they do because of how each persons action negatively (or positively) impacts others. See if you can figure out where our problem as a society falls as our home ownership rates fall.

HeavyG ......as I have said many times before, it will never be a "free market" until my tax payer dollars stop going towards.....

1. The accommodation supplement - if a landlord is taking the money out of the taxpayers pocket, so the tenant can afford to pay the "nominated" rent, how can that possibly be called a "free market"

2. Working for Families - if a business cannot afford to pay a reasonable salary/wage, why should that business even be "in business", while the only way is to reduce its wages/salary amount it pays, is with the "difference" straight out of the taxpayers pocket !

If you can "solve" the above 2 points HeavyG then we can start to talk about a free market and address the issues you have raised.

Scrap both. The Government can step in and provide free housing to all those that want it. No need then for rent subsidies or WFF as the state will provide all.

Hooray !! ...now we can start talking turkey ! .....the "State" shouldn't have to provide ANYTHING AT ALL when it comes to housing - the only thing it could provide is housing for people with a chronic or debilitating mental or physical illness/es, who have no family at all to look after them, however could look after themselves with only minimal or no assistance.....everyone else can "sort it out for themselves". ...then we would have a free market and all those taxpayer dollars for the AS & WFF can go into educating, training, retraining etc ....then the people would have a decent income and you then as a landlord will have renters who would actually be able to afford your rents, that are BASED ON WHAT THEY EARN and not assisted by a government AS "top up" that goes straight into the landlords pocket.

Sounds good in theory - but what about people with children who can't afford decent housing? I know, I know - if you can't afford to provide for the properly don't have children, but a. sometimes people's circumstances change in ways they either couldn't or didn't predict or plan for or b. sometimes the children are unplanned. Unless you are going to forcibly sterilize people, force abortions on people, or go round removing children from otherwise good parents who simply don't earn enough, you either have to provide some housing support or consign a whole lot of children to growing up without decent housing.

al123 .....I totally understand what you are saying, but if rents actually "matched" wages, wouldn't that at least help ?

When you have 2/3 of your net pay going on rent, and because the landlord knows if you can't afford it, the government will "top you up"....wouldn't that money be better spent to help those children you mentioned ? .....and not go straight into a landlord's pocket ....and eventually back to an Australian owned bank.

Yes, it would help - but I just can't see any way out of having to provide support for at least some families with children. I do think though that state housing would probably have cause less distortion - at the very least there wouldn't be any rent-seekers (i.e. landlords) benefiting directly from state support.

In previous generations it provided by contributing to affordable supply through multiple avenues. Such that no one who benefited from affordable house prices can claim to have done it all on their own two feet.

Certainly a better avenue than recent years' focus on pushing prices up to benefit portfolios of those who had access to that affordable supply.

The supply of housing is directly controlled by government entities, through land use restriction. This is not a very free market.

It could easily be controlled by discouraging so called investors and speculators from owning housing. Affordable dry housing is a basic human right. Bring in a capital gains tax, and stop individuals or companies from owning more than one house plus holiday dwelling

Freely giving the wrong exploitative people the cash support is what is wrong with this Society.

People should vote for their corrective treatment in the next election.

Never one rule for some, but not for all.

All lives matter fairly in Society. All those screwed by the elite, should be tossed out into the pitfalls they created, not "Supported" by Politicians with their own "Agenda".

If we have to pay for Social Housing, it should not support an Aussie Bank, nor a stolen amount of dosh, put aside by a bent Politician, into others pockets.

Fair do, or don't do. All lives matter. That applies in the monetary system as well as those making a killing out of rental Housing at the Taxpayers expense.

It is murdering the affordability of simple housing, for simple folk, Taxed on every dollar they earn, while others "Claim' the rewards by avoiding the beneficial payment of taxes, with no accountability.

Get real or get lost you thieving people...you ain't Royalty, but you act and take like a Whore-lord of ill repute, from times gone Buy.

Supporting the Rich to get richer, is not a Labour Supporters.....Ideal....

It is skimming the poor and middle classes.........Classy eh!.

Nor is importing cheap Labour...with no hope of Housing...themselves. Labour is not "Working", like it used to mean. This is still a top down, with free top up...

All change, no change.

Woe that is about 70 comments from this one thread. That's some "Pent up" tension.

The psychology may become, 'why buy now if I can buy cheaper in the future?'

A deflationary spiral for houses! Housing crisis solved.

No need to build more houses. Lots of offices will be vacant and CBD's strugling. The buildings will be repurposed to apartments. This reinvigourates the CBD's, supplies houses employs the construction sector and adds income for councils.

Correct.

That, and face to face work places are no longer needed as they were in the past. We were already heading in that direction, and Covid has sped it up.

Those businesses that come out the other side will look at the bigger expense items first, and after wages rent/lease costs are normally second.

Commercial Landlords will be faced with sit tight and find someone to lease or repurpose offices.

The effect this has on residual house prices will change the way the system operates and even the social structure of NZ.

The problem is a lot of these commercial landlords business model operate on having a full time tenant and property prices going up.

Its a huge investment to refurbish into places of residence. What happens if they cant obtain finance, made worse when theres 100 other commercial landlords in the same boat?

Bankrupt and the country can kt afford that so Kiwi Build will change tact. That will only take two decades to change the letter head and kick it off.

The proverbial car has driven off the cliff - nothing supporting it now other than momentum (and gravity being tampered with by government stimulus and bank mortgage holidays). Can only last so long before coming down to earth.

One potential downside to coming out of lockdown early might mean that we become one of the first in the OECD to experience the aftereffects - the popping of the property bubble being just one.

I would argue that the psychology is already "why buy now if I can buy cheaper in the future?" - wonder how many of the property spruikers around here have actually bought recently? Have had plenty talking about how they've sold.

Don't listen to what people say, watch what they do.

I personally agree with this take, but me watching the Wellington market closely (looking to buy) prices are still soaring. The pain hasnt started yet anywhere but Queenstown. going to take time to filter through the system. Wage subsidy has cushioned everything.

"Wage subsidy has cushioned everything."

Mortgage payment reductions and deferrals have also had a significant impact. There were over 40bn in loans where borrowing customers adjusted their debt payments in one way or another.

Hi Fergus the RBNZ has been doing most of the cushioning by dropping the cash rate so interest rates are the lowest they have ever been, and most of the drop was done last year, before the Covid crisis!

"Don't listen to what people say, watch what they do." ......thank you polygonalvector, best thing I have read all day !

All these property "spruikers" will never tell you what they are "personally" doing and I know full well that many have already sold excess property or downsized well before now ...take the greatest NZ property spruiker ever, Sir John Key and his Parnell property .. ...he knew the "writing was on the wall" years ago !

And that's why people have no time or patience for these "property bulls" ....they are just pushing their personal barrow to suit their particular situation or strategy ! ....while they will quite happily promote a narrative etc in the guise of "advice" to help their own cause ....and stuff the consequences for those who take said "advice" .....they are on a par with the old "used car salesman" pictorial character, in white shoes and a "flashy grin", while you are thinking ...."would I really buy a car from this guy ?"

Yep and Chon Ki also has his Sydney apartment currently for sale

This is thankfully, exactly the kind of thinking I'm seeing around me at the moment. I know two couples who are hoping to buy late this year or early next year. Depending on how far things have dropped, they'll then be weighing up the balance between buying while prices are still too high vs continuing to rent. I hope to see more awareness of this in the next few months. There are still people jumping into the market with blind optimism or simply unwilling to wait.

IO, I am one of those now firmly in the 'why buy now if I can buy cheaper in the future?' camp, after actively bidding on properties pre-lockdown

The main downsides are that I'm still paying rent, and the potential upheaval of finding other accommodation should the Landlord decide to sell or undertake his EQC rebuild.

I can live with both those downsides if it means being able to afford a bedroom each for myself and the kids in the next 8-12 months. After that time I think the frustration of not being able to setup/modify the house to suit our needs will wear me down....

"We expect house prices to decline less severely than during the Global Financial Crisis"

An interesting point of view, given that during the GFC, 12 years ago, GDP fell about 2% at it worst, yet the projection by the IMF see us falling over 7% this time; more than 3 times as much. And, of course, unemployment stats will be on an entirely different planet.

My thoughts exactly

The USA is now in far more trouble than during the GFC. The decline was predictable and hardly a surprise for those that can see the global perspective. March was the top of the roller coaster, the release just went "Click" and we are on the way down and gathering speed.

The difference is in the cause. The GFC was caused by subprime lending and overheated real estate markets in the U.S.A thus house price falls were larger.

This downturn is not caused by problems in real estate markets, they are simply collateral damage that has the potential to quickly produce further collateral damage itself as people spend less as their wealth declines

The banks here and Australia are seriously leveraged with property debt.

I was reading that and thinking this doesn't make sense. But they're a bank economist so are a reputable source of information I'm told.

Their predictions are always right.

The trick is to keep changing your predictions all the time. Eventually, about a day or two before the target date, the "prediction" will be spot on.

"The trick is to keep changing your predictions all the time. Eventually, about a day or two before the target date, the "prediction" will be spot on."

Exactly.

I remember Tony Alexander saying that property prices were going to keep rising due to the housing shortage in February & March and there was no mention of any risks whatsoever to those price forecasts. Then he does an about face and forecasts property price drops.

These economists are constantly adjusting their property price predictions which are only of use to short term property traders.

In reality, most property buyers are long term owners with longer term (multi-year) ownership periods, not short term traders.

Trying to predict short term price movements consistently, is impossible.

I think you are being overly generous describing Tony Alexander as an economist.

There are plenty of other words that fit his particular line of work much better.

I was confused by this also.

Don't all indicators suggest we will feel this far more than the GFC? Especially since the GFC mainly impacted USA (and had little to no impact on Australia).

I don't understand the reasoning that this recession won't harm prices as much. Everything seems poised to be far worse.

It is still wait and watch as housing market though should be at the cliff waiting for the push but does not seem to be so as of now.

So wait and watch as how pandemic and economy plays out after few months as now many small businesses are doing excellent business (Know about Auckland) due to liquidity though those in City Centre and tourist places have taking a hit. Many have also made quite a decent money in wage subsidy (As got 3 months wage subsidy though started after a month and with a bang) and other government freebies. Many big business who have fired employee is actually taking advantage of the situation and restructuring to save money in number of ways ( Not all like Air NZ).

Currently lot of money in market so is not recession for many expect those hit by it (Belong to 10% unemployed) is a depression.

Agree that till now house price have not dropped as it should have and is resisting any downturn.

What will happen in future only time will tell if this generous stimulus by government helps in controling the damage or just delaying the damage as entire world is on money printing spree SO yes have to wait and watch as in unchartered water.

It's not the house prices resisting the downturn. It's every reserve bank and govt doing their very best (and more!) to prop up the house prices that would otherwise disintegrate in a matter of months.

I know we're saying the same thing, but our narratives are different. Spruikers like to word it as "resilient housing market", which is simply false and hides the root cause of why prices aren't falling.

We can only hope ;)

Buy the dip and score a $$$ million $$$ on the rebound! Hurry, while stocks last.

Is that you Robert Mugabe?

The big dip is about 12-18mths away... then bargains galore

The assumption there is people have jobs and spare cashola.

The next quarterly NZ labour market stats (including unemployment stats for the Apr-Jun quarter) are due out 5 August:

https://www.stats.govt.nz/release-calendar

Probably one of the main clues we will get in the next couple of months about the trajectory of the recession.

Were heading toward 10% unemployment at the exact same time as our tap of 50,000+ yearly migrants has just been turned off. I would suggest a housing pull back AT LEAST as big at the GFC is on the cards.

Unfortunately we have degenerate reserve bankers who will not tolerate economic reality impacting their house price sacred cow.

They will debase us into penury before they ever permit housing to drop.

The headline is a little disingenuous and could alternatively have been written as "Westpac economists don't expect the fall to be as bad as the GFC". Also, why not provide some context, how much did NZ house prices fall in the 90's recessions?

Question is why don't they expect the price falls to be as bad? There's a problem with bank economists. Their self interest steams from the salary they receive from their own employer. What's more, you could say that the banks ability to lend monery into existence is the single biggest driver of housing bubbles (definitely not a stretch).

I think 7% to 10% fall caps it in prime Akl/Wgtn. There will be more stimulus (negative rates for example) if the outlook deteriorates.

I think it's worth adding that my comments are what I believe will happen, not what I want. Not having proper economic debate reduces threads to reddit quality diatribe.

That's quite specific expectation TK. How do you arrive at 7-10% for that segment of the market? And can you not use your assumptions for the wider market.

It's a guesstimate, I'm not adding anything if I say 0 to 20% !

I see. It's your own take on the "I reckon" school of modelling with a dash of trying to look precise.

the "I reckon" school of modelling. I like that. Perfectly describes almost everything in the interest.co.nz comments section.

Honestly I barely read the articles anymore!

the "I reckon" school of modelling. I like that. Perfectly describes almost everything in the interest.co.nz comments section.

Most people wouldn't even know where to start to model or forecast house prices, including Bindi and Ashley. There's a whole lot of gut feeling going on.

Gut feeling being mentally governed by hindsight, recency and confirmation bias.

Well it's actually a little more substantial than that, perhaps I was being modest?

Would you be good enough to provide a forecast with some insight as to how you arrived at it?

We could always have a bet, I've flushed a few lightweights out that way before.

We could always have a bet, I've flushed a few lightweights out that way before.

You could. But not with me. I don't bet on things like the direction of house prices. Call me a lightweight, but I prefer betting on games where the odds are more deductive, such as blackjack. Or assymetrical bets like BTC. Betting on the direction of house prices is too much about false ego.

Oh, they did that card-counting thing on the Hangover right?

Probably. The Blackjack probabilities are more fun in my opinion that "house prices will go up / down 7%", which is not really any fun at all. Of course, I'm always interested in how people can estimate house price movements. I've yet to see a hypothesis that has sold me on the idea that anyone can really forecast house prices, particularly in times like these.

How does anyone in the financial universe survive? Fund managers, pension funds, Banks, Insto's - they all manage to operate with forecasts that are intrinsically unknowable.