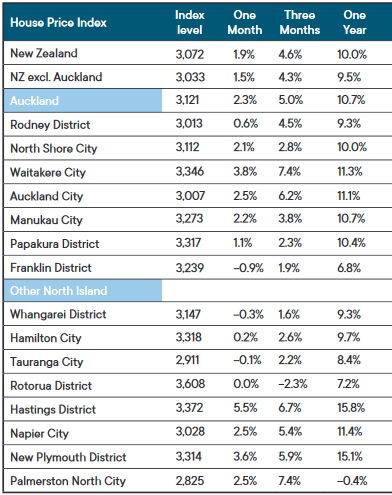

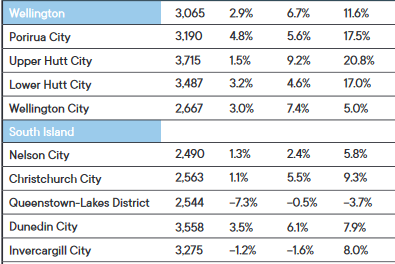

The housing market has shown remarkable resilience since the end of the Level 4 lockdown, with house prices rising 4.6% over the last three months to hit a record high.

The table below shows the movements in the Real Estate Institute of New Zealand's House Price Index (HPI) over the last year.

The HPI is considered a more reliable measurement of overall price movements than median or average prices, because it adjusts for differences in the mix of property types sold each month.

It shows that price growth has been sustained in most parts of the country over the three months to the end of August, with Rotorua, Queenstown-Lakes and Invercargill being the only cities to record price falls during that period.

It is perhaps not surprising that prices have taken a hit in Queenstown-Lakes and Rotorua because their local economies are heavily reliant on international tourism, which is still being severely impacted by COVID restrictions.

Prices in Invercargill appear to have been impacted by plans to close the Tiwai Point aluminium smelter which is a major employer in the area.

Apart from those three districts, price increases were significant and sustained across the rest of the country over the three months to the end of August.

In Auckland the HPI has increased by 5.0% over the last three months. In the rest of the country excluding Auckland the HPI was up 4.3%.

The HPI was sitting on a record high for the Auckland Region as a while in August, as well as for all of Auckland's sub-districts except Franklin in the region's south, where it declined by 0.9% from the record high set in July.

Other districts where the HPI hit a record high in August were Hamilton, Hastings, Napier, New Plymouth, Wellington Region, Porirua, Upper Hutt, Lower Hutt and Christchurch.

The price growth has been all the more impressive because it occurred over winter, when the market is normally more subdued, and against a backdrop of considerable economic uncertainty.

The comment stream on this story is now closed.

REINZ House Price Index - August 2020

102 Comments

Looks quite different to the Corelogic equivalent. Any idea what the differences in approach are?

StuckAtHome

REINZ and Core Logic data is quite different.

REINZ data is properties going unconditional in that month - that is the sale has not been completed other than it going unconditional. REINZ data is for those sold by REA only.

Core Logic data is those properties registered with the land transfer office and are over the proceeding three months. Core Logic is for all sales including private sales.

So Core Logic data is based not only on a three month period - compared to REINZ being just the previous month - they are further delayed due to the time between going unconditional, settlement and being registered which is commonly a month to two or even three months.

REINZ - although not all sales - gives a better real time indication of what is happening in the market.

CoreLogic was not intended to give a real time monthly indication - rather its basis was originally intended for RV purposes when a long term state of the market - and not that of a particular month which could be variable.

So two different sets of data for two different purposes.

Note: Auction data - while seriously limited by sample size - is the best real time indicator (note "indicator") state of the market as sales are immediately unconditional at time of auction and as reported by interest.co for that week which unlike REINZ data is likely to be conditional agreements made a number of weeks (up to three or five) prior.

Suggestion: Read auction data for an indication of the real-time market, use REINZ HPI to confirm that indication, and CoreLogic for longer term confirmation.

Hi Printer8,

That’s an excellent, informative post. Thanks!

What we can take out of it is that the DGM have been wrong by each and every measure - REINZ, Core Logic and auction data.

But getting the DGM to be accountable for their on-going botched forecasts is like trying to get blood out of a stone....

TTP

I'm just glad that at least some people who participate in criminal conduct are eventually held accountable... I guess buying that house in Remuera will have to be postponed a bit, aye?

Exactly, while Corelogic is showing falling prices, according to what's happening in the market the data of the housing lobby shows the opposite, interesting coincidence right?

B21

Current (August) CoreLogic data will include raw data relating to contracts entered into during March/Lockdown Level 4. So it is not surprising it may show some negative indications whereas REINZ data will consistent of data exclusively post Lockdown hence will both more positive and reflect the current state of the market.

Given the current very positive auction data next month’s REINZ data is likely to be slightly more positive.

CoreLogic data is like the “Queen Mary” - very slow to show any sign in direction although the rudders have changed direction.

What do you mean by positive? Maybe for you and a few more, raising prices cannot be a positive thing when housing is already highly unaffordable.

Positive as in the numbers/metrics are heading in a positive (increasing) direction. A mathematical turn of phrase, not an emotional or judgemental one.

What numbers are you talking about? Housing affordability or unaffordability? Since the sentence is about data and how positive it is it is hard to tell in a mathematical way.

One stat on that table is baffling to me. Supposedly the Palmerston North HPI is down on what it was a year ago (though not by much). If I understand the HPI right, this means that the same house in PN should sell for roughly the same as it did a year ago. It's the only place other than queenstown with a drop yoy in the HPI. Anyone have any insights? It doesn't seem very plausible to me.

Its entirely unsurprising. NZ house prices are being priced like bonds, a reduction in long term funding rates sees prices rise, irrespective of the season.

What the article doesn't address is the outlook. If we see negative OCR and similar moves across the swaps curve down we will see higher prices if we dont have a collapse in employment or wage levels.

It's a real mess being driven NZs historic and current passion for buying residential housing as its primary investment class.

Unless we start taxing capital gains on investment properties we are never going to see a relationship again between wages and house prices.

Tax free earning - Why would anyone put a full stop to itby introducing CGT.

Asking the people benifitting the most to frame policy/tax against their interest.

Even BLT if go ernment is serious should make it mandatory for vendor selling a house to fill a declaration (Just like buyers have to declare thatare resident/citizen) and declare if they own any other property individually or jointly orunder trust or a company andif yes details since when.

Surprisedwhy no experts have highlighted which I saw as a comment earlier and by doing this is not introducing any new tax but just ensuring implimention of tax as it should be.

Glitzy - Just which country had success bringing house prices down by adding a Cgt tax ?

UK has CGT for both residents and non residents on residential property. They have 40% less property owned by investors (to total stock) and dont have the same 7x income plus borrowing FHBs in NZ have to endure because the banks wont lend those multiples.

And the real difference isn't the CGT, its the limit on advancing credit.

Australia likewise has cgt on investor properties, and their house prices are just as crazy as ours, because they have the same banks we do, willing and able to extend credit.

Because it’s tax on a gain, the investors are still making profit so why would it stop property investment. A company wouldn’t shut down due to a tax on profit. It still makes sense to have a blanket CGT on investment properties. Sounds like it a problem you don’t want to have solved anyway.

I doubt a CGT would bring down the prices, but it would make housing 'investment' more equal with shares etc - tax wise. It has the other benefit of redistribution of wealth on these hugely profitable transactions.

I think the relationship between wages and house prices decoupled almost 40 years ago in the 80s.

Theoracle

I agree - this was at the time of Rogernomics of which the Employment Contract Act is part of and has led to considerable wage disparity.

Note: House prices are not decoupled from high income earners - just the lower and middle income earners.

Question Greg: is this rise AFTER inflation is deducted? Thanks

Mike, the REINZ HPI doesn't have an inflation adjustment. I would doubt Corelogic would either as they are both designed to maximize the published rise.

Thanks

So to me it’s actively misleading

GDP is quoted nominal or real but not house prices

Mind you, inflation has been low (at least according to the CPI...) last couple if years

Glitzy

"both designed to maximize the published rise "

A poor comment - neither are designed or intended to maximise a rise.

Rubbish. REINZ is the trade body for real estate agents, they have no purpose other than generating news beneficial to the sale of more houses.

You are a real estate agent aren't you ? Please dont lecture me about what I choose to comment on when you've skin in the game.

Glitzy

That just goes to show you are abysmally wrong you are on two accounts.

For those who know my interest.co comments over the past 9years 10months will clearly know that I am not a REA.

REINZ and CoreLogic simply present raw data and other than calculating HPI.

Their data is not intended or designed to report on anything other than the state of the market.

Your baseless comments are emotive rather than objective; at best based on not willing to accept what is happening to the market and justifying reality with a conspiracy theory.

Your comment on me being a REA is very clearly simply that; a conspiracy theory and you destroy all your credibility. Very sad if your comments are reduced to being based on erroneous accusations.

"REINZ and CoreLogic simply present raw data and other than calculating HPI."

Is this meaningless gibberish supposed to represent a coherent argument ?

"Their data is not intended or designed to report on anything other than the state of the market."

A rising index with no reference to cost of funding or inflation is of course a marketing tool.

It's a housing index, not an adjusted return index. Do bond, stock or commodity indexes adjust for rates or inflation? Of course not. If you want to adjust for those variables you can do that.

No they don't. But did you ever ask yourself why ?

Stock market indices have the same issue as the HPI published by REINZ ~ they are published by vested interest groups. MSCI, published by Morgan Stanley ~ a broker, NZX indices ~ published by NZX. You get the gist of it ?

Some are cap weighted, some are price weighted but all have one primary function, to market the investment class.

Glitzy

It is simply raw data.

As to the cost of funding, that is calculated and shown in interest.co affordability reports which considers the variables of interest and wages.

For most people, raw data regarding changes in the market affecting potential value of houses is what is of importance and most widely used when either selling or buying to help determine a likely price range.

As to inflation adjusted movements - well that can be simply calculated using RBNZ data along with REINZ data. However that information has limited demand.

You seem to think that REINZ published the data simply to show a positive spin of increasing prices. Please keep in mind that the data is not always positive - during the GFC (and two other periods I had experience of) it was negative, and for Auckland over the period 2017 to 2019 it was slightly negative and at best flat for much of that period. Yes, REINZ interpretation and comment on that data is when spin can be applied.

However, it is seemingly likely that you are unhappy with the current data trend and this is shaping your comments.

You are missing the point. REINZ is a trade association for Estate Agents. They only generate news with a positive spin for their members.

The data trend is irrelevant.

On the topic of raw data, REINZ DONT PUBLISH ANY OF THEIR RAW DATA.

In fact they refuse to publish any data whatsoever which would enable investors or homebuyers to properly research the market.

No, they will know you have repeatedly claimed not to be an REA.. but so did your mate takingthepiss.

Mike

My understanding that it is neither REINZ nor CoreLogic data is inflation adjusted. It is simply raw sales data.

Mike, Fitz and Glitzy

A more significant factor than the significance of inflation that you are overlooking here is leveraging on the mortgage.

You comments seem focused on just how well have property owners done when inflation is considered.

However, the leveraging through a mortgage is considerably more significant and far outweighs any inflationary consideration.

If a person such as a young FHB has 20% equity in a property, and that property even increases only by 5% (whether that be 1 year of 3) then their equity increases by 25% as the mortgage is fixed.

So 25% increase in a year on equity - even though property has increased by only 5% - is pretty attractive.

So even by historic standards a very, very modest 5% increase in house prices in three years - such as the order of Auckland over the past three years - is still going to provide an increase in 25% on equity which compares more than favourably with returns on a KiwSaver Growth Fund.

Yeah, yeah, with a fall leveraging is also significantly greater, . . . . and yeah, yeah, in hindsight isn't it marvelous to say how that stock did so much better.

The bottom line in this is that I look at my fellow boomers who have rented all their lives and now live in cr*ppy social housing are far, far worse of financially than those who now own very comfortable homes.

You make greater gains on any leveraged investment. You can buy shares, bonds, currency etc all using leverage. I dont get your point, this thread is about whether an index includes an inflation adjustment.

Glitzy

Great. Go buy your shares, bonds, currency etc. Not a problem.

Any relevance to the thread about the housing index ?

So if you aren’t a real estate agent then what are you? Chief Editor for One Roof?

Albert

Pathetic.

Clearly unable to add anything constructive other than slagging off. Well done!

What an 'economy' we have built for ourselves. And there are still 'journalists' out there who genuinely think this is a good thing!

(Australian) Treasury documents disclosed under freedom-of-information laws describe how the Economic Security Strategy was introduced specifically to “prevent the collapse of the housing market”. Over the long haul, its continued operation would only serve to help inflate a real estate bubble.

If Treasury understood the real risk of a mass default on Australian home loans, the prospect of widespread foreclosures put the fear of God into the RBA. In fact, things were so serious that the RBA concluded from one stress test in 2014 that the result of any mass default would be catastrophic:

All of the capital assigned to protect the major banks’ $1.25 trillion mortgage books would be wiped out by a ‘severe downturn’ in the housing market.

https://www.theguardian.com/australia-news/2020/sep/12/young-australian…

If in 2014 the situation was bad can imagine how bad it will be today.

God save the nation.

And yet we all continue on down the same path; most ignorant to the consequences of the risks they do not see.

I'm highly critical of the RBNZ role in all of this. But wrong though their tactics have been; stupid they aren't. Paralysed with fear, as the RBA was/is in the above article; Yes. And THEY KNOW what we are up against and have a pretty good idea that we can't keep the current settings going. Whether they have the courage, or capacity, to change course, and when, is all that matters now.

> Whether they have the courage, or capacity, to change course, and when, is all that matters now.

Adrian Orr talks a lot about courage. Courage to lend, to borrow. Perhaps he should lead by example.

RBNZ isnt really to blame here. In any economic calamity rates reduce. We aren't alone in having a yield curve near zero, its somewhat a standard now across the G10 and beyond.

What makes NZ somewhat unique is the zero tax policy on residential property investments ~ and that's fiscal policy, not the remit of RBNZ but that of the government of the day.

The regulatory capital rules imposed by the RBNZ cause banks to extend around 60% of their lending to one third of households to engage in residential property speculation. The RBA embraced the same policy with greater enthusiasm.

{kind=link}

Nonetheless, your observation about interest rates is without fault.

Re-recession Not Required

In other words, not recession precisely but lack of recovery in between downturns of whatever ultimate size. That’s why yields turned negative in these key sovereign markets when they did (and why they were nearly simultaneous in doing so). Rising liquidity risks combined with little to no prospects for meaningful economic growth to offset them (recession or not) resulted in this situation people struggle to understand.

The UN's most current claim for universal utopia includes the following:

Goal11. Make cities and human settlements inclusive, safe, resilient and sustainable

11.1 By 2030, ensure access for all to adequate, safe and affordable housing and basic services and upgrade slums

TRANSFORMING OUR WORLD: THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT (Pdf page 26 of 41)

A little perspective helps though... NZ implemented more restrictive LVR policies compared to Australia while in Australia until recently it was pretty easy to borrow up to 95% LVR even on an average income.

Rising house prices are treated with great glee. Even the Radio NZ newsreader had glee in her voice when reading the 'headline news' of increasing house values....

Rising house prices are treated with great glee. Even the Radio NZ newsreader had glee in her voice when reading the 'headline news' of increasing house values....

Of course. Middle NZ is glowing in the glee. "We's rich" they're thinking. In reality, few of them really understand what's going on.

They don't need to know what's going on. They knew enough not to have dithered around complaining that prices were too high and that they were going to crash in 2010, 2011, 2012, 2013 etc etc.

I would back a doer over a procrastinator with a higher IQ every day of the week.

Fritz and JC

"Rising house prices are treated with great glee."

I can assure you that at the outset of Covid Lock Down the potential for falls in house prices was meet with more than "great glee" - "ecstatic" would be an understatement.

Unfortunately (yes, unfortunately) the market didn't and, as an aside, what is particularly noticeable is that some of those that were so excited that one could imagine them peeing themselves are noticeably now absent or at least far quieter now in commenting on property. Posters that come to mind are Rastus, Carlos67, Independent Observer, Foreign Buyer, Npc, Becnz (the "bears have won") . . . or have become quite negative in their comments.

You two are a few of those still commenting and is great to have your comments.

Cheers - all this is just an observation not to be taken too seriously :)

I can assure you that at the outset of Covid Lock Down the potential for falls in house prices was meet with more than "great glee" - "ecstatic" would be an understatement.

Ecstasy or glee. All subjective. But now the ruling elite needs them to behave accordingly. Go out and buy that boat and drop in to the cafe on the way home for a round of coffees and smoothies for the kids.

Being pleased because you just might be able to afford a stable home for your family is a bit different to being pleased that your house is now worth a bit more than it was. One makes a massive difference to the lives of those who aren't already pretty well off. The other doesn't.

Being pleased because you just might be able to afford a stable home for your family is a bit different to being pleased that your house is now worth a bit more than it was. One makes a massive difference to the lives of those who aren't already pretty well off. The other doesn't.

I understand your sentiment, but I'm afraid that the die has been cast. There is no will or desire for the ruling elite to change anything. What's more, many people are happy with the status quo.

What I will suggest is that these people who consider themselves to be well off might not really understand that this wealth is largely fictitious or based simply on perception.

So al123 and J.C.

Yes, home ownership for 25 to 35 year olds has fallen from 65% to something like 35% over the past thirty years. That needs to be addressed.

However, RBNZ data indicates that 140,000 have become FHBs in the past three years; so if you are not a home owner what are you doing about it?

J.C.; your comment "this wealth is largely fictitious or based simply on perception" is seemingly that you don't care. Keep with Shiller if you like, but he really didn't get the NZ housing market right in the GFC.

What am I doing about it? Trying to buy a f**king house, that's what. I've moved cities to a much cheaper area (one of the cheapest cities in the country). I've spent years saving more than 40% of my take home, I have a well paying job that I am highly qualified for, and house prices have been going up where I live by more than my entire yearly take home pay for the each of the last two years. I've spent months and months looking. Every time I make an offer, even well over asking price, I get gazumped by people offering more or even by people offering less who don't need a mortgage so can have fewer conditions. The next week the house inevitably pops up for rent on trademe at an exorbitant price. I'm not looking for a flipping mansion - just an ordinary house.

Needless to say, I'm feeling pretty pissed off about the whole thing.

al123

I wish you well - a genuinely meant comment.

As previously posted, I am disappointed that despite a badly needed economic reset, no party is currently addressing this in the lead up to September elections. Robertson has brushed it aside on the basis that dealing with Covid and the economic aftermath has priority - it always seems the wrong time.

I see that economic reset not only about housing but also more widely also about economic disparity and especially the increasing levels of poverty.

I accept that you have genuine concerns regarding housing affordability but so do those who live in poverty.

The current economy can be traced back to Rogernomics following Muldoon’s interventionist philosophy. While needed at the time, we are now reaping the negative consequences of that reset 35 years ago.

I see the current situation as just critically alarming as being on par with the situation in the early 1980s.

J.C.; your comment "this wealth is largely fictitious or based simply on perception" is seemingly that you don't care. Keep with Shiller if you like, but he really didn't get the NZ housing market right in the GFC.

Of course I care. Fundamentally, I think credit-driven bubbles are destructive. History supports that opinion.

As for your troll about Shiller, I've never heard him talk about NZ housing. Can you point to any reference?

J.C.

Over the past few years at least I think I recall that you have often referred to a bubble burst and to substantiate that you refer to Shiller.

It was your constant reference and belief in him that I investigated both him and his comments. However, despite his status as a US economist and predictions re the US GFC bubble burst I don’t think that his comments were relevant to NZ then (which proved to be the case) nor currently.

Robert Shiller is not a market forecaster. Never has been. You're trolling.

As you know P8, I wasn't predicting a crash, I said 10-15% drop, pretty much in line with most economists.

Even Tony Alexander said a 5-10% drop.

Fritz

I wasn't commenting on your predictions; rather I was referring to your comment how rises are greeted with glee and making the point that so too comments on potential falls were also made with glee.

Although we usually have different views, I have always found your comments regarding the market to be both realistic and substantiated.

Your prediction of 10-15% at the time was consistent with RBNZ and bank economists - that seems quite a reasonable comment. Those I listed were making far more extreme predictions (30 to 50%) but most importantly were both unsubstantiated and inconsistent with, RBNZ, and bank and other economists.

'House prices have been rising steadily in almost all parts of the country over the last three months'

Still the government's focus is to provide stimulus and subsidies to protect and promote housing ponzi more than businesses and regions that have been badly affected by panademic.

Government stopped/ending stimulus and subsidies that affect directly to business but to protect housing have extended the mortage defferal till March 2021, removed LVR -which too is risky in this uncertain times but did to promote the ponzi.

This confirms that the only economy in NZ is housing economy.

Should ask Jacinda Arden now, what she has to say about housing crisis, as was the issue that got her into power.

Took U turn on CGT as suited their vested biased interest so is she open again to take U turn on CGT after panademic and housing market going into Hyper bubble but have doubts that will take U turn as does not suit their interest.

I think now, even their view will be that housing crisis is a good crisis but may not say aloud.

Economy concequence of coronavirus have not yet started so is wait and watch.

Many small towns like Te Anau have been badly hit and it took years to build those town and without government support may end up being ghost town but government more busy with housing - feel good econony.

In this election Noone is asking the rightquestion togovernment and opposistion being over shadowed by panademic but still time to ask.

Should ask Jacinda Arden now, what she has to say about housing crisis, as was the issue that got her into power.

It was clear early on that she nor her govt were not really interested in this. I believe they are sincere about reducing poverty and a better life for all. But they didn't fully understand that popping the bubble meant disturbing those who have benefitted from the bubble. The trade off was too great. They have learnt that the wealth effect is probably too great to be kicked to the kerb and also realized the extent to which the 'whole' economy is inextricably tied to the bubble.

Yes, Jacinda did say homes for all, but I think she just underestimated the time it would take to provide them. I don’t intend to give up on her, yet, and I see others like Rick Strauss have the same view.

Why U turn on CGT.

Fought earlier election on CGT than also formed a tax committees to recommend tax particularly CGT and still backed out. So why did she fought election on CGT and than formed tax committee if had no intention of CGT.

As mentioned by someone can also make it mandatory for now for all vendor to declare about any other house that they may have either individually or in joint name or under trust just like buyers have to fill a form to declare are citizen or resident entitle to buy in NZ.

No action as no intent.

Richard

A lack of a CGT is demonstrably (as Winston would say) unfair and immoral.

Unfortunately while that is true, it also appears demonstrably true that Winston killed it for self- centred political reasons.

I’ve lost faith. I voted Labour for the first time at the last election, but I won’t be again. It’s clear, now that they’ve ruled out any substantial change to - tax, or the benefit system, or anything at all, really - that they are more scared of losing those now-plentiful middle-class votes than they are of Aotearoa turning into Brazil. From where I’m standing, housing affordability and homelessness have only got worse. They’ve gone from Transformational to Key-like do-nothing complacency in record time. Good job on the Covid, but it’s a nope from me.

brisket

Note that Jacinda was not in favour of no CGT - in fact she expressed some disappointment.

Labour and the Greens were in favour, however both NZF and National (and ACT?) were opposed so there was not the numbers to peruse it.

No CGT clearly lies with NZF and not Labour or the Greens.

It is AMAZING that people forget that Winston killed it. I reminded three people of this the other day. Blank expressions until we used this thing called Google. ‘Aw yeah, that’s right... I remember now’

If Jacinda really wanted to bring in a CGT she could campaign on it this election. She'll have the numbers to govern alone this time around.

The information that is contained within the Real Estate Industry

When buying a property through a Real Estate Agent the questions the agent asks go something like this

What is your price range or budget?

What type of property or house are you looking for?

What size, 2 bdr, 3 bdr, 4 bdr

Residential or Investment

Are you an occupier, or a builder or developer?

If residential

Are you married

The size of your family

If we find a place that meets your specifications who will make the final decision

Are you a First Home Buyer, if not

Do you own the property you are currently living in

Are you selling your current property

Will you require finance

How much finance will you require

In other words is it a cash transaction, or

Will your planned purchase be

-- conditional on the sale of your current abode, or

-- conditional on raising finance

-- do you have pre-approval - how much

If by Auction, potential bidders are required to register and be qualified

I'm guessing, but, by registration and qualification much of the same information is obtained

The point of this is the body of knowledge of what is driving the property market is known by the Real Estate industry but never finds its way into the public domain. If I was a leading writer on property matters I would make it my business to get alongside pre-eminent agencies and pick their brains. I would have a very good idea what is going on

Why are Central Banks Dropping interest rates?

Before getting into it, the central bank simply doesn’t factor. Monetary authorities possess no monetary abilities therefore they follow along with what bond markets are already doing. Sometimes that means lowering their benchmarks, like Jay Powell’s “unexpected” cuts last year, at other times it means yet another QE. Link

After the best years ever for Kiwi fruit, apples beef, sheep, avocados, deer, velvet, only wool is letting the side down. Yet the bonds are screaming no growth for years.

We must have had substantial inflation in the cost of food, rents, rates etc? Is inflation linked to growth and rates falling because they see falling real incomes?

Or is it the end of the debt super cycle some have been on about?

I want to know what's waking Central Bankers up at night in a cold sweat ?

Hmm, in Hastings Napier things are really on a roll, well at least as far as houses and land go, stories of people making over %50 capital gain in the last year abound. However there is another side that not talked about much, as we start to look more like Argentina

https://www.nzherald.co.nz/hawkes-bay-today/news/article.cfm?c_id=15034…

'We all know that fiat currency is going to fail. Historically, every

experiment with it did sooner or later. The fact that the current experiment

survived longer than any previous one proves nothing. In addition, the

regime of global fiat currency has become the breeder of irredeemable

debt. Logic tells us that the construction of such a Babelian Debt Tower

cannot continue forever. It will collapse like its biblical forerunner has,

and will bury the conceited builders under the rubble. The problem the

monetary scientist must confront is to predict when.'

The Quantitative Easing program, the Zero Interest-Rate Policy

and the creation of trillions of dollars in new money throws into

gear an engine that may not be possible to stop except at the cost

of a terrible crash, loose talk about 'tapering' and 'exit strategies'

notwithstanding.

Considering these facts, it does not change the picture in the

least, nor is it of the slitghtest consequence (except in so far as it

misleads people), for the policymakers of the monetary regime

to call themselves "stabilizers" and "experts in the art of moneymanagement". Their good intentions (if any) amount to nothing

in face of the consequences of the uncorking the bottle and

letting the genie out to roam around the world creating chaos in

its wake.'

https://professorfekete.com/articles/AEFAppraisalGlobalMonetarySystem21…

This guys references Babel but doesn't know his history. Historically, ALL forms of money and exchange have eventually failed. There seems to be a massive fetish for returning to the gold standard lately but there have been massive debt crisis occurring many times over the last 5000 years (including during the gold standard era).

Debt existed **before** money. Debt is just something that you owe someone, it doesn't matter whether it is denominated in coins, cauri shells, taxes, sheep, salt, wheat or hours of labour. Debt cycles occur regardless of the method of exchange, they always have and probably always will. We have had asset bubbles throughout history There were some doozies during the Roman Empire, for instance. After the civil wars that saw the rise of Augustus as Princeps, Rome had a major financial crisis. Augustus implemented something of a "new deal" with massive infrastructure spending (ie fiscal stimulus) and eventually followed by loose money (monetary stimulus) when interest rates dropped from 12% to 4%, which led to an increase in prices (including land). Beyond that though, several Emperors debased or rebased the coinage to deal with spending, debt, deflation or inflation.

https://mises.org/library/boom-and-depression-ancient-rome

https://epicenter.wcfia.harvard.edu/blog/financial-crisis-then-and-now

Fiat money isn't the problem. Human behaviour is the problem, particularly when those in power promote policies that amplify these issues. We seem to live in a state of perpetual, deluded, optimism that somehow, there will always been enough money in the future to pay for consumption in the present.

In many contexts this can be true. Debt *can* be a good thing, when it is prudently granted and used productively. But human beings have a major flaw in our ability to perceive risk. Risk is not assessed rationally much of the time , regardless of what some theories claim. And we never learn the lessons of the past. We forget the perils of unproductive, piles of debt and have to constantly invent new ways of responding to them. Over history this has included debt bondage, debt jubilee, debtors prison, fuedalism, the invention and reinvention of banking and insurance and now we have mortgage deferrals, Central Bank interventions and negative interest rates.

Debt cycles are as old as human civilisation. Debt is recorded in 1000's of cuneiform clay tablets. Many writers have such a myopic lens on economics. Mostly choosing to only focus on the last 30 - 100 years but divorcing this from all other historical context, despite how incredibly consistent human psychology and behaviour is throughout all recorded time.

I don't have your knowledge, i'm just not into economics as much as history, linked as they are. From our family experience. We came here from Scotland in the 1860s, bought land in Otago and went farming, probably like home. Several depressions in the 1880's knocked them for six. It was 1886 until more people were born in NZ than immigrant. Those depressions cost the family the farm, somehow they were also caught up in the big Clutha flood , snow drifted 25 meters deep in parts of Cromwell. https://blog.metservice.com/node/1020

They survived and ended up in Hawkes bay after some tough years ,became extremely risk averse which got them through the 30's. That's what I think is going wrong today. My father used to talk of the cattle market correcting once a decade and wiping out those who were to exuberant. Today Central Banks go all out to stop the natural correction process of the market, the recessions that keep you on your toes but also represent buying opportunities.

In my farming world this has been a long run of good times, good or better is the new expectation, 2008 should have seen a lot of farms on the market debts were huge and profits were thin or non existent. Those farmers are today back buying more land , land prices have not corrected.

The classic example of the inequality this produces and who the winners are. John Key bought a 2 million dollar house with tennis court in AKL , was sold 15 years latter for 20 million, minus the tennis court. This has benefited the asset owners hugely and they expect it to continue.

I have a friend in housing, 15 odd houses all low income areas, he told me the general view amongst property investors is ,the Central Bank has your back you are safe as houses ,they will do whatever it takes to keep houses values on the up and up including increasing the accommodation supplement. This is leading to reckless disregard of a market correction and banking crisis in my view.

Debt Crisis in Australia - Yet to start

https://smallcaps.com.au/beware-second-layer-critical-covid-19-debt/

Hopefully not in NZ and economy in NZ will bounce back without much damage.

Agree. "Visible' debt crisis has not hit Australia yet. Or NZ. Don't be surprised if it does.

Remember, the situation is being set up in Australia where distressed mortgages can be ignored. Even in the U.S., there are people still in homes since the GFC where banks didn't follow through with any drastic action. Borrowers can't meet their obligations but have being allowed to stay regardless. The bigger priority has been not to make the banks' books look worse than they really are.

Also different in USA where they have 25 year fix terms dont they? So negative equity can be ignored because they're not up for refinancing every 2 years like here.

They are if finance rates fall - A Tale Of Two Housing Markets: Mortgage Delinquencies Spike 450%, Yet Refis Boom With Low-Principal Loans

"Impressive" is not the adjective i'd use. Why are we celebrating something that benefits only those who own two or more properties? Prices sailing up and away into lala-land are incredibly frustrating at best for the vast majority of NZers.

Yes I thought the use of that language biased as well. Totally unimpressive for FHBs trying desperately to get on the ladder.

I would prefer if this website just provides results without commenting on its merits or otherwise.

Isn't this website concerned with personal finance though? The gains have certainly been "impressive" considering it was against expectations.

Spent a week visiting Christchurch (hometown). Was amazed at the prices of new builds in Rolleston...low $400k's for 3 bed on "enough" land. When compared to Masterton.....

https://www.realestate.co.nz/3779543/residential/sale/lot1065-the-barra…

Bloody hell, Masterton???

Masterton has gone nuts, have a look on Trademe. Sure it's at the end of a fairly decent commuter rail service but it doesn't stack up. Our equity has more than doubled (almost tripled) in 3 years which is cool I guess *shrug*.

It's Masterton....

Why does everyone say there is no capital gains tax. A bright lines test exists for properties sold within 5 years Sure if you hold longer than this then you don't have to pay technically but if you hold for longer than 5 years I'd like to think your a landlord providing rental accommodation.

Correct. Was 2 years. Then changed up to 5 years. Can be increased to 10 years

Thinker

Couple of points.

Yes, a bright line test of five years, but also not necessarily exempt after that period if a property was bought solely for capital gain. An extreme but clear example is if a property was purchased, left empty, then sold six or more years later at a profit then IRD would be looking at taxing the profit.

Secondly, a CGT does not apply solely to real estate. It applies to investments such as precious metals, bitcoin, and shares where yield is clearly not a motive.

Two articles about the same REINZ report in just two days, REINZ data is tainted by their own vested interest so we need more journalism asking the right questions like for instance, is this data inflated by unreported sale prices which sold under asking price?

I hear more and more boy racers on Saturday nights these days, feels like early 2000s again when things were taking off ...compare to GFC way less boy racers...

Young people seems to have money to spend?

They can just borrow it more cheaply.

Wow... who needs a money tree when you can buy a house (and live in it too)

Diabetic requires regular sugar goosing

It wears off

Another required

Eventually sugar bag empty

See interest rate cuts

OCR cuts and LVF changes are good predictors of increased and decreased sales volume in Auckland

August 2007 - now, 8 month time series shows clear pattern of surges and retreats in line with cuts to rates and LVR. Much to my surprise when I did the research this morning, price rises do not lead to lower sales. Rather, absence of OCR cuts leads to stagnation. This is a diabetic market, dependant on sugar hits and then subsiding again into a torpor. The figures for monthly sales show that the peak will be August- November 2020 and sales will then decline in line with prev reversion to mean, until July 2021, which is end of 56 month cycle that started in 2016. Meantime it seems prices will continue to increase.

Average pcm sales in 8 months to March 2020, were 2015, about same as in 8m to March 2014.

Average pcm sales for last 12.5 years has been 2,003.

peak was 8m to July 15, which was 2699 pcm.

12 year range is 1347 to 2699.

Surges in sales are followed by fall backs to revert to mean.

WE had an 8m surge to March of 18%, due to interest rates being cut and surge continued after lockdown due to cuts in March. But ammo and sugar is running out and drop off is due, from November onwards.

Rate cuts allows bracket creep as people leverage up.

Then stasis sets in and people wait for signal to leverage more.

When no more cuts are possible, stagnation sets in.

With down turn to come, the existing surge will not survive.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.