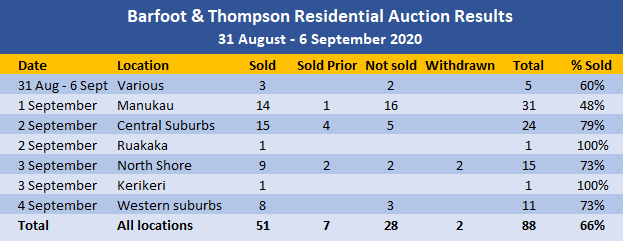

There was a slight dip in activity in Barfoot & Thompson's auction rooms in the first week of spring.

The real estate agency marketed 88 properties for sale by auction in the week from August 31 to September 6, down from 111 the previous week.

Sales were achieved on 58 of those properties giving an overall sales rate of 66%, also down slightly from the 71% sales rate the previous week, but still a robust result.

At the major auctions the highest sales rate of 79% was achieved at the central suburbs auction on September 2, where most of the properties were from suburbs including St Heliers, Remuera, Mt Eden, Glendowie, Grey Lynn and a few from south Auckland.

The lowest sales rate of 48% was achieved at the Manukau auction on September 1, where the properties were from the city's southern and eastern suburbs (see the table below).

Details of the individual properties auctioned and the results achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

27 Comments

To save me repeating it all, please see my post reply to Printer under last auction piece a few days ago (5th Sept, about 10 comments down) covering which parts of Auckland are up and which down, and why. Basically auction numbers are too small a sample.

4 bed sales and prices in upper bracket doing brilliant. Papakura, MC and apartments doing badly or worse.

Cheers Mike

111 minus 88 is 23, or a 20% drop.

is that "slight?"

Might be connected to fact that listings have dropped a fair bit in last 10 days, as has listing per day.

So, it appears Spring is not going to be as good as usual .

Not really a surprise as market goes in ebb and flow.

For a few months sales expand and then take a rest, so the reversion to mean keeps sales pa within a range of 23,500 - 24,500.

The surge is over for now. Will Spring be less than 2019? Likely.

Bear in mind when comparing that the first 5 months of 2019 were lower in sales than 2007

And if comparing October, November, Dec, sales were on rising trend in 2019 and hence comparison to 2020 will be unfavourable.

There are some real challenges in this environment getting properties to market that would likely be contributing to the lower-than-normal level of listings. E.g. the Covid-induced eviction freeze, end to 90-day evictions, dealing with tenants in the lockdown, getting tradesmen in lockdown, even trying to get a house and garden presentable with a hosepipe restriction.

I suspect the spring surge will still arrive, but maybe a bit later this year.

I reckon the spring surge -- when, and how big -- is the key. The 2019 spring surge was small and late. What will this year's be?

I reckon it must be dashed hard for REAs to obtain listings right now, especially since the market is in a crescendo phase......

Further, if you do sell your house you'll earn very little interest on a bank deposit - less than 2% (from which interest will be deducted). And, because stock is low, finding another house might take quite a while - which could be perilous.

The moral of the story is plain and simple: don't sell unless you have to do so. (But you knew that anyway.)

TTP

You got to buy it now! Once Covid is over, the flood gate will be opened, demand and prices are going to skyrocket further.

No DGM here..

There I said it!

CM ...... you should also add "prices will never be cheaper" !! ...thanks for that, best laugh all week !

Well it's official; National really does not care or give a damn about the health of the NZ people and residents. Quote from this morning Herald: Landlords 'should wait on election result' before installing heating.

"The advice comes after National under new leader Judith Collins confirmed to the Herald it would tear up new Healthy Homes standards recently brought in by the Labour-led Government."

https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=12361468

That is pretty obscene from Collins and National.

We as taxpayers should have to fund more and more in healthcare because we cannot possibly expect investors to invest only in viable assets? They should be able to rent out substandard housing and have NZ pick up the downstream effects, because it might impact their profits?

What's next? Collins to tear up food safety standards because they lower they create extra costs for restaurateurs and we could instead have taxpayers fund more services for food poisoning recovery?

They just cannot seem to stop their self-absorbed mentality of take, take, take from society.

100% Agree with you Rick. And if they're that blatant about lack of foresight, as you quite rightly pointed out in regards to NZ peoples health. How on earth would they cope with managing the Coronavirus. Since the Nats are already itching to open flood gates of our boarders in the name of 'Free Enterprise' (Free enterprise for themselves of course).

They'd be the ambulance at the bottom of the cliff party if they hadn't already sold them off as a fleet of food trucks.

Yeah, read that too, how can a party have such disregard about people's health, this behavior is highly unethical yet legal.

A Trawl through the individual sales

Most of the premium over GV is in Te Atatu South

Generally the premium over GV is less this auction compared to last weeks auction

With an interest in Ellerslie the sales that are occurring are redevelopment prospects

While they are the sale of a single dwelling, the prices paid are for conversion not a single dwelling price

8 Walpole St Ellerslie 660 sqm $1,780,000 = $2696 per sqm includes plans and consents for 3 x two level units

28 Rockfield Rd Ellerslie 551 sqm $1,200,000 = $2177 per sqm. Probable 2 unit development

Wrote last week about 18 Arthur Street which sold for $3,800,000 for 1214 sqm

20 metres from Ellerslie Panmure Highway, 50 metres to Southern motorway

25 Metres to Ellerslie village, backs onto light commercial buildings and shops

Will be high density flats

Ellerslie used to be my hood.. Rockfield Rd, my car was broken into 4 times in 8 months!

Makes me want to cry

My grandparents owned a 1200 sqm property in Robert St Ellerslie for 45 years. When they passed away, a member of the family who was executor of the estate was in a hell of a hurry to sell up and distribute the proceeds to himself and his brother and sister. Sold it in 1984 for $40,000 with 100% vendor finance for 2 years.. The property changed hands twice in the 2 years after settlement. The same executor owned his own house on 1200 sqm in Carr Rd Hillborough just around the corner from Hayr Rd. He sold up and moved to Titirangi. After marriage split-ups and divorces, its all gone

Hi Chairman Motor Moa,

Re your comment above: would that outcome be a reflection on the locality - or the personal company you keep?

TTP

Time To Pee, what do you think? Tell ya it's still safer than Ferguson St in Palmy North

2/12 Markham Place unit went for 1016000 with a CV of 860000

What does it indicate ?

So looking forward to those manic, hot weekday afternoons in the B&T Auctions Rooms in Auckland City, as I watch people throw money away for that damp. leaky, south facing Mt Roskill dump ...... I will be surrounded by all those who have been drinking the kool-aid for the last 8 or so years, prepped up by all those TV shows doing renos etc and NZ's own "The Block", foaming at the mouth to get that land and knock down the existing building and replace with quick and shoddily built townhouses.

There is an extremely strong case for financial education in high schools - at least to the point where you can see an asset is overvalued !! .......but that will never happen here, as too many "vested interests" and those clipping the ticket on the way.

But the problem is that "current values" have to be at least maintained, as because as soon as there is even of whiff of prices decreasing, the sheeple will start to panic ......and you will have more sellers than buyers.....then Economics 101 takes over...and why would you hold an investment property if there were capital losses ??? ......no doubt our regular property spruikers will chime in, with their "pearls of wisdom" :)

why would you hold an investment property if there were capital losses ???

Rental income? Large capital losses seem unlikely though.

Even small capital losses make housing as an investment not a good one for all costs associated to it in contrast to other assets.

ZS .....has it ever crossed your mind that the Western world is broke...that's why they are printing money ....even NZ is doing it.

What happens when it stops ???

Crazy Horse and b21

Experienced investors look to yield, i.e. cash flow positive. A property investment is long term (for a variety reasons) and capital gain is not realised until it is sold - and usually considered a bonus - hence prime consideration being cash flow yield.

A current net yield may be only 3 to 4% but far better than cash investments and Improved by leveraging off the mortgage at 2.5% (i.e. making 1 to 1.5% on banks money).

You also clearly don’t understand that property investment is long term; the risks of short term (next 2 to 3? years) falls are irrelevant - same property, same rent, same yield. In fact the reality is likelihood of improved yields with falling mortgage rates over the next couple of years (as indicated by RBNZ and bank economists).

So risk of fluctuations and capital losses in short term are not really relevant or of importance to investors buying now. Those who have owned investment property for some time are feeling pretty content likely having good capital gains already.

The thought of investors being hurt by short term falls are just wishful thinking by those envious of investors.

Cheers :)

What happens when the tenant can't pay the rent ?........BTW not envious at all ....been in AKL property since 1986 as both an owner and investor ...so glad to be out of it with a freehold home in AKL and now sold out of the USA market ...so have cash parked and waiting to see what happens....but building up the Bitcoin & alt. coins and watching gold & silver.....don't you property bulls realise that fiat money is going to get inflated out of existence ? ....or there will be deflation and there will be no money at all for those rents..... interesting times indeed.

Crazy Horse

Problems with tenants paying rent is always the bogey man.

However it is a risk that can be negated through care in selecting niche property and tenants. For that reason properties suitable to either young married couples tend to be good (if one loses a job it is not a major but the downside they tend to be only for two to three years before they buy their own property or with babies look to a three bedroom) or look to solo mum (have income security of DPB and tend to be long term for children's stability and schooling).

Currently here in HB there is still a severe housing shortage and - not trying to wind renters up - but MSD are desperate and accommodation supplements assisting those in need.

Loss of income is more than likely be readily met with an accommodation supplement.

I agree that there is a lot of future uncertainty, and even RBNZ and bank economists aren't crystal ball gazing or saying much beyond the next year. Personally, long term I see risk of possibly a little downside (not inconsistent with bank economists), and as there is a disjoint between house prices and incomes I see the likelihood of a long term with flat or moderate period of house prices until such time as affordability improves.

For that reason, yield is particularly important for those investors currently looking at buying. For those who have owned their properties for some years - well they are laughing as lower mortgage rates have improved yields and they will have - on paper - made good capital gains and if they propose exiting are likely to be not adversely affected by some fall. No doubt some will be considering cashing-in but currently yields will be more attractive than cash.

Bitcoin and PM are possibilities but investors I know tend to be older, more conservative and risk aversion, as well as less likely prepared to invest considerable sums in these options. In times of uncertainty PM have always been the risk aversion option.

Don't fall over with shock but today I am going to agree that certain seam of the market in Auckland is going gangbusters.

It is 4 beds with about 200m of floor area. The median sale price for this, from my analysis of REINZ website data, has risen 10% since March alone.(From $1.41m to $1.56m Which anyone has to acknowledge, is v fast acceleration. By contrast the median for 3 beds about 90-130m square has fallen from $810k to $795k since March.

Had a conversation this morning with an Agent whose listing was under contract in 3 days.So, it seems by negotiation is better than auction for right type of property. And yes it was 4 beds, 183m square with a sea view

So, clearly, in the right seam of the market, prices are jumping up.

My belief is that this is due to:

1. returning kiwis

2. Chinese buyers from HK buying via relatives

3. Safe haven land investors escaping stock markets in the greater fool phase they (were) in til yesterday.

How long will this phase of market last? Well, even Agents are guessing and my guess is until Xmas, or around 17th of December, after which the decline will commence (in price) and sales will begin to slow

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.