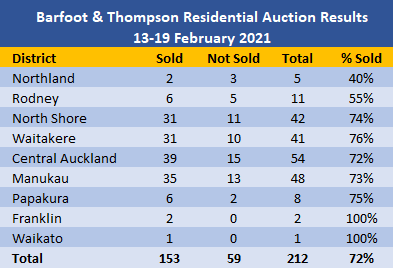

The number of residential auctions handled by Barfoot & Thompson took a slight dip last week, while the sales rate rose slightly.

The agency handled 212 auction properties last week, slightly down from 248 the previous week, but the overall sales rate increased to 72% from 68%.

In the equivalent week of last year (15-21 February) Barfoot auctioned 180 residential properties and the overall sales rate was 67%.

In the major centres of population within the Auckland region the sales rates were fairly consistent, ranging from 72% in Auckland's central suburbs to 76% in Waitakere, while auction numbers remained relatively low in Rodney where the sales rate was 55%.

Where the selling prices of the properties that sold could be matched with the properties' rating valuations, 99% sold for more than their rating valuation.

The table below shows the sales breakdown by district.

Details of the individual properties offered and the results achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to you inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

61 Comments

When are the new RVs updated in Auckland? They're so outdated now.

I can only assume the 1% that didn’t sell for more than RV had some sort of serious defect or was deliberately sold cheap in a family deal.

Even in the first home buyer groups on FB, potential buyers get told not to pay any attention at all to RV as it is a meaningless statistic in the current market.

They were supposed to be revised last year but due to Covid has been delayed to this year.

https://www.aucklandcouncil.govt.nz/property-rates-valuations/our-valua…

Ahhh another housing delay 'due to covid'

RV update not really top priority of council, rate payers, Government (anyone with a pulse) at the moment. I appreciate DGMers are frothing at the mouth as the old "sold below RV = market crash" is getting harder given outdated RVs and Auckland property price increases since 2017. I am sure you can find something else to crow about in the meantime.

Isn't the economy going well at the moment? Do you think it's better to update RVs later when the economy might not be doing so well and then have people pay potentially higher rates? Why delay it?

Rates go up or down independent of RVs. The council desire for mullah determines how much you will be paying, not the RV.

So no harm in updating the RV's now then?

Probably not the best moment to do it now.

It's great isn't it!

Now, everyone that owns a home gets to pay more for the next one they want to move to; downsize their lifestyle as an alternative or just plain stay (financially trapped?) where they are. They get to take on more debt (if they qualify) or tie up otherwise disposable income that might have flowed around the economy.

And that makes us wealthier?

(NB: No matter which way it's looked at, in aggregate New Zealand is taking on more debt, and the capacity to repay it - future earnings - isn't increasing at the same rate. That, my friends, makes us poorer, not wealthier. Debt doesn't matter - until it does)

Its how our monetary system works mate, its called new money creation through debt. The other article here on interest has new record lending on houses which equals more money in the system. Yes it makes home owners more wealthy, that's the bottom line. You don't always have to trade up, there comes a point in your life where you downsize and take the beans off the table.

Have you actually tried 'trading down'?

It's surprising how few beans are left on the table for most people once the friction costs of moving and the replacement cost of a new place are deducted. (a 5-bedroom house costs little different to a 3-bedroom house. I know. When I was building the cost of an additional set of bedrooms etc was relatively small. That's' why people, like I did, build larger rather than smaller.)

And all that 'new money' you talk of? Where's it gone? It's gone right back into the same asset class it came out of! Trapped back in the property ( and other speculative asset) markets.

It hasn't made it out into the real World to 'do good' - make us wealthier, if you like.

All it's done it put two changed numbers on the national spreadsheet

One says "Gross Debt, Up"

and the other shows "RV, Up"

The actual result to our society isn't offsetting though; zero - it's negative.

its called new money creation through debt

Incorrect. The debt is created from the money being lent into existence.

In govts mind paying $100 for a loaf of bread probably makes us wealthy

More money for the baker, and a beautiful expensive loaf for us. Ponzi finance is the way forward!

That's why the situation right now is not benefiting anyone except for the people who are moving to a retirement village or moving to a small town to retire. You bought a house right now? So what? Still need to pay off huge debt. Sell your house? Yes you get some capital gain. But you will be back to your rental. Might never catchup property ladder again. Upsizing? Be ready to take on more debt. Downsizing? If you want to live in similar area, don't know it's worth it or not.

.. and we will continue to see worse outcomes for poorer NZ'ers.. despite bandaid measures like rising min wages and increased accom supplements. Jacinda still thinks property prices should trend slowly higher, asnd no politician will touch it though until its worth their while.

The property Ponzi scheme is underwritten by ever increasing liabilities on the taxpayer, as the government desperately tries to close an equality gap that is becoming a yawning chasm.

RV's now well out of date. The new RV's down here in Tauranga are due out in July so its going to be crazy increases, probably the biggest increase I have seen to date in the order of $150K on your average property.

WooHoo!

The Statutory Mangers of Council Affairs will be able to charge all the ratepayers (aren't many of them retirees?) more rates to live in the same place! Guess what those Ratepayers will do - spend less on other things. How's that for 'stimulating' the local economy!

(NB: The recently sacked elected Councillors ran riot; spending like there was no tomorrow. How many tens of millions was spent on the downtown, multi story car park building that has to be torn down before it's even been finished? Or the leaky building that used to be the Council Chambers, likewise to be demolished; or the new road works in Greerton, that was some Councillor's idea of how to make traffic problems worse than they were before the expensive 'fix' or the Wharf Street "Eat Street" conversion (done 3 times!) that is like a ghost mall 99% of the time, and on and on it goes.)

bw

Yet again.

RVs simply determines one’s share of Council’s total rates take - it does not affect the total rate take.

Total rate take is determined by Council budgeting process.

If one’s RV increases by the city average, ones rate bill does not increase other than by Council budgeted increase.

There is no increasing Council rate take or an individual’s rate bill simply because RVs are up.

Never let the truth get in the way of a great rant.

HeavyG

I agree - lots ranting not understanding.

Wasn't the proposed rate hike for Tauranga an increase to their budget-take

The individual annual hike of 12% will be the home-owners share of the New Budget based on RV

Exactly right. How confused is he

Don't worry Carlos ...if the CV goes up $150k average most of the "sheeple" will think that is "money in the bank" and just go out and buy more property with the extra equity .....crazy times indeed !

Just read an article by Robert Gough about how you can get yourself a $1.4 million dollar mortgage based on the equity you have in the original property you bought...with a mortgage -

‘In order to get finance approval on a $1m investment property - a surprisingly common price bracket in Auckland, Wellington and Tauranga these days - an investor would need a deposit of $400,000.

It’s a common misconception that investors need that money sitting in their bank account - ie as cash. Home-owners can use the value in their own property to borrow this deposit, essentially meaning they are borrowing 100% of the purchase for the new investment property (40% on their own home or other investment properties and 60% on their new property).

Home-owners can borrow up to 80% of the house they live in. For example, a homeowner in a home worth $1 million and with a mortgage of $400,000 could borrow another $400,000 against their own home (up to 80%) and use that money to buy a $1 million investment property for a total mortgage of $1.4 million ($1 million for the new home and the original $400k they had on their personal property).’

How is this news? Its why speculators will always have a massive advantage when competing with FHBs.

It makes no sense to update the CVs at this stage, it would be a one sided game, unless you are on that side of course which would make you pretty happy.

b21

What is your reasoning for it not making any sense to update RVs?

Note: In the HB, CoreLogic issued new RVs for Napier CC late last year, and in Hastings DC I think earlier in the year.

You know exactly why, which is the reason why you replied to my message ;)

b21

I’m not being obtuse - you have made a statement which wasn’t really clear nor with rationale and I’m genuinely interested what you mean and the reason.

I really though it needed no clarification but here it is: Increasing CVs in an overheated market will just add more fuel to the fire. The reason is that owners will see realized potential capital gains into an official document which will potentially push asking and auction reserve prices.

b21

I take your point.

Note one can already virtually get the same data on a couple of very common algorithm based apps - Insights and One Roof which are determined in much the same way (based on compatible sales) just as CoreLogic determines RVs. And of course CoreLogic provides this real time information as well.

I suspect many have looked at these apps and have a fair idea of the current value of their properties.

Interestingly here in Napier while all are pleasantly shocked at their estimate, three sales I am closely aware of have gone for quite a bit more than even theses. However the reality for homeowners is that of course it is about having a home and they are not in a position to realise their capital gains.

Makes no difference to my point, none of those are official sources and merely estimates by private companies likely to fluctuate with the market. On the other hand the CV is a sample in a very specific point in time, taking such sample at this point will be harmful.

No it wont. Anyone relying on a rateable valuation when determining the price they would pay , or accept, as consideration for the sale of a house is a fool. Similarly, comparing sales prices achieved with RV for the property will provide no useful information as to the state of the market. Much better to look at HPI (https://www.reinz.co.nz/residential-property-data-gallery).

Furthermore, trying to cook the books by only updating RVs when the property market drops in price is not only stupid but also unethical. RVs are used to determine the share of the councils rate charges required to be contributed by a property owner. Using them as a substitute for a registered valuation is ridiculous.

Last CV review in Auckland was made at the peak of the 2017 inflation run before prices were flat and even down for quite some time, doing another review during an inflation run would be unethical indeed.

HG

Totally agree.

b21

You are incorrect that it is harmful “taking a sample at this point of time” - that is not what CoreLogic did last year in determinin Napier RVs during which time annual inflation was around 20%pa, nor Gisborne, again last year, when house price inflation was 30%pa.

Note that CoreLogic for RV purposes don’t use “a very specific point in time” - their data is over a three month period to avoid short periods of volatility. And keep in mind the purpose of a RV - it is not to determine the “actual real value of a house” (you pay CoreLogic $600 for that) but rather a comparable value to other houses for the sole purpose of determine an estimated value for equitable rating purposes.

When calculating RV CoreLogic uses it data which is taken over a three month period. That is exactly the same three month data they produce every month. I suspect that One Roof possibly uses REINZ monthly data (which although potentially volatile is the most current and therefore “accurate” during periods of very rapid inflation) whereas Insights may possibly use CoreLogic as their data seems less volatile and a little behind OneRoof. Of course CoreLogic will be using the same data set that they use to generate RVs . . . although I suspect they consider a great range of individual property variables when doing so.

That wasn't what I said. You should spend at least the same time reading the messages to which you reply as you spend writing yours, might save you some embarrassment in the future.

b21

What?

Not only read your comments I quoted them. “Harmful”? ‘Sample”? “Unethical”? Your words and I read and referred to them!

b21 3.09pm: “CV is a sample in a very specific point in time, taking such sample at this point will be harmful”

“Specific point in time”? – no, three-month period. “Sample”? – no, all change in titles (sales) registered with LINZ. “harmful”? – CoreLogic (much like RBNZ) have no responsibility for the market, just reporting on it.

b21 3.59pm: “Last CV review in Auckland was made at the peak of the 2017 inflation run before prices were flat and even down for quite some time, doing another review during an inflation run would be unethical indeed”.

CoreLogic did so last year in determining Napier RVs during which time annual inflation was around 20%pa, nor Gisborne, again last year, when house price inflation was 30%pa. Possible, done, and not harmful nor unethical (as no responsibility for the market).

Whew!

HDC was August 2019.

GC

Correct - it’s just that time flys when one is having fun.

This housing situation is so "crazy" neeeigggghhhhhh !! ...even this "crazed" horse is seeing stars !

While I chew on my breakfast of oats, I'm now pondering on just how high they will go ..... ?????

Looking over this cacti filled dry valley, they just have to keep going "to the moon" as if they stop, there will be no more of 'dem capital gains ......whoops ! game over ...........

they might one day shut the stable door but only after horsey has galloped many a mile

Just don't bet the farm.

Poor old JA, copping it again.

Is the government also busy with COVID today?

Of course, any excuse. SACK the lot of them.

All day, every day. (p.s. please don’t mention the housing crisis).

BUY NOW OR NEVER

Consider this paper released today by NZ Initiative- though my company had already worked this out years ago, this is the first time a public oriented organisation has worked on this in this manner.

In one of its 36 simulated scenarios for the next 20 years, even if NZ completely shut its borders (zero migration), it would need to build 20,000 homes annually to keep up- and that's on top of demolitions, replacements and the current undersupply!

This is the type of checkmate that makes Garry Kasparov waking up, breaking in sweat every night.

All prospective property buyers should now consider buying everything and anything- they can always trade later.

The price propulsion is powered by a nuclear plant, it'll take forever to run out of fuel.

Get in quick, you will be very very rich.

Summary page: https://www.nzinitiative.org.nz/reports-and-media/reports/the-need-to-b…

Report link: https://www.nzinitiative.org.nz/reports-and-media/reports/the-need-to-b…

Better hear the author talk about it. (Assuming your message is ironic)

b21... Leonard is saying that with zero immigration we need to build 20K houses PA just to keep up. He seems to imply that because this is a difficult task we do not need to consider (and worry about) how much more difficult it will be to build the far more house we will need if we continue with the madness of mass migration. Basically he is try to argue that because we have an issue that is a challenge (or a problem without migration) that we should blindly continue to compound the problem by massively adding to demand through immigration. He is correct, zero migration would not solve the issue on its own (and we need to take action that is unrelated to immigration) but zero or very low migration would make the issue far far more manageable and less destructive for our society. Leonard Hong, shame on you for framing your interview and your paper in such a pernicious way. The way that people like yourself, Ashley Church and Tony Alexander twist reality does immeasurable harm to our country, in particular our poor. And Martin North is also culpable, albeit to a much lesser extent, for not nailing you to the wall on this during the interview. Again, shame on you. Your words (and reports) have consequences.

CWBW... so how many houses over and above the 20 000 do you think we will need to build just to keep up if we return to the "100K+ migrants a year" policy?

If you bother to read the report, you'll realised that without positive immigration, it will be worse.

CWBW... yes the report says that even with zero immigration it will be worse THAN NOW. But it conveniently does not cover how much bigger and more serious the problem will become with immigration.

CWBW... so to summarize his 58 page paper. With zero migration it will be a massive challenge to build enough houses for everyone. If traditional levels of immigration continue it will make it absolutely impossible. However, this paper will focus solely on the supply side and the implications of our immigration settings on our housing crisis is not in the scope of this paper (even though the effects of immigration are very large and very problematic).

Could have beaten you in 3 games of chess in the time it took me to read it. LOL

Contrary to what you think, I believe the solution to the housing issue is more immigrants. YOLO

YOLO El loco.

Owner occupier LVR reinstate = T - 5 days.

142 listings (new today) added on RE NZ already

So, person who corrected me other day appears correct that listings more numerous in mid week, thanks

On Monday at 11am it was only 69.

On November 5th (a Thursday) it was 256.

So, I will check on Thursday for comparison between high listing seasons

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.