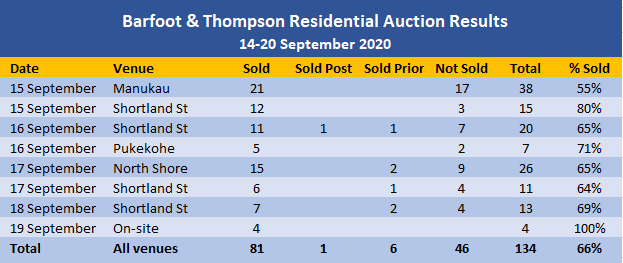

There was more than a hint of Spring in the air at Barfoot & Thompson's auction rooms last week (14-20 September), with a big jump in the number of properties auctioned and sales achieved on two thirds of them.

The agency marketed 134 properties for auction last week, up from 98 the previous week.

Sales were achieved on 88 of those, giving an overall sales rate of 66%, almost unchanged from the previous week's sales rate of 68%.

Barfoot's auction sales rate has remained within the 66-68% range for the last three weeks, suggesting a sales rate of about two thirds is the norm as the Spring selling season gets underway.

The sales rates at Barfoot's individual auctions last week ranged from 55% at the big Manukau auction, to 100% at the on-site auctions - see the chart below for the full breakdown.

Details of the individual properties auctioned and the prices achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

86 Comments

The world is heading into a major depression. The central banks are trying to put off the inevitable. Watching buyers in this market is akin to watching beachgoers before a tsunami who find the beach getting larger and celebrate just how lucky they are having such a large beach.

Well said!

Welcome back!

Pointless, snarky comment deleted. Please try and keep comments constructive. -Ed.

Hell-oo Poppy, watcha been doin' ?

Hi TTP :)

Hi CJ099 :)

TTP

ANNOUNCEMENT:

TTP advises that he takes the above criticism from the editors seriously (i.e. editorial deletion of his post [above] for his failure to adhere to a reasonable standard of etiquette/conduct on this website).

Having considered his transgression carefully, TTP sincerely apologises to the editors and readers and further advises that he has penalised himself by voluntarily imposing upon himself a ONE-MONTH BAN on posting on this website. (This particular course of action has been taken in accordance with the principle of self-regulation.)

Thus, editors and readers of interest.co.nz will not be hearing further from TTP until Saturday, 17 October 2020.

TTP

1 week for being rude, 3 weeks for referring to yourself in the 3rd person.

Dp

RP - Your back ?? How are your TD's going ? Or are you diversifying into property or still waiting for the big Crash ?

Retired Poppy

You're back!

Calling a bubble burst all last year and longer - didn't happen and those highly recommended term deposit rates have just being going south.

Your predictions haven't had a good track record over the past year, and your advice regarding term deposits isn't looking too great going forward.

No wonder you have been so quite, but great to see you again.

Welcome back R-P !! .....and back to the absolute madness, that is the NZ residential property market !! ....my advice for anyone even thinking of buying, is to keep you powder dry and keep on saving up that deposit while the gummint is dishing it out ! ....then pull up a chair and watch it all unfold ....to oblivion ! ...... 90% of the sheeple out there are still blinded by Ashley Church, One Roof and all the rest ! ....Crazy Days ahead says the Crazy Horse !! nniiiiieeeeeeeeggghhhhhhh

CHorse...If you think Ashley Church spouts one-sided biased sermons on property, check out his pernicious diatribes on Israel. They make his views on property almost seem balanced, rational and sane.

Yep my neighbour is a real estate agent ,they said it's gone nuts and off the record ,u would be mad to buy now ,prices for properties are obscene for what you get .

The world is heading into a major depression......how lucky they are having such a large beach

This is quite possibly the most DGM comment I've read on this site

JC

Re a tsunami being the most DGM comment - it’s not quite the first.

Last March Carlos67 was predicting an imminent tsunami - along with hurricanes making landfalls - leading to an all time crash.

Interestingly, I think he is currently talking about buying in the BOP. Clearly is leaving such predictions to GeoNet and keeping with his day job. :)

by Carlos67 | 22nd Sep 20, 11:12am

Yeah the storm is coming but I have jumped back into the property market and bought a house last week. Unforeseen factors are now in play and the chances of a decent price correction were reducing to the point that if I saw my dream home then I'm back in. Sure it could loose 5-10% in the short term but in 10 years time it will be worth more than I paid for it.

DGM? Doom and gloom?

Apex Andy, May be you are correct based on fundamentals BUT fact is that Housing market is All Time High and most houses are going at Premium.

Also low interest rate have been offset by the rising house price for FHB, in fact are taking more debt than before but hard for them to overcome FOMO and rightly as housing market touching new high every week, for now.

Just like Stock Market have confidence that fed will intervene and will not allow it to crash, similarly housing market too has confidence that come what may government will not allow house price to fall and infact will go out to promote it as is main indicator of rock star economy in NZ.

Just checking Manukau auction result and most houses sold went for 20% to 40% above RV.

Saying houses going at a premium is understatement as are going at price where soon FHB will have to even stop trying unless are ready to pay a million for pigeon hole.

Does Adrian Orr have any idea what he has done?

This is what Mr Orr and government wanted.

Hi Apex,

Adrian Orr is a very astute guy.

I'm sure he remains very focussed on the economy and what he's doing.

TTP

He has a portfolio, has he not? He must be aware of how it's inflated.

The fundamental reason for a booming property market in NZ is because NZ is and will continue to be a very desirable place to live for at least another 30 years.

True that, and low interest rates

I think those were "Forced Down Interest Rates"......not to be negative............in truth.

The fundamental reason for a booming property market in NZ is because NZ is and will continue to be a very desire place to live for at least another 30 years

I think if you could get the team of 5 million around a water cooler, the consensus would be that NZ is a 'pretty good place to live'. In fact, that's pretty much the answer to everything. Crusher's Antipodean Silicon Valley will just be icing on the cake.

1 million of the 5 million are not around the water cooler though, they are in the queue at the food bank. They are the DGM's as the priveliged call them. Struggling to cope as the asset class are made richer. Ever wondered why the NZ suicide rate is so high?

You're on a bit of a roll with this DGM stuff. I hope these people lining up at the food banks do not comprise the majority of the the pool whom the other 80% want to rent houses to. As a justifcation for the housing bubble, it wouldn't make any sense.

Lower interest rates + LVR manipulation = bubble = fake elitest manipulated market benefitting only the rich

No change in interest rate + no LVR manipulation = crash = free market where everybody is treated equally

One million in the queue at the food bank? I had no idea it was that bad.

AA, is there a positive correlation between rising house prices and suicide? There are countries with much higher wealth gaps than NZ with a lot lower suicide rate. NZ needs to spend a lot more money on suicide and mental health, I hate these stat's - but it's not house prices. We have a macho male culture where you don't ask for help, Maori and Pasifika who are stuck in a cycle of underachievement etc etc.

I read in May that the salvation army had another 11000 new requests (ie first time requests)for food and that number is rising,not good.

Hi xingmowang,

Indeed, a longer term perspective is very appropriate when considering the property market....... But all too frequently, it's overlooked.

TTP

Good afternoon TTP .....can I please ask a question of your good self ? ....have you even heard of or listened to Martin North, Joe Wilkes, Harry Dent, Robert Kiyosaki, George Gammon, Prof. Steve Keen etc .....as regarding your so called "longer term perspective" for anyone to think, that in 10 years time the western world is going to be "just like it is now" or even going back to 2019, must have a very narrow perspective.......thoughts ?

The REAL fundamental driver of property prices is availability + serviceability of credit.

Sure some houses are selling, but not all, there's no boom, you have to look granular. It's way too easy and lazy to put a blanket statement out on the status of the property market based on a few sales. I know it's used by the RE industry to generate FOMO, and that's understandable as it's their livelihood. But there are plenty of houses on TM property that are still there from 5 - 6 months ago.

Yeah the storm is coming but I have jumped back into the property market and bought a house last week. Unforeseen factors are now in play and the chances of a decent price correction were reducing to the point that if I saw my dream home then I'm back in. Sure it could loose 5-10% in the short term but in 10 years time it will be worth more than I paid for it.

There's some confidence. What do you think interest rates will be in 10 years time?

5 to 10%, how would that go?

Everything changes when you buy a house with no mortgage. Also as you get older you care less about what your house is worth and more about getting on with life.

You are correct as come what may government will not allow house price to fall as entire NZ economy is dependent on it and as the bubble grows more the support needed to avoid bloodbath and government will go all out just like have done it now - mortage defferal to March 2021.

Carlos67- Well done it's not a good time to be out of the property market !

Carlos

Congratulations.

With Covid being a one in a hundred event and lockdowns there was no past experience on what to base the likely scenarios.

The extent of NZRB and government actions such as QE and subsidies are unprecedented.

Clearly RBNZ first priority is economic stability, and if that disadvantages FHB or retirees savings then that is clearly considered of secondary importance.

However, as to where from here, the RBNZ seem to accept that stability (or some growth) in house prices are important in maintaining stability. For that reason I don’t see a “significant crash” in prices. While it could be said it may be outside of RBNZ ability to avoid that, I anticipate that the odds are in their favour.

Bottom line, FHB risk further upside in prices, and there is likelihood in downside in mortgage rates. As long as they can service the mortgage, have job and income security, and are prudent they have little to fear.

Carlos you are correct, any short term fall is of no significance provided these conditions apply.

Since my school days I have never really seen a real world application that would prove that one negative multiplied by another negative would equal a positive. Then along came the NZ housing market?

So when is the housing crash going to start?

And by how much? And where? Auckland and/or rest of NZ?

Do you have the courage of your convictions and outline the scenario? And what will be the drivers / catalysts?

I predict that when the OCR reaches -0.75 all RBNZ's ammunition will be depleted. Orr will resign and the housing market will then slowly drop 30 to 50% of what they are at that point. They will probably around this price level at that point. One to Two years away. DYOR !

Andy meet Retired-Poppy, Poppy this is Apex Andy

National government created a bubble and Labour government carried it forward to create a Hyper Bubble but still no one is raising /asking government during election though the price jump / speculation is much bigger than under national.

If we are being honest this bubble started under Helen Clarke's lead....

Keep the party going! My equity has nearly tripled in 3 years, thanks Mr Orr.

Yeah it is boom for some and doom for many FHB.

Yeah, but it's like the environment and fauna. It's not like we'll see the negative consequences so it doesn't really matter what we pass on to next generations. We can just live off their wealth in advance so we can party harder now.

I was a FHB 3 years ago.

From 12th August 2020 landlords cannot increase the rent more than once in 12 months and this Friday the 6 month COVID rent freeze finishes.

Labour Govt policies usually have unintended consequences so any predictions what impact, if any, these could have on the property market, tenants and landlords?

The new tenancy laws won't exactly drive down rent prices, more like the opposite right?

However building 100,000 affordable homes, is much more likely to reduce house prices and rent prices.

The cost of building should be the scapegoat in my opinion

Sorry, but RE NZ listings are static to falling for Auckland for last 16 days.

Listings for NZ as a whole are down.

Listings should be rising into Spring.

They are not.

On September 6th NZ listings were 25,890.Today they were 25,318

For Auckland, 9874 on Sept 6th versus 9797 this morning.

For Auckland NSC on 9th Sept for houses and townhouses was 751. It was exactly same today.

For Auckland houses and townhouses the total on Sept 6th was 5384 and today is 5427

Rodney was 708 on September 6th and today is 697

Does not look enthusiastic to me.

Auctions sales are showing what went OTM a month ago and sold this week.

Listings trend over last 15 days does not support idea that Spring launch is upon us.

This is not surprising given the sales in June-August. Market is reverting to mean.

Immigration reduction will now start impacting market.

Total sales for 2020 for Auckland highly unlikely to be more than 10% higher than 2019 (which as lowest sales pa for a decade by way).

Oh my dear Mikey, Mikey Mike

Once upon a time, there was this commentator called Retired-Poppy......... don't worry, long story

v constructive. Great contribution

Thanks Mike, it's often tricky to give constructive criticism, especially to ppl with entrenched positions

Oh the irony.

Calling statistics an 'entrenched position'...

If you're implying that I'm calling statistics an entrenched position, I did nothing of the sort. That doesn't even make sense

To clarify for you - by entrenched position, I'm referring to Mikekirks permabear position.

Just because he interprets or uses statistics to suit that position doesn't at all mean he's right (doesn't mean he's wrong either)

By all means, follow his advice if you have a high-risk profile imho

Sales rate exceptionally high in June-August.

Lots of pent up demand released due to LVR and rate cuts, so people moving up a bracket, price wise.

This has an end point and further sales surge not supported by demographics or immigration, nor economic growth. So there will be reversion to the mean. Sales have a 64 month cycle and the recent surge started last November.

Average pcm sales in 64 months up to April 2017 were 2397 in Auckland.

Since then pcm average has been 1845 up to end of July.

This surge resembles that in 2009, to Nov 09.

After which it fell back 20% to 1633 pcm, which is what I expect for next 8 months.

This surge is not sustainable and won't be sustained, like that in 2015, when pcm sales hit 2771, the previous peak, from April to November 2015. That was driven by Chinese money and immigration. Neither is present now.

Do not expect 2020 sales to exceed 24,876. That would be a 10% rise on 2019.

That requires next 4m to come in at or above 2419 pcm. Won't happen. Only 2007 has managed that in this phase of the year. Not since.

The reality Mike is the less stock on the market the higher people are willing to pay for it- that is what’s driving the market up right now

I am referring to buyers and demand.

There is no an infinite source of buyer stream; it dries up and comes in fits and starts.

Hence, look at historical sales record and compare. Which is what I did.

People do not just move and buy bigger because it is cheaper to do so. yes, that happens. BUT there is a limit to the tranche that will do so in a set period.

Which is why I do not believe this current surge will continue and will not equal 2015 or 2007.

In last 4 months of the year in 2012, sales in Auckland were 9866. In 2015 it was 9891. In 2019 it was 8309.

To sell 10% more in 2020 than in 2019, Auckland market has to sell 9678 in last 4m of the year. I do not think so.

It is worth reflecting on what has happened in the past year.

Many on this site - along with Retired Poppy - were claiming immanent bubble burst last year and strongly advising FHB against buying.

Over the past year - despite Covid and lockdowns which if anything, should haver precipitated a bubble burst - REINZ August figures show that both national and Auckland house price medians have increased by about 16%, and RBNZ data show that mortgage rates over the past year have fallen by about 1% (from 4.5% to 3.53% for 1 year).

So that FHB Auckland home last year at $650,000 is now going to be $754,000 ,and nationally that $500,000 house is now going to $580,000.

Interest rates is going to mean that on that $500,000 Auckland home mortgage are now going to be $5,000 per annum or $191 a fortnight less. If the mortgage was affordable the past year, it is going to be a lot easier this coming year and the outlook is for further interest rate falls.

Ok, ok, ok . . . . "the bubble burst is coming". Well Independent Observer admits to claiming that for five years now, and Retired Poppy for well over a year at least. So what if there is a correction: as long as the FHB has job and income security - as Carlos67 agrees - they have little to fear for short term corrections.

There are too many scaremongering comments on this site, and those like Retired Poppy need to admit and own their comments from last year.

Hi Printer

I take it some of that was directed to me?

I did not say "bubble" or "burst"

I referred to historical demand and sales push criteria not being present.

I said reversion to the mean.

This is a rational assessment. It is not about a crash in sales or prices.

prices will not fall til a major economic hit happens and gov and RBNZ have postponed that til who knows when, but at least Feb (cue snore from Yvil no doubt)

No Mike - it was not direct at you but rather the numerous number of those on this site who were claiming bubble burst.

During the winter I was posting that the Auckland market seemed to be bottoming out and argued that any further fall was in the range of buying well and poorly. Last September on the basis of auction data, I said there was indications that there was signs of an upturn in the market. I was overwhelmingly rubbished by a number of people including Retired Poppy.

So not directed at you, although I think do recall you saying last September that the "market" was heading south.

Note: I have long maintained that auction data - provided one can interpret the signs - are the best current real time indicators of the market. The signs to look out for are the number of auctions, clearance, and as a guide, the percentage selling over RV.

As I have previously posted; the most valuable thing I learnt at Uni was pick the signs of a likely great party, don't wait to hear that it is a great party because you have missed most of it, and certainly don't wait to Monday morning to hear stories about it because it will be all over and you will have missed it. Same with the property market.

Printer you are correct

But what everyone missed is the amount of money the govt and the RB were able to throw into housing with the mortgage deferrals and interest rate cuts and dropping of the LVR. Next year you’ll see the deferrals extended a further 6 months and if the market goes backwards Due to job cuts and low immigration you’ll see som form of FHB grants to get on the ladder.

Tillers

I agree that there is uncertainty - as there is with most things - and there may be come correction (Treasury for example estimate 5% ).

For that reason I usually add the comment that as long as one can service the mortgage and has job and income security, then short term fluctuations are irrelevant.

A potential FHB can anticipate that a fall may happen, but there is no certainty of that and if not they continue to struggle more so. However, that is dismissed by many as simply FOMO.

To me, bottom line; one's first house is a home. Too many overlook that.

You do know that Robert Shiller warned about the US property market tanking about 5 years before it happened in the US - and he has a nobel prize for asset pricing? (not that I'm comparing myself to him, but I have read many of his books and watched much of his youtube including his free Yale Finance/Econ courses - so have an understand of how he sees the world). Did that make him wrong for those 5 years while everyone loaded up on debt and purchased more properties - encouraged by people like yourself on sites like this? Note that I lived through that first hand in America - I watched it all unfold. If your intention is to dismiss over peoples views because they make you uncomfortable, then your going to be sadly disappointment that we don't disappear. We don't go away. What is going on with debt is a potential disaster in the making so I stand by my comments.

IO

Ok, ok but:

- US "tanking" was due to US subprime mortgages not present in NZ

- while US tanked the housing market in NZ didn't (other for a brief period) and in fact gave impetus to rapid increases for the following decade, and

- is he currently predicting falls specifically in NZ market?

I accept that there is always risk including housing and, as I comment above, for that reason I often refer to the necessity of being prudent.

It also needs to be recognised that there are many risks at a personal level which can be even more devastating.

Haha the risk/s in the system at present could be considered many times worse than the subprime mortgage crisis! That might look like a small blip when all of this has played out.

IO

I agree with you that that current growth in the market is unsustainable and with there is some uncertainty and increasing risk.

I would not be surprised to see some correction over the next year or so and in the longer term the market could be relatively flat. We may not see growth periods similar to what we have seen over recent decades.

Either house prices are going to come into line with wages, there will be a crash, or NZ is going to be a country where home ownership is not the norm as is the case in many European countries. I hope for the first case.

In the short term, potential FHB need to recognise the uncertainty and risk and be prudent. They can take some comfort from the banks as they are being prudent in their lending by considering job and income security and applying the 7% stress test. That protects the banks - and borrowers - in a market correction does not seem reckless lending to me. This is quite different to the situation in the US leading up to the GFC.

IO .....I can guarantee you not many on this thread would even think that what happens overseas, whether the USA, UK and Aussie etc is going to affect their "bullet proof" NZ property market.....they have their "blinders" on, to anything that could disrupt or change the "status quo" now here in NZ .....in fact it can be summed up and has been said many times before on this site ".....but were diff'runt".

I experienced parts of the USA market from 2011 onwards and I will never forget in November, 2011 walking into a beautiful home with all the "bells and whistles" in Phoenix, AZ only to find out later the owners were "underwater" with their mortgage v. house value .....and here's one for all the property bulls out there .....the owner was a real estate agent.

Hi all, newbie here. I have been doing research on the housing just like all of you. The fastest way to end recession is by encouraging people to spend. By reducing mortgage rates etc, the govt is going by the book and doing things. Asset prices tend to rise during huge events and are encouraged by the govt. Ideally, govt won't let house prices to fall. They might stabilize by 2022. Once this happens, all the remaining things like groceries and other prices will start rising. When the govt decides house prices have over shot and might risk mortgagee sales, it might rise oil prices and other rates which will immediately bring a little control back to the housing market as people are discouraged due to the rising prices. Economy of the whole world is suffering. This will definitely have an effect on the economy. What actually is needed is to encourage people in nz give out ideas and make it self sustaining. Focus on self reliance will encourage people to do more and be creative than focusing on asset price increasing. This is something which will any way happen.

I disagree with the negative sentiment here. If I had the deposit and the income, I would buy as much property as I could. Cheap interest rates, New Zealand a good place to be long term (relative to other commonwealth countries), stable government, and a major shortage of property means house prices can only go one direction - up.

Also as my former mother in law said - Auckland is a young city by international standards, it's still finding its feet, and we're 20 years behind Sydney. If you could buy in Sydney 20 years ago, would you?

Sure, let's take financial advice from your former mother in law...

So if Sydney is 20 years ahead of Auckland, why aren't house prices 4-7 times higher there? Since property prices always go up and they double every 7-10 years.

Auckland is one of the ugliest poverty stricken cities in the OECD. 90% of it looks like a shanty town. It's certainly no Sydney.

Yep ! ......finally the people are waking up !

Sure, some parts of Auckland are great and really beautiful, but that's a minority .....but there are certain areas that ask ridiculous prices, because of the land being close to the city - but the look of some of these areas is a real mess, with crappily built or unmaintained houses, while depressing, damp and cold in winter.

Lived in Sydney for a year and yes, for housing it's streets ahead of the AKL.

You 3 are so relentlessly negative it's sad. Of course Sydney is pretty in the glamour suburbs (like NZ) but also butt ugly in many others and, Paddington and inner west aside, housing is architecturally poor. Most motorways are heavily tolled so that a tradie living in the west is clocking up $200+ a week to work in the east or north. There are swathes of ugly high density living as well. The roads are in shocking condition. A house withing 5km of the Harbour or Bondi/Bronte starts at $5m and go all the way to $50m no problem.

Just like 2015 boom?

2015 sales were 31,707

So far in 2020: 15,198

June-Aug 2015 sold 8620

In 2020 it is 7441 (13.7% lower)

Sept-Dec 2015 sold 9891. Not going to do that this year.

Unfortunately Mike all I see now is an upside for housing in New Zealand. The rest of the world is turning to shit and what we do best is grow food and have clean air to breathe. If we stay covid free then there will be no shortage of people with big money wanting to move here to escape. The whole world is in a downward trajectory caused by overpopulation and New Zealand will be the go to place to live.

Carlos67.... IF we stay covid free; IF your aunt had balls she would be your uncle.

I've argued for a long time , if their is a major global military conflict or foreign governments go into some sort of real real serious economic melt down ie 30% unemployment, nz will be a safe haven for the very rich if the government let's them in and and if so asset prices will climb higher.

However I'm not feeling positive for the average kiwi battler struggling with mortgage payments.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.