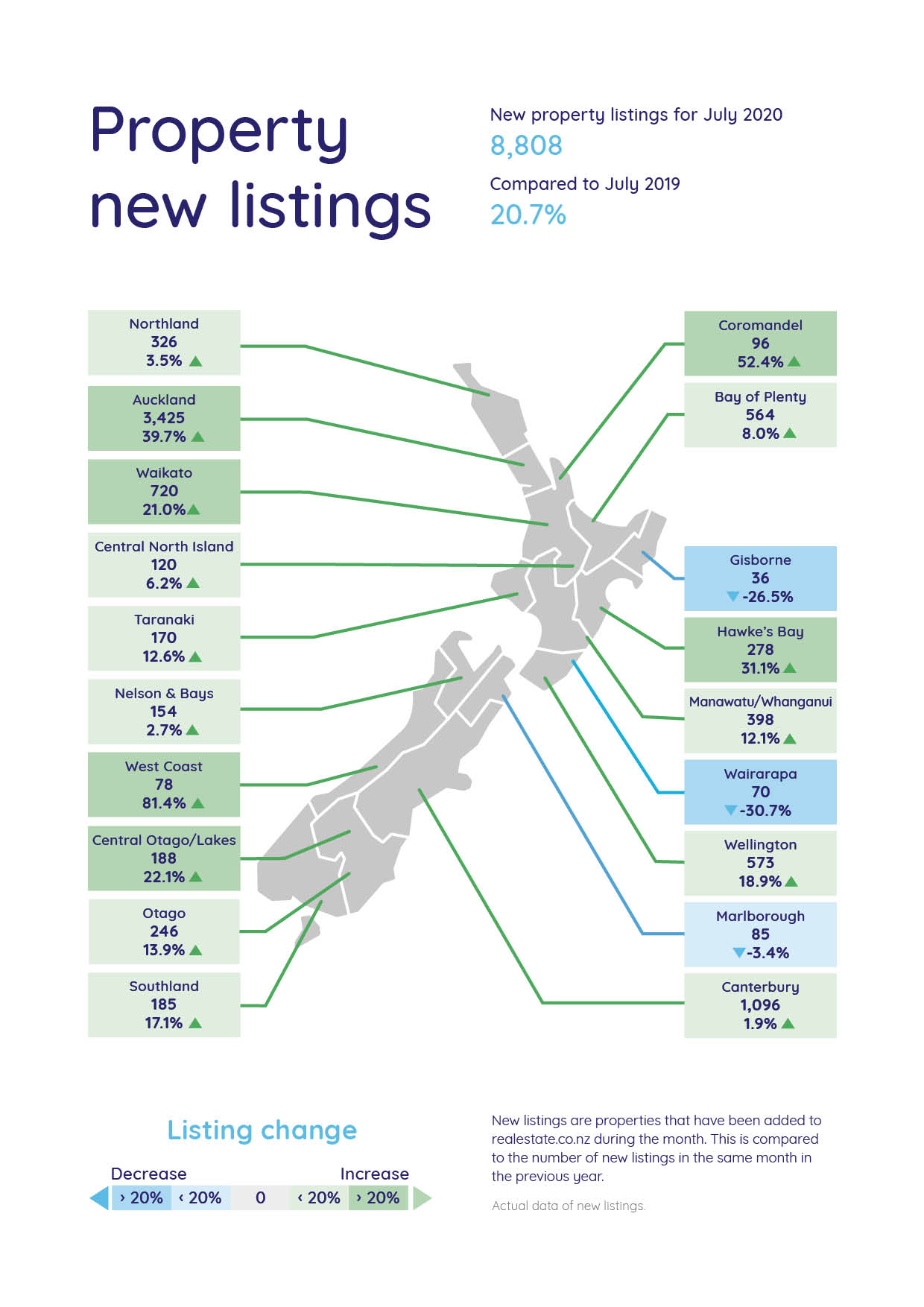

There was a flood of new residential property onto the market in July, particularly in Auckland.

Leading property website Realestate.co.nz received 8808 new national residential listings in July, which was up 20.7% on July last year, and was the highest number of new listings for the month of July since the tail end of the last property boom in 2016.

The rush of properties onto the market was particularly strong in Auckland where 3425 properties were newly listed for sale on the website in July, up 39.7% on July last year, and the highest number for the month of July since 2015.

New listings were also up strongly compared to July last year in the Waikato +21.0%, Coromandel +52.4%, Hawke's Bay +31.1%, Wellington +18.9%, West Coast +81.4%, Central Otago-Lakes +22.1%, Otago +13.9% and Southland +17.1%.

The only regions where new listings were not up compared to July last year were Gisborne -26.5%, Wairarapa -30.7% and Marlborough -3.4% (see chart below for the full regional breakdown).

July was the second month of strong new listings growth, with June's new listings up 19.7% compared to June last year.

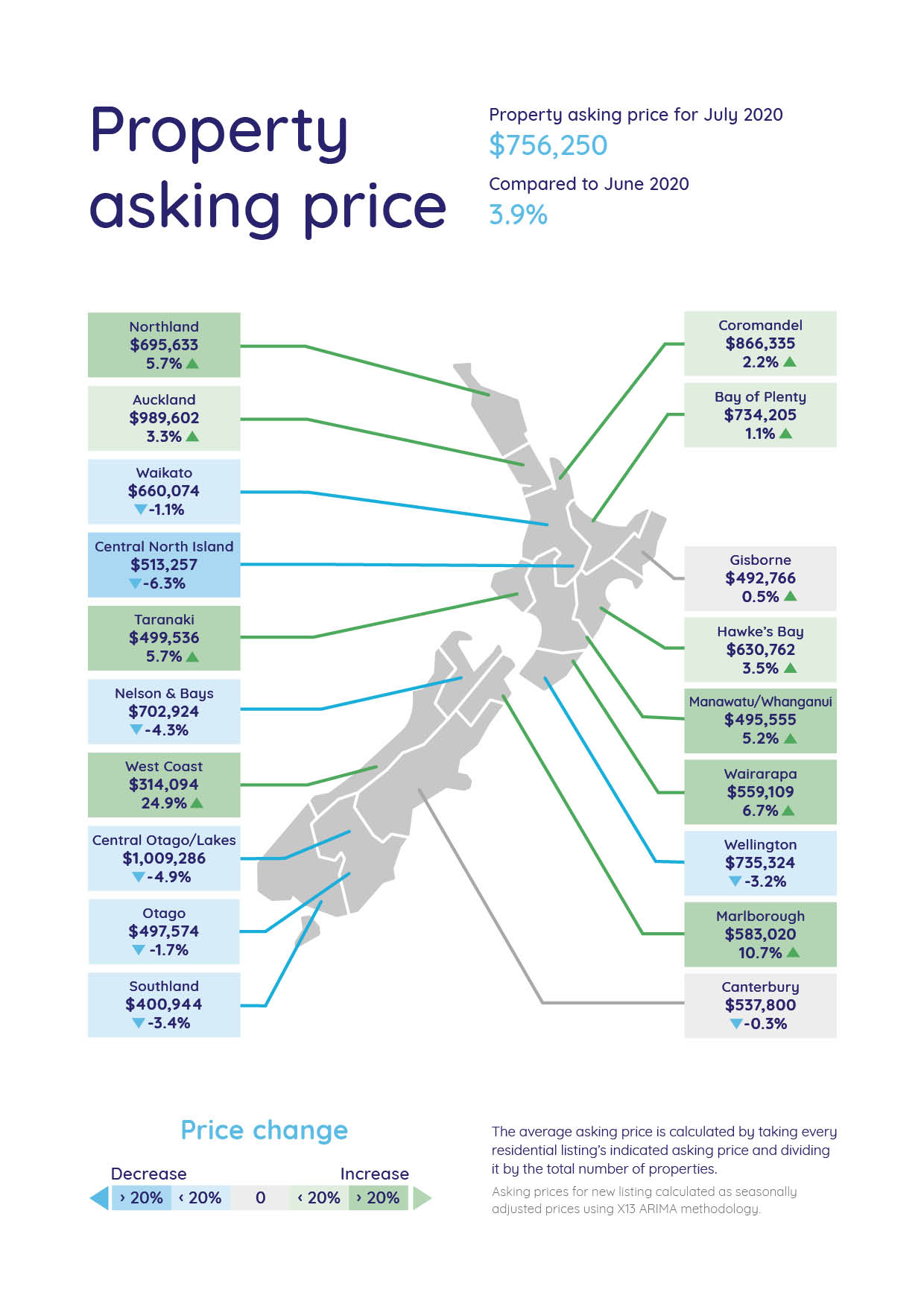

Vendors have likely been encouraged by the generally buoyant housing market since COVID-19 lockdown ended, which has maintained prices near the recent highs achieved just before the lockdown commenced in March.

The average asking prices were a mixed bag in July, tracking higher in 11 regions compared to July last year and declining in eight.

The biggest increase was on the West Coast where the average asking price was up 24.9% in July compared to the same month last year, while the biggest decline was in the Central North Island where it declined by 6.3% (see chart below).

116 Comments

Total listings July 2020 in each region compared to July 2019?

Notable that Coromandel listings were up 53% , thats all those Baches and holiday homes that are a big expense for the family, and a huge amount of dead capital lying idle for most of the year .

Yeah not much demand now air bnb is toast

The 'Air Borrowed n Busted' market could be quite interesting to watch over the next year or two... Over 2% of New Zealand's housing stock! I should add that this is already hammering places like Spain where the remortgaging of the family home occurred to have a holiday place that could be rented out at a premium for the rest of the year. Was it Gordon Gecko that said 'Greed is good?"

The majority of bach owners were only able to buy the bach courtesy of the income they could get renting it out. AirBnB and the likes brought a whole new type of bach buyer into the market, and in doing so pushed up the prices of baches to the equivalent (or higher) of city homes. For instance a 70m2 hydro house in Twizel is selling for around $500k. Stupid prices! Now these families are having to pay for those half million dollar mortgages on top of their OO mortgage, and many are struggling. Even those who still have jobs. God help those who have lost jobs or are on reduced incomes. I think many would have held out to the end of the school holidays to honour existing bookings, but now its all over rover until December, and I doubt those people will make it that long.

You asked the most pertinent question MortgageBelt, total housing stock is down 11% in NZ !!! Down 5.6% in Auckland and is down even in Coromandel 14.1%. But I guess it makes for much more dramatic reading saying listings are up and most will conclude (wrongly) there are many more houses for sale so the price will go down

Which means the buyer is down more.

It would be greatly more helpful and informative if RE NZ stated how many of these "new residential listings" were in fact new builds that are not ACTUALLY finished or even started. I have been to the trouble of counting them on the RE NZ site: it is between 27-35% of the category "houses and townhouses". These are not owners selling. But the impression is given by the site that they are. And I keep a record of listings of houses and townhouses by area, at regular intervals. This week, Auckland City listings of houses and townhouses are up 23% on 2019 at same date. In NSC it is 1.5%. In Rodney it is down 13%

In Auckland as a whole it is DOWN 1.5%. So, whatever is coming to market, a lot of it is not owners selling houses they currently live in.

I suspect that you're right, that most of these are new builds and probably safe to assume considering how much private residential building has been going in Auckland. It's probably been the main driving force in keeping the upper price bracket rising where the lower to mid has remain fairly subdued. Also noticed that most of these private builds seem to be Chinese which is even visible in the auction results (Buying up residential areas for new builds probably being sold to offshore owner).

This and the headline on Saturday "Sales achieved on 58% of the properties at auctions monitored by interest.co.nz"

Well, strap in boys and girls, we are going for a rough ride!

Houses and townhouses in Manukau City on RE nZ, compared to a year ago: - 4.7%

Waitakere City: - 4.7%

AC: up 23%

Hibiscus Coast - 15%

Auckland as a whole - 1.8%

Listings for all of NZ on July 28th: 27,707 on RE NZ

On first day of lockdown (March 26th) it was: 29,822

On that day Auckland total listing was 10,581

Today it is 10,437

On March 26th the total listed houses and townhouses was 5798. Today it is 5698.

Looking at the bark of the tree does not show the wood/forest. That is the equivalent of looking solely at June and July.

Suggests that the smart money is running for the exits before the wage subsidy ends and mortgage holidays come to a halt!

Yeah it's going to be much harder to explain how house prices are rising in Auckland when there's mass unemployment.

Unemployment is not a problem, lack of income is. The government will most likely provide more income support if unemployment gets too high

Unemployment causes lack of sufficient income, which in turn prevents people from buying in properties, Not only that be we can't expect tax payers/banks to keep subsidizing mortgages and even rents indefinitely.

"we can't expect tax payers/banks to keep subsidizing mortgages and even rents indefinitely."

You're sure about that? (not saying it's right, only suggesting it could last much, much longer than most think)

There is a possibility for short term. But you can't just create money out of nowhere. If government just keep printing, not long we will have inflation issues. When we get to that stage, we will be forced to rise our interest rate, it will be a disaster for property market.

or we head into a liquidity trap - but same outcome, interest rates will eventually have to rise

That isn't how printing works. The "printing" doesn't become money in the economy until it is lent out by commercial banks. Of course central banks are doing absolutely everything they can to prompt banks to keep lending and prevent a credit crunch or liquidity crisis but if banks don't lend then only helicopter money or some other direct government spending could contribute to any possible inflation. And we'd probably also need NZD to weaken significantly in relation to other currencies, which is something Orr has stated he wants, but has so far failed to achieve. Weaker currency is also what Powell wants, but struggles to achieve.

And even then, for inflation to happen, the amount of money being printed and then actually spent in the economy would need to be MORE than the massive hole that has been left by reduced spending during the lockdown, reduced or lost incomes and any subsequent cuts back by households and businesses.

The "printing" doesn't become money in the economy until it is lent out by commercial banks.

Commercial banks don't need 'money printing' to lend. They've been creating money in the form of mortgages. This is probably the single biggest driver of the bubble. Would be good if all NZers could get this down pat.

https://positivemoney.org/2012/10/still-unconvinced-that-banks-create-m…

Errrm. JC, you know that it's a lot more complicated than that! Retail/commercial bank lending is a complex system influenced by regulations, reserves,capital ratios and interbank lending. They don't just make money lending to us schmucks, they are busy doing all kinds of stuff between themselves and other financial institutions, whether they be sovereign wealth funds, derivatives, REPOS whatevs. All the churn between all the financial institutions in the financial system are all ultimately still dependent on animal spirits. They all still need to have some semblance of trust in each others solvency and pricing of risk. They will all be making their own assessments of risk, and right now, that almost certainly means more conservative lending behaviour and focus on exposure to down side. Central banks can't make the retail/commercial banks lend freely, the printing might make them feel more reassured about liquidity but that didn't always work during the GFC so who knows?

Errrm. JC, you know that it's a lot more complicated than that!

Beside the point. King explained very well why the central banks haven't been able to stem the flow of money from commercial banks.

Unemployment is the problem. When you're unemployed, you're not thinking about buying a house and taking on a gigantic mortgage. No matter how much 'income' the govt gives you. Or do you think WINZ will start paying out $1500+ pw per person?

Unemployment is a big problem but so is bank lending. Even if government matches your wages via WINZ so that your income remains the same, banks won't consider you a desirable borrower.

Yes bank lending (or lack of it) is crucial and underpins house price growth. Residential lending for July fell off a cliff compared to July 2019. It will be interesting to see if this is a growing trend over the next few months.

A thought: will people get trapped by tightened borrowing standards in a similar way to negative equity? E.g. the bank won’t force you to sell, but they also won’t approve you to buy again if you do sell.

Yes, banks will tighten lending in an attempt to keep bad debts down, further reinforcing the downturn.

Based on RBNZ's current performance, I wouldn't be surprised by a reverse-LVR restriction. A *mandatory* amount of high LVR mortgages.

I know you're joking, but that scenario could actually happen.

Hi kiwi,

What "downturn"?

TTP

I wish I had you "sense of total optimism" TTP - perhaps you should start manufacturing and marketing those "rose colored" glasses for all us DGM'ers ......by the way do you read the news outside your area or do you think only the cities will be affected and the rural areas and smaller towns won't be affected ?

For shorthand we need an acronym for the opposite of DGM.

Crazy Horse's "sense of total optimism" (SOTO) isn't bad.

STO drop the of.

There's already a term for these - Bulls and Bears. Markets follow their sentiment when collected together.

TPP is so invested in the DGZ he despises the DGMs.

This has been seen many times in many housing markets around the world. I mean maybe the Australian banks have a different culture to all the other banks in the world and will just carry on lending as they have been, but they would be massive global outliers if they did. The RBNZ is certainly behaving in step with all the other western central banks.

My guess is that for a time, banks will compete heavily for the most solvent and desirable buyers with very low rates (ie big deposits/equity and secure jobs). Then there will be a sliding scale of relative credit tightening for everyone else with a general reduction in DTI multiples. We were offered x10 DTI by our bank in 2017/18, which I was really shocked by because in the UK it was capped at 3.5 or 4.5. I would bet I wouldn't still be able to get x10 DTI and am hearing lots of reports of banks scrutinising income and expenditure and just generally offering smaller loans.

10x DTI???? Holy f***. Be right back, I'll just go buy a 6br waterfront property...

Hard to square with supposed stress tests at 7%. 7% interest + ~3% principal at 10x DTI is all of your income!

Unless you don't mind renting from the bank on Interest Only forever. The interest only headache between 2010-2018 will come and bite us on the arse in the next few years. It's great when prices are going up... on the way down not so good. Just ask the Irish and North of Englanders now living in New Zealand with homes abroad still under water.

To be fair to them, we had a huge deposit and other assets in the mix. But there are plenty of people who have an overall loan portfolio that is many multiples higher than just their employment income because the banks have included all kinds of things and alternative income.

For us personally, we were looking to borrow to build a garage/sleep out so they wanted a rental assessment on the build (students and air B&B) to include as income and increase the amount they could lend us, even though we had zero plans to rent it out (and they knew this too). If the banks want to lend, they will find all kinds of ways to increase the amount they lend you, if the banks don't want to lend, they start going through you expenditures and adding takeaways and haircuts to your monthly outgoings and reducing the amount they will lend.

Banks will accept very frothy rental and home valuations when they are in a lendy mood and then the exact opposite when they're not. It's just standard behaviour.

That may be true but the income the government does provide won’t come close to matching pre-covid income...once the jet ski, boat, second car and other discretionary spends are sold usually the house is next.

Yvil 'Unemployment is not a problem' - what planet are you living on? Unemployment is hugely stressful for those it effects, particularly those with debt and it causes all sorts of relationship and societal issues... FIrstly, I'm amazed that 6 people have voted for that comment and secondly that you are still allowed to post on this site.

2nd hand Jetski look to have started to come down in price. A fairway to go yet I'm guessing..

He meant for the property market. Which so far, has proven to be true. The government and RBNZ have acted to suppress market forces.

Toppertee, it would be nice if you pasted my whole post "Unemployment is not a problem, lack of income is." Then I go on to say that the government is very likely to provide some sort of income support. I stand by my post

I doubt the wage subsidy will end. It was a categorical 1st September but we'll see. Low interest rates were supposed to be temporary after the GFC too. Hard to unwind these things.

Toppertee, sorry, the “smart money” would never got into that situation in the first place. It’s more, if you are going to panic, panic early.

Bit of both perhaps? I saw a DFA posting last year with a similar heading. 'If you're going to panic, panic first.'

Agreed. It aint smart money if its still in the game.

Warren Buffett — 'If you've been playing poker for half an hour and you still don't know who the patsy is, you're the patsy.'

Just watched CEO of RE NZ in a video re this announcement.

https://www.propertynoise.co.nz/housing-shortage-driving-prices-up-acro…

She is a spruiker with no facts and is spreading incorrect information. More site activity doesn't mean more buyers, it means many people with a property are looking to see what they can sell their "investment" for.

She is a spruiker with no facts and is spreading incorrect information.

Degree with honours from Waikato in marketing and strategic management followed by 5 years of medicore marketing experience before joining realestate.co.nz Another 5 years and now GM of marketing.

She's no Robert Shiller. That's for sure.

Nope.

But even that is far more than other self-professed 'experts' have behind them.

Its her job to put a positive spin on things.

Nobody would ever list with a company that was taking the negative position even if it is true.

Sellers want to believe they will get top dollar and will always go with someone who is telling them what they want to hear...

'Property Noise'? How fitting.

Perhaps 'Property Noise' could be given a catchier name like ANZ's Truck-ometer to help push it as a means of measuring potential investor distress?

You could even make it rhyme with Truck-ometer to accurately reflect the sentiment that you'd be measuring!

50% of NZ households have less than 5k of cash savings to tide them over in the event of incomes/working hours are being reduced. It would not be long before this placed serious stress on tenants and by association their landlords.

@toppertee , thats the crux of it , most Kiwis have a shocking savings level , with almost no buffer at all .

Working hours are being chopped all round right now , and thats going to feed directly into take home pay very , very quickly

The landlord / tenant relationship in NZ has been historically adversarial , and its going to get worse as people decide which to pay for first , food or rent

@Boatman. Its a house of cards. Even the 10% of Kiwi households that have the buffer of savings over $50K. It doesn't take long for that comfort to erode with a job loss and $1-$2 million mortgage. I'm not sure if people really understand what a tightrope we're treading with respect to NZ household debt to income levels and total lack of savings. You're comments about the Coramandel listings would be indicative of people wanting to create a buffer for tough times. If these homes start selling for lower prices and with lower mortgages written for the subsequent purchase then 'money is being destroyed' from the banks balance sheet and the real economy takes the hit. You ever seen those Western films where the train track over the river has been destroyed but the driver of the train doesn't know that yet?

I'm not sure if people really understand what a tightrope we're treading with respect to NZ household debt to income levels and total lack of savings.

It's not lack of savings. It's access to savings, which is all tied up in the house for most. Liquidity.

Silly me.... It will all be okay!.. People just need to borrow more against the house to keep them liquid! I wonder if that was the plan'edemic' all along.. Create a liquidity issue to save the banks by creating a need for more borrowing worldwide.. hmmh

Silly me.... It will all be okay!

No. It won't be OK and that wasn't my point. The point is that people 'think' their 'savings' is in their house. That means they're more comfortable with low cash reserves and other liquid assets.

In the wider Ponsonby area houses $2 - 3M up to 22 listings from 12 in June

Could that be a sign that people are experiencing mortgage stress and looking to get out of their hefty mortgaged lifestyle? Be interesting to see what those numbers do when we come out of winter. Keep us posted Yvil.

I don't think there's mortgage stress, not yet anyway, it could come for some, maybe in few months but not now. I think the additional listings in July is due to very high prices having been achieved and some thinking "that's a good time to sell, prices could go down"

There must be some -- airNZ pilots, etc -- but it's reasonably well cushioned at the moment (in the aggregate anyhow) by various forms of support: wage subsidy, covid-affected dole top-up, mortgage deferrals.

Some will take the decision to sell the family home and downsize to the BOP/Coramandel second home they already have. Others will sell the holiday home. I think we are likely seeing people look to deleverage and get themselves a cash buffer for tough times. You'd be stupid not too!

IMO deleveraging is the dumb decision. We've seen enough in the last 6 months to accept that house prices here will be underwritten at all costs. This is the kiwi version of the "Fed put" where mass easing of monetary policy takes place any time equities are down 15%. Cash is what you don't want to own, as by definition governments have to debase it to prop up nominal asset prices.

The "Fed put" didn't save Lehman. So if you are very highly leveraged and your income isn't solid, you're still playing a high risk game.

We'll see how wide the exit doors are I guess. At this stage there will be cash that just wants security of a home in an uncertain world where rates on savings are so low. Once that cash goes, you're back to mortgaged buyers and job uncertainty and reduced household incomes will definitely temper the enthusiasm of many to borrow big.

Yeah, mortgage stress in NZ still seems to be much lower than in Oz, which according to the FMA site is badly stressed everywhere - all states, investors and owner occupiers. If Oz is NZ's near future, it will be interesting to see how the banks and govt behave over there, given those institutions are essentially the same as in NZ.

Coming months will show the reality of housing market in NZ.

One of them is someone I know, they have a 7 digits mortgage (with a 2 in front)and now they are panicking!

I'm not worried about people with $2 million mortgages. Assuming the banks don't just hand out that much money to people on less thank $400k annual income. Also assuming people who take on a mortgage of that magnitude know what they're doing.

A $500k mortgage can be just as bad or even worse. And that's the average young couple who scraped together a deposit by draining their kiwisaver, plus 'a small gift' from their parents, and bought a dud.

Errrrm yes they do. One of my fam, had 2mil in home loans, was earning maybe $110-120k until made redundant. Owns several properties so provided his tenants keep paying and he doesn't have to sell, he'll be okay living for a time. He was planning on ploughing his redundancy pay back into property and has no inclination to diversification. I think he might not find the banks all that keen to join him on that in the near future though.

“Know what they are doing?”. Not even sure a person with financial acumen could account for the 1 in 100 event that is covid. A couple who are both air pilots could service a large mortgage like that pre-covid; post covid they should be very worried.

By "know what they're doing" I mean prepared for bad days. Yes, even bad days like COVID. I'll buy a house next year, but I'll keep at least 1 year's worth of living expenses in the bank for rainy days, instead of going for a $1.2 million house vs. a $900k one...

Buying a luxury home with high LVR is either speculative or idiotic (not mutually exclusive). If they have a low LVR, they'll be fine, just have to sell now and switch to a less luxurious lifestyle.

I think it’s a massive assumption that higher income earners are more likely to have their finances in order....it’s often people in higher income brackets that are trying to keep up with the Jones’s spending well beyond their high incomes allow for on credit.

Lifestyle inflation.

Vanity - if you take a look at Digital Finance Analytics' mortgage stress data for Oz . It is the affluent postcodes that are being the hardest hit in Australia at present.

Can't remember where I read it but almost 2/3 of luxury cars on the road are in some kind of finance.. don't judge the book on its cover I guess!

Yes, its central suburbs in all the major cities that have most stress.

Didn't Isaac Newton, considered to be one of the sharpest minds to ever have existed, lose a fortune in the South Sea Bubble? He was considered financially savvy, he even sold out early on thinking that the prices might correct and then got totally caught up in FOMO and bought into the bull trap.

I think depending on circumstances, pretty much anyone can be susceptible to contagious ideas and associated risks, financial or otherwise.

Overall stock still looks pretty tight though. I reckon the proof will be in the spring lift: when, and how big.

In 2018 the spring rush started in mid august, and there was 25% more stock by xmas. 2017 had a similar 25% pickup but didn't start until late Sept (election, probably). 2019 was very different, pickup didn't begin until well into October, and there wasn't much -- only 8% more at xmas.

I spent the weekend at the bach in Pauanui, I had a look at Richardson's window display, (No1 Coromandel RE agents), there were barely any houses for sale so I went in, expecting them to have struggled. They said nope, we have sold most of our stock, we are desperate for new listings. Yet RE NZ shows a 52% increase in listings in the Coromandel, very strange, maybe be micro location dependant?

Perhaps RE NZ asked the wrong Richardson's office?

Could well be the canary in the coal mine, some of these areas. If you hit financial stress, which are you going to sell: the family home, or the bach?

Holiday home goes first. The next negative tension will be 'how much can I get' followed by 'who's going to buy.'

I meant it as a rhetorical question which agrees with your answer. Though thinking a bit more I wonder if it would be different for boomers whose kids have gone and have more “family home” than they need.

Same story in Whiritoa - overseas returnees are snapping up holiday homes as have to have the "boat,Bach, Bmw...all cashed up and nothing to do.

Really? You relocate halfway round the world in the midst of a global pandemic and the first thing you do is go out and buy a holiday house?

overseas returnees are snapping up holiday homes as have to have the "boat,Bach, Bmw...all cashed up and nothing to do

Tui ad. Actually I do know a lawyer returned to NZ from a corporate role in SEA. He's been marketing fishing charters out of Auckland. Another lawyer who still has a firm overseas is currently holed up in Queenie. Never struck me as a tech-savvy type so wonder how the business is holding up.

Wow , 52% increase in stock levels in the Coromandel !

I have always looked askance at the prices down there, way over the odds when compared to say Mangawhai (or even the Gold Coast) , and thinking I would only buy a property there on my retirement , or possibly just rent long term .

Either way , its very likely we will see some prices on the Peninsula drop back to more sensible levels over the next 2 years as this pandemic wreaks havoc all round

The longer the pandemic lasts the more companies will close their Goffam city office and the staff work from places like Coromandel.

Far more productive working from home than battling traffic to the Auckland CDB and then negotiating road closures and construction around Queen Street.

Sales in Auckland, by selected price bracket shows that FHB is NOT where action is:

Jan-June inclusive, residential sales 2019, price 700-950k: 2901.

In 2020 it was 2622.

So, down 9.6%

Now look at 1.4m and above: 1258 in 2019 and 1544 in 2020: UP 22.7%

In June alone, the 800-900k bracket sales were up 7.7%

Over 1.2m they were up 47.7%

Apartment sales in June were up 19.5% compared to residential (excl apartments) up 12%

Yet all media keep reporting ANECDOTALLY, long queues outside shoeboxes that FHB want to buy?

Rich folk are selling far more than those lower down.

Someone might ask why and to whom, instead of FHB obsession.

Like stock market, I suspect rich are getting out while prices hold up

Sales in lockdown in April and May were 57% lower for bracket 700-900k, compared to 2019 for same months

In 1.4m and above bracket, they were only 42.7% lower.

Yet, in June, when free to go to open homes etc, sales in 800-900k bracket only rose 7.7% on 2019

While in 1.2m plus bracket rose 47.7%

Suggests that more expensive property is selling without buyer viewing, perhaps from places not in NZ?

Not too far to happen here....

https://news.knowledia.com/AU/en/articles/sydney-and-melbourne-house-pr…

...New Zealand is not Sydney or Melbourne. Our housing market is "Armor Plated"

You could say it's armOrr plated...

Hand me my longbow...

Every agent I talk to says they cannot get their hands on enough stock...

The demand is THAT great. Everything going to multi-offer.

The stock might be up, but the demand is through the roof.

Is it possible that RE NZ talks to a bit more agents than you do?

Is it possible you can't read? I'm not saying the stats are wrong, I am saying that demand is soaking up all at extra stock.

Is it possible you can't read? I'm not saying you said the stats were wrong.

Well here's a bellwether. 139 Ladies Mile went for more than 500k over CV today. I'm f***ed if this is a property bear market, demand out there is nuts and more than enough to take us through the September "cliff".

Anything with a bit of grass in the suburbs is getting frenzied bids, there seems no limit to what people will pay.

The market feels like it's popped higher, there is going to be tears.

Sold for $1,100,000 in 2016. Are you saying it went for North of $1,700,000? A bit rich for 144m2 but it would have tugged at a lot of NZ born Kiwis heart with the construction, character etc.

My feeling is a number of these new listings are on the bottom of the scale.

Interest, why did you choose not to talk and show the graph about total housing stock which is DOWN 11% in NZ ! Down 5.6% in Auckland and is down even in Coromandel 14.1%. Many people will wrongly conclude there are more houses for sale so the price will go down

I'm no expert, but I'd say that once the YOY monthly asking price dips below 0% (esp. in AKL), get ready for the carnage!

How would listing average over Feb ,March, April and June ?

I spoke to a real estate agent last week ,in this person's area they had six listings between 12 agents ,quite worried,however,they said the prices being asked for some of these properties was absurd and unofficially they wouldn't recommend buying right now.

It's a mixed bag out there,I get the vibe that certain areas will drop dramatically and some will hardly move,time will tell.

So with Labours new tenancy bill, you nice tenant can move in gang members and you cant ask them to leave. All those that leveraged up in the thriving centers of Hawkes Bay and Tokoroa etc....coming to a rental near you.

One thing to bear in mind is that over leveraged investors cant offload their investment properties until they can get rid of their tenants (to either renovate the property and get it ready for sale, or to deliver vacant possession as is to a buyer), and that is only possible in 90 days from the 26th June. The clock is still ticking ...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.