Strong house price growth is now occurring in all major districts throughout the country, according to the REINZ House Price Index (HPI).

The HPI adjusts for movements in aggregated selling prices caused by shifts in the mix of properties sold each month, giving a better measure of overall movements in prices than averages or medians.

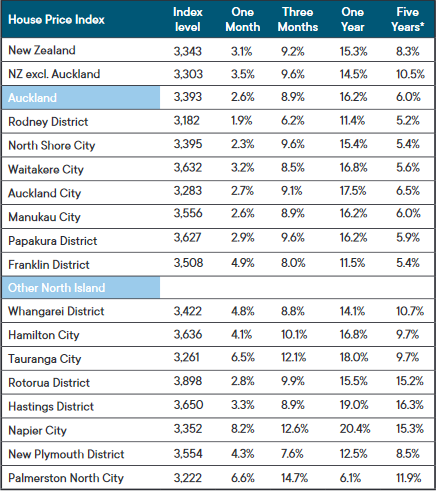

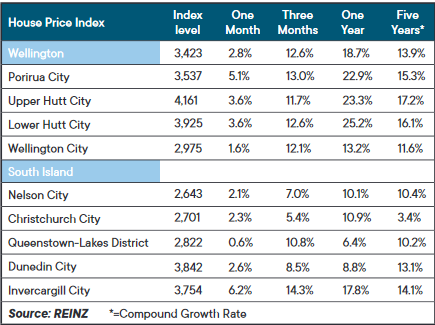

It shows that in the three months to the end of November, prices across New Zealand increased by between 5.4% in Christchurch and 14.7% in Palmerston North.

Of the 24 cities or districts tracked by the HPI, 10 recorded double digit growth over the three months from September to November (see table below).

That would be considered strong growth on an annual basis but it is exceptional for a three month period.

Even the beleaguered Queenstown-Lakes District recorded price growth of 10.8% in the three months to November.

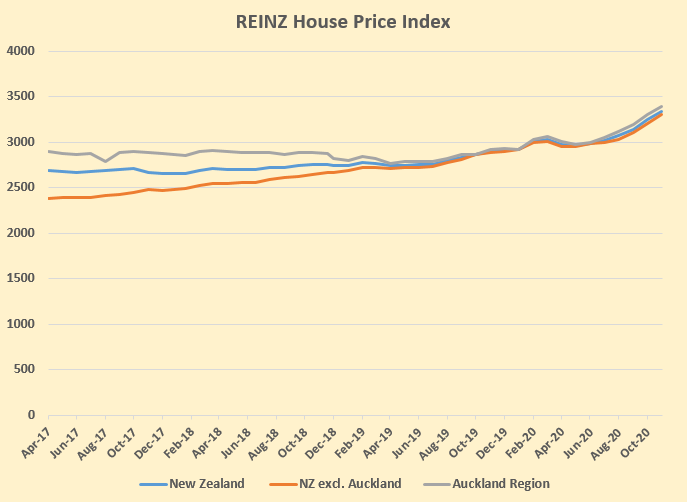

The graph below compares price movements in Auckland with those in the rest of the country since April 2017.

It suggests price growth was higher in the rest of the country than in Auckland up until the middle of last year. But it was then relatively uniform across the entire country, with stronger price growth starting to kick in about May, as the real estate market started coming back to life after the Covid lockdown and lower mortgage interest rates started stoking prices.

The comment stream on this story is now closed.

REINZ House Price Index

101 Comments

When winning lotto will not even buy you a decent house. This is madness

There's you problem right there, Lotto is $10 Million at the moment, so are you telling me a house that is $10 Million is still not up to your "Standard" ? Madness is spending $1500 a week on rent so you can "Impress your friends" so you can live in a house you cannot actually afford.

Winning lotto is $1 million (less if more than one person wins in any week) - winning powerball is the one that jackpots to the multiple millions you are talking about.

Not everyone who wins lotto wins powerball - but everyone who wins powerball has also won lotto.

What Kate said.

C'mon .....stop all this BS talk and do something ! - the 3 actions to take to bring residential property back to from being used as "pension plan" and for houses to be a "home" are:

1. Tax all unused land in urban areas - unless used for horticulture, agriculture etc

2. In all urban areas, where rental demand is high, tax empty houses.

3. Capital gains tax for second or subsequent properties - including the "holiday" home.

What's NOT to like !

Simply the only real way anything will change is if there is a massive increase in supply of homes. Tinkering around the edges with taxes / rules will never really help.

I have two rentals and have made $700000 in the last three years on those plus $400000 on the family home, No capital gain on any as I have had them long enough. I do not feel guilty as doing the governments job for them and providing great housing for two great families.

Any gain from those is for my children to buy their first homes or they can have my rentals.

Stop the whining and get into it people as the more weeks you talk about how bad it is the prices keep going up.

No matter what you are telling yourself house prices will never never never start going down, look at real estate history.

The gains are only gains when you sell.

Prices 100% can go backwards.

Advocacy of charging in, with no pause to regard the general financial health of this country is poor advice.

No asset bubble in history, driven by debt, survives.

To continue recent price gains, consistently, over another 7 years, will require kiwi households to take on more household debt to gpd than basically anything in modern history.

Perhaps the real issue, in additional to debt growth, is that the massive growth in liquidity leading people to realise cash has no value. Cash is now pouring into assets of any kind.

Bordering stagflation?

Keep on dreaming and I will buy another house interest only.

No risk as have 70% equity in my homes together, so will always have a place to sleep.

Hi bzkw2b, can you give details particularly the address of the home you are looking to purchase today . It would be helpful for all Interest followers to have your input and outcome, as you appear to be a seasoned investor.

Stick to Lotto

A member for 18 hours. Curious rant. Remember to take your medication as prescribed. Do it for your family.

Sounds very like a former commenter who got banned. They just cant keep away.

FB "The gains are only gains when you sell."

That is a very common way of thinking, it's also unfortunately one of the most damaging beliefs for one's prosperity. For your own good, let go of that belief

“ The gains are only gains when you sell.”

This the danger when people think this is how it works, those who are in the game know it is almost the opposite. Please people don’t take this idea onboard or else you will get truly left behind....

This

"it is almost the opposite", a very astute observation.

Hi Fluffybunny,

You reckon "Prices 100% can go backwards."

Yeah right...... When did that last happen in NZ?

It's like saying a freight train can go 100mph backwards...... It's theoretically possible - but not too common in reality.

Let's have some sensible discussion. Scaremongering serves no useful purpose.

TTP

TTP, FB doesn't say prices can go backwards 100%, he says that he is sure that property prices can go backwards.

TTP, the very fact prices haven't gone backwards significantly (even the GFC was minuscule) is even more reason they will, its called reversion to the mean. When they will is anyone's guess but the trajectory of house price inflation since they 1980"s is just not sustainable.

2007. The data is readily available if you care to look.

https://www.interest.co.nz/charts/real-estate/qv-house-price-index

Approx 10% drop in prices, with about 5 years to recover the peak price.

Good on you mate.

Really earnt that $1.1 mill in the last three years! How long will it take those without houses to save that amount?

Great that your children will be able to buy houses. What about NZ youth that don't have that luxury and now have the ladder pulled up?

I'm alright, Jack.

I also have two rentals and a family home. They have increased in probable sale price over the last 3 years but far less than yours. Prices can go down and it can happen quickly. For example in 1990 I bought in the East End of London a property for 70k UKP which was being advertised a year ealier at $105k UKP. I bought a new apartment in Auckland CBD in 2007 which they had advertised at $340k for $179K. Note how I'm boasting about my good buying (luck really) but there were two sellers who had made significant losses - you never hear from them.

A drop in the cost of buildings is feasible, a drastic drop in the price of land is likely. My home has a CV of $250k and the land is CV $900k; that latter figure is 90% unrelated to any reality/sanity.

I totally agree that land prices can drop. But i do not see how they are 90% overpriced. A factor that explains a portion of the price (but not all of it) is the cost of infrastructure. Whatever is supplied by the government will cost everyone 4-5 times more than it should. Just look how much it costs to build 1 km of road. Then try to estimate how much would it cost to build a new neighborhood (i.e. develop a land that may worth about $1sqm). Then you can see if you still your land is 90% overpriced or not.

Your points are correct, to a point, and then are incorrect.

At certain points in the land value process, the land price is overpriced by 1,000% plus.

The overpricing comes in the form known as non-value-added costs. These are costs you could take out and would not change the amenity value of the product. So how do these non-value-added costs get to exist?

In short, due mainly to restrictive Govt. policies.

The easiest example is seen is when land is first rezoned to residential. As rural zoned land is worth about $50,000 ha with the farmer grazing dairy cows and on the basis of the purchase, he paid for the land and the operational costs he can sell milk at a price we can afford.

Then the council come along and rezone it for housing. The land has not physically changed yet is now worth $2,000,000 ha. The only reason the price has gone up at this stage is because of how we restrict the supply of residential land, whereas the land available for dairy farms is not restricted in the same sense, and is tied to competitive global milk price. This price difference of $1,950,000 is known as non-value added. It has not added any physical benefit and only exists because of policy constraints. The farmer cannot put up the price of his milk just because of the rezoning.

The farmer, if he was allowed, could have built the same houses without the zoning, but the raw land price would be at $50,000 per ha. Post-development, the land use has obviously changed from rural to residential, but in a nonrestrictive, non-monopoly, free-market the land price would not change. This is what happens in jurisdictions that do not have restrictive zoning and they, therefore, have very affordable housing.

The example I give about the development on the fringe is important because the fringe land price sets the price for all land going back into the CBD. If the land is expensive on the fringe, then it will be a multiple more expensive going into the center. If the land is cheaper on the fringe, then it will be relatively less expensive than the more expensive fringe cities.

Then of course we can do this comparative non-value-added costing all again with the monopoly that the council has in consenting, and for when and how infrastructure gets provided, but it all starts with the land.

Approx. 1/3 to 1/2 the value of housing in NZ is made up of non-value-added costs, ie housing could be developed for that much less.

Even without zoning restrictions, if the farmer was allowed to build lots of houses on that land then the land price would be higher than $50,000 per ha. You're right though that it would be less than $2,000,000 ha.

It would only be higher than the rural land price if it had some other amenity benefit that added value as part of residential development. It could also have some negatives from a residential development point of view, but a developer could not buy it for less than its next best use price which is dairy farmland as the farmer knows he can get at least the dairy farm price for it.

Also if it does not command an extra value because of a positive residential amenity feature, and the farmer wants more than $50,000 per ha, then the developer is free to go to the next available farm that will be for sale at $50,000 per ha. Thus the farmer has to be competitive in his price, no matter what use the land would be used for.

Of course, this only happens in jurisdictions without restrictive land policies, which is not NZ, hence our unaffordable house prices.

But a congregation of housing *does* have a higher amenity benefit than empty land, due to community, business, etc.

Sure you could build some isolated houses on cheap land but most people don't want to live isolated lives. Most people also need to work, and they don't want to spend too much of their time and money commuting.

You are starting to go off-piste with your thinking.

We are talking about the raw land price ie what the land was doing before it was bought to build housing on. So any existing raw rural land amenity that could have a positive value for residential ie for example land that borders or has a lake on it. It may have some water supply advantage for a farmer but will have a far greater residential value for its views, swimming, boating, etc. It is only in this type of situation where it would have a higher residential land value above its present dairy farm value.

The point is that most of the increase in land price bought for residential development is via restrictive land policies that allow both land bankers and councils monopoly advantage so supply is always less than demand. This artificially increases the land price.

And this has nothing to do with some isolated houses on cheap land or commuting time. This has to do with the price of all housing right into the CBD. This is land economics 101.

If you really want to get your head around it. Read anything by Evans https://books.google.co.nz/books/about/Economics_Real_Estate_and_the_Su…

or Bertaud https://www.amazon.com/Alain-Bertaud/e/B001KI1QDG

Plus Hugh Pavletich's website http://www.performanceurbanplanning.org/ has some great reading as does https://www.newgeography.com/content/006693-demographia-world-urban-are…

We've had 3 or 4 months of mania, after a year or so of flat gains re prices.

Total sales volumes are not exactly rocketing away.

Current price Mania driven by the rbnz dumping huge sums of QE cash into the economy, the government underwriting most of the jobs in the country via subsidy. And mortgage deferrals etc.

So any gains now are not exactly happening in a healthy underlying economy.

Business lending, which would potentially actually improve national productivity has fallen off a cliff.

Big chunks of our economy are still out of action.

We (as in the people who are taking bigger and bigger mortgage commitments) are simply borrowing away in order to keep the growth model moving forward.

And to top it off, the people who manage this shit show (Rbnz) don't take into account house price inflation, when try to manage the country's overall inflation targets via the dustribution of all this "wealth"

(that about sum it up? )

I'm not saying one thing or another will happen. I have rich as f*** parents and a rental home also so let's the part continue!

But we could not raise interest rates with a major crash.

At some point we will have to raise rates.

Personally I'm waiting for Brexit to wrap up and Joe to get going before taking on any significant debt.

You have no idea what 2021 will bring.

"doing the governments job for them and providing great housing for two great families."

So you built the two houses? Otherwise you didn't provide jack, you're just playing musical chairs.

And are party to the banks sucking the cash out of the economy.

I do not give a rats, I will look out for my family, suggest you do the same.

You keep on talking and I will keep on gaining, looking at another house today actually and the banks giving me it all interest only.

I am guessing you are a "have not" by the comments, get on with it.

You must be a robot. Any human being with half a heart feels compassion for those less fortunate than them.

I feel compassion but helping people does not mean me dropping my $$$ for them.

Work harder, no difference than any other generation but these young ones now whine more and think the world owes them.

Do not buy a $1500 iPhone and fancy clothes.

Get on with it....

Great show of a complete and utter lack of understanding for far, far too many people in this country. You will not die wondering why I think this whole business is little short of "people farming"

"No different than any other generation" when prices are making more a year than white collar professionals.

But sure, iPhones, avocados, ... whatever.

What about those joining the work force now for the first time in their lives? Not all those can rely on the Bank of mum and dad. Many will leave to work overseas where wages are better, the cost of living is better and houses are cheaper to build, ie Australia.

Really Australia, good luck !

Yes Australia and they are already leaving.

Yes Australia and they are already leaving.

Actually just purchased myself a new Apple iPhone 12 Pro today with some equity on my rentals.

I love property $$$

I am even going to claim the cost and my new upgraded plan against my rental gains.

Purchased a lawnmower, ladder and weedeater the other day, all claimed against the rentals.

Living the dream...and my children will one day from my gains.

Teaching them the business now so they can do it too.

Build more homes, build more homes, build more homes.

Imagine thinking you're doing well when you have to take out a mortgage to buy a phone. Cash flow issues?

Hahaha, read between the lines. Have a nice (large) income thanks. Its called tax benefits numnuts.

I claim everything I am allowed and take it to the max, having a great accountant helps with that.

Living the dream.

Funny how all the great advice/comments that flow on these spam comment sites are from losers with no real idea how to "BE SUCCESSFUL".

And yes I man $$$$$$ but also mean happiness.....I am laughing all the way to the bank.

BUILD MORE HOMES - THE ONLY WAY IT WILL CHANGE - ECONOMICS

Or did you not graduate from high school !?!

I dunno, this behaviour doesn't scream "happy life" to me.

Australia is actually really cheap Brisbane- average house price is $500K, Perth + Adelaide $450K, Melbourne $670K

Add in higher wages and the fact the personal tax system is currently been reformed with anyone earning from 2024 less than $200K paying 30c in the dollar (with a tax free threshold of 18K) - Australia will complete the holy trinity for young kiwis - lower taxes, higher incomes and cheaper houses.

Cheaper food, cheaper petrol and it has a real summer.

dreamtime

You wont buy a stand-alone house with its own bit of dirt within 40 kms of Melbourne CBD for $670k - enjoy the commute

well you cant buy anything within 40kms of Auckland or 30kms of Wellington for under 700K either - so I'm not sure what your point is.

Hmmm, really? https://www.realestate.com.au/property-house-vic-werribee-134535726

That's just over 30ks away for $520k, brand new 4 bed, 2 bath detached. And remember, average wage in Aus = $89k. Average wage in NZ = $53k.

Someone I know bought one of these for $550k even closer not long ago. Being built to his spec as we speak, he's loving it. IT guy earning "in the mid hundred k's" working in the city having gone over last year. We are looking at building an hour from Wellington and it's going to be $1m for similar spec. Basically they don't compare at all, you are the one in dreamland iconoclast.

Yeah you will. I lived there for three years.

https://m.realestate.com.au/property-house-vic-point+cook-134717302

No idea where some of these people pull those prices from, Melbourne used to be cheap like 20 years ago now its horrendous. Its serious spread out and your going to have a massive commute to the middle of nowhere at those prices. Its like saying Pokeno or even Hamilton is cheap then drive to Auckland CBD every day for work.

Have you been looking at a different real estate history to me? The one I'm aware of is littered with instances of prices falling at different times and in different countries. I'm only in my 30s and have lived through a few of these episodes - have you been paying attention?

Not to say that investing in houses doesn't tend to work out alright, but please check your facts.

It's also worth having a little self awareness - for obvious mathematical reasons it's not possible for everyone to own a couple of rentals, and society needs to provide for those unable to afford entry into the market. I'm speaking as someone with a couple of houses, but under no expectation that prices will continue to fly to the moon without any correction.

What do you mean not everyone can own a house plus two rentals of course everyone can.

They're just not working hard enough. Buying to many iPhones and smashing avos on them.

;)

See exactly, as soon as you hear someone say, 'everyone can do it,' and 'prices always go up,' then you know they can't do the math, or history.

"I do not feel guilty as doing the governments job for them and providing great housing for two great families." Actually not only have you provided great housing for two great families, you have deprived two other great families from owning their own home.

Boom and there we have it, the exact reason why we are in the current situation. Amateur landlords speculating on property with monopoly money and absolutely no consideration for the negative effects such behaviour will have on NZ and its population, especially the next generation. Im going to look after me and my own and stuff the rest of you. Having an opinion on a subject that is going to have a massive affect on my kids chances of being able to live in their country of birth is not whinging, and maybe just maybe some of us aren't "getting into it" because we are investing our money elsewhere in productive investments that maybe just maybe will allow our kids to have jobs when they are older to put a deposit on a $12,000,000 do'er upper thanks to people like you.

Perhaps a quote from Aristotle about property regulation says it all."for if both in the enjoyment of the produce and in the work of production they end up not equal but unequal, the complaints are bound to arise between those who enjoy or take much but work little and those who take less but work more."340BC

I guess its not that "cash has no value" but that cash alone is not a very good investment. However cash by itself has been declining in value for as long as I can remember. This reality just seems a little more stark now.

Labour too seems to be declining in value. You have to work harder as a courier or Uber driver to make money. Globalism and the gig economy is eroding the value of labour in Western countries. It's always been a bit shite in non Western countries. You need a degree now to make a subsistence wage so education has declined in value too.

The answer is to invest your money in property, shares or a business maybe. Money needs to be put into property or equities as early and regularly as possible. If you can get about 5% return consistently you should be okay.

KiwiSaver has shown the value of non cash investing although it is a little artificial with employer and government contributions. A lot of KiwiSaver money is now being converted into property assets.

So, everyone takes your advice and invests (presuming you mean more than your own home) in property. Then what? Who pays?

Build more homes, Build more homes, Build more homes, Build more homes, Build more homes, Build more homes,

Everything else is a waste of time.

We’re you kicked off your local property investors Facebook page? You’ve stumbled across the wrong website mate.

No it's absolutely the right website. Interest started with mortgage rates, which is obviously needed for purchasing property. Sadly over the last year more and more righteous non property owners with no experience in buying, owning and selling houses are poisoning the comments section

Give it a rest Yves.

So you're actually condoning this spam dribble Yvil? Why am I not surprised? Birds of a feather and so forth....

This advice is for readers of this website. I was thinking about this after reading a comment on YouTube from someone who had worked in Japan for 37 years and found himself unemployed and practically penniless. He had spent quite a bit of his own money on his students over the years but he should have at least put away 10-15% of his income into equities and would probably be having a much more pleasant time in retirement in Japan. Apparently many older workers in Japan including native Japanese find things pretty tough in their later years. This probably applies to all countries now.

Just got a little div on retirement village shares. So that's another way to invest in real estate. If no dividend reinvestment program offered can just manually buy more shares with recent dividends and keep doing that to infinity. Share price promptly dropped so at least next shares cheaper. Dollar cost averaging. Anyone with $50 or less can buy shares.

Over the last decade investing in the aged care sector has produced capital gains well above direct investment in housing eg Rymans $1.14 in 2009 when I first bought them, $15.00 today. Multiple new sites underway (hence relatively high gearing at the moment), currency risk spread given increasing AUD component and demographic trend ensuring strong future demand. A hassle free exposure to the housing segment with lower risk of political interference than directly owned rentals.

Well done Middleman. Everyone should have some exposure to equities as well as real estate.

Built more homes, Built more homes, Built more homes, Built more homes, Built more homes, Built more homes

Everything else is a waste of time.

I am doing my part for the economy and putting money back in, picking up a new Toyota Highlander on Tuesday (3.5L V6 one) so will enjoy that with my gains and pay my taxes back in with the petrol used. Getting a new Toyota Corolla for my son going to university next year.

Love property $$$$

Built more homes, Built more homes, Built more homes, Built more homes, Built more homes, Built more homes

Everything else is a waste of time.

Forget about buying your son's admiration with a new car. Get him an old thirsty falcon station wagon that keeps him broke and regularly fails a wof. He will actually get some real friends, be happy, and in the long run will be less likely to abandon you in a rest home.

Your doing your part for some other country's economy and just adding to our balance of payments deficit, but hey, don't let that little detail get in the way.

Another import with English as a second language? Or a product of our education system?

Built more homes, Built more homes, Built more homes, Built more homes, Built more homes, Built more homes

Everything else is a waste of time.

Notice I have said Built not Build as it should have already happened but we people in power who do not really get economics.

Troll?

Sounds like one of the former nutters returned.

Has similarity to The Man in terms of lack of empathy for those struggling to get on the ladder.

I disagree most strongly. The Man2 was all about urging people to buy a house as soon as you can in Christchurch and it turns out his advice at the time was good. He really had a lot of trouble understanding why people refused to take his advice as to him it was so obviously the right course of action.

His arrogance, age ,lack of empathy and his inability to spell did not help his cause.

Please explain how TM2's age damaged his credibility.

He is a lucky boomer. No expertise needed. Just bought when cheap. If true could not do it now.

Thanks for clarifying that by virtue of being a 'lucky' boomer his credibility is diminished. I'd be interested to know what other groups you similarly consign to irrelevancy by virtue of their demographics.

Just boomers. Luckiest generation to date. I am one of them. I have commercial and residential property assets and equities that I was able to buy when they were far cheaper than today.

Yes, lucky no doubt. But only with the benefit of hindsight. You will have lived through the trauma of the 80's and 90's restructuring of the economy. Horrific times for many boomers with the casualties mostly invisible given the lack of venues to discuss their pain. Unlike today. Few back then foresaw the inflation that would rescue us and in the process reorder NZs economic hierarchy. Millennials and I gens sneeringly portray our lives as one long easy street, the fearful reality was quite different for a large swathe of the population. Today two thirds of boomers depend on NZ super for their income. 20% have supplementary income, with only a modest percentage owning sufficient assets to make them independent. Hardly the popular image of widespread boomer affluence.

Yet not every "boomer" is wealthy, why not since they were all born at a similar time?

Were you in NZ during the 1987 crash?

Lot of people lost, many got wiped out in 1984 reforms

Then there is marriage break ups

Then there is poor life choices

Then there is attrition due to health, deaths, road toll

Of the original inventory of boomers, not all of them made it through, many didn't

Being born a boomer in NZ was no guarantee to el-dorado

Thank you, "Being born a boomer in NZ was no guarantee to el-dorado" is precisely my point to the silly comments that say "you're just lucky cause you're a boomer, you were born at the right time"

Can this spam please be stopped? He's just posting the same thing over and over again in response to different comments.

Sounds like the governments sustainability goal may be met by depopulating New Zealand of two generations.

"maladaptive behavior that repeats, typically known as repetition compulsion, is one of the primary reasons that people seek psychotherapy. However, even with psychotherapeutic advances it continues to be extremely difficult to treat"

Hang on, 6% growth in AKL in the last 5years, isn’t that normal?

HPI is 6% in Auckland for last 5 years

Not the headline of course that REINZ is putting out. Far more shiny to talk about last 3 months or last 12 moths, which of course will continue in linear fashion, at annualised rate of 36% pa.. Not

Mike. yes, hyperbole makes far more interesting headlines but the negative impact of this type of sensationalism on FHB's has become very real. The RE industry may regard it as simple marketing and I'd normally agree, especially given it's mostly the naive who take pronouncements from the RE spruikers at face value. But the environment has changed with FHBs now suffering widespread, significant and very real anxiety. You get a sense of this from comments here on int.co. It's no longer a game.

The 5 year column is annual compound growth, so an increase of on average 6% per year for 5 years, or approx 34% over the 5 year period.

compound growth rate, not CAGR, big difference!

It seems some people don't get the compound growth rate. Basically thats how house prices have run away from wages. Not only is it higher per annum, some years there just has been no wage growth at all. Decades later here we are, wages have barely tripled and house prices have gone up 15 times what they were so even any small percentage increase now just smashes your pay rise. Even if your million dollar house only goes up 1% a year now its still killing the average wage increase. Just cannot see a way back from here.

Theres more to come! On the one hand local & national politicians bleat on about affordable housing. On the other hand, they continue to impose more & more cost on a new build. Coming additional requirements include - attenuation tank approx. $5,000.00; water garden approx $8,000.00; revised geotech requirements for foundations approx. $20,000.00 & it wont stop there. Builders are getting the blame for new house costs - but they are helpless in the face of rapidly rising costs

I've read many comments suggesting a CGT on everything including holiday home. Why couldn't I buy the family home, my wife the holiday home and my two adult children a rental each. There would be a confidential agreement between us because all four properties are actually mine and paid for by me. Or am I missing something.

Why can't your adult children just purchase their own homes?

Don't think that would work if using the American model. There you have a "Homestead" which is declared as your permanent residence address. One person is only allowed one "Homestead" property which needs to be certified each year. And of course because US Tax policy is always centred around "family income", and not "single income" couples would not split their "homesteads", or they lose the "Family Tax Rate". Same when it comes to Federal Social Security Pension. The lower income earner gains far higher pension by receiving 50% of the pension of the major income earner. Could be the difference between $1000 per month for the minor earner of the couple by filing with a husband or wife versus the two filing individually for their Social Security retirement income.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.