Reserve Bank (RBNZ) Deputy Governor Geoff Bascand doesn’t want there to be an abrupt end to the six-month mortgage repayment deferrals banks have been offering their customers since the end of March.

Speaking at an event hosted by Kiwibank on Friday, he said the RBNZ was looking at how it could enable banks to transition away from the temporary relief provided to borrowers under financial pressure due to Covid-19.

The RBNZ a couple of weeks ago told interest.co.nz, “An extension is one of the options under consideration, but not the only alternative.”

It wouldn’t detail what these alternatives were.

Bascand said the RBNZ would make an announcement within the next 10 days.

He pointed out it was ultimately a bank’s decision whether it enabled a customer to defer the principle and interest repayments on their mortgage.

But what the RBNZ could do, was treat these loans as performing, rather than impaired. Impaired loans require banks to have more capital held against them.

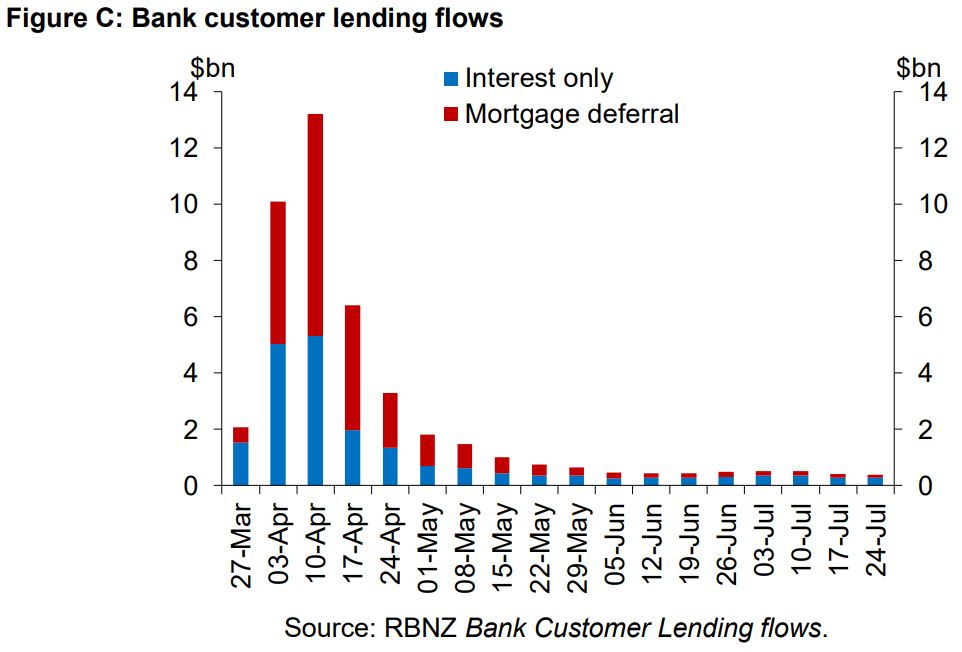

Bascand said $20.6 billion of residential mortgages are currently deferring principal and interest payments, and a further $18.3 billion of mortgages have moved to ‘interest only’. This represents 14% of the banking sector’s mortgage book.

Now’s the time for banks to draw on their capital buffers

Bascand repeatedly urged banks to keep lending, saying, the sector was at the “end of the beginning” in terms of its response to the Covid-19 crisis.

“Now is the time for banks to prudently drawdown on their buffers to support their customers,” he said.

“Shareholders will have to be patient for longer-term payoffs.”

Bascand recognised demand from businesses for credit for capital spending had fallen.

However, he also said there was some indication banks were being more cautious with their lending - beyond higher risk sectors like commercial property and dairy.

“Given banks are anticipating a deterioration of their loan portfolios, hunkering down and tightening lending standards may seem to them to be the optimal response to perceived increased risk,” Bascand said.

“However, given banks’ dominant role in New Zealand’s financial system a synchronised lending contraction across the banking sector would risk a ‘credit crunch’ amplifying the economic downturn.

“Therefore ultimately it is in banks’ own interest to maintain the flow of credit and contribute to the long-term stability of the banking system by preventing large scale borrower defaults and disorderly corrections in asset markets.”

‘Aspects’ of bank capital rules should definitely be implemented from 2021

Bascand said it remained the RBNZ’s plan to start requiring banks to make the seven-year transition to meet more stringent capital requirements on July 1, 2021.

The RBNZ in March deferred the start date of these new standards by a year to ensure it didn’t deter banks from lending.

Asked whether the RBNZ would seek to defer the start date even further due to Covid-19, Bascand said the RBNZ hadn’t made a decision yet, but would have something to say on the matter in October or November.

“I think there are aspect of it that we would definitely want to get in,” he said.

“The review had a multitude of elements of reform. The most headline one was the minimum level of capital. Everyone in a sense is focussed on that. But there are lots of elements of structural parts to our capital regime underneath that as well.”

Shareholders should expect lower returns

Bascand acknowledged low interest rates were likely to be an “enduring challenge” for banks.

“In the short-term, low interest rates can be beneficial to banks by reducing funding costs, increasing asset prices and lowering default risk,” he said.

“However, a prolonged period of low interest rates could pose significant challenges to banks’ business models and profitability.”

Bascand said banks needed to “anticipate” and “manage” this.

Coupled with the reality that banks face more competition from financial technology firms in the future, with the proliferation of open banking, Bascand stressed bank shareholders should expect lower returns than they have “historically enjoyed”.

He didn’t say when the RBNZ would lift the ban it put in place in April, restricting all locally-incorporated banks from paying dividends on ordinary shares and preventing them from redeeming bond issues until “the economic outlook has sufficiently recovered”.

See Bascand’s speech notes here.

153 Comments

There is a tidal wave of buyers waiting for the mortgage holidays to end.

How many people are actually still on deferrals?

A truly massive 7% I think I heard other day

Is that of all the people who took up a deferment or 7% of borrowers on the books? The latter is a terrifying prospect.

Also: how many who took it really needed it and/or still need it, as opposed to thought that they might. Very hard to know until it actually ends.

Total value under Deferral and Interest Only due to C19 is around 15% of lending (Borrowers on books), roughly half and half across these. Total balance is around $50 billion, comparable to the entire mortgage book of one of the big banks.

Do u have an rnbz reference to this?

14-15% there was an article on it this week - with a measely 19 comments.

79000

The problem with statements like this is the lack of numbers. How big is that tidal wave? At what price point?

And how many will still be keen when the wage subsidy is gone as well.

Where will that tidal wave of buyers do now, most are sick and tired of paying rent to rentiers and KS balances have recovered. Big weekend of open homes this week I think

Probably generally true. Not me though - regarding renting, I'm in it for the long haul :)

Likewise, more than happy to bide my time and watch this play out whilst paying someone's meagre 2% gross yield.

Really rob, if you're not in a position to buy that's one thing but if you are then that's crazy. An animal would not rent its lodging, why should people? I think longterm responsible tenants are a landlords dream and you seem like a decent person.

The market I would be in (AKL) is just too scary. I am a good tenant - have been in current place for years and suits me and I'm sure the landlord, as you say. I could buy but as I mentioned a week ago or so I'm burned out on it all and don't have that kind of courage. I enjoy this site and the comments are excellent - lots of knowledge out there - but I won't be buying property. "I'm just sitting here watching the wheels go 'round and 'round...".

It might be a cold retirement "in a bedsit eating cat food" was how someone recently put it

I'll drop some of the good dog food into you for Christmas HW.

I dont need handouts whatsoever in fact I am lucky having food on the hoof ready for xmas bbq. There will be many disappointed politicians who will need the help. Cheers

It's even worse for me - I'm vegetarian

Vegan here and also FHB still waiting it out. Maybe we can flat together in our retirement. Under a bridge?

Good for you, but No, we would end up competing for grazing.

Wise decision, Rob. The market now is pretty risky, especially when you see government and RBNZ have been injecting so much money into this and encourage more first home buyers to get themselves into more debts, you will know it won't end well one day. If you are renting, you have the freedom to move your money around or choose another region to buy. Although the deposit rate is low, the inflation rate is also low. You wont lose much value of your money. But if you buy it high, you get yourself tied into your mortgage for a long time. Remember, the money you've earned and saved is still yours. But the house you bought with bank's money is not entirely yours until you pay off your mortgage.

Hi Rob, loads of people on here, including houseworks, gave me a hard time because I rented for 3 years despite having the means to buy. In the end I managed to find my dream property/reno project, under the RV and without having to engage in a nasty tender or auction process and getting sucked into FOMO. I took my time and made the best decision for my family. Cold rational decisions on big spends are usually wise. My other investments gave a good return and more than covered the money spent on rent when matched to the inflation over the same time of the house I purchased.

Excellent - glad that worked out so well for you and family!

Ginger

Great to hear.

I note you comment "I . . . made the best decision for my family. "

While there are economic factors to consider, the key things to buying a home - as compared to a house as an investment property - is the intrinsic value and both the social and financial securities that go with it.

I trust that you and your family are appreciating having your home and I think that whatever fluctuations there may be in the housing market they are irrelevant provided you are are able to service the mortgage.

Congratulations of laying the foundations for a both good family and secure financial future.

If it's warm enough, dry enough, secure enough and you can afford it then agreed.

Unfortunately there are plenty of people out there who are 100% resigned to renting because that is the best decision they can make for their families, despite 20 or 30 years ago someone in a similar position to them being able to attain home ownership. For what reason?

I was already financially secure before I bought the house. The best thing for my family would not have been getting woefully indebted but thankfully we managed to avoid that. Having lived through many housing busts, thankfully, I know that there is a good and a bad time to buy. I agree that home ownership affords an intangible value but not at any price. Having had many friends trapped in negative equity and/or bankrupted after bubbles burst, I can also say that sometimes home ownership can lead to previously intangible misery. Normal market, normal buying conditions, healthy LVR? Sure. Fill your boots. Bubble prices and a massive incoming global recession? Maybe an occasion to take pause.

Hi Rob,

Unfortunately, while the wheels go 'round and 'round, the prices go up and up.

I wish I'd got in the market when I was a young guy.....

At least others can now learn from my misguided hesitancy to buy a house. Upon reflection, I was very unwise - should have bit the bullet and got into my own home years ago.

Terminal renting is a fools' game. And there are quite a few old fools who come here to graze each day.

TTP

We know lots of lovely boomers in what should be their golden years renting tiny flats. Even with savings in the bank a tiny flat in the regions is all they can afford as they still want something they can hand to their kids/grandkids

Unfortunately that old myth of "leaving something for the kids" has indeed resulted in less than desirable outcomes for some. If they'd gone and purchased a decent home they would be in better living conditions and probably have something far more significant to leave the kids. My partner's parents are the same, good bank balance but won't travel or spend the kids inheritance, despite none of them needing the inheritance by a long shot

Come on somebody’s got to be renters for the system to work.

Pleased you find this site helpful. Maybe you would be better off being yourself an investment property outside of Auckland so you are on the property ladder.

Yes, an option. I've used a few ladders - they go up, and down too. I'm with cmat on this - it's not worth the risk for me - RE has becomes a game for people braver than me.

Yes, an option. I've used a few ladders - they go up, and down too. I'm with cmat on this - it's not worth the risk for me - RE has becomes a game for people braver than me.

You would have been far better off in Bitcoin over the past 10 years than buying NZ houses. Dollar cost averaging on a monthly basis for past 10 years would have returned approx 27,000%. Even in the past 5 years, you would have 7x'd.

*

*= past returns are not necessarily indicative of future performance

This applies to all investments. Residential property included.

Couldn't agree more.

27000 percent... Yeah sure mate

You would be a gazillionaire if only you'd taken your own advice.

It wasn't advice. It's just the reality.

Spoken with the clear advantage of hindsight. I take it you didn't take your own advice 10 yrs ago. Also until relatively recently BC was trending down. The experience of Cryptopia should be enough to make people very very wary.

You really think that the best thing for a person with a spare 150k(or thereabouts) to do right now is to buy a rental property in the regions?

It's a better return vs risk profile than most other investments. Might need a bit more than 150K to freehold one though

An animal just takes their lodging, I'm all for that if thats what you're suggesting.

Like a cuckoo steals the nest which another worked hard to build. A few humans are cuckoo lol but we are taught not to steal.

Spoiler alert: humans are an animal

Yep. Big weekend for Open Homes.

Anecdote:

Friends of Mrs W's who have been small-time property investors since the late 70's. They have a small unit block of 4 flats and 3 other stand-alones, the last of which they bought just before Christmas - 'before the upswing comes!'

Guess what? They have the whole lot on the market this weekend.

Interesting times are here!

If the friends of Mrs. W have been property investors since the late 1970s, then I assume that they must have started in their late 20s, meaning that they would be in their late 60s today.

I guess they are retiring and think that now is a good time to cash out.

But they weren't retiring before Christmas? It just occurred to them in the last eight months you reckon?

Great name.

And it's time to go To The Pint.

Maybe they saw the certainty of another 3 yrs of Landlord bashing and decided they'd had enough of the BS

bw himself is a seasoned investor from way way back, dont let him fool you with his cynical comments

True hard to stop housing and share price from going up as seem unstopable.

@Due Diligence , I hope that "tidal wave of buyers" are buying a home to live in , and more importantly have secure incomes .

Right now , no one else should be speculating in the housing market

Will not happen soon as more free money on the way to boost share and housing market.

Now ecenomy will go to next level below and share and house price will go to next level - up.. More disparity between real gloom ecenomy and asset boom prices.

" what the RBNZ could do, was treat these loans as performing, rather than impaired."

What's the word I'm searching for? Perhaps legerdemain. And just as in 'The Prestige', eventually, everyone sees through the trick and realises the bird was dead all along.

You are on the money bw.

This statement acknowledges the inadequacy of moneyless, central bank QE actions and zero bound interest rates.

In all seriousness, what would you do differently?

"Extend and Pretend" is the American term.

" what the RBNZ could do, was treat these loans as performing, rather than impaired."

A little different, but after the bubble burst, it took about 10 years for Japanese companies and commercial banks to move to 'mark to market' (https://www.wsj.com/articles/SB1001877901777968560)

Different I know, but the behavior and attitudes are similar: They know it's all bad and don't want to face the reality.

Capitalism no longer exists.

The residential housing market defines the NZ economy and the RBNZ want to protect it at all costs from market forces.

Central banking is the biggest kink in the hose that is capitalism.

Central banking is the biggest kink in the hose that is capitalism.

They're simply a lead player in the complex that involves the govt, commercial banks, and the legal system.

"They're simply a lead player in the complex that involves the govt, commercial banks, and the legal system."

And the "elite insiders"

Precisely.

How many of us are now past caring?

Those in charge, like our RBNZ, have no idea what they have constructed for us and still think they can 'rescue' what's left of the capitalist system with more cheating, lies and deceit.

Even worse. They knew what they were doing all along and decided that 'something' might come along to help. But, frankly, I doubt that they are that clever. Because the really clever operatives don't work for Central Banks. Central Banks are run by those who weren't good enough to make it in the big, outside World.

But, frankly, I doubt that they are that clever. Because the really clever operatives don't work for Central Banks. Central Banks are run by those who weren't good enough to make it in the big, outside World.

Most of them never worked outside academia and the institutional framework in which they currently sit. They're proponents of the prevailing dogma. You can't go against the system and hope to progress in the central bank paradigm.

Which is part of the problem. Central banks should be run by the best and brightest but the institution doesn't offer the wages to attract that demographic. It's not even a high status job because everyone hates the central banks and thinks they are a bunch of incompetent twats with a limited range of options.

I don't think they are incompetent. They know exactly what they are doing. They are morally bankrupt and corrupt. But reasonably competent at it.

A recent example being a new role advertised for an RBNZ head of money and cash position- where did the job go - to a 20year employee of the RBNZ. No new thinking allowed here thanks!

I can't help but think of Paul Keating's quotation about Banana Republics. Substitute Australia for New Zealand.

Keating said, in 1986:

We took the view in the 1970s – it’s the old cargo cult mentality of Australia that she’ll be right. This is the lucky country, we can dig up another mound of rock and someone will buy it from us, or we can sell a bit of wheat and bit of wool and we will just sort of muddle through … In the 1970s … we became a third world economy selling raw materials and food and we let the sophisticated industrial side fall apart … If in the final analysis Australia is so undisciplined, so disinterested in its salvation and its economic well being, that it doesn’t deal with these fundamental problems … … Then you are gone. You are a banana republic.

He was warning against the dangers of relying on mining and primary product for our export earnings. In the event, it was the excesses of the 1980s that brought the economy undone.

The recession of 1990 followed the stock market collapse of October 1987 and was caused by international recession and high interest rates. By 1992, unemployment in Australia reached 11 per cent. The standard variable mortgage interest rate was 17 per cent.

"treat these loans as performing"

War is peace

Freedom is slavery

Ignorance is strength

The last one is super applicable in this instance.

Cue the Benny Hill music.

They dropped interest rates and people capitalised it into the values of houses and land. Now people living in poor parts of town are facing 20k plus rentals with no real increase in take home pay, it's a disaster from any angle except those that own houses subsidised by the accommodation supplement.

The makings of the next financial crisis are now apparent, the RBNZ is letting us down badly with its encouragement of reckless lending.

RBNZ needs to revoke this biased capital incentive to lend to those seeking to speculate in the residential property market rather than productive GDP qualifying business ventures.

{kind=link}

^^this

End of the long debt cycle Audaxes (in Ray Dalio's speak). When people are using leverage to gamble on asset price appreciation, then its a one way street to eventual defaults/deleveraging. How else do you reverse the trend?

Never going to happen.

Money printer goes brrrrrrrrr.

It can and will happen.

RBNZ & Govt is trying to prop up the economy from the huge impact on Tourism, Intl students & immigration, not to mention all the other impacted industries from the deepening world wide recession. It can do it for a while but we are going to be impacted for years. If QE and fiscal spending gets too high and we crash our currency, it always end in austerity via standard of living, increased taxes and the hidden tax of inflation to inflate away the debt.

This is a marathon not a sprint, pulling out all the stops to keep everything afloat now is probably not the wisest thing. Spend wisely and targeted!!!

The best way for the mortgage holidays is to offer them onto 1/2 interest only for 3 months and then to interest only after that. Those that can survive 1/2 interest only would be best to make the difficult decision and exit and sit on the sidelines until their situation improves

There is the best way of doing things and there is what actually happens.

The money printer can and will always be made to print faster. Brrrrrrrrrrrrrrrrrrrrrrrrrrrrr.

Trying to defy gravity. Let the free market prevail. The cornerstone of freedom of the people.

There will be hundreds of Terry Serepisos in waiting before Xmas.

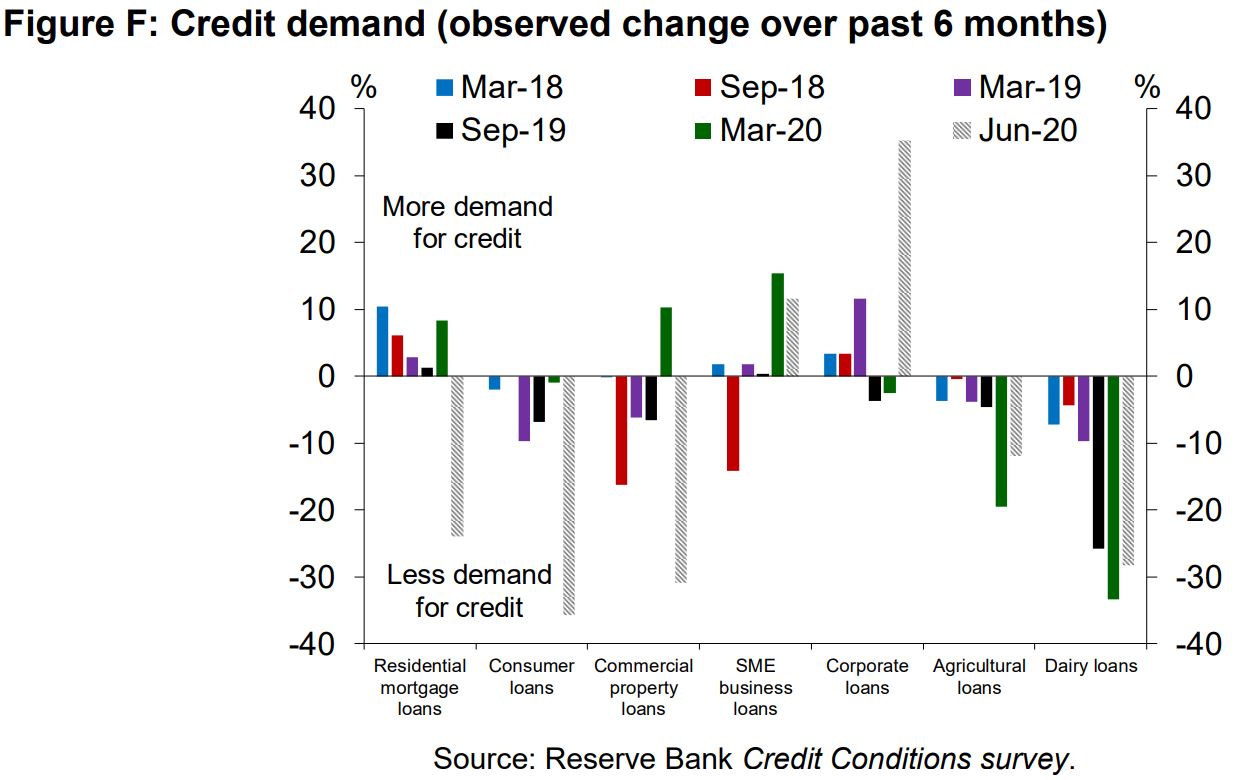

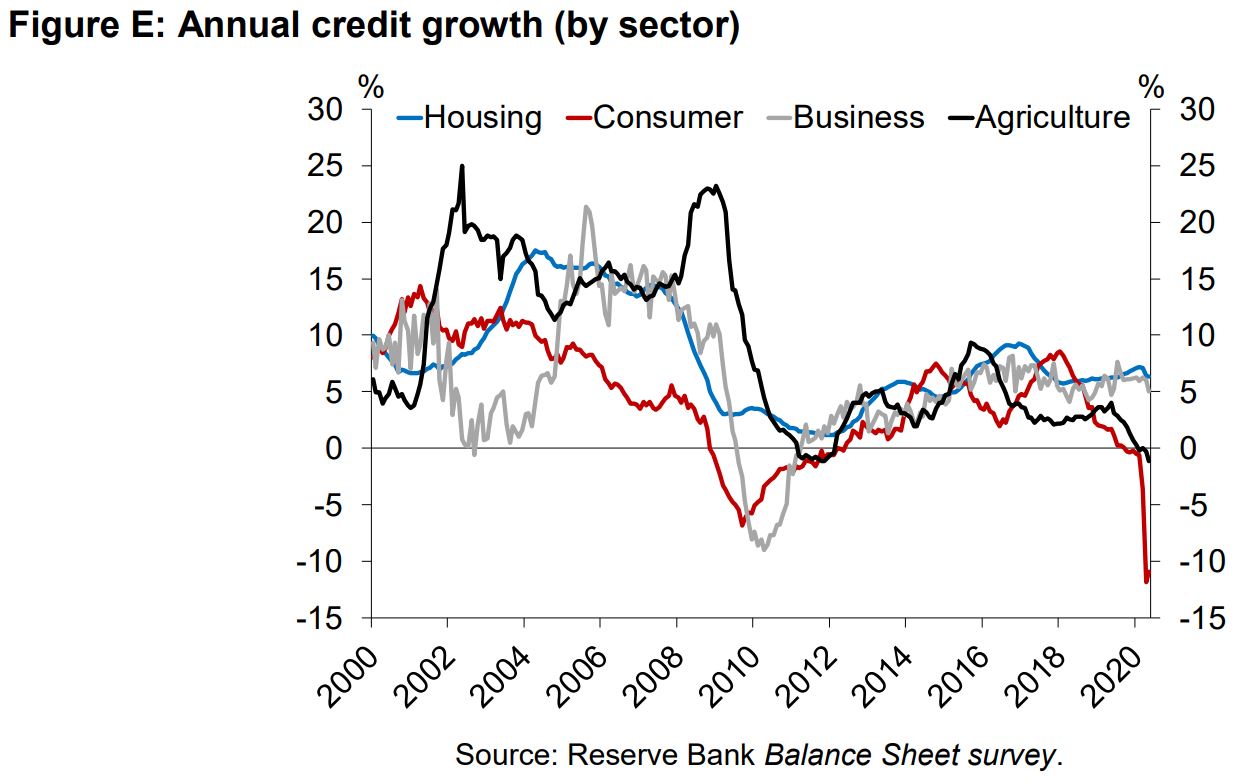

Credit demand off a cliff already.

Mortgages granted in June total was lower than a year ago.

An economy with no credit growth is ripe for serious trouble.

No wonder he wants to continue with extend and pretend.

Treating an NPL like it is not, is just like the nonsense EU been doing since 2008.

Do you think it's because our credit growth (approx $20b a year) helps fund the profits of multinational corporates? I.e. $5b to the banks and $15b to various other multinationals? They're convenient numbers.....

I know 3 friends who are stuffed with no job and a mortgage. One is on the market, the other 2 are putting onto the market. Tough times ahead.

Glad I am mortgage free since 2018.

What industry are they in if you don’t mind me asking?

I don't understand how people get into this situation.

Surely you would borrow a hundred grand more than you actually need and keep that in an offset account for a year or two worth of payment buffer for rainy days?

Isn't that the rational thing to do?

How would you do that? I didn't think a bank would lend you more than the value of the house minus the deposit...is that not right?

That's a good point I guess I don't frame the issue with just scraping together the bare minimum deposit because that's not my personal circumstances.

Regardless you should not over-borrow and immediately start working towards having at least a year worth of buffer for when the SHTF.

All the statistics ever collated show that the vast majority of people don't have a rainy day fund. Let alone a years buffer plus a housing asset. The NZ average debt to household income ratio is what 163%.

So many claimed that the last decade or so was stellar economic performance and policy...yet we saw bare minimum GDP growth built on the back of soaring household debt (the foundation of the "wealth effect"). What growth without that massive debt increase? Certainly not a lot of growth in productivity, one of the core reasons many of us voted for Key in the first place.

Whilst that is a good rule to follow Brock, the reality is most buyers can barely scrape the minimum together, start a family too soon and thus find themselves with little to no free disposable income with which to build a buffer. Why do you think raiding KS is so popular for FHBs now

Because the average FHB can't even scrape up a 20% deposit, let alone borrowing more than the purchase price. It's estimated that 60-70% of FHB actually need family assistance just to get the banks to lend them the purchase price, let alone anything beyond that.

The drop in credit demand says it all.

But not quite.

RE NZ for Auckland City shows its listings are 23.8% higher than a year ago, compared to Auckland overall which is at - 1.5%. Only AC and NSC are up. Half of what is on sale in AC is priced over $1.4m = no mortgage needed.

No wonder Auckland sales in bracket 600-850 are off 41% in last 4m, compared to 2019.

By the way, to hit the same total sales as 2019 for May, June and July, then July will have to be up 39% at 2776.

Somehow, I do not think so.

Just like the economy, when activity (as now) reaches same level as last June, this is not a recovery. That neglects the hole you just climbed out of, ie about 9% GDP drop n last quarter, if USA is anything to go by.

In housing terms, that means sales have to make up for the deficit caused by lockdown. Nowhere near that yet, despite all ho hah form the industry high priests and bank hanger ons.

Apparently the US economy has contracted by an annualised rate of nearly a third (32.9%) between April and June - the worst contraction since the Great Depression of the 1930s. Since they're still knee deep in Covid-19 with an inept president who is trying to distract the voting public by trying to delay their election. Hopefully we're not in the same boat, seems the top end of the AKL property market is still thriving (Still wonder where they get the money from). BBC Republicans to Trump: You can't delay 2020 election https://www.bbc.com/news/world-us-canada-53599363

Okay. So the US GDP shrank by around 9% in the secod quarter. It would be the height of foolishness to multiply that (probably one-off drop) by a factor of 4 and rename it as an "annualized rate."

Annualizing one-time events is highly misleading to the point of being fraudulant.

Having said that, the Q3 US figures could still be negative, but far less so than the Q2 figure.

You Trump supporters can try to put a big pink bow on things but that doesn't change the facts: The US GDP shrank at an annual rate of 32.9 percent, according to the Bureau of Economic Analysis, the agency that publishes the statistics on quarterly economic activity. Not to mention that the US unemployment figures are still surging, the number of people collecting jobless benefits also increased to 17 million, up from 16.2 million the week prior. Next you'll be supporting Trump on postponing the November election which he's currently trying to do.

US News: Unemployment Claims Rise for Second Consecutive Week. https://www.usnews.com/news/economy/articles/2020-07-30/unemployment-cl…

Doublespeak: a bank's assets are in FACT its loans.

Deposits would be the actual assets, ie to normal folk, what they have in hand - except they don't as they lend it out leveraged. This rubbish re "assets" is as bad as mental "health for illness, challenging for hard and credit for debit. Language distortion of course has a purpose and it is not to make anything clear.

Good one MK29. When the typical NZer hears 'bank assets', they're probably thinking of bank deposits. You know, the 'liabilities'.

it is not a credit crisis, until it is.

And it is a self fulfilling prophecy as banks ALWAYS make recession worse by tightening lending standards.

Of course Aussie banks made how much profit last year????

I gained preapproval back in Feb. I’ve been taking my time house hunting, I’m in no great rush and feel there are incentives to buying later rather than sooner.

Anyway, I’ve renewed my preapproval twice since Feb with no issue and very few questions asked. My preapproval was up for renewal again on 21 July. I emailed the banker who I’d been dealing with up until now. I updated him on my strengthening financial position and that my deposit had increased 10% on what it was when I first gained preapproval. I updated him on my debts (student loan and car loan) when I’d continued paying off and reduced these by 10% also.

The banker took longer than usual to reply to my email. When he eventually did respond he explained there had been ‘changes in their policy that now require a certain overlay for the affordability’. He provided an estimated amount for my preapproval that was lower than had been extended in the past 6 month. He said this quote was provisional as he is now required to consult with the credit team who will finalise the preapproval.

It doesn’t really affect me as I was never looking to max out my credit to begin with and the preapproval still exceeds the price range I’m looking in by a large margin. I did however find it interesting that despite a 10% greater deposit and reduced debts, My preapproved amount decreased and there was a more stringent process this time round.

Take from that what you will. The bank is ANZ for those of you wondering.

Thanks for that info - I'm an a similar position with the same bank, so your story is really useful for me - I better double check my limit before I make any offers!

VofOCR

This illustrates what I have been posting; banks are tightening up on criteria regarding their lending.

Although RBNZ have removed LVRs, banks are protecting themselves and not lending with gay abound.

This is about protecting their vested interests; however it also should give some assurance to borrowers that in protecting themselves, they consider that the lending/borrowing is not being reckless.

It appears that in a number of instances FHB are now not meeting bank criteria - more so than investors are although not currently very active.

Sorry, thumb hit the report button by accident.

Yep. I’ve half expected this to happen. It’s why I’ve kept my preapproval rolling over - thinking it’d be easier to maintain preapproval than get re-preapproved. Seems my plan didn’t quite work out but so far it’s not impacting my house shopping. If they tighten again though it might become limiting.

You do realise the banks have reassessed their risk exposure. I find it interesting that you have a car loan, a student loan and a deposit you're increasing, doesn't speak to much financial literacy. also any credit cards you have are considered debt liabilities up to your credit limit not just what you currently owe. If I were you I'd clear the car loan first, close your credit cards and use Eftpos only and work on reducing that Student loan. You'll find your bank will be more favourable as a result

Get rid of the car loan if you can. Credit cards and vehicle loans are red flags unfortunately.

The banks are facing the prisoner's dilemma. They are self-interested to reduce risky lending, but the RBNZ is telling them to "cooperate"...

It underscores how negatively banks see things at present.

It was only 2-3 years ago that RBNZ was the one trying to pump the brakes on the banks and reduce the amount of lending happening with the introduction of LVR rules for residential property, and the requirement to hold extra capital against rural lending which increased interest rates.

Can we sack the lot of these central w*nkers? Bascand is the biggest brain we've supposedly got, and all he can think of is making the banks pump more loans into the economy to prop up incumbent asset prices. Do these guys even understand finance and efficient allocation of capital?

Of course they understand it, they aren't stupid - just cowardly. After a decade or more of digging their hole deeper and deeper, there are only two options left to them: keep digging and hope it doesn't blow up before they retire, or stop digging and it blows up on them. We are too deep now, they can't tighten credit, can't raise interest rates, can't even report on impairments now or they are hosed.

Of course they understand it, they aren't stupid - just cowardly. After a decade or more of digging their hole deeper and deeper, there are only two options left to them: keep digging and hope it doesn't blow up before they retire, or stop digging and it blows up on them. We are too deep now, they can't tighten credit, can't raise interest rates, can't even report on impairments now or they are hosed.

Well said. Stuck between a rock and a hard place sounds too nice. They played their part so they will get what they deserve (kind of).

It's more that they are desperate than stupid IMO. The best hope and biggest gun in the arsenal they have right now is monetising and deflating down the debt ie keeping everyone drinking from the punch bowl. They are trying to create inflation. They are printing. They want to deflate the currency, of course they do. Weaker currency means a potentially healthier trade balance, happy exporters, a little light inflation to reduce the debt burden of both indebted households and government... plus maybe even some wealth effect but please God anything but the dreaded deflation. RBNZ will do everything they can to deflate the NZD and create inflation IMO. They will hope to contain the inflation of course, but they think that containing the inflation is more manageable and viable than breaking a deflationary cycle. All the central banks clearly hoped they had more time to normalise before the next economic shock came but 2020 decided to be a bag of d%$ks instead so here we are.

They are stealing from those who work and save and handing it to those who those who overleverage and speculate. Financial repression. Because the bubble they cultivated is too big to fail.

I wonder if Orr and Bascand would care to disclose their personal stakes in the property market in the interests of full transparency.

If they print and deflate the currency, yes they will savage bonds holders and savers. But those are the group that are always savaged at this stage in the debt cycle when the majority of everyone and everything else is over leveraged. The savers have lost wealth but they have remained solvent, which is probably perceived as an acceptable, collateral damage compared to the mass insolvency of the indebted households, businesses (followed by nations potentially) . It ancient times they had debt jubilees, they recognised that debt eventually reached a point that it could never be repaid. At least that was honest.

How much of it is genuine need for mortgage holidays, and how much is just people thinking they are getting a free break from paying their mortgage?

Judging by a lot of comments on social media about the topic, I would guess a lot of people have no understanding of how a mortgage holiday actually works and don’t realise that the interest is still accumulating quietly in the background.

A great Q to ask, and totally agree.

That a 'lot of people' have no understanding + relative silence on this from govt / banks (knowing what they know) -> actually morally wrong.

Farmer

You are correct that there were some who wanted to have total deferment or interest only for additional cash flow during these uncertain times. However, my understanding was that banks acted as gatekeepers and if there was no need for the facility then the application was declined or at least discouraged.

You are correct that there were many - even on this site - who misunderstood what a "mortgage holiday" was, despite it being a facility that banks have had in place for considerable time. Some initially thought not only that it meant there was no interest accruing, and some even thought it meant that the government was paying their mortgage for them. The latter - renters - were spitting hot tacks.

You've got a bit of a gripe with renters aye? What gives?

A bit of convenient forgetfulness there printer8, likely pointed at me. The first statement from the government suggested the bank would be supporting banks, by enabling them to offload the risk of mortgage holidays to the bank. The risk part being a core part of calculations on mortgage affordability. As risk ramped up, it sounded like the government essentially gave them a free pass to keep lending and approve as many loan holidays, as the government would back stop it. The details would be worked out in a few days after discussions with banks.

GR obviously had a change of heart and the banks couldn't figure out how that would work. So they just used their own loan holiday schemes already in place, likely with government assurance that they would work something out down the track.

And now we know what - by not recording non-performing loans as non-performing (madness), they are picking up the tab at the other end by wallpapering over the cracks in the concrete, so that banks aren't hit with big bills. The recognition of non-performing loans are there for a reason, to suggest ignoring them is amplifying the risks to the financial system. If it all goes tits up, it will lead to bank bail outs later - i.e. the government bailing out all and sundry.

I will definitely say that it wasn't "free money" as it previously sounded like it was. Interest and principal payments certainly keep increasing. In fact, I know of two couples who are on this now. However, you should acknowledge that these announcements are sounding very much like "extend and pretend forever", to try and stop anyone from foreclosing. And the two couples that I know are on LRH's - both are now working as they were before. One of them is saving the money saved on mortgages for future payments in an unsure economy (see the increase in bank deposits reported today). The other just bought a new motorbike with the money saved from not having to pay their mortgage. Like I said, a distortion that will be near impossible to remove.

I think you might want to have a chat with those two couples blobbles. They are both obviously in serious need of some guidance - maybe just a good swift slap on the back of the cranium because that's what they both richly deserve. The one with the motorbike actually deserves several slaps

So many elephants in the room on an 'official' level - which many of us here can see, unaided.

a) Consumer credit growth slide -> underscores that you and I are beginning to 'get' it about credit - while govts (incl RBNZ, BoE etc) + banks follow each other aimlessly, endorsing credit, as if money grows on trees!

The idea that doing something is better than to be seen to be doing nothing. SO lacking in integrity and leadership.

b) That June explosion in corporate loans.

c) Talking about implementing 'aspects' of bank capital rules -> arguably obfuscates the reality of lack of direction (aka emperor's new clothes)!

Allowing a bank to inaccurately record impaired loans as "performing" should depress their share prices significantly, who wants to hold shares in something that you know for a fact is cooking the books on you? That in turn should reduce their CET1 value, meaning the capital they are holding against these loans is worth less. So by doing this, banks might end up having to raise more capital or lend less anyway.

Good point. Circa 2007/8 redux. No one knew which banks were exposed to toxic assets so no one risked exposure to anyone else. Hiding toxic assets didn't work in the GFC why would it work now?

How to support and inflate asset class come what may seems to be only priority of fed and governments.

sooo... if I was considering selling early next year, I'd take the holiday, then reap the massive capital gains at the back end of it... save money now, make lots more money later when I sell to the Californians... win win!

if I was considering selling early next year, I'd take the holiday, then reap the massive capital gains at the back end of it... save money now, make lots more money later when I sell to the Californians

This seems like an eternal NZ fantasy that has swung from the buyers of China to the West Coast of the U.S. swamping the suburbs of NZ willing to hand over a king's ransom for a bolthole.

Ah, but the Californians are on their way... they are opinionated, loud and they are political. You will soon see them at all levels of governance, from your local PTA to the higher echelons of the Beehive. They will be bringing their “...dreaming” to the antipodes and will be righting all our ‘wrongs’ with their vision of utopia...

Pretty flawed logic there HubHub and a BIG assumption on the capital gains, "massive" or otherwise

Please enjoy 4 minutes of train smashes while considering what we've done to our banking system and the residential property market. Observe that when something is very big and it has a lot of momentum, its impossible to stop in time to prevent significant damage - neither the train driver nor its victim have any control over the outcome as you can't control that amount of momentum. Also note that RBNZ decided to remove all safety systems related to our 'train', including LVR's recently, so that young people can freely play on the tracks without protection.

Funny. Is the RBNZ the train or the truck, I wonder?

I'm sorry I just love metaphors and have to do this:

The truck is the real economy

The train (about 8 times bigger) is a massive load of fiat currency loaded onto every financial asset you can imagine

The train driver is the central bank (could be any of them)

The truck driver is sitting tight, planning to grab some of the currency as it flies into the air

Thanks for the nightmares.

At least the stretch limo got it - no tears there.

There are just metaphors everywhere here - every crash was a bit different.

I quite like the one that starts at 2.12. Just when it seems like "OK - just a freight truck derailment", breaks finally grab, then WHAM!!

Ugh.

Is there any other country out there with a Reserve Bank that thinks like ours?

Pretty much all of them!

"But what the RBNZ could do, was treat these loans as performing, rather than impaired".

So the message is to treat the loans in a way that they are not in actual reality!!! Continue withe the housing Ponzi game?

An amplification of the earlier exhortation by RBNZ for banks to be "forgiving".

By logical extension, courts should be "forgiving" to those who ran foul of the law.

And supermarkets should be "forgiving" to shoppers unable to pay for groceries at the till.

What a wonderful thing indeed to be lauded the world over for NZ to be known as a Nation of Forgivers!!!

As for me?? Hmmm. If my bank is going to be so charitably-inclined as to how they handle my monies, then I am persuaded to park my terms deposits elsewhere.

OBR crept up a bit closer. Which bank though?

Rbnz today showing deposits rose $22billion from Feb to April. Then dropped $10 billion in next 2 months. Up front wage subsidies replaced lending. Net increase in demand hence nil. Other $10 billion been tucked away. Bounce over

ASB won't let you execute a purchase for ASX PMGOLD through their online share trading platform. I wonder why?

Wow really.

The Fed is instructing central banks around the world to drive the banks under so they can issue their own digital currency and take over the system. Freedom gone hmm..

A bunch of nations have been looking at introducing their own digital currencies (which would really make it electronic money, not virtual currency) - not just driven by the FED.

But regardless of semantics, the big question I have is will the jurisdictions that issue these new digital currencies retain the ability to just make more of them at a whim. If so, we are back to money printer go brrrrrrr....no real change, probably presented as a New World Order.

Backed by the printing machine of reserve bank. 15% property discount still possible?

At what point do the conversations turn to, "dear valued customer, your mortgage holiday ended in Sep, you have now missed the last x months payments... we need to talk about, gulp, err, umm, selling your house"

Do banks excuse payments up to a certain equity point? Or is it a payment frequency loss trigger? Many people may have had a 100% increase in house value and therefore have low LTV. My guess is it's probably a 3 to possibly 6 month period before it turns ugly, and would therefore not really impact those with job losses until early next year. Can anyone with actual understanding of the process explain?

What do you mean "Can anyone with actual understanding of the process explain?"

We're all guessing what is going to happen mate. That includes the government, RBNZ and the commercial banks.

I'm referring to the specific process of banks enforcing a mortgagee sale. Obviously that's a last resort, but there must be some reasonably generic criteria they follow (ie missed x payments, time to put it on the market)). Not something banks will wan't to do as they'll encourage the prices to go down and further increase their risk.

Wow, its like the Banks are dictating what the RBNZ should/must do, and banks share holders must be looked after above all else. The super profits for the banks may have to be returned for some re capitalisation.

The banks are doing exactly what they should be doing to stay in business and shutdown their lending because its obvious what is happening in the market.

So what happens if NZ has to go into a level 4 lockdown again? Allowing house prices to rise as much a they have done IMO, has created this problem. NZ houses shouldn't be as expensive as they currently are, and that is really the problem. Buying a house often now relies on a two wage houseshold, and if businesses are cutting costs, which often means staff, who are a big cost, then many households could be down to a single income earner, or even no income earner. At least for a certain period of time. Continually lowering interest rates, to pump up house prices is going to come unstuck at some point in time IMO

Welcome to extend and pretend. As many of us have been saying, this is what has been happening over the past 10 years, via continually lowering interest rates.

Think about this though - the RBNZ performed 2 shock drops of interest rates last year and this year, to try and buoy the economy (even though businesses were saying they had no problems accessing capital) and in the expectation that it would almost fall off a cliff due to COVID19. Now, the economy has proved to be a bit more resilient and is actually doing really well. So we should expect those interest rate drops to be reversed, at least partially right?

If the answer is yes, then we have the economy the economists and bankers think we do. If the answer is no, then it's extend and pretend ad infinitum and we don't have the economy they think we do.

So by arrangement , 14% of all mortgages are not having any Capital Redemptions whatsoever.

This is not healthy , given that another ? % of borrowers are making no repayments whatsoever .

Now you may think this is all fine and dandy until you realize that banks have obligations too , they have to keep paying interest on deposits , fund their day to day operations , pay wages salaries and rent , and still pay tax on the earned and capitalized ( but unpaid ) interest income .

Subsidy should be targeted to those affected as a cushion and not universal bonus to many. Even government is aware of how many have used it to their advantage (misuse) to make a decent profit by manipulating the system supported by their chartered accountant.

As a result also the money available will run long and government should think and distribute.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.