Auckland's housing market may be close to peaking and could start to cool next year.

The latest figures from property website Realestate.co.nz suggest the Auckland market is on a different course compared to the rest of the country.

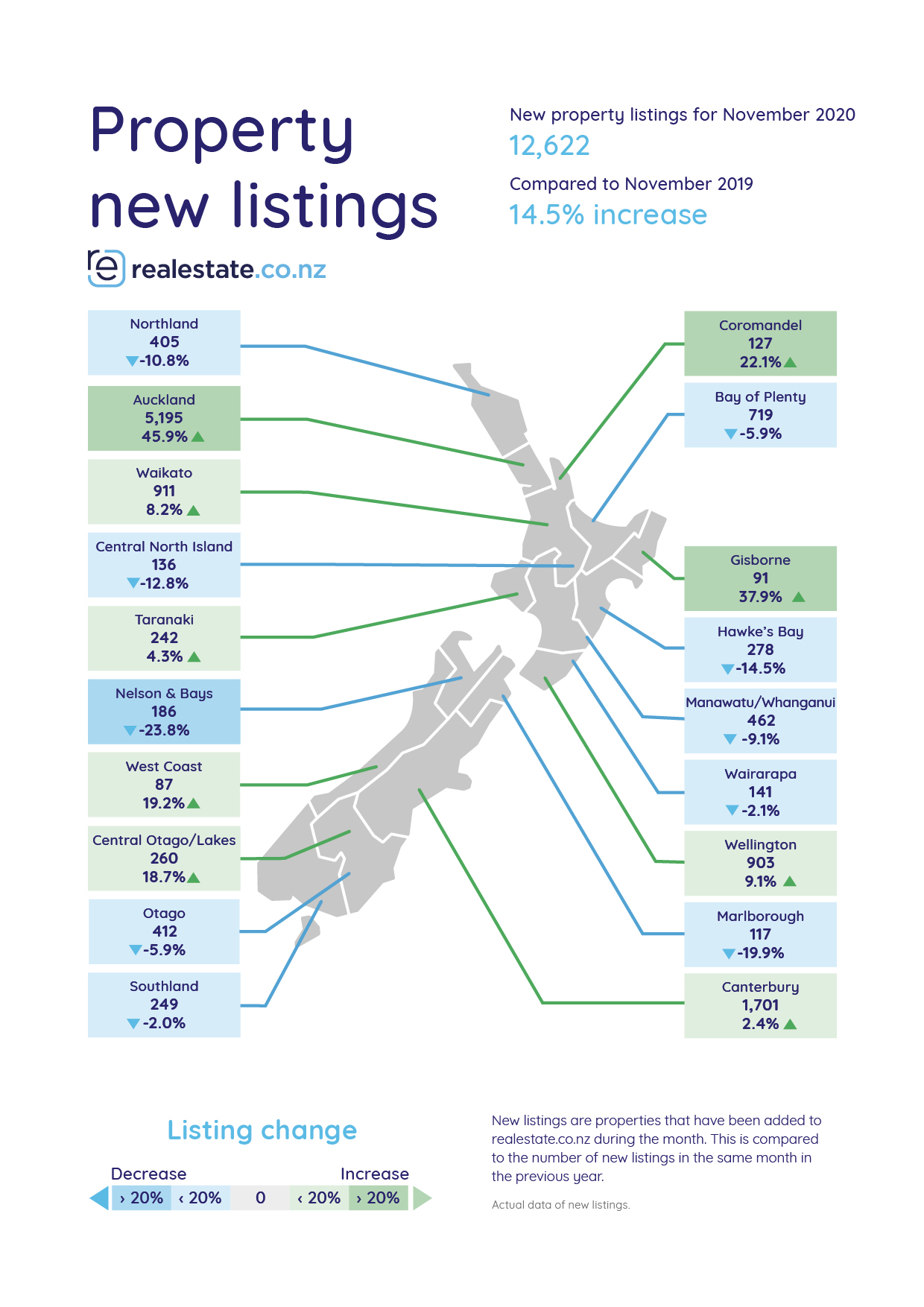

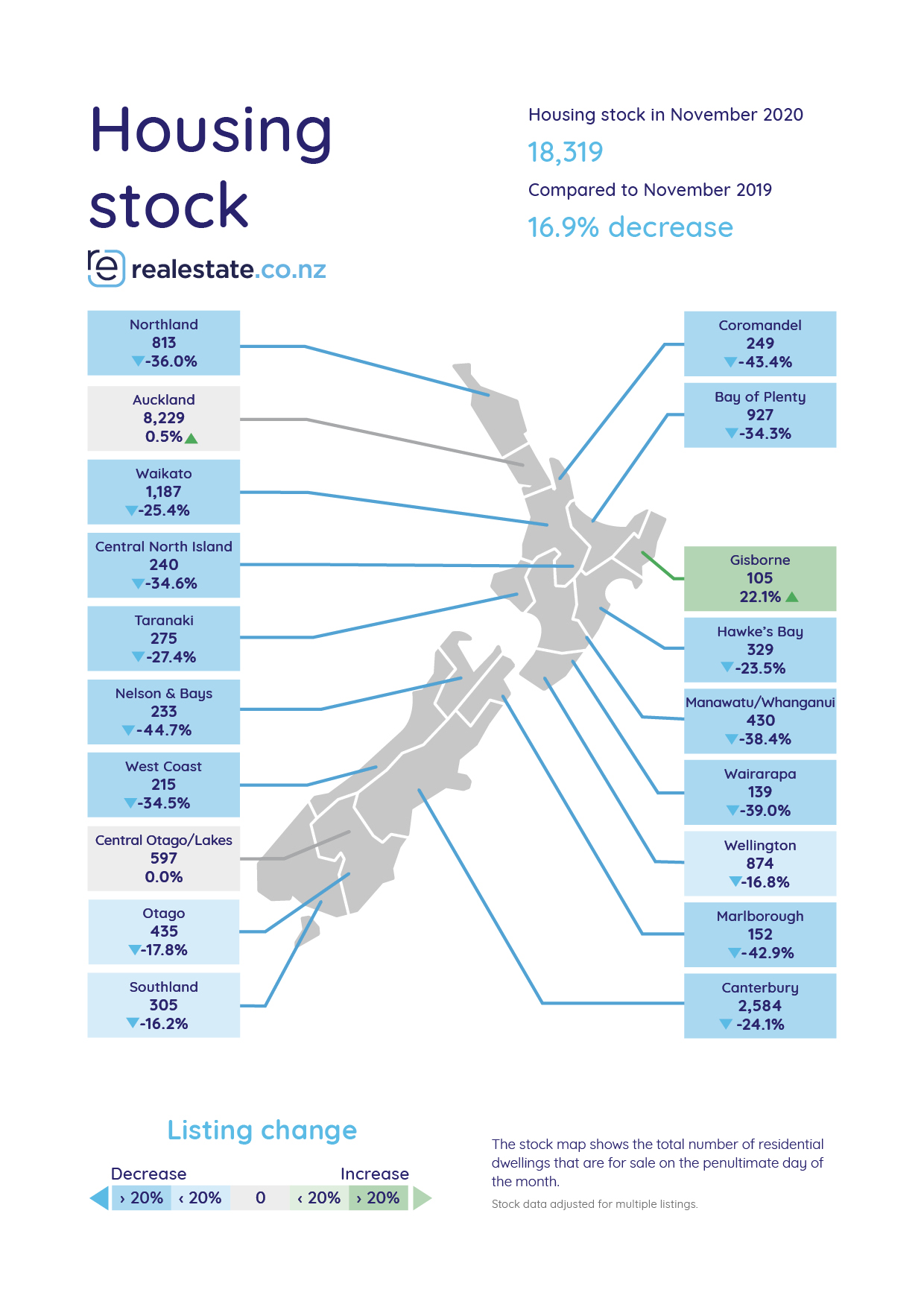

Although the website received 12,622 new listings from throughout the country in November, up 14.5% compared to November last year, the total stock of dwellings it had available for sale at the end of November was 18,319, down 16.9% year-on-year.

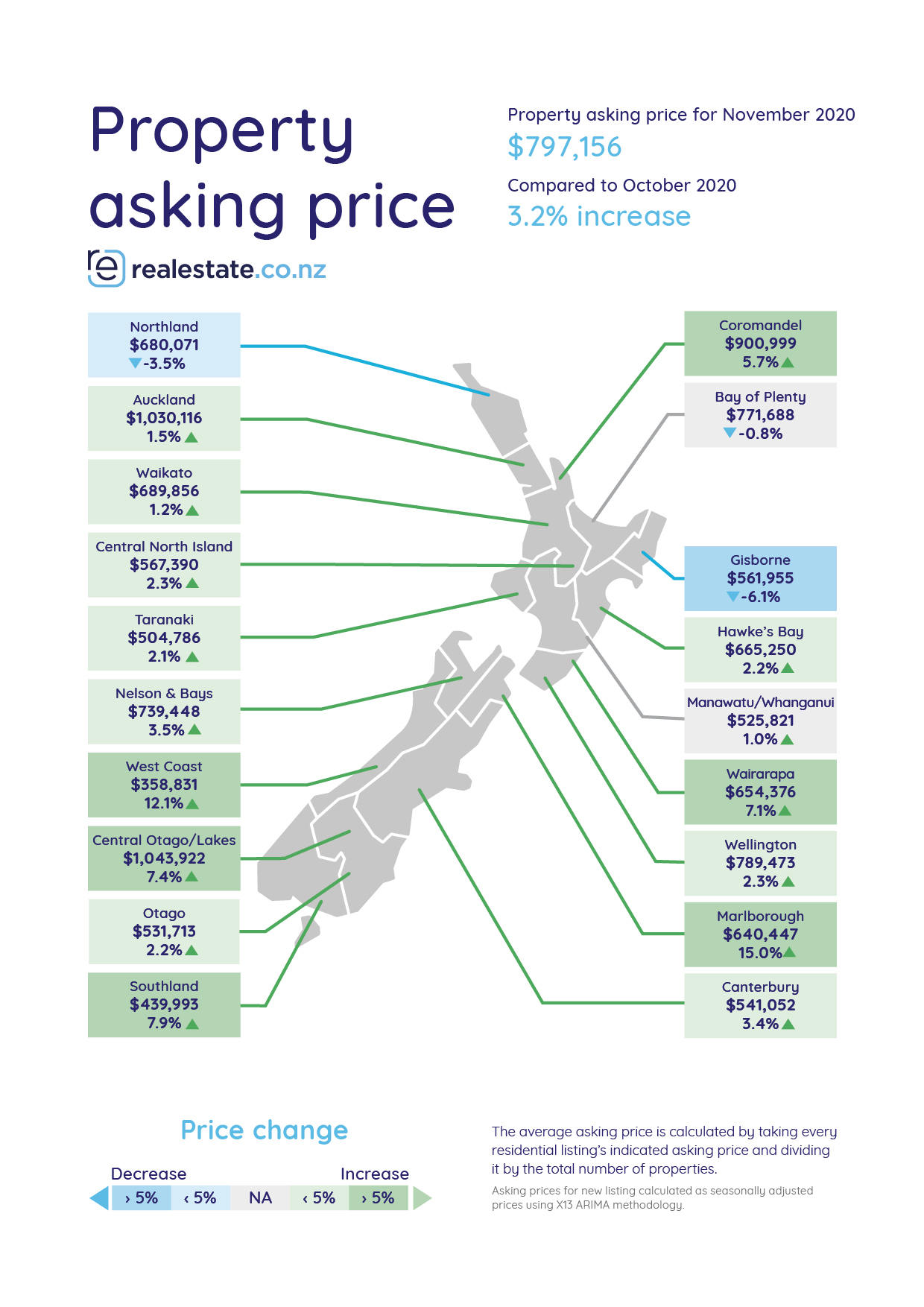

Over the same period the average asking price of all the residential listings on the website increased by 3.2% between October and November.

Those national figures all point towards the sort of overheated property market other indicators are suggesting.

However the Auckland figures paint a different picture.

Realestate.co.nz received 5195 new Auckland listings in November, up a whopping 45.9% compared to November last year.

That was the highest number of of new listings for Auckland in the month of November since 2007, and the highest of any month of the year since March 2008.

And it was not just a monthly aberration.

New listings in Auckland have been running at significantly elevated levels for the six months from June to November and that is showing up in the total stock levels for the region.

While stock levels for the country as whole were down 16.9% in November compared to a year earlier, in Auckland they were up by 0.5%.

Not surprisingly, average asking prices in Auckland increased by 1.5% between October and November, which was less than half the national rate of increase.

All of the those figures suggest that supply and demand are moving more quickly at getting into some sort of balance in Auckland than they are in the rest of the country, and that if the Auckland market hasn't already peaked, it may be getting close to doing so.

There's an old saying in real estate that Auckland leads the market and the rest of the country follows. If that's the case, we may be looking at the beginning of the end of the current housing boom.

However 2020 has been nothing if not unpredictable and 2021 is likely to offer more of the same.

On the one hand the Reserve Bank appears committed to spewing out more cheap money into the banking system, most of which appears likely to end up in residential mortgages, and mortgage rates are likely to fall further.

On the other hand the Government is increasingly getting its panties in a twist over affordability issues, with a restructuring of the Bright Line Test for taxing property re-sales on the cards. And the Reserve Bank is moving to reintroduce restricitons on high loan-to-value ratio new mortgage lending from next March.

So whatever happens in the housing market next year, it won't be dull.

The comment stream on this story is now closed.

82 Comments

Given housing represents an increasingly large slice of New Zealands econony will RBNZ allow house prices to cool? My thought would be any hesitation in price inflation would be passed through to CPI and RBNZ would trigger a new tsunami of liquidity.

I agree with the headline but it depends what we mean by "cool".

Clearly the current levels of increase are not sustainable and even REINZ have stated this. I posted about a month ago that I see the market being flattish next year with some minor correction as was experienced 2017 - 2019 but quite likely for a longer period of time; I see that as "cooling".

Will RBNZ be prepared to live with this? While they have committed to FLP which will provide some stimulus they have also signaled LVRs for March next year.

So yes, RBNZ will seemingly allow this.

As the vaccines roll out, and economies not only adapt to a Covid world but also activity begins to pick up there will be less need for stimulus such as need to protect employment.

However, I don't think that after all the actions RBNZ have taken to simulate the economy and as a consequence housing, I don't think they will be willing to see all that undone. So I expect that will take whatever action required to try and avoid a major correction.

I see your point but have you taken into account that CPI is still under RBNZs forecast with house prices rising at this rate and that New Zealand likely has one of the least closed economies so there is less bounce to be had?

Likewise I agree with your point.

I note that the government and RBNZ are in talks regarding housing and as I understand it’s the government that sets the target and to whom RBNZ are ultimately responsible There may need to be some compromises on both employment and inflation if government accept that the housing issue is urgent and high priority.

You know more about economics and policy than you do about politics and government. :-)

Well once upon a time, sheep meat and wool used to make up a big chunk of our economic output. But I guess houses are different.

.

Unlikely

When their is news that RBNZ and Government may act - reluctantly as been forced and have no real intent still -still so called experts and media mostly supported by rich and powerfully RE lobby will start blackmailing government on tax or anything (as they know that Labour party has a complex of being portrayed as anti business and to prove otherwise easy to be blackmail or influenced ) and also news about cooling housing market...........anything to influence and deter Labour government for whatever little they may be forced to do to stop speculation.

Let us be honest, only economy in NZ is housing economy and no one wants the ponzi to stop.

Great- no need for rent controls or any other Bolshevik rubbish!

Is that because it is really, really good to have a few people owning all the houses while the rest can barely put food on their tables from having to pay for them for them?

You are exaggerating.

So is the guy whining about Bolsheviks above, welcome to the comments section - where hyperbole and ignorance are the name of the game

Come'on Ace - where would we be today without the RBNZ's "bolshevism for Bank-owners"? Since 1934, this country has a proud history of socialism for the rich, propping up banks too big to fail, and ensuring their bank-owning school chums never have to see a loss. State intervention is only distasteful when it favours the common man.. Let's not forget it!

Yes need;

Becroft said he was calling for an increase in benefits, increased supply of state and social housing, and “new ways” to manage rental costs.

https://www.stuff.co.nz/national/politics/123565920/new-report-not-enou…

Point is, if we don't pursue these "new ways", the call for more taxpayer subsidisation of the cost-of-living just grows louder and louder.

Kate.... apart from wgtn, rents are not going up that much. So why are rents in wgtn and lower NI rising but not the rest of the country. That's the question you should be asking. Could it be something to do with new HH standards forcing them higher... houses in wgtn need a lot of work to bring them up to standard or am I wrong about that.

Public sector attracting both full timers and contractors, tech sector in Wellington is strong, rates going up by an anticipated 22%, nowhere easy left to build, most buildable land is owned by private land bankers. Difficult to build up - strict earthquake standards. The rate of demand continues to outpace the rate of supply. I wouldn't say you're wrong about the HH standards, but I'd say most LLs are cashing out rather than upgrading them to the required spec.

Come on @flying high. Can you look yourself in the eye and tell yourself the favorable tax treatment and incentives for property investors isn't exacerbating the issues in housing affordability? We've all got different views on this subject but I think we all need to acknowledge a core number of facts.

Yes, these other things are exacerbating the problem BUT only because of the lack of any supply of alternatives. If affordable new supply was allowed that already had these benefits then any outdated stock would be discounted back to reflect this.

It would be cheaper to just hand out 40% off puffer jackets to all.

What is so difficult for people like you to understand - it doesn't matter how many layers you put on, windows you open, or walls you scrub. If there is visible mold in a crappy old damp home then there is also unseen mold being breathed in also.

That's the question you should be asking.

No need to ask any questions - we just need to demand the government take action that is not at the expense of the general taxpayer.

The welfare state is not there to subsidise the cost-of-living for working New Zealanders. The cost-of-living needs to come down and the best place to start is with the largest expense for most people (accommodation).

Monetary policy is providing cost-of-living relief for asset owners - so regulation (fiscal policy) has to do its bit for non-asset owners.

No need to ask any questions...

Ok that's fine you but it may not help your one eyed cause when people point this out to you. Hahhahahaha keep hammering away Kate,,, I have someone hammering away for me

I have just realized that this is just a wind up... probably to scare off potential younger investors. You have already said you don't care whether there are negative consequences from fixing rents and now it's the one eyed "no need to ask questions" or have a solid view.

Life is what you make of it... sam Morgan grew up poor and look at him now...

As a child, Sam lived with his motorcycle-riding hippy parents and two siblings in a house bus parked in a Newtown backyard.

Too poor to afford a mortgage, his mum Jo drove buses for the council, while dad Gareth pored over horse race statistics hoping to develop a get-rich-quick scheme.

Sam Morgan - the boy's done good - NZ Herald

https://www.nzherald.co.nz/nz/sam-morgan-the-boys-done-good/UMLNSZSRQ6C…

You really need to add in the next sentence to give context.

'The horses failed him but Gareth became a successful economist instead and got the family out of the bus and into Wellington's posh Oriental Bay.'

But you have to give it to his Dad, what a great segue, horse race statistic get-rich-quick schemes (I think a few horse people have just been convicted of similar-sounding schemes) to a successful Oriental Bay economist.

And 'nex minute' head of a political party.

Its a tough road lifting oneself out of poverty particularly with a family in tow. The morgans have made lots of money from their trademe idea and beat eBay to the punch.

B727...wouldn't want to do anything to endanger resumption of your business class holidays even if it would allow people to put food on the table and clothe their kids.

No international flights currently so no BC for me either!

I've never paid for business class....or increased rent on an existing tenant!

Cool? To what? A bit less unaffordable?

Affirdable means rise by 50% than fall of 10% to pacify FHB this is the way experts and government screws average KIWI

Could an explanation for this 45% jump in listings be simple pent up listings activity that was differed because of disruptive lock downs in Auckland?

Always important to look at what we are comparing to. Listings in 2019 and 2018 were weak and old stock OTM was about 32% of total stock.

Ditto, sales, which were on 5 year lows in 2019.

Hence second half of 2020 looks v manic by comparison.

Yet sales still 4,000 below 2013 in Auckland, on 12m running basis.

MAY be cool from NEXT YEAR.....

1 : Not sure but may be cool from nezt year

2 : What happens till Next year.... After 50% rise.

Why this Hypothetical theory/article now, when truth/fact is that housing market is on fire and average rise in Auckland is as much as from $4000 to $6000 per week and not $2000.

I imagine it's the same reason behind this article from him eight days ago over at The Spinoff:

'Are first home buyers really in a worse position than three years ago?'

https://thespinoff.co.nz/money/24-11-2020/are-first-home-buyers-really-…

Saw an article yesterday saying that FHB's are starting to loose interest in property with high prices & auctions. Do these articles try and reign people back into RE?

QD.. I have asked Greg Ninness to write an article on exactly this several times. Sadly he has never obliged or responded. Why? Who knows?

Orr - "Hold my beer"

He's been doing this stuff for so long I'm starting to worry he'll get dehydrated

IV drip, he's got it sorted. Don't worry.

"From each according to his ability, to each according to his needs" In the NZ context the need is a few rentals and ability is to be able to borrow easily.

This is not unique to New Zealand. We are nothing special. We are just following what is happening throughout the rest of the world. Central bank policy is to allow people to borrow as much as possible as cheaply as possible - in other words take on massive amounts of debt because it's cheap and therefore affordable. The borrowing Is completely centred around personal borrowing - no appetite for lending to businesses. Looking at the bigger picture what does this tell you? That we are somehow special and invincible? Or that we are up sh1t creek in a sinking boat without a paddle.

This is my take on it as well - it's a global problem and we'll soon see the effects of the coronavirus lockdowns from Feb / March manifest itself a year later in 2021. Basically when the virus hit, all governments around the world responded with lockdowns, stimulus, mortgage deferrals, wage subsidies, halt on evictions etc. Those basically bought us time to get to where we are now, having more knowledge on containing the virus (well, here in NZ we do, but the USA is another topic) and potential vaccines getting rolled out. But because people weren't forced to sell (so less supply) and cheap credit influenced people to buy (more demand) then obviously prices have risen. But come 2021, once more businesses close down and unemployment rises, more people will be forced to sell and there will be less people available to buy. NZ is not in a unique situation at all. This will first happen in the US then followed by Europe / Canada / Australia, then Auckland will soon follow. Then the rest of NZ. It will be a synchronized global slowdown.

Stock is up in Auckland but it's terrible - North Shore/Rodney anyway. Poorly maintained & out dated. As soon as something decent comes to market it's snapped up in a week.

Hi Nifty,

I keep a record weekly of RE NZ stock for different districts. On November 28th 2019, Rodney district had 847 houses and townhouses OTM. It is virtually identical now.

But on Hibiscus Coast listings are way down, by about 20%.

Some small towns are still catching up to Auckland from the pre-Covid price rises. It's very hard to justify houses in Tokoroa and Taumarunui selling for the same price as a three bedroom house in Tauranga, but in some cases this has been happening.

There is a lot of cheap money available that is fueling a one-product asset bubble. There are some very over-priced houses on the market and when we do finally get the correction, some communities are going to be financially ruined, while others likely won't see much of a correction at all.

How that correction occurs isn't likely to come through any change to supply. It's probably going to come through homeowners losing their jobs and needing to sell their home to put food on the table. The government paid half the country's wages for six months this year, and that money is starting to run out. The "kindness" will probably last til Christmas, but I expect there will be some grim faces early next year when the Christmas spending figures come in.

That scenario seems distant to a lot of commentators, but it's the most likely situation where we will see a sell-off.

Yes, some places in NZ are now looking very expensive, even when compared to Auckland. I think many areas are overcooked. Auckland Kiwibuild new houses don't look too badly priced, even though they don't look like great options.

So... Aucklanders moving out, creating overheated markets in other regions?

Auckland stock is different to what it was a year ago, although only slightly own in total.

The over 3m OTM proportion is lower by about 7% due to increase in turnover, which has risen about 50%.

That is, stuff sells a lot faster and a lot of stuff selling is not built yet (which used to clog up listings like bad oil in bottom of your sump.) That sludge is getting sold!

Also, the slow down in new listings per day started 3 weeks ahead of usual seasonal norm and has fallen 16% off the peak. So the "slowdown" or moderation, has in fact commenced already. Prices still rising however.

What happened to the 25% drop you were forecasting in April this year?

Again I will explain: in mid 2019 I forecast that prices in Auckland (median) would fall to $670k by end of 2021.

It is now December 2020 and no financial crisis has occurred YET.

As most financial commentators of erudition acknowledge, this is because of massive QE, far in excess of that 2008-13, already (in 10 months, not 5 years) + government largesse.

None of that, or CV19, was in sight or forecastable, in mid 2019. Plus interest rates cut in half and LVRs removed.

So, hardly surprising that my forecast has been derailed is it?

Prices will continue to rise until some of the above factors are removed, or we have an economic crisis that all of above factors are designed to prevent.

All these factors mean it is NOT a free market, so normal predicators of market cycle of sales and prices are anaesthetised.

Agree with all of that however do you honestly think Labour will allow a resumption of a free market and the potential it has to cause damage to its new found friends.

A little ill-advised, Greg, to use term "panties in a knot"

Wiser to keep it gender neutral!

Undies in a twist, perhaps.

So you're saying as a bloke I can't wear panties? The audacity of some people!!!

mikekirk29...in this day and age he needs to be more inclusive. What about those who don't wear panties? They must feel terribly marginalized and left out.

This week we knew more and more buyers thinking it is not a good moment to buy and given these listing numbers sellers think exactly the opposite, it is a recipe for prices to start going down and summer will also help in that respect.

The Labour Party will have a pretty close figure of how many of the people who voted for them have houses already, and how many don't. My suspicion is that they have to pay lip service to the non house owners, and actually look after the owners. We will know by their actual actions, not their semantically careful words, what they really intend. Bringing in a new Bright Line tax doesn't count of course. Grant is starting to seem as financially imaginative as his Dad.

Their narrative is limited to saying this is happening in other countries too, which is as simplistic as it gets. They miss to mention they can but won't do anything about this but probably a simplistic sentence that can make it to a short header works for most of the population and they know it.

They campaigned on Nationals policy platform (i.e. do nothing, apply a little window dressing to social welfare etc.) and now they are following through on that. TOP didn't even get over the parliamentary threshold talking about comprehensive reform.

What do voters expect? They made their bed.

Too simplistic. I own property, i am also a boomer and also a former Nat vote. I voted Nat out for housing reasons and will do the same with labor if they don't get on with it. I have many friends who are of the same mind.

Boomers + Home Ownership does not always = property spruiker.

Its just that noisy property owning boomers control the media narrative.

There's definitely an osmosis effect percolating (osmosizing?) out of Awkland. The plumber just around the corner from me is working on a $17m house in Fendalton, by a stream, and in an area badly affected by the Christchurch earthquake sequence. Irrational Exuberance doesn't begin to describe this.....

$16m will be for strengthened earthquake foundations. A group builder will be supplying the rest.

New listings of houses and townhouses on RE NZ yesterday: 111

Prev 6 day average : 176

Prev 6 day average prior to that: 213

peak day: 256 on November 5th.

Market listing is dropping and started doing so 3 weeks earlier than normal.

Fewer properties on the market means higher prices as there will be more competition for what is available?

Hey lets not forget Christmas is now only a few weeks away and summer has not yet kicked into gear. Still more life left in this party yet. If we ever get the boarders open then people are going to start piling in here. Just as property begins to faultier in May 2021, then open the floodgates again, its a sure fire fix. There is no change on the cards as far as I can see. Clearly it doesn't matter who is in government, its just more of the same shit different day.

FLP hasn't even kicked in yet, Orr's going to keep this party going!

Had an email update on past weekly sales in central auckland from ray white. All sales had price undisclosed? What is the point of this? I would have thought in the current market they would want to be advertising the price far and wide

Guess it's at a stage now where prices are discouraging prospective buyers. Prospective sellers may enquire - sale lead opportunity for them?

It’s either a) Agents desperate for business so they ask people to phone in for info so they can be “worked on” or b) The sales prices were not as high as the spruiking suggests.

Government and reserve bank need to improve LVR to 50% for investors, and improve investors' interest rates. Otherwise, only a few people will own all the houses, and other people will just wait for HNZ to supply free accommodations. NOBODY wants to work hard to save deposits for a house because it is UNAFFORDABLE!!

Well, there is only so much cheating the system that the RBNZ can do, and the economy balance will sooner or later reassert itself: once the Covid situation gets under control overseas, I expect that a good portion of high-skilled young professionals will leave our shores as a result of the utterly ridiculous house prices in NZ.

Maybe we will be left with a shallow economy over-reliant on house speculation and with a bunch of boomers selling mostly empty and depreciating houses to each other (PS: I am a boomer myself, so I feel like I can freely use this term).

Look at the prices in the sky. How we can say it is cooling down?! Government and RBNZ need to take action NOW urgently!!

I think the horse bolted - back in about 2013 - now its wild. Trying to tame a wild horse results in injury, meaning the responsible tamers (central bank and government) don't want to go near it.

Here is a new saying, 'Every city/town in NZ is just an Auckland cluster$&%@ waiting to happen.'

'increasingly getting its panties in a twist' - ugh

On the other hand we have a currency that is hitting multi-year highs which is hurting exporters and making imported goods more appealing vs domestic goods. Seems to me that dealing with that problem could be at odds with a cooling of house prices.

Also, if the vaccine really is just around the corner, that's going to throw some more fuel on the fire.

4 more years of upward movement in Auckland prices, no way is it over, 2024 peak.

What value will Dow Jones be by then probably 50k and total bubble

Wishful thinking headlines, just remember even a slight of wind probability or if majority of Economist (which means everyone) forecasting any correction, the opposite knee jerk reactions will be spear headed by the authority. Remember slight spooking house of cards or domino ponzi scheme in NZ? - the whole country will be at risk. Never, happen here.. so to all. Happy investing! - NZ has been promoted worldwide, for single assurances type of investment.

How many times have commentators said this? And yet the price keeps going up and up.

Let's face it, just materials and labour costs alone will keep the prices high!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.