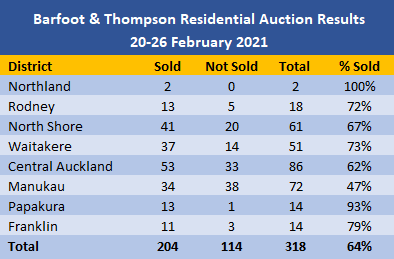

There was a big jump in the number of properties auctioned by Barfoot & Thompson in the last week of February, while the sales rate took a bit of a dip.

The real estate agency handled 318 residential property auctions in the week from 20-26 February, up by 55% from the 212 the previous week, and more than double the 151 properties the agency auctioned in the equivalent week (22-28 February) of last year.

Of the 318 properties auctioned last week, sales were achieved on 204, giving an overall sales rate of 64%.

That compares with 153 sales the previous week (sales rate 72%) and 85 sales in the last week of February last year (56% sales rate).

Within the Auckland region sales rates ranged from 47% in Manukau to 93% in Papakura (see the table below for the district breakdown).

Details of the individual properties offered and the results achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to you inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

64 Comments

MikeKirk

No evidence of that 18 February downturn. :(

Mike Kirk

It was cloudy last night. I couldn't quite see the planetary alignments.

18/2/22

Auction rooms are crowded, real estate agents are talking and laughing. Successful buyers almost cry, finally relieved from watching the ever-decreasing trademe list. Those who couldn't compete for prices that high need to downgrade their expectation and go back to the next search.

What needs to happen is rapacious, blood sucking behaviour of property "investors" need severely curtailing

Printer.

Please go back and refer to EXACTLY what I said about February 18th.

I said it represented the turning point of the market.

Are auctions the whole market?

The market is slowing (re listings) by about 15% cf November.

Market in terms of sales will not start declining til May.

Noice that I have prev detailed that the drop in sales from Dec to January is usually 27% and was this year, 46%

That is, market has peaked.

Hence my referring to the turning point. No crash was predicted.

Biggest impact on market will be economic as bond market and inflation undermine efforts to keep interest rates down on open market

Also it represents Turing point for the economic cycle and inflation, all of which in evidence as bond market in turmoil and ALL now talking re inflation whereas 6 months ago no one said a word about it and laughed at those who did.

There's plenty of evidence the bubble which started in August 2020 has run out of steam, REINZ numbers have been dropping for 2 consecutive months and deals in Auckland CBD apartments will make FHB consider that option, will likely positively affect the regional entry level segment helping with affordability.

Whether this positive trend will continue will just depend on how the Government and RBNZ continue manipulating the market in favour of home owners.

I've noticed a surge in listings in Wellington actually, which is usually chronically low. A friend mentioned open homes at the weekend were quiet too (at least the ones he attended).

That said, it's difficult to get hopes up anymore. I'll believe it when I see it.

Visited a 6 open homes in West Auckland this weekend from which just two could one say that were busy. My impression is that frustration not being able to save for a deposit has become more important factor than low interest rates. It could as well be that the pool of buyers which happened to be able to secure a deposit due to the change in conditions by the RBNZ (which has just been reverted) started draining by the end of the year.

I'd say the listings are creeping up in Wellington. The surge was surely just the second half of the summer market kicking in. I didn't go to open homes this weekend (couldn't face it) but weekend before still seemed pretty busy.

Euston Rd Wilton had a line down the street

Interesting. Though Homes has it down as a cross lease at 60m2 for $570k - $655k. At least the lower end is active. Prime investor and FHB territory.

My mate was looking at more typical 2-3 bedroom villas over $1 mil. Possibly it's the upper end that's tapped out?

2 bedroom villas are now 1.1, 1.2. There does to be a ceiling of sorts though in that you basically start paying 150k a bedroom after that. so you can get that large 4 bedder for 1.5, if the bank lets you get up in to that range.

Oh stop it Mike, you were predicting the RE market to go down in February 2020

Yes he was.

The market was going down in February 2020, maybe you didn't notice something that happened since March last year?

BS, I predicted in September 2019 that the market would reach a new high in March 2020, which it did, your post is incorrect

It was... and then the fix went in

Nope, absolutely incorrect

Hi mikekirk29,

Suggest you pay homage to the time-honoured wisdom.......

"When you're in a hole, stop digging."

TTP

Not going to be silenced by your narrative contributions pal

Yvil was correct but even he didn't back himself 100% and took a dollar each way bet and sold a house thats now worth $100's of thousands more. No point looking at the past guys its the here and now that matters and the future is looking like inevitable gains for at least the short term anyway. Anyone now predicting a crash would be viewed as coming from the looney bin.

I'm surprised the LVR's seem to have no effect at all so far (banks said they will implement the tougher LVRs before March)

Same surprise here. I wonder what I am missing. Perhaps another quarter for things to work its way through the system? Head scratcher for me.

Perhaps that restriction does not apply to the already pre-approved loans.

Or Many buyers have more than 30% deposit, therefore less affected by the tougher standard.

Or many investment buyers ran off to the small banks and 2nd tier lenders that didn't implement LVR restrictions. But they only have so much capacity for lending, its just going to take a bit longer to see the slowdown.

Restrictions did not apply until just today, I have been saying for quite some time I know for a fact banks were not as tight with new loans as they used to say and this is proof for those that didn't believe it.

As government and Mr Orr does not want the ponzi to stop, so the very reason of all the options they introuduced only LVR was, that it will not have much impact now.

Never underestimate the shrewdeness and cunningness of politicans and people in high places. Thick skin @#$#@ (on behalf of FHB)

LVRs are meaningless when the equity increases in property portfolios alone in the last year mean no additional cash deposit is needed for new loans. I got property this way and most existing investors can leverage their portfolios... wait maybe your comment was sarcasm because it was plainly obvious mainly FHB would really be affected by LVRs in a rising market. Most property investors can practically ignore LVRs.

I'm surprised that you still surprise that nothing will affect NZ housing affordability, it's the way it is the past 20-30yrs. Surely, you've figured out by now.

Not much differ to terminally ill patients, the result always the same. Or if you want to add to world living certainties: Death, paying taxes.. and NZ housing cost.

Collating historical and current listings and weeks of inventory points to continued pricing pressures, without any consideration of current mortgage or OCR settings.

Out of curiosity, where do these people get their money? NZ is such a captured market that people are OK to spend insane money on things that would otherwise cost lesser elsewhere.

Why be surprised. If Jacinda Arden and Mr Orr wants the house price to rise in double digit on a monthly basis if not weekly basis so be it.

Enjoy and Borrow as they have more to worry for your debt than the person taking it as it us their future at stake, if the ponzi crumbles so chill.....

Correct, Government and RBNZ have more to worry and lose (their reputation and face) than individual taking debt, if individuals were to default.

Jacinda Arden and her team has allowed themselves to be cornered and by not acting are digging bigger hole for themselves. As far as Mr Orr is concerned, he is aware that will not be reappointed so is doing all that he always wanted to do under the excuse of panademic before quitting as is not answerable to people, may be answerable to government but government lacks understanding and as are ignorant lacks guts to take him.

They won't stop until NZ is a gulag of economic and medical tyranny

1/ They won't let the ponzi crumble easily. They will pile up an obscene amount of debt & destroy our currency before they let that happen.

2/ If the ponzi does crumble, all those who are swaggering around now going "Loadsa Money!!" will be braying for a bail-out. And they'll get one no doubt.

3/ We are stuffed.

Auckland, no better place to live - in lockdown every second day, harbour bridge collapsing, water shortages, sewer filled beaches every time it rains... Worth every cent at auction.

I hear the harbour bridge has 10 years left in it and all heavy vehicles will now have to divert through the upper harbour to avoid the bridge. Not sure how this information was allowed to get out and was not gagged. Forget about a second crossing, there will be no first crossing. Even if they started building a new bridge tomorrow, how many years will that take ? This country's is starting to have more to worry about than just Covid, the infrastructure is falling to bits.

Plenty of time for a public transport upgrade. There’s are huge stretch of water called the waitemata with no traffic on it and doesn’t need a bridge.

True we could probably get some of those great old sailing ships going back and fourth to the North Shore to transport people to work, all very green and should lower our carbon emissions significantly. If they are a bit slow for you then you had better learn to Kitesurf.

If you were listening to the same interview as me he said we won’t be needing to redirect heavy traffic for several decades yet. They will just need to continue maintenance

The prices are just totally insane. If they think this is going to lead to more spending in the real ecomony, I tell you, it's going to be the exact opposite. No one will be spending. OCR needs to go up..fast and hard..NOW!

Sad that many people can't do basic sums and figure that out. Grant Robbers-son even believes that a house price increase means the owner can spend more (wealth effect)

As long as there are no bail-outs & no taxpayer subsidies, I don't care what this confederation of dunces does. I see people lecturing others that they must downgrade their expectations. How good is property! Again, as long as there are never, ever any bail-outs then it's very hard to begrudge these financial geniuses their wonderful gains.

Agree but government and RBNZ have put themselves in a situation where have no choice and RBNZ governor has got the opptunuty of a lifetime to play under the exvuse of coronavirus.

Earlier one accepts better that govt and rbnz will always support the ponzi entire NZ economy is linked to housing

The great profit Mike Kirk is wrong again! What will his legion of DGMs feed off now???

Let’s guess. You are up to your armpits in mortgage debt? Sorry to say that rubbishing Mike ain’t gonna affect the outcome.

Yeah far better to be vaporising money on rent and never owning anything...

That’s why you’re all on here commenting day in day out hoping for a miracle

Another idiot who assumes I rent. Mortgage free +++ and more.

And yet you’re on here continuing the DGM narrative what a sad state of affairs that is.

Everyone is vaporising money. Some are bank/debt slaves and some arent. Personally I gave up on buying a house, I just do not see a million plus bucks in a worn out 1930s bungalow on 400m2 of dirt. Doesnt particularly fill me full of confidence.

Learn to spell

Surely this has got to cool at some point soon?!

it’s an overheated market filled with overly eager investors. More and more investors are buying up any property they can get their hands on with a decent yield. They jump on in, as does every other person with a bit of equity (anyone who owns who brought more than 6months ago).

Soon enough inventory becomes scarce. S**t it’s already scarce. When there is F all to buy then prices rise even more rapidly (hello 2020). These prices are too rapid to justify or support that the property/asset is worth what’s being paid.

Some of the investors who started buying 5+ years ago then realise that the prices and current trajectory is unsustainable. They start selling, maybe only 5 initially. Then Bob from down the road heard how Tom started selling so he sells a few too. Other investors catch on and start selling a few too hoping to still make bank. Fewer people then want to buy in a falling market hoping for even bigger falls, especially those who have been saving for 8+ years, what’s another 6months or a year to save 20-30k. For the ones who entered the hyped market too late, they will suffer the most and in this case it will most likely be FHB (which is devastating).

I hope the market gets the opportunity to correct itself and there isn’t more money printing and lowering of rates. I don’t think it will “burst” but I do hope that the bubble gets a little smaller and more manageable for FHBs.

This has been my take of the s***show for the last 3 years.... nothing’s changed except higher prices though. So maybe the minute I start saying prices are going to skyrocket, that’s when it will simmer.

From what we're seeing the temptation to sell is too great for some long-term investors, just not nearly enough to meet demand (at least in Wellington) so prices continue to rocket

Not many investors sell their properties. Those that do often regret it. Investors are faced with similar difficulties to FHBs when buying as well as having to make financial sense so good rental properties are not that easy to find.

What temptation to sell? Where does the money go once it’s been sold? It’s actually the exact opposite and no investors are selling and never will while rents keep tracking up over time and they have a nice income stream and larger and larger capital to leverage off.

Property investors don’t sell they accumulate everyone seems to know that apart from a few clueless posters on here

Our landlords have 20+ properties 3 of which they sold earlier this year. They’re an elderly retired couple and their words.... “we want to live a little before we don’t live”.

I guess you aren’t always right, Lord Downer.

Yeah it has to cool, the problem is that it never really drops does it ? Even small gains now on $1million house totally outstrips wage growth.

Another good factual reading:

https://www.stuff.co.nz/business/opinion-analysis/124385961/new-zealand…

Some section of world communities in the past believe that the Earth is flat, Sun orbiting the Earth, day only consist of daylight or night time.. couple members of those communities move out to avoid whole absurdity.

So when the great pandemic is over and people are working their way through financial challenges - the question will be asked ..

So NZ what did you get up whilst the world was in lockdown and how productive was your financial packages at supporting future industries/alleviating poverty/social injustice and greening..

Oh well.. You know the way we like taking on Aussie debt and selling each other houses.. We just did that but in overdrive

Another sign of economy performing well, 2020 NZ defy all normal gravity. NZ has proven with the world. No matter how long it is to lock down the border? reduce of economic activities.. in the end? it's all about supplying the phantom numbers to all companies, banks etc. Worry about downturn of profit?, close your eyes.. then the next day.. The reported/forecast of account spreadsheet number can be added at will.. even the profit.

NZ has shown the world how to do it, the rest of the world will follow with these forever stimulus... results?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.