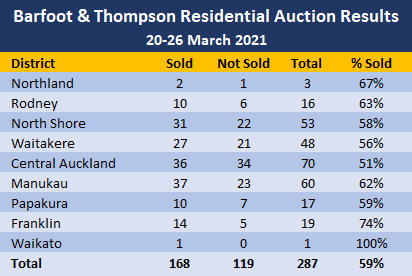

The number of residential properties auctioned by Barfoot & Thompson dropped back to 287 last week (20-26 March), down from 305 the previous week but still well up from 226 the week before that.

On Tuesday of last week the Government announced changes to the way residential investment properties are taxed, but it is too early to say if that is having an effect in the auction rooms.

Last week's dip in auction activity compared to the previous week was not unexpected as the peak summer selling season draws to a close and the overall sales rate of 59% was barely changed from 61% the previous week.

Unfortunately it's not possible to draw a comparison with auction activity in the same week of last year when the country had just gone into level 4 lockdown and there was very little sales activity taking place.

Around the Auckland districts the sales rates last week ranged from 51% for properties in the city's central suburbs to 74% for those in Franklin on its southern flank (see the table below for the full district results).

Details of the individual properties offered and the results achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to you inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

89 Comments

The housing market and house prices destined to remain resilient.

What's new?

TTP

DGM destined to remain pessimistic.

What's new?

TTP

trite. adjective. (of a remark or idea) lacking originality or freshness; dull on account of overuse.

Things is with this new tax policy, it almost seem like they are indirectly allowing “negative gearing” again, just in a different form.

Nothing will change.

But being 'ringfenced' I'm not sure how the negative gearing is beneficial. If your 'business' can make losses for the duration of its existance then its a terrible business. Or very 'tax efficient'...

Time to buy more properties, rented out, increase rent.. OZ banks will be there to spread the wealth plan.

Soon, (hopefully) the new player/Chinese banks will establish in Aotearoa, another good cheaper credit channel towards new migrants land grabs, wait, pop up the price then re-sell to the next compatriot expat to solidify the segment market... in NZ branch.

BGM/Bright Glitter Merchant destined to remain optimistic, not even stadium4 cancer and painful torturous chemo can turn that around.

Investors moaning about not being able to deduct their interest only loans?

Yeah forgetting massive capital gain...

I find it absolutely laughable when investors say that they are doing good, providing a much needed home to NZ'rs like they do it from the goodness of their hearts.

- When the new requirements for warm, dry homes came through they winged and moaned to get their property up to standard.

- When the interest rates hit rock bottom , I did not see any landlords decrease their rents.

- When paid off their mortgage, did they reduce rents?

- When they sold homes, did they pay income tax?

None of these happened? They are doing nothing out of kindness, they don't care who has a roof over their head. All they care about is money. The ever ending desire to make money at others expense.

The government should cut off the accommodation supplement, lets see how many homes hit the market. The government can buy them and have them as housing NZ homes. Landlords take and take and take and take. It was never about ethical home ownership and has always been about greed.

Great points. Last week it became obvious the huge amount of resources the lobby has in comparison to other collectives, including think tanks, mass media and would not be surprised if they would also have social medial commenters on payroll. They have been quite vocal about what they want and even threaten with passing the cost of having lower returns to renters.

Interesting piece related to this from RNZ

https://www.rnz.co.nz/audio/player?audio_id=2018789167

A few years ago the air force housing at Whenuapai was assessed by the government/ housing new zealand as possible future housing. It was deemed substandard so they did not buy them. This area has now been completely redeveloped and makes up part of the Hobsonville area. I would imagine, having visited friends at Whenuapai and seen the low standard of housing there along with houses at the upper end here in the Eastern Suburbs of Auckland, that the government WOULD NOT buy the majority of rot boxes from landlords should that issue ever arise.

So tell us how you really feel lol. Landlords are investors, as in, they invest their capital for a return. If it offends you that they did not invest for social good (as I am sure you have otherwise you would be a hypocrite) that is another matter and not sure where you came on the idea that they should? Is that not the purpose of Governments?

Lol. They don't really invest their own capital though do they? Interest only speculation with the risk underwritten by the government.

Leeches.

Another silly comment, of course you invest your own capital, collateral from another property is your capital and if you default on your mortgage all properties used for collateral are at risk

I would like you to read my first sentence with a bit more care if you can. I said "I find it absolutely laughable when investors say that they are doing good...". I am directly talking about these landlords who act all saintly and are so emotive about how much they care about putting roof over people's heads like they do it out of social need and claim that they are providing this service where the government has failed etc etc. Government provides social housing, landlords don't. It is as simple as that so I have no time for those playing Mother Theresa.

PS - they don't invest capital. They leverage equity on their own home, without paying any capital, use interest free terms with banks for 3 years, then shift to another bank to continue interest free terms for as long as they can and sell at a bumper profit and not pay tax. Yeah I am telling you exactly how I feel about this unethical practice. Absolutely disgusted!

I appreciate your opinion and indeed investors who want to virtue-signal as a saintly are tiresome.

Being able to leverage your capital is a simple business activity that most businesses do, its not unique to property investors. This mechanic is as old as business and has been going on for thousands of years.

The scheme which you are disgusted by was enabled by poor legislation, this regulation should be the target of your disgust surely?

Thank you for the appreciation and yes I have been disgusted by the poor legislation for years and wrote to John Key and Bill English back in the day and have written to Jacinda and Grant in the recent years with my opinion on poor legislation. Perhaps it is one of the reasons why I am not having a bar of investors moaning now that there are provisions being made.

With that all being said:

When you take all the fruit and not contribute to the honestly box in front of you, does not make it poor of the person who didn't police the honestly box. It shows the character of the person who takes them without paying for them.... Just because the government legislation is not up to mark does not mean you should swindle your way through the property market. Honesty and Integrity is so lost in the society these days.

You forgotten, most of the ruling elites both parties, local councils CEOs, RBNZ team - mostly, are the investor.. to build up wealth, to reach where they're now, the vested interest was in subconscious. Will let you know the secrets; by the time requiring expensive terminally ill medication? shhh.. almost all of them queue for public hospital service, and ask for the med subsidy.

The only thing left now for all those essential workers? is to do prolong roll over strikes, not just yelling and stop work one hour with placards asking for car horn too toing. But simply, just stop work.. try the minimum of 12wks full.

When all that is left really 'nothing to loose' further.. then, why not? - oh but wait, OCR, LVR, DTI, CAR, TD deposit, Unemployment, Housing.. are all being pass on to RBNZ (independent xixixi). Soon after all those massive roll over strike, govt plan to pass on the law to RBNZ too firstly, to print extra wages to 123% to entice back to work.. but by then? housing won't go down by 55%.. but instead? yip, you guess it.. difficult, delicate, supply, no CullenCGT (the person still here right?),.. it will be following those wages percentage increase.. magical link.. only in NZ.

Destined?

"resilient".

Define your terms.

Housing market, presumably including sales as part of that generic term?

So, if sales fall off from peak, does that imply market is not so "resilient"

is market you refer to in Auckland, NZ or NZ excluding Auckland?

"LVRs put brakes on housing market, as prices drop 4%"

https://www.oneroof.co.nz/news/39162

Not much can be read into these short term figures but the cynic in me wouldn’t be surprised if OneRoof massage their figures to try and deter the government with following through with their recent policy announcements.

How are these figures different from those from a month before which nobody questioned? Oh wait, prices are DOWN.... 4%!!!!!

Real Estate lobbyist are good at spin and fibbing the data or news to suit.......

Stop it, if the articles say prices are up you complain that the RE article is spin, if the article say prices are down you still say it's spin. It's really silly talk

They spin it in both direction to suit their narrative at that time.

Too much spinning gets you dizzy. Stop defending what's not defensible, makes it obvious what you do.

"Makes it obvious what you do" What kind of a silly comment is this, I'm not ashamed of what I do. I own 3 businesses, I employ people and I invest. What do you do that is so noble that you think you can judge me and others?

I could not care less about what you do or if you happen to be Jeff Bezos himself, but you just provided proof that you make your comments out of a position of privilege so no surprise you keep defending lobbies and the usual suspects around here. I am in no position to judge you since I don't know you but even though I could choose to do the same I am comfortable with saying my comments are not written to support my own personal interest.

I'm hopeful the govt isn't taking policy direction from Ashley Church

Hmmm, interesting, March is usually stronger than February. It's actually quite a good article (if we look past the silly anti RE comments). The drop is also widespread to all regions, whatsmore the drop is clearly before the latest government announcement about tax rules for investors. I previously stated there will be a significant slowing in sales and cooling in prices but I did not expect it to happen already.

Hi Yvil

a measured response.

My basic is that market was in mania and factors causing that have now largely been braked.

Also, reversion to mean suggests, as usual, that sale sand prices could not continue at that lick, so will inevitably fall back.

Only question now, is not whether or when, but by how much.

A large piece of this may well be what HWI are choosing to do and how much risk they see in different asset classes

Pretty much as Mike Kirk called it, albeit a few weeks off.

by printer8 | 1st Mar 21, 1:01pm

MikeKirk

No evidence of that 18 February downturn. :(

by B727 | 27th Feb 21, 11:22pm

Mike Kirk said price increases have already peaked so I guess we have that?

by B727 | 1st Mar 21, 8:18pm

The great profit Mike Kirk is wrong again! What will his legion of DGMs feed off now???

by B727 | 1st Mar 21, 8:18pm

The great profit Mike Kirk is wrong again! What will his legion of DGMs feed off now???

Perhaps Mike Kirk is a great 'profit'...or did he/she mean 'prophet'.

Well, well . . . there you just go.

So it seems that the housing market is simply all to do with the planets as Mike's basis was Saturn and Uranus aligning up somehow.

Who would have believed it? I'm absolutely in awe.

Looks like we all have to follow astrology sites now - one can be right one in a hundred times and its absolutely nothing to do with chance.

He'd make a great bank economist P8!

Hi Printer,

I take the humour in good heart.

Just so you know, the planetary alignment is Saturn square Uranus.

it occurs every 12 years roughly and last one was in 2009.

Also, due to retrograde motion, it occurs (exactly 90 degrees) 3 times in a year.

18th February was first time (the turn, as I referred to it)

Next one is in mid June, when proper fall off in price ACCELERATION will occur, and also greater fall in sales and listings

And yes, that will be approaching winter so no surprise (except that last year turned that truism on its head)

It is interesting that SA_UR square is symbolic of government and private sector being in conflict, which well describes what gov just did to investors.

But the peak was already in b4 the government intervention and that had nothing to do with astrology as much as reversion to the mean.

Sensible folk do not rely solely on one club in the bag

8014..One Roof are probably just trying to head the Govt off at the pass and try to reduce the chances of more sensible action. "See it is working. We do not have to ban interest only loans and unoccupied homes". Like a detective, when it comes to One Roof, always look for a motive.

There's still plenty of cheap money available. There's still a shortage of houses. There's still heaps of people looking to buy. Nothing is going to change until interest rates go up or tens of thousands of houses are built.

Exactly Sam but only ONE of those solutions can be implemented at very short notice.

Or we get high inflation!

You don't understand, they just made interest only loans not attractive for investors anymore which is the main way their "business" can work. 1) they cannot deduct a considerable part of it and 2) extending the bright line test means many will have to start paying mortgage principle which is usually more expensive and from which they cannot deduct anything if they want to avoid paying capital gains tax. This is the actual reason why they have been moaning non stop and so loud for the past week.

Yep place just sold on the weekend in Pt Chev for 2.7 mil, 3 bed.

FHBs can keep waiting and wishing that thier saviours labour are going to get them a bargain while watching rents climb and prices going sideways at best.

Depends on which place and how good you cherry pick.

Auckland HPI since Feb 2017 up 26.8%

Median up 33%

Rest of NZ excluding Auckland, median up 57% in that 4 years

NZ as a whole also 57% up in 4 years.

Auckland since July 2020 up 19.8% on median. or 2.83% pcm

Nov - Feb up 6.78% or 2.26% pcm

Total Sales in January and February in Auckland were 5% LOWER than in 2020 by the way, not that you hear that in MSM. In NZ as a whole they were 16% lower

Auckland residential sales were up 37% in those 2 months.

Which suggests that land sales took a hit

By the way REINZ reveals that in the 3 years to October 2019, prices in Auckland FELL 2.3%

So, prices do go down but not by much

So many contradictory stats & statements with little to no fact.

"Little to no fact" ?

Price rises are slowing and so are sales.

And, it is late March, and now Pollyanna brigade will say oh well it will go back up in May.

Not this year.

Listing per day rate on RE NZ been falling also.

Most of the time its worse than that, stats stats stats then drawing the wrong conclusion !

really.

SO, what is your view and what is it based on

Do not even bother, a lot of views on this website are not based on facts but the source of personal income.

Mike all data points how screwed first home buyer is and still government is not treating it as an emergency and acting instead of waiting for advise and further announcement.

Nothing new ...had mentioned today morning :

Barfoot's auction today in Manukau will highlight that all this noise till now was and is just a distraction to stop government and RBNZ from firing the silver bullet ( Nearest possible) to stop Interest Only Loan.

Buyers fatigue (temporary) should not be confused with latest announcement - though good but meaningless till government and RBNZ targets speculative demand, which for some reasons are silent after a passing remark in announcement and their intent reflects that is to avoid and delay though accepting the importance of restricting Interest Only loan to contain speculative demand.

https://www.stuff.co.nz/life-style/homed/real-estate/123635705/market-l…

Surprising everyone along with government, be it opposistion, economist, experts, media.....are silent for know that it can be a real effective tool and as many if not all deep into interest only loan, do they even want to raise the issue or highlight it for fear of government actually targeting it ( conflict of interest).

https://www.stuff.co.nz/life-style/homed/real-estate/123635705/market-l…

https://www.interest.co.nz/news/109739/suez-canal-reopens-us-factories-…

IF SERIOUS AND WANT TO TACKLE SPECULATIVE DEMAND - STOP INTEREST ONLY LOAN.

Why no discussion on it or avoiding taking action. Why and for what Mr Orr and Jacinda Arden waiting for....passing the bunck as both are not serious about controlling SPECULATORS as they are main pillar of this housing ponzi = NZ economy.

Mind you with this action FHB and genuine investors will not be affected but will be a disaster for speculators.

Please tell Jacinda Arden that have no silver bullet, agree but in absence of Silver Bullet why are you ignoring the next best bulllet.

Next time if she talks about No silver bullet or waiting for advise or will announce ......stands exposed as soon as she utters this words should be booed out.

Watching Barfoot's auctions live online right now. Of 14 auctions so far, 10 sold and 4 passed in. My maths ain't great but what's that, about a 70% sales rate? Seems ok to me...

Some really abysmal numbers in those results, wouldn't like my property to be sold by auction which actually explains raising numbers of sales by negotiation these days.

As I mentioned above, DGM are destined to remain pessimistic......

Sure enough, that lot are quick to prove I'm correct.

TTP

What can a cheerleader do except for cheering? No matter how bad it looks like always pretend it's up.

By DGM who are you referring to TTP - its hard to tell now if its the landlords or the FHBs. Both seem to be whinging in equal quantity....'my poor interest deductions' or 'houses are still too expensive'.

Everyone except an agent is now a DGM. In fact if you express any thought about the property market that deviates from the OCD totalitarian autistic line "everything is fine and always will be and property equals prosperity in a vacuum with no real world complexities or consequences" definitely you're a DGM.

Its really just a term used to troll people - so was odd that darklords used it so regularly to troll their own customers...i.e. those people who rent and can't afford to buy. Not sure many other businesses where you troll the customers and expect them to come back for more business. Odd country we live in.

Do we get the feeling that we are being watched from across The Tasman, to see how our little experiment goes?

Economists told the Financial Review Banking Summit that surging property prices will raise the prospect of tighter regulation and the reform of tax incentives like negative gearing.

https://i.stuff.co.nz/life-style/homed/real-estate/124692627/national-h…

Jacinda Jacinda where are you ?

When is next announcement for future announcent

Interesting that article must focus on that precisely today we got numbers showing the positive effect of LVR restrictions pushing prices down 4%.

Barfoot auction live - selling price as strong as ever before and will be till pipeline of cheap and easy fund supply though interest only loan is not stopped - main source of fund to multiply purchasing power use by speculators.

Nope. There are shedloads not selling.

How time flies.

Happy Easter everyone!

Listening to Kerry McIvor on the way to work this morning Newstalk, a young woman called in and complained that she is currently already paying 5k per year out of her own pocket to cover rental expenses on an investment property she bought. I was absolutely staggered. This is before any tax changes kick in for her. Surely she is only paying out of pocket on the expectation capital gains. Either that or she became familiar with basic addition and subtraction only after purchasing her rental 'investment'. Kerry was silent throughout the girls monologue..probably as amazed as I was by the foolishness of this poorlord. Left me wondering on what basis the banks have been lending, solely based on equity? Do investors have to show the bank how the rental property will pay its way before they get the green light on the loan?

"Do investors have to show the bank how the rental property will pay its way before they get the green light on the loan?"

Obviously not !!

She was just in it for capital gain and she is just one of many. It is great to see the landlords moaning. People only moan when they are hurt. I have to take it back. Labour has finally done what they said they would do and they will not stop here if prices do not rock back in some way. If there is any evidence of unreasonable rent increases then look out. Labour is in the mood to sort out what is in fact a dangerous situation in our economy.

They won't learn though. Likes moths to a flame

She may not be out of pocket if her rental expenses include principal payments. We have been over this before with you guys! Principal repayments may be $200 a week so the tenant was paying off $100 and she was paying off $100 or her loan. Quite a good way to save some money with a small business. However Labour are now going to make her pay the full $200. In actual fact the tenant will pay that $100 to the government instead of to her now. So tenant will now be no better off, probably a bit worse off as landlords look to at least make a bit of money, even if it is just 20 or 30 dollars a week.

Comprendé?

What do you think is going to happen to that young lady when interest rates go up and tax deductability down. No tenant in the world will be able to fund those kind of expenses. I feel sorry for the young ones getting roped in by old ponzi pumping boomers. Pumped and dumped

Interest rates could also go down. If she hangs in there and doesn't panic things will likely work out over the long term. May have to spend a few years negatively geared even.

Not happening. Globally central banks are already doing what they can to hide the inflation already there.

The only reason why rates are not increasing now is because the Feb is choosing to protect its bonds market.

All I would like to say is that we subsidized our two rentals to start with for about $200 a week, which we could not claim back, the two properties that we have as an investment, we pay tax on the profit that is made which then goes back to the government, there is another reason for taking away the interest tax deduction, the government will be squeezing so much more tax out of the property investors, to help pay for this pandemic

You're not 'subsidizing' anyone but yourself. You're buying yourself an asset, that (presumably) you couldn't afford to buy outright. The fact that not all of the cost of purchasing that asset is covered by the amount you can rent it for is a result of your own choices (choosing to buy a property for which you needed a mortgage, for example).

The working taxpayers subsidise your rental yields to the tune of more than $3billion per annum, only counting direct subsidies. Meanwhile, investors are also freely allowed to pretend they didn't buy for capital gains, to evade taxes.

You are not hard done by.

If you want to drop the house prices, it's simple... Increase the interest rate from 2.29% to 6% overnight. Heck, why not go to 8% while we are at it.

Instant house price drop by 15-20% drop. Housing crisis solved (just only a lot of pissed of home owners), and I'm not even a politician or government official. Thank me later!

Interest rate could nor rise, now but they can stop easy n cheap flow of money used by speculators - Interest Only loan.

that's exactly what they are going to do in two months....

move 40% of investor loans from interest only loans to principal and interest....

you aint seen nothing yet!

I think you need to be careful what you wish for because any increases in cost will be passed on to renters. There is currently nothing to stop rent increases is there ?

This is fear mongering

They are fooling as have not intent and are just trying to buy time to delay if cannot avoid.

Interest rates are tied to global movements. They move when our dollar dictates it (the fed).

Movement of that magnatude overnight by just the nzd would 100% rip apart our little economy.

At a global level if done now, the fed would not be able to afford to repay its debt without printing levels of money multiple times more than current levels. Remember the whole pre ww2 Germany thing?

Best thing nz can do now is govt policy to reign on debt, and hunker down for the hurracaine that's coming up.

At some point people will loose faith in the US treasurys ability to print endless cash, either that or the dollar will be allowed to fail or we switch to a new reserve.

This is just the beginning.

20-30yrs upright trajectory record, even JA uttering that housing increase is to be wrap around.

OZ banks are the ultimate, cheap credit issues that cannot be controlled by both RBNZ & govt.

If OZ export the undesirable characters to NZ, nothing can be done to prevent it.

Since OZ export mostly to screw NZ, then why not young prof qualified NZ citizens just move across the ditch? no brainer really, in turn? used the build up capital to prop the NZ ponzi, it will be paid by .. new rich migrants.

Niness, March 13th: "Auckland market may have peaked in February"

Westpac March 3rd: "current boom in one sense has already passed its peak"

Max auctions was last week in February according to Interest co nz survey : 389

So, the "prophet" looking to have less egg on face than some expected then....

I wonder how many folk on here want (and predict ) prices to fall and how many expect and predict them to rise, this year? of course, many are not in double camp of wanting and expecting either way.

But simply on "expecting" I would say UP is about 6 people and down is about 15, with rest not frequent contributors and of no opinion either way.

I'm happy to see house prices continue to grow, but I'd also like to see a considerable market correction.

Have seen spectacular paper gains on my OO property, but I have relatives and friends who are struggling to pull a sufficient deposit together.

Auckland new listings Tuesday 23rd March: 126

Tuesday 30th March: 116

Record sales in Jan and Feb resemble xmas spending where people borrow from future and pay back in Feb/march, resulting in a dip.

Ie, what happens is people load up in some months and then do not buy in later months.

This is what happened July-Feb. Now we will see the inevitable reversion to the mean.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.