The Government is broadening KiwiBuild and introducing a similar scheme whereby it will underwrite, and in some cases invest in, housing developments.

The aim is to make it easier for developers to secure finance at a time banks are expected to be more cautious with their lending.

The underwrite would see taxpayers buy a property below market value, if a developer can't sell it.

The eligibility criterion outlining which sorts of developments would qualify for an underwrite or direct investment from the new ‘Residential Development Response Fund’ is still being designed.

However Housing Minister Megan Woods said the fund would “help to progress stalled or at-risk developments” that support the Government’s “broader housing objectives such as ensuring the supply of affordable housing and providing jobs”.

She said it would “support the sale of a range of housing types and price points to meet financiers’ presale requirements”.

This arrangement is basically a broadened/less prescriptive replica of KiwiBuild, which requires developers to build houses with set design features and price points, and sell them to first-home-buyers.

Developers who get support from the Residential Development Response Fund can sell the houses to anyone.

The underwriting approach is similar to the KiwiBuild, however the Fund can be used to purchase properties or underwrite sales at any stage of the development, to help developers experiencing cash-flow issues part way through a development.

Woods estimated it would enable 4,000 new homes to be built “that otherwise might not be built because of barriers to developers securing finance”.

In terms of funding, $100 million is being allocated towards the scheme from the Covid-19 Response and Recovery Fund, and $250 million is being redirected from KiwiBuild.

“As we saw following the Global Financial Crisis when house building halved between 2008 and 2011, credit can be harder to access in uncertain economic times,” Woods said.

Reserve Bank Deputy Governor Geoff Bascand last week said there was some indication banks were becoming more cautious, despite demand for credit dropping.

He reiterated his plea to banks to keep lending, saying now was the time for them to dip into their capital buffers.

Woods said: “We know from talking to the building sector there is a relatively solid pipeline of construction activity until the end the year, but the outlook beyond that is unclear.

“Providing assurance through the fund will ensure developers can keep building homes, and workers employed.”

The aim is for Kāinga Ora to be ready to start receiving applications from developers in the first half of November.

Another KiwiBuild reset

Separately, Woods announced changes to KiwiBuild to give developers more flexibility.

Should developers struggle to find an eligible buyer for a KiwiBuild home, they will now be able to:

- Sell it to a progressive home ownership provider, community housing provider, and if suitable, Kāinga Ora, which can use the property for public housing.

- Sell up 25% of KiwiBuild homes in an underwritten development on the open market, rather than 15% as was previously the case.

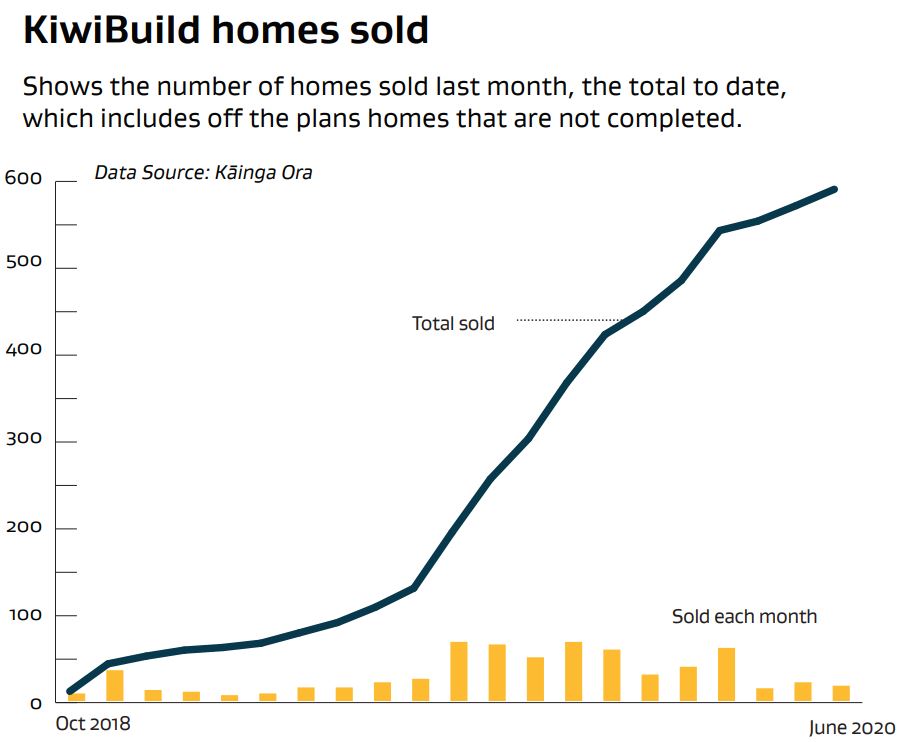

589 KiwiBuild homes have been sold to date. There are 302 on the market.

Labour, at the 2017 election campaigned on building 100,000 houses over 10 years under the KiwiBuild programme.

Woods in September 2019 ditched all numerical targets around KiwiBuild, recognising the Government had underwritten unsuitable houses to essentially get runs on the scoreboard.

As a part of the KiwiBuild “reset”, the Government also reduced the amount of taxpayer money put on the line to pay developers if they couldn't sell KiwiBuild properties.

KiwiBuild aside, the number of building consents issued was on an upward trajectory until Covid-19 lockdown.

Building consents - residential

Select chart tabs

66 Comments

Over-supply and banks unwillingness to extend or re-negotiate credit. This is the stage 5 of a housing downturn

And what this idea from Labour strongly intimates, is that this problem is now coming into the face of NZ. About 4m ago, the CEO of Citibank sitting next to Trump said "This is not a credit crisis" At which point my rejoinder was: not yet. But that is inevitably coming. When income streams holding up ridiculous debt are interrupted, all the authorities in world try to bolster those income streams. But it only takes about 6% (in case of subprime) to cause cascade of doubt and liquidity counter-factuals to bring down the house of cards. Labour doing its best on extend and pretend and has more rope than many countries but they cannot keep it up past January 2021 I would say.

So you are saying that Labour will try to hold the market up, but will be unable to do this for more than four months post election, then the taxpayer will own up to 4,000 properties at above the ultimate market value?

I think he's saying the credit crisis/crunch will hit very early next year.

The point is, the government will need every one of those 4,000 houses for Kāinga Ora's social housing portfolio if a global Depression takes hold. And if it does take hold, nearly all commercial and residential construction will stop dead in its tracks.

Why buy them near the top of the market if the crash is inevitable? Just let the market do its work and let prices fall. Also, if I had sufficient private means to buy a home, the first question I would ask is if the Government had guaranteed the development as I may not want to live next to State Housing. Taking the guarantee almost ensures that the houses will be less marketable to private buyers.

Both good points EE, I would guess there are a number (if not most) FHBs with young children who would be less than keen being a neighbor to Kainga Ora. If Labour think they can buy/build 4000 homes now, what's changed since the abysmal failure of Kiwibuild? Or is this just another iteration of Kb by another pathway? The fact that only 600 homes have sold in 21 months means the developers are either building the wrong types of houses or they're in the wrong places.. or both.

Why buy them near the top of the market if the crash is inevitable?

Two reasons

1, Have to keep this afloat for a couple more months until after the election.

2. We have a reactionary Gov't not proactive.

These are new builds - much wiser investments for Kāinga Ora than buying old houses and then having to upgrade/retrofit. They already own a whole lot of those in their housing portfolio. The more new builds they acquire, the more old stock they can retire to the private sector.

That idea of whole neighbourhoods of state housing is a thing of the past. It only becomes a market/price/NIMBY issue when talking greenfield development.

Re: old stock they can retire.. so when National did this it was unforgivably passing the burden to community organisations who couldn't afford the upgrades and private landlords who were in Nationals pocket and would profit off the vulnerable. Now it's a good idea because it's cheaper than upgrading/refurbishing. Interesting?!?

As for greenfield development, I think you'll find the concerns regarding Kainga Ora housing plonked amidst existing suburbs without any consultation with or consideration for existing community members might be a bit more negatively received than a greenfield development.

National's problem was they sold off more than they built, hence the stock shortages we are dealing with now, on top of the burgeoning wait list. A double whammy.

Re your second point, such 'existing community members' will just need to get used to it. I recall the big outcry when a large apartment complex threatened to change the grammar zone line - and the hilarious thing was David Seymour and his "Freedom to Build" mantra went right out the window. He folded being 'in' the grammar zone into individual property rights - the anti-thesis of the neoliberal notion that property rights end at your section boundary.

I have very little sympathy for NIMBYs. The more they become separated from their closeted lives, the better they become as citizens.

National sold the existing social housing stock to predominantly community providers so there was no nett loss, just different owners.

As for your comment regarding existing community members, I take it you're unlikely to be one of them. Like it or not there have been many accounts regarding Kainga Ora "clients" and their lack of neighbourly values, quite valid concerns IMO. I fail to see how being subjected to intimidation and loss of quality of life makes someone a "better citizen"

New shitboxes instead of old ones. At least the older ones had decent bones.

yes, Kate, thank you. That is just what I am saying.

I am a Real estate agent but mostly analyser buyers.

Am on linkedin with regular contributions.

I feel Auckland market is headed for over-supply and this is mostly due to drop in demographic between 25-44 in 2018-23 plus huge increase in consents in last few years.

And add to that CV19 impact on credit

Agreed. The next govt gets to decide who it will financially punish for this mess.

I’m in favour of this. It seems our predisposition towards overvaluing property is such that nothing can stop it; so build, build, build! Every house in Auckland is worth a million dollars, so think what it’ll do for GDP!

Exactly Mike.

‘The underwrite would see taxpayers buy a property below market value, if a developer can't sell it.’

Surely if a developer can’t sell it you just keep reducing the price until a buyer gets interested. Without that how does the government ever know what the market value was. This idea is simple lunacy. Let the prices fall to meet the market rather than taxpayers bailing out daft deceleoperes who paid too much for land and daft banks that funded it all!

Message from government : Do what you want as we have the printing machine to print as much money we want but just keep the ball rolling at whatever cost.

Who is at risk Tax Payer and country at large and who benefits - people who have streched and speculated or entered in high risk projects.

So does this men we will get 104,000 homes?

Probably means about 25 homes, 3 years from now.

This is exactly what I said they should do about 2-3 months ago

It's almost like there's a message there: expecting people to take on 30 years of punishing debt for a 70sqm two bedder isn't sustainable.

Never was but the general populace swallowed the idea hook, line and sinker. The ruling elite have been complicit in this farce.

Within business and risk management this is generally known as "escalation of commitment" essentially a lose-lose policy. They'd be a whole lot more effective to regulate the housing market, but don't want to do that as too many MPs are housing investors.

How should they regulate housing market? you mean ration it? regulate the prices? forbid private sector to construct houses? forbid private ownership of houses? do not allow investors to get bank credit?

> do not allow investors to get bank credit?

that would be one of the sanest and most effective ways to change the balance more towards OO properties. Even better, heavily restrict investors buying existing houses unless they commit to redeveloping the site in the next 24months, (with large penalty if they don't do it). Let them buy new builds if they want to buy.

"The underwrite would see taxpayers buy a property below market value, if a developer can't sell it."

Errr.....

Whatever ANYONE pays for a property IS market price!

Do we think any developer will on-sell to The Government if they can get more than that and establish a higher market price? No.

So whatever is paid IS market price....and any buyer should be aware of that.

Buy one of these in any development, and if ANY sell below what you paid - Voila! You have a new market price for the re-sale of your property.

(It's just like buying Off The Plan, and if another buyer can't settle, then the Developer sells them up for 80% of what they contracted for ( keeps the 20% deposit + 80% - they are happy!) any other proeprty is tarred with that brush.)

Exactly. The 'market price' means the price at which a buyer and seller meets at a point in time - not the past and not the future. The only way by definition you can sell below market price is to ignore higher bids.

exactly right,this policy is appalling in its stupidity, the market price is what someone will pay in the current circumstances, if the developer is prepared to discount it to the Govt then why? What does he care who is the buyer? why not discount it to a FHB and then the taxpayer is not on the hook.

market price is not v good when no one wants to buy and there is knowledge to that effect.

If no one wants to buy at the market price, then it's not the market price. Someone should remind this government of that fact...

Its all round the wrong way.

More a feast for cost plus everything, councils included.

How does this help affordability

How does this reduce costs

How does this achieve build productivities.

Hint: Anything for the jobs and incomes of the now and To be housed?.

I'm sure all these developments would have been completed eventually (if the houses are wanted with only a short delay), just some not by their current owners. This is just bailing out banks and giving the developers the credit to hold out for the desired price, I would suspect the government knows this.

If the project goes bad and the developer goes bankrupt and the next developer takes over for cents on the dollar, such as The Lakes in Tauranga. And if the banks wont lend the new developer will get a really good price.

Another thing that I had suggested, which I think is better than this, is that the government could buy sites with resource consents in place, at a current market valuation (which will include some value uplift following RC approval). Then contract builders to build the developments, then sell to FHBs at cost.

The scheme described in the article is still not achieving affordability. My suggestion, by taking out the profit margin that developers require (typically 20-30% of the sales price), would.

Why are you assuming that the cost of build will be equal under government and private developer? it is very likely that the cost to government will be more than the cost +20% margin in private sector. Unless the government is subsidizing the costs.

I disagree.

Why should the cost of building be higher for government? Especially in an economy where builders may be screaming out for work.

Also if the government signs up builders to multiple development projects then they should be able to negotiate lower, unlike all but the largest developers.

Easy to scoff at the Government endeavouring to address housing supply but it is something very sadly needed.

The reality is that housing shortages is a significant driver of housing prices and current affordability issues.

Housing supply does not seem to have kept up with high levels of immigration and population growth - hence many currently housed in motels, and rents and house prices driven up by competition and aided by low interest rates and accommodation supplements.

Unfortunately 600 KiwiBuilds is a failure. Underwriting to “help to progress stalled or at-risk developments” makes me very nervous.

Maybe, rather than Government trying to encourage houses for private ownership - which even the private sector builders have shyed away from - they should just settle for more state social housing creating less pressure on private sector.

Whatever happened to the idea of an Empty Homes Tax? Some thought it might help with housing supply and market rent. Does anyone think it might be helpful and work in NZ ?

“The underwrite would see taxpayers buy a property below market value, if a developer can't sell it.”

If the taxpayer is paying more than what the developer can sell it to the market for, which would be the case in this scenario, the taxpayer is by definition paying above market value.

I think the scheme would buy the properties at cost + a negotiated margin, similar to what Fritz is suggesting but still below market. Having said that it seems to me that we'll get more situations such as what arose in Te Anau and BellBlock in New Plymouth

Something like cost + negotiated margin seems likely.

For me it really comes down to the definition of “market price“, being the price that the free market will pay at that point in time.

If the government pays, for example, $500k (cost plus negotiated margin) because the developer can’t sell it on the market for $500k, then “market price” is by definition below $500k and the government is buying it above what the market will pay, being the “market price”. To know the market price, the developer would need to keep reducing the price until it sells on the open market.

I would think that's the point to make sure these houses don't sell for market value and start setting prices lower. The government can't be that stupid to believe this policy makes houses cheaper.

Houses will drop in price during a credit contraction no matter what the government does. That said though, if it set out a schedule of accommodation supplement reductions going forward - that would likely have a negative impact on house prices. Not a plummet but a steady gradual decline based on the timing of the reductions.

Of course but they can delay it and hope for the absolute best. They can extend and pretend that with some miracle cure, treatment or vaccine will turn up that its all BAU by next year. I can't see how the Melbourne lockdown does not eventually take out one of the big 4 and its NZ subsidiary triggering the beginning.

Housing market my a$$...

https://www.newshub.co.nz/home/politics/2020/08/the-number-of-propertie…

AND one expect them to introduce CGT... lol

Why do I get the sinking feeling that this scheme will continue and expand if Labour win regardless of whether credit conditions improve.... they love intervening in property markets to fix problems caused by legislation in property markets.

So what's the problem caused by legislation?

RMA (undersupply) + Tax status of housing (overdemand) + Council incentives (undersupply) = Less houses built at a higher price.

Admittedly this is a comment on the housing market in general and the government's propensity to throw legislation at problem's caused by legislation

why dont they just become a 2nd tier lender charging interest at that level. if the development doesnt work they step in and complete the development for themselves.

I like the idea of the gov’t encouraging developments to continue by guaranteeing a floor on the price, in all honesty. So long as the floor isn’t too high - say, at a level where the developer is making a modest but not disastrous loss. Developer sells units for whatever they can get, the rest goes to State housing at a discount. Don’t see a serious downside pragmatically speaking, though the concept has elements in it to piss off both capitalist and socialist dogmatists...

But, but, but, everything these days has to painted and believed in as Most Excellent and Good, or Most Awful and Bad, so as to encourage us all to be tribal. That way, the banks, the ploiticians and ex politicians and the bureaucrats who benefit from the mess can keep their jobs while we argue and fight amongst ourselves.

You appear to be suggesting that a wide range of schemes can be adapted by reasonable men and women to be perfectly functional. I mean, that is pure heresy to our preisthood.

This is just what they did for Kiwibuild, which saw developers put properties on the market at a valued price, which by definition has a range.

They were then listed at the top end of the range and when they didn't sell, the Govt. ended up buying them at the lower end of range/market value, so did not get a discount all.

What we need is affordable, warm, dry, healthy homes, Not what we will get being unaffordable, low-quality housing.

Given our building regs - what do you mean by low-quality new build? Any dwelling meeting today's code must to mind mind be well insulated; weather tight; have a heating source and have adequate kitchen/bathroom amenities.

Good question

Building regulation in NZ are on a different planet to what I experienced in the UK. I would say that compliance in NZ involves 75% more time and cost than in the UK but there is no way NZ houses are 75% better in quality. However, my tradies work to a much higher standard than the UK, even on stuff that isn't regulated and inspected. Go figure.

On a different planet - meaning under-specified/loose; or over-specified/rigid? Or a different planet because of the compliance/inspection regime?

I'm surprised you think that Kate. It's well known that our building code is a joke by overseas standards.

They are not well insulated, yes they have more insulation than in the past, but still very low by international standards. They are not windtight, or airtight so the effective R-value of an NZ house (which is already low), is up to another 50% less than this already low value. The mixed methodology they are using is just setting us up for leaky homes version two.

The heating source is completely inadequate for whole-house heating.

While other countries, especially their Govt.s are making quantum leaps in building quality and methodologies, NZ the supposedly 'Green' country is like 30 years behind what we know we could do.

Anything built to NZ standard today is like replacing an old model T Ford with a 1970's Nissan, newer and better than what it replaced, but still poor quality and way overpriced.

I recall plumbing in central heating radiators myself in the upstairs rooms in our house in 1984, when our first child was on the way. So more than 30 years behind, more like 50. Funny thing was, being impecunious at the time, it only cost about 10% more to heat the whole house all day long than just the downstairs in the mornings and evenings. That was a big surprise. As you say, drafts are the biggest factor.

The minimum wage will continue to increase (a Labor promise that they are delivering on). There will be more regulation and compliance costs only increase. Energy costs will increase (with green initiatives that is the only way the costs will go). Construction material will be more expensive (due market conditions that are very unlikely to change). So most inputs are going up.

The only significant cost component that may reduce in an economic downturn is land values. But since the supply of new land relies on NZ local and central government, i struggle to see that cost is reducing anytime soon.

Having said that, supply of new houses is only important if there is continued strong demand. The strong demand in turn mainly relies on net positive immigration (with a lag of 3-10 years I would think, i.e. a new immigrant family takes between 3 to 10 years to buy their home. So the strong demand for NZ house is likely to be around for another few years given the all time high immigration numbers in the past few years, unless we see an exodus to Australia/UK/Canada).

I

Um, shurely the nice graph should have the vertical axis running to 100,000 (or if its an annual target, 10K)....

Oh great, more licence for developers to build stuff they know nobody wants with the knowledge the government will bail them out when their properties inevitably don’t sell.

We are already seeing this with the LakeSide development in Te Kauwhata being bought out by Kainga Ora.

https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=12339757

I am building in Te Kauwhata currently, and as far as I can work out, this was Wintons plan all along, because they couldn’t possibly have believed their development would be successful at the price point they were asking, when for very little extra money people can go to either of the other subdivisions in town and buy a real house nearly 3 times the size with at least 5 times the land.

Very cunning, those Winton people.

You give too much credit to the developers, more like very stupid the Govt.

For developers, it's like taking candy off a baby, no extra skill needed.

It's fairly obvious that this is about keeping property prices inflated, and underlines the fact that there are no free markets anymore. Credit crunch is the key part of this, as there is clearly a concern about the ridiculous sums in loans out there. Printed money is looking for places it can be utilised without too much attention being drawn to it.

The fed is buying as many CBMS as they can. The credit crunch is alive and well, and threatening the financial system. They cannot stop printing money, and with every $ they print, the actual underlying problems,( that existed b4 covid came along, remember September repo market), simply get worse and worse.

Real people and real markets rely on real information, and sadly those days are long gone. When the majority start to realise that printing money devalues their savings, and their income, that will be one thing, soon after, they start to realise that their assets, ie, their houses, are being devalued in the same way, then the majority might start taking a greater interest in what a fiat currency is. Then there would be massive cries for a complete change to the system. I seriously doubt that day will ever come.

Well said.

Real people and real markets rely on real information, and sadly those days are long gone. When the majority start to realise that printing money devalues their savings, and their income, that will be one thing, soon after, they start to realise that their assets, ie, their houses, are being devalued in the same way, then the majority might start taking a greater interest in what a fiat currency is. Then there would be massive cries for a complete change to the system. I seriously doubt that day will ever come.

Not so sure about this. I think there is a lot of talk and discussion about the nature of money, just not delivered through the mainstream media.

So what is the government's list of businesses the government should bail out if they look like they're going to go under? Shoe shops? Kids need shoes. Clothing shops? We need clothes to keep warm. Cafes and restaurants? Insurance companies? Pharmacies? Where does it end?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.