Property values could be at a turning point and may be heading for a 5%-7% fall, according to property data company CoreLogic.

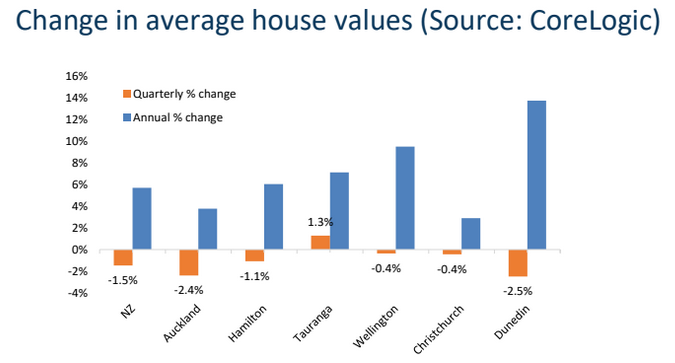

The company's latest Market Pulse report says its quarterly housing value index declined 1.5% nationally in the second quarter of this year, with larger falls seen in Auckland (-2.4%) and Dunedin (-2.5%) with smaller falls recorded in Hamilton (-1.1%), Wellington (-0.4%) and Christchurch (-0.4%), while Tauranga went against the trend and was up 1.39%.

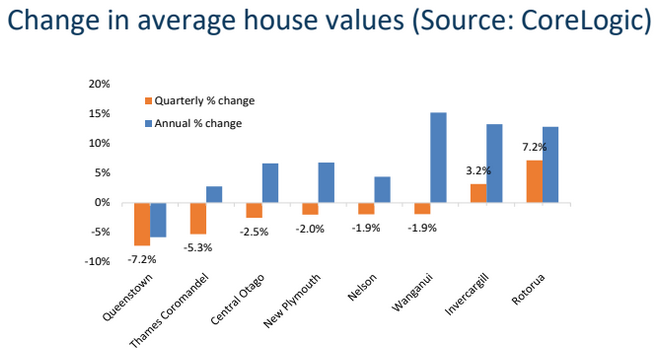

In regional centres the biggest declines were in holiday hot spots Queenstown (-7.2%) and Thames-Coromandel (-5.3%) with a mix of falls and rises in other centres (see the graphs below).

The decline in values is unsurprising, given that housing market activity was severely restricted for much the second quarter and the broader economic repercussions that followed, but the CoreLogic report suggests the Q2 figures may mark a turning point for the market.

"The overall message is that the worm seems to have turned for property values in the main centres," the report said.

"Given that we are in recession and that unemployment is rising, it's no surprise that property values have started to face some downwards pressure.

"Overall, property values seem to have reached a turning point and we estimate that the national average could ultimately fall by 5-7%.

"That would obviously be unwelcome for any property owner, although a bonus for would-be buyers, but it would be a smaller fall than the figure of 10% during the GFC," it said.

The comment stream on this story is now closed.

153 Comments

As a first home buyer this is very welcome. To be affordable the market needs to drop by 40%.

If you wait for a 40% drop you'll probably never buy. Or if it does happen, you won't be able to buy, you'll most likely be on the dole queue like 30% of the workforce for it to fall that far.

Never take advice from someone who has skin in the game.

Been looking for 8 months and had to sit back as people were paying exorbitant amounts for rubbish. So very wary at the moment

Ironic coming from "RealAgent". I'm neither a broker, agent, or property investor.

:)

Pragmatist is an fhb

Not that either... was a FHB 20 years ago.

Am referring to the fact you're not a homeowner at present but are looking. I assume that's still all correct. As opposed to having vested interest aka skin in the game

What was that thing you said to me yesterday? Side-step, ball up in the air, distraction and all that...?

Eh? You're not making any sense. Pragmatist has been a fhb for as long as I remember but if he previously bought a house 20 years ago he must have sold it. Someone made the comment he has skin in the game ie vested interests... ok? Holding all the angst doesnt do you any good CJ

He picks on anyone who has a disagreement with his opinions.

Thks Chairman Moaner. You know what they say about people who are critical, they are never happy.

No, you're not correct, we haven't been looking since late last year. Staying put for the foreseeable future.

All good, I think you may have said that but I wasnt sure whether that had changed. The point is you have no skin in the game.

TTP is also a fhb.

f = fourth, fifth or fifteenth?

fiftieth..?

He buys others first homes lol

Correction - he buys others' first homes.

A 40% drop would require a subsequent 67% rise in price to get back to where it started.

Dang, you sure? I think more like 99%. I think the price of beef should fall by 99% to be affordable as well. How about a Lambo? Damn, that thing needs to drop 99% to be affordable :P

C'mon, that's a pretty cheap shot. There are broadly accepted definitions of what it means for housing to be affordable, and its usually put at 3-4x income. Given that average house prices are currently around 6x income, a 40% drop would put them right in that ballpark. There are not, as far as I'm aware, similar widely accepted definitions of what it would mean for beef or Lamborghinis to be affordable.

Your 3/4x assessment is way out of date. Look at the affordability index as it is more comprehensive and relevant. As easy as 123 al123

It's not out of date. The Demographia International Housing Affordability survey uses a median multiple of 3.0 as a benchmark for affordability, for example. What affordability index are you referring to, and why do you think it is more comprehensive and relevant?

Edited to add: if you need more evidence that the median multiple measure is neither irrelevant nor out of date, interest.co.nz has a page on it.

https://www.interest.co.nz/property/house-price-income-multiples

Waiting on housework’s to reply

Thank you sir. I am truly honoured. Now what?

Also waiting on Stev-O's reply

Is ignorance bliss? Here is the link: (note higher numbers indicate less affordable housing - you will notice that the index has declined since 2005)

Housing Affordability Index | Ministry of Housing and Urban Development

https://www.hud.govt.nz/news-and-resources/statistics-and-research/hous…

Enjoy

.

I know the govt likes to mother and smother people these days, you really must learn to spoon feed yourself though. Try the national index, but I think all indexes are telling a.similar story that housing has become substantially more affordable. Remember it's as easy as 123 al. Got it?

A quick ' get out of jail ' edit you made there al123

I can tell you what I said - I asked you for the measure you were referring to, and I'd googled it and found a couple of different options. As soon as I posted I saw youd provided it.

The measure you linked to doesn't show what you seem to think it shows. It's a measure of trends in affordability, not a measure of whether something is affordable. In fact it specifically states that does not set a level at which housing is or is not affordable.

Could you please cut all the snide comments about spoon feeding? Asking someone what they are referring to when it has not been made clear is not asking for 'spoon feeding' as you put it. It's a perfectly reasonable request.

No one will be able to ever make you change your mind that is obvious. There will always be an excuse or debate irrespective of the quality of the evidence. The evidence I provided was from the ministry of housing so you cant get more independent than that. Or can you? You are also welcome to continue renting for the foreseeable future or indeed forever . While others will be there providing you with an affordable healthy rental

I know the evidence was from the ministry of housing. I clicked on the link. That's how I know it's a measurement of trends that doesn't make any claims about what is or is not affordable

But it seems this discussion is making you really upset houseworks. If you don't want to talk about affordability measures that's fine, but there's no need get personal about it. I think best leave it there.

Al123 the clue is in the title - Home Affordability Measure. Affordability is improving, that does not fit with your narrative. Like I say no one can convince you no matter what, however you have lost the wind from your sails and the energy from your argument. Enjoy.

You really should read what you link to. Do you really not understand that "affordability has improved" is absolutely not the same as housing being affordable.

Something reducing from 8-10x income down to 6-8x income = 'affordability improved'... but if it still required 6-8x income, it cant be called 'affordable' now can it.

The question is - intentionally misleading or just conceptually inept?

Many commentators seem surprised about your comment yet it is a reality housing is severely overpriced and unenforceable, which means that it is just a matter of when the correction is coming, it doesn't look it is going to take long and the numbers will vary but 40% doesn't seem like an unlikely number for some areas, just looking at recent apartment auctions not unlikely at all.

Logically and even Fundamentally housing market has to fall, once the crutches of wage subsidy and other subsidies is removed.

One does not have to be economisit or and expert to predict it, so more the need for FHB to overcome their FOMO now. If ever their was a time to be patient is now.

Many leases expire around January. I know a few who are in this position and concerned that prices won't have dropped enough by then. I can see them holding until December, but beyond this they are likely to give in. I'm sure this is the case for other FHB still in a position to buy, with their leases ending early next year. I hope the time is coming for everyone who has held off jumping into this overpriced mess.

I'd negotiate an extension of 6 months if that were my position rather than signing up another year

Absolutely. By then, you'd think most landlords would welcome even 6 months. If not, then I can see how being locked in another 12 months or the thought and expense of having to move into another rental is enough to send them over the edge.

The balance of power has shifted to favour the tenant IMO.

I am in the camp that says prices will fall. At the same time, building costs are rising. Rarely a week goes by without getting a notification from some supplier to advise of price rises. My conclusion is that I can say without fear of contradiction that I have no idea whats going to happen!

Building costs can also decrease when construction projects dry up.

Only if cost of materials falls into line also

Good chance labour costs will come down. As building work reduces sharp pricing will appear. It always does.

They might but trimming the cost of materials will make a far more sustainable impact for the industry

Oh they are; internal furnishing are dropping their prices first followed by everything else later down the track.

I certainly think there will be a drop, but not to the level everyone thinks. The bulk of the "bargains" will be at the top end as that is where most of the job cuts are happening. The middle to low end will be fairly stable.

Jobs are been lost at all level.

I agree that there is certainly a lot of froth at the "top end" but the apartment and air B&B market has also been frothy af, so i'm expecting to see hurt in those places too.

curse of the DP

Not to worry, just rely on the Bank of mum and dad. After all it was their fault for pushing up house prices

https://www.oneroof.co.nz/news/38147

Very Privileged Son ....

Really? There is no way I would want to be in his shoes.

Yeah, risky move to stretch at the moment. As the article says: "Post-lockdown buyers have shown they are willing to stretch themselves to secure well-presented, well located properties, and this Mt Albert home was certainly that,". Maybe that part of the market us duffrunt?

Not a problem if its dads money bought in cash... market can do what it wants

Well, in that case it would move the loss to Dad, but Dad is still taking a loss in the form of buying something that, odds are, will be cheaper if they wait. I suspect they don't care about that risk.

Yes, the narcissism must continue. No ponytails in sight. Very sensible.

There is a lot to unpick in that article.

House prices on the horses. FHB with Braveheart. Stay strong people. Don't break ranks and buy now.... HOLD!

Nice analogy! Light, irregular (scruffy) infantry facing the charge of some fine cavalry, holding their morale while doing nothing.

Hopes and prayers for Palmy.

And Horowhenua too. Levin and Foxton have also been enjoying a brief moment of property madness - $600+k for a 3bdr A1 home in Foxton Beach??

Tim Mordaunt was pretty hot for Palmerston. Maybe he can offer some news from the coal face? You lurking TTP, any oscillations to comment upon?

If we see a 40% drop in asking prices, then they will still be 20% overvalued compared to other places in the world. NZ is full of cheaply constructed, poorly built homes that are not suited to the climate.

I'm still shocked by how accepted this is here. Just unbelievable how garbage the housing really is, and for such insane prices. People almost welcoming the mould all over their window frames within a year or two on a new build. We should have thermally broken frames on windows with the climate here, among many other issues. Instead people are openly vocal about using black frames to avoid feeling the need to even wipe condensation down and prevent mould, rather than insisting on better standards. It's just been normalized.

Unfortunately you're 100 % correct. People have been beaten into submission by vested interests to the point that they'll accept anything, including massive market failure, working homeless, huge gains being untaxed and rotten housing stock

Go to a northern English city, India, China, much of the States, Eastern Europe, and you’ll find houses much worse than in NZ. Then there’s Pakistan, North Korea, Bangladesh...

Seriously, there are some really rubbish homes in the UK, London as well as the forgotten north. Victorian slums built for factories that have long been idle, unbelievably s*****y blocks built in the 60s and 70s, and some really average new builds on estates. A relative has one that has major structural issues less than five years after being constructed. New homes here are pretty solid and energy efficient.

The main fault and problem with NZ homes is poor heat and ventilation, rather than poor build quality IMO. Kiwi homes tend to have a one or two heat sources (a single fire or a heat pump in main rooms) which causes cold spots. The only ventilation will be kitchen and shower fan/extraction. Whereas most European countries (including the UK) have central heating (which creates *even* circulating convection heat) and ventilation in the roof, walls and in the windows (if double glazed). I lived in a UK house once that had been given a very expensive renovation, underfloor heating in every room, high end timber double glazing, loads of insulation etc. The house had a massive damp and mould problem. We had a damp assessment and it turned out that they had neglected to put vents in the roof and had effectively turned the house into a tupperware box where moisture couldn't escape. Wet air is much more difficult and expensive to heat. NZ is pretty wet as it is, but there is very minimal ventilation in most homes. Double glazed windows don't have trickle vents even. A lot of bedrooms are the coldest rooms in NZ and yet as people sleep, they are breathing out gallons of water. If you heat the whole home evenly, the water will travel upwards and out through roof vents, if you create cold spots with uneven heat, the water will just settle in the coldest rooms and cause mould.

Good stuff GN. It's all about moisture in and moisture out. Schools should teach this stuff.

Even running a dehumidifier in some NZ homes isn't enough to make them stay warm - but damp certainly never helps things. I do miss centrally heated UK houses, where you just never feel cold when you were inside.

It’s possible in NZ, just spend the money. Our 80’s Auckland home has gas central heating, gas fire insert in the fireplace, double glazing, thermal backed curtains, batts insulation and heat pumps (used more to cool than heat). Add North facing to the mix and it’s very comfortable.

Wow. How much did that set you back, if you don't mind saying? Did you end up with lower electricity bills in the long run, or was it just worth it to you because it's a way more comfortable way to live?

We bought the house with the gas central heating already installed. It’s an old Brivis unit that can’t be zoned (all the house or nothing). It had no impact on the buying decision as we’d never had central heating before. It’s brilliant in getting the house to temperature. Costs ~ $100 per month to run along with the gas fireplace insert. The insert cost $4,000 installed and is more of a way to use the fireplace without having to get wood than anything. Double glazing the Front cedar windows cost $12,000. Thermal curtains went on single glazed windows. $500 of Batts were added above bedrooms on top of the Cellulose rubbish in the ceiling. Two split system heat pumps were added for Summer heat control. That cost $10,000. The property has a current core logic value of $2.55 million, but much of that is land. If I had to chose one thing I’d install in a house it would be zoned gas central heating. I spent enough years in Wellington in front of a bar heater. Central heating is an all around heat and is a far better living heat solution.

Thanks very much, that's really helpful.

We've only just completed the first quarter of the new reality. The second quarter from July - September will be interesting to watch, especially as it includes an election. I can't help but think that the govt's still got lots of borrowed/printed money to spend yet. Perhaps they'll double the unemployment benefit, they've already doubled the amount of people unemployed. How to win/buy an election by giving away future taxpayers money today - The Labour Party 2020.

And your predictions for what National will be offering are?

National will be offering; Flinging the immigration door wide open, welcoming in the coronavirus along with cheap low educated/skilled workers. Oh not to mention lifting the Foreign Buyers Ban and Anti Money Laundering rules as a way to artificially inflate property prices way beyond local Kiwi's reach.

Sounds about right, just the usual self serving policies. I never fully support either 'side', as there are always issues. But I sure know who I won't be voting for. Somehow people here are surprised by the amount of left leaning commenters. They seem shocked that their fellow New Zealanders expect or are hopeful of even having a chance at a decent future ahead of them. It must be very frightening to realize that so many people are now far more wary of the ponzi scheme and not happy for BAU to continue.

I’m shocked you believe the rhetoric and promises after three years of non delivery but the people get the government they deserve. Fill your boots.

You're assuming that I believe their rhetoric. Despite stating that I don't fully support any side. I see full well how little has been delivered on many fronts and it disgusts me. Unfortunately the alternative is far worse. It is foolish to give wholesale support to any of them.

Yeah I agree.

I will be voting Green for the first time this year. Certainly don't buy into all their policies, but I do on most of them. Disappointed in Labour, and the Nats, goes without saying they are bereft of inspiration, and are morally bankrupt. And more practically speaking are a shambles.

Of course that's your personal choice Fritz. Dont be like those who voted MMP who later claimed buyers remorse.

Im happy with MMP, we had to stop Nationals open border policy of immigration and foreign funds.

It hasn't reached the levels I want, and house prices haven't dropped as far as I want, but maybe in the future. National getting back in would be a huge backwards step, maybe labour knowing that people are voting for them will help them become more robust about reducing immigration, and create more affordable housing. I will wait and see, I'm not happy with labour, but National would be a travesty.

Agree also, won't be voting National in the foreseeable future. The selection of Brownlee as Deputy was the last straw. If someone that incompetent can be promoted, there must be some scary/fundamentalist skeletons in the closet when it comes to the rest of their front bench.

But voting Green? As a protest vote or a real choice?

I worked recently with a alternate chap with dreds. BOP

He successfully gained sovereign status, ie citizen of no country.

Believe me he said , all govts do not like, and make it very difficult. as they borrow on immigration and population.

Ok , its a bit out there, but remember the old saying ,worth your weight in gold.?

Why would you want sovereign status? Its the worst of all worlds. The least rights anywhere in the world, nowhere to call home, but he's still a tax resident of wherever he lives. all the costs, none of the benefits?

Greg, can you please check your percentages. I am seeing too many negatives. I was told house prices never fall. You must have a couple of typos in there.

This is old news, of course the Q2 showed a drop the Economy was shut down, anyone who has been active in the market since Level 3 knows it is very buoyant. It is cheaper to buy in Auckland in the 700-800 range than rent. From what's actually happening out there I would be surprised to see any drop other than perhaps Queenstown.

It is cheaper to buy in Auckland in the 700-800 range than rent.

Your thinking is too simplistic. If your housing costs are the same in rent or buy scenarios, but you have to shoulder a potential loss of $80K+, then it is very easy to rationalize that renting is cheaper. It's called loss aversion.

From what's actually happening out there I would be surprised to see any drop other than perhaps Queenstown.

Who's in charge of the "what's actually happening out there" measurement? Newstalk ZB?

JC - The 10% drop particularly in Auckland is not happening, we are looking at the start of a up cycle, we will all know in 6 months my money is on stable to positive

The 10% drop particularly in Auckland is not happening, we are looking at the start of a up cycle, we will all know in 6 months my money is on stable to positive

OK got it. You're just trolling.

JC - What is trolling ? I'm talking facts in the market place ?

Hi Shoreman, can you please explain your logic for supposed 'up cycles' starting now?

Key words in this article: declined, falls and downwards. Music to the ears of my adult children who are patiently waiting to move from over-priced rental properties into their own homes.

Entire Orchestra will play in very near future.

A property cycle lasts many years,not months or quarters.

Now we are seeing just the tip of the iceberg.

Like Japan? Perhaps they're in some kind of 'property cycle' with a long duration between peaks and troughs.

Yes that's right JC - sometimes decades and in a downward direction!

You will find that the Japanese population is actually falling. Moreover, the provincial towns are aging and dying, with the youth concentrating in the Osaka and Tokyo areas (as has been the case for decades).

Japan has a net migration rate of 0.544 per 1000, or 0.054%, compared to our 11.4 per 1000, or 1.14% - that's more than 20x higher. Could be a factor.

I don't think the population was falling in the 1990's when their property market started falling - if that is the point you're trying to make?

No evidence of any price falls at all. Some amazing prices being achieved at very busy auctions in Auckland. Open homes still very busy, lack of rentals and rents still going up, interest rates at record lows. On the plus side, I guess you can buy with confidence now knowing that interest rates will never rise.

For most people, there is stronger emotional attachment to 'evidence' that they want to believe.

'On the plus side, I guess you can buy with confidence now knowing that interest rates will never rise'

- nor potentially will the capital value for the next decade (or more..).

Good grief IO, doesn't it get tiring being so relentlessly negative and gloomy? There is chance house prices don't rise, or even fall, but history tells you this is unlikely over the medium term. What if house prices do rise and someone missed out because they read your comment? I mean, how many of you here have actually missed out over the last decade? There is a point where a family can no longer keep renting and want pets and kids to be able to paint their rooms, not to have to move around or worry about a landlord.

I don't see falling or flat house prices as negative and gloomy. So that view says more about you and your paradigm than me and mine. Thanks.

And I don't see house prices going up as particularly positive, but I'm not the one telling people not to buy.

Haha who is this mythical person that has been telling people not to buy? Are you suggesting that is me?

I don't care if people buy or not - I'm just pointing out risk. If you think pointing out risk equals me telling people not to buy well that just simply isn't true so again it suggests more about your thinking towards my comments than what I'm actually saying.

Why buy ? I was in that camp for a few years but moved on - I couldn't bring myself to join the church of the sheeple.

You are also welcome to continue renting (and moving) as long as you want (or can stand). Doesnt this prove the need for having private landlords.

Trying to predict is futile , give it up already

What about the report this article is about? Is that not evidence of house price falls?

You don't look for evidence of any price falls, you look at the market and analyse how the market goes and analyse the risks involved. When there is evidence shows price falls, It will be too late. You'll know what I am talking about if you have been investing in stock market.

Hence most of the narrative in NZ is based upon confirmation, recency and hindsight bias. You don't see that in other countries that have experienced housing market corrections as that negative experience is built into the narrative and as a result they are more balanced and cautious in their views...not here (for the most part).

Too late for what?! Housing is far more illiquid than stocks and tends to correct over months to years not days like the stock market

Lack of rentals? Haha we are moving out of our flat and into another thats $100 pw cheaper and in a better location. There is so much more to chose from now, and at much better prices.

Where

Central Auckland Suburbs - Mt Eden, Remuera, Parnell, Mission Bay, Orakei ect.

Pretty much everywhere in central Auckland and nearby suburbs, lots of vacant properties due to the lack of students and negative net migration.

Potential FHB should be assessing their situation and looking at their short term future (six to 12 months).

There have been - and are some coming - advantages that will improve their situation.

- Based on those with expertise (RBNZ, Core Logic as valuers, banks as lenders) there is the consistent comment of a likelihood of 7 to 10% fall in property prices,

- Mortgage interest rates are falling and (as said by the above) are likely to remain low for some time,

- The RBNZ has removed LVRs, and

- Today ASB (and other banks likely to follow) have removed the high LVR premium.

As long as one has good security of income and can readily service the mortgage (and banks have a 6.2 to 7% test) then the outlook for purchasing is getting better.

On this site there is considerably negativity regarding buying a home based on market trends. However, provided one currently has the income security and ability to service the mortgage, then for FHB then market trends are largely irrelevant. For FHB it is about home ownership and not a short to medium term investment - unfortunately for those on this site negative towards FHB they are unable to distinguish the implications of this.

Those FHB who have faced affordability issues need to look at the possibility of opportunity over the short to medium term (6 to 24 months).

For FHB it is about home ownership and not a short to medium term investment

Wrong. Purchasing of houses has been financialized to the point where it "has to be" an investment. House price growth has far outstripped income growth (Ipsos research shows that approx 2/3 of home owners couldn't afford the home they live in). It's not just about what the buyer can afford to pay. It's also about what a buyer can not afford to lose.

I agree. I'd love to see a survey of homeowners who have either used their home's capital gain or plan to use their home's capital gain as leverage to buy a rental, bach, boat, car etc.

ydab

Home owners' prime reason for buying a home is simply that - to provide a home for themselves and family.

Over time being able to leverage of one's equity is a consequence - and a really great and very common consequence and one that long term renters don't have.

I don't dispute that. But I would say having the ability of using your property's equity isn't a consequence, it's a major motivating factor in buying a home. Due to rapidly rising house prices, one's home has become a shelter, store of wealth and capital farm all rolled in one.

I agree. I'd love to see a survey of homeowners who have either used their home's capital gain or plan to use their home's capital gain as leverage to buy a rental, bach, boat, car etc

The 'wealth effect' is more subtle than that. Think about behavior at the supermarket. Look at people's trolleys. Seriously. Most people don't understand that the data collected about supermarket shopping trips is very revealing and valuable.

Also, think about the winter holidays to Fiji and the private school fees. Many are surprised to know that the people doing it really tough are in the higher socio-economic classes.

I don't 100% follow J.C. are you saying that the higher earners are the ones being more frugal in their supermarket shop?

An insane amount of people loaned up to the eye balls living beyond their means in the higher earners bracket. Quite a few people I know have a strategy that has been borrow now and enjoy and the debt is inflated away. i.e. they buy a house for $500k but it is worth $1mill in 10 years but they still only owe the initial $400k loan. Just made $600k so keep doing what you are doing. That game is falling apart and we are about to see who is swimming without togs on as the tide goes out.

JC

Not a problem.

Just keep renting - landlords need and love long term tenants.

Just been looking at the property investor pages on FB. A few people now talking about Tiwai closing and the comments are coming 'anyone else think I should get out now before others with my Invercargil rental property?'. Be interesting to see if this narrative catches.

Just keep renting - landlords need and love long term tenants.

I will. My business is in HCMC and my rent is tax deductible as an investor expense. And you've have to be stark raving mad to be buying property in a country like Vietnam, even before the virus.

Who is selling?

On RE NZ today there were 5761 listings.

Of the most recent 1155, 17% were new builds or not built. So, those were not being sold by existing occupants.(Put OTM 30th June to July 16th)

Of the 800 oldest listings, 49.5% were new built or not finished.(listed pre 3.2.20)

A lot of these will have had deposits paid on which people are saddled with or can walk on, or face negative equity as price drops 10%

Lastly, these developers will often be seeking revised loan arrangements as sales do not materialise

Are the banks going to be nice to them with prospect of fewer sales as time goes on?

Doubt it. Which means a lot more sitting on market or being sold at discounts, driving price down.

Really, to judge a market properly, we need to know what % of exiting stock is being put OTM at any one time.

We do not have this info.

The census did a pathetic job on counting how many owner occupiers there are in Auckland, so that figure is pretty unreliable too.

Comparing RE NZ figures on the market from one year to next misses crucial variable of what % are people selling their own property and also how many houses there are in the housing stock, taking account of new builds. So, many comparisons are invalid.

Broadly, since 2012, sales in Auckland are down 26% (in 2019) yet stock is up about 13% (looking at consents)

Tracking down pretty much as expected. I said Hamilton and Wellington wouldn't fall much, and Queenstown would.

The only thing that surprises me is Tauranga's resilience- at least for now.

Also 'tracking down as expected' the number of auckland rentals. Steadily dropping, now below 4900 for the first time since I think april. On the way up you were giving us an almost daily count as the number available soared to over 5250. Are you spitting tacks fritz.

You are a sad, bitter and angry individual. Boring, and not worth a response.

I checked the other day and it was nearly 5100, so it's up and down but I am not obsessed about it as you obviously are.

If you are such a successful property investor, why do you waste all your precious time trolling and attacking opinions that differ from your own? Insecurity?

Jesus you must have commented about a dozen or more times with your characteristic snide remarks this evening housework’s, is your life that boring?

Nice snide remark yourself mate. You dont have to torture yourself with my boring posts. And when you post multiple times its because you're more intelligent than others well you think so. Ps dont take out your angst on the innocent voiceless animals and not descending to ad hominem would also be a good start.

I may not have to torture myself with your boring repetitive posts but we all get sick of having to wade through them to reach the intelligent and salient posts that others contribute. What’s your disturbing obsession with animal cruelty? That’s the second fallacious comment you’ve made about my profession. It’s kinda creepy mate.

Almost 1M Aussies unemployed ....

https://www.theage.com.au/politics/federal/almost-1-million-australians…

That's 7.4% unemployment rate.

NZ unemployment rate is due to be released any day now and it's forecasted to be 7.3%, not much better I am afraid!

No longer the lucky country... ozzie will be losing its workforce faster than you can say "Queensland had x number of Covid19 cases today"

Such a heavy focus on house prices in NZ, as if NZ is a completely insulated economy. The usa doesn't look so good at present, neither does Australia, let alone the rest of the world. This blind belief that interest rates will never go back up is a dangerous one, based on the assumption that central banks are in complete control. If that is the case, then there is no need to worry, or even consider, that there are any dangers to the economy, especially house prices in NZ. To FHB I would suggest taking a much broader view of the global economy, and more in depth research, not simply on housing.

I would be asking myself how much trust are you placing in the hands of the central banks of the world?

It's not simply buying a house, it's a massive amount of tomorrow's that you will be borrowing against.

I would also recommend taking an in depth look at the local council in the area you are interested in, it's rates, regulations, and most importantly its level of debt.

Such a heavy focus on house prices in NZ, as if.....

Have you heard about Rock Star Economy.

Only economy in NZ is housing economy and it has been made Rock Star by selling NZ assets to overseas buyers at premium to speculate for Tax free returns later on joined by locals.

If housing economy crash - NZ will not be able to handle and will be finished and everyone is aware of it so government and reserve bank and everyone is trying everything to do to avoid bursting of the ponzi.

Question is, will they succeed - they may by printing and throwing money BUT is just delaying the inevitable and more the delay more the bubble and Bigger the pain.

"I'm free falling..."

Pretty sure that's a song. Post electoral bribes the next 24 months could be the toughest since 87, which for the younger set, was worse than GFC. Vulture funds get ready. Will the banks be ready to protect the stupidly in debt with no revenue...Popcorn.

Waiting on TTP’s view before I read the rest of the comments.

I like the way this is heading, but there is always the risk that it keeps dropping past 7%. Still, even if house prices drop 15%, I'd still be secure in knowing I had at least 20% equity and the capability of serving the debt. Sure, my capital gains would be shot to hell, but then I wouldn't be looking to flip. My only concern is buying from a disgruntled mortgagee seller, who then sets fire to the house they used to live in for 5 years, with me in it.

Thanks for sharing the real estate lobby propaganda!

no problem, I was trying to demonstrate no one has a clue

The fact is that everyone that is really involved in RE and economics knows where we are heading, while the mass media and their shareholders are desperately trying to offload investment properties to clueless FHB in a shameless manner by continuously sharing pieces or propaganda like that which will cause a lot of pain and misery down the track.

Interesting - do you have any evidence of this occurring?

it's going to be interesting to see how this unfolds. Will it be an orderly decline, or something more chaotic?

I'm curious to know how the "the property only goes up" crowd will behave once their mortgage lever arm works against them instead of for them. Will there be a rush to the exit?

I bet many will hold out and get spanked further down the track.

I think the smart money is leaving real estate right now, and the flurry of activity post lockdown was an absolute gift for those savvy enough to sell.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.