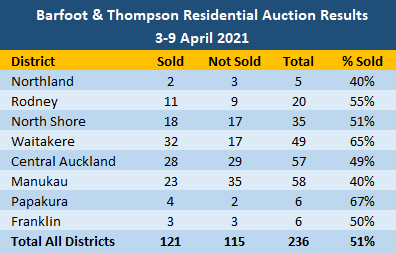

There was a significant drop in the number of properties auctioned by Barfoot & Thompson last week but the overall sales rate remained just above 50%.

Auckland's biggest real estate agency handled 236 auction properties in the week of April 3-9, down from 310 the previous week and 287 the week before that.

Of those, sales were achieved on 121 properties, giving an overall sales rate of 51%, down from 53% the previous week and 59% the week before that.

It was the fourth week in a row that the sales rate has declined at Barfoot & Thompson's auctions, which were commonly achieving sales rates above 70% a month ago.

Last week only two districts had sales rates above 60%, Papakura at 67% and Waitakere at 65%, while the sales rates dropped below 50% for properties in Manukau where 40% were sold and Central Auckland where the sales rate was 49% (see the table below for the full breakdown by district).

Details of the individual properties offered and the results achieved at all of the auctions monitored by interest.co.nz are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to you inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

61 Comments

Ha.... classic to see National pinged for undeclared donations from Barfoots....

Who would have guessed?

With Mr Luxon having seven houses and the party needing the donations....can’t see National lifting a finger to help other than lifting their middle finger to young New Zealanders....

Just reading up on the old John Key aspiration of NZ becoming the next Switzerland of the South Pacific (re another story on here today) and what flashed across my eyeballs from 5 years ago?

John Key... is frankly unapologetic about the massive increase in Auckland residential property values, which has resulted in many established Aucklanders becoming relatively rich, but younger people being locked out of the market.

Some things are harder to change than others.

https://www.nzherald.co.nz/business/fran-osullivan-keys-vision-switzerl…

And was not long after that he called it a day as PM, under PM Bill English house prices stabilized in 2017. Since then Labour was elected by Winston to increase house prices far more than JK ever did. My mates 2 bed crosslease ellerslie house value has risen over 250k since late 2019. It is the classic fhb house but now worth nearly 1.2 MILLION. Jaconda has done more for boomers than for millenials

What an epic betrayal of young Kiwis John Key pulled off, given his campaign rhetoric in completely the opposite direction:

https://www.scoop.co.nz/stories/PA0708/S00336/key-speech-to-new-zealand…

Over the past few years a consensus has developed in New Zealand. We are facing a severe home affordability and ownership crisis. The crisis has reached dangerous levels in recent years and looks set to get worse.

This is an issue that should concern all New Zealanders. It threatens a fundamental part of our culture, it threatens our communities and, ultimately, it threatens our economy.

Such a shame he seemed to have merely lied to New Zealanders to get into power.

The ballhead who looks an an escapee from Paremoremo and owns truckloads of properties wants to be PM. I can't see that working out somehow.

Is a ball head someone who is follicularly challenged? Because I have been called a ball head and retain a good mop of hair. Is it my right leaning, boomer privileged pedigree that earns me the moniker? Wishing Chris all the best, anything is a step forward from the Greens and smiling teeth.

So no housing shortage last week then?

If Jacinda Arden is sincere, should curb inerest only loan through rbnz - removing it now will go a long way, not only now but in future also to curb speculative activities. Perfect opportunity but both rbnz and government does not seem to want to control so most probably will come with excuse instead of closing unfairness that PM talked about between the investors and fhb.

I don't understand why that would be the case. An interest-only loan reduces how much you can borrow. To my understanding, you only use interest only because you want to pay down non-deductible debt before deductible debt, it's a tax strategy, not a buying strategy. But that nuance is out with the new lawe change.

My concern is government subsiding yield:

If investors purchase properties for prices which amount to negative yields after repayments, rates, insurance and policies handed down by the King (NZ Government) - who takes responsibility?

Property in NZ is already heavily subsidized through; accommodation supplements, working for families, underfunding of infrastructure, suppression of the Cash Rate, etc.

I think investors are often being negligent.

Personal responsibility needs to be rightly FORCED on investors for the risk they've taken if it all goes tits up. Otherwise NZ society will start becoming South Africa.

All infrastructure maintenance and growth, and consents, and services connections should be covered by property rates. That would put a dampener on property prices and also apply the burden to those who benefit from the economic growth in the community... the landholders. Right now Auckland council takes $5billion in revenue yearly, only $1.5billion is from property rates. $400million of which is spent immediately on maintaining the $10billion debt burden.

Double or triple property rates and levy them against land values. It's really simple. 3% LVT for property rates, and we'd solve this housing crisis in a heartbeat.

Asking older investors to pay their own way is just obscene. Unconscionable!

I'd be surprised to see data showing most investors run negative. Even if you buy a negative rental, once you discount the future rent increase back to today, they are positive. This is the same way a company making no profit can be worth a ton of money; discounting future expected income back to today.

Seen far more bumpier landings at Wellington airport. :)

59%

53%

51%

next week?

frazz

We wait and see with interest.

Early days only, yet so far no signs of a crash and lots of carnage.

Still expecting a flat market over the next few years at least with some possible minor fall especially over the winter. I am expecting RBNZ not to take imminent action on DTI and IO loans. But used to the wife telling me that I'm wrong.

I forecast growing carnage as investors start having conversations with their accountant's - looking at the numbers, then quickly ringing the real estate agent (which goes to voicemail).

She's a smart woman, your wife...

MTP

Yes . . . she married me. :)

Great comeback P8 !

You don't see an international financial crisis occurring in the next few years? We are due for one.

If you do see one occurring, do you think the RBNZ have sufficient ammo left to prevent a crash?

Fritz

I agree.

An international financial crisis is quite possible . . . as with another significant event such as a conflict which will be equivalent to Covid.

I grew up in an era when the terms depression and recession were regularly banded about in the MSM, and the "Great Depression" and WW2 were deeply impressed in the minds of older generations.

The past two or three decades have been remarkedly stable - and RBNZ have minimised the impact of the GFC and Covid through monetary policy and yes, their powder is seemingly now in short supply.

It is for this reason I often refer to being prudent - one needs to protect oneself from adverse situations.

I don't believe in the simplistic term "safe as houses"; however in the event of a serious calamity - financial or otherwise - then I would tend to think that housing in NZ is likely to be safer than other areas of the economy. One is more likely to see stocks and businesses more severely hit and in some instances disappear but there will always be a need for housing. Yes, I am aware of the housing bursts in the USA, Ireland and Iceland. However NZ housing was not adversely affected in the GFC as, despite criticism of them, our banks tend to be more regulated, and conservative and prudent.

But watch out; it may not be the financial crisis that gets you . . . . it could be the big red bus when crossing the road, or any one of other numerous risk factors in life.

New Zealand has the highest homeless rate in the OECD - RIGHT NOW. Also we have some of the most unaffordable housing in real terms, IN THE WORLD.

I respect you comment and points, yet they seem a tiny bit unconsidered in light of these facts. Going forward, outcomes will MUCH depend on the decisions of the King (Labour Government) over the next year-and-a-half.

Franky, in policy terms, Labour have a year-and-a-half to make changes - then there's a year (or less) for the public to evaluate the past 6 years of Labour's reign, until the next election. I doubt many people will vote National.

The only hope for NZ is Act and TOP. Both parties have different, yet coherent economic policies/visions. I'd be happy with either course.

Act or TOP is a really interesting dichotomy. But I think there’s a lot of sense in what you’re saying. Both would approach it from two very different directions, but in a principled way that would likely result in a good outcome. Currently, the two major parties are in a centrist stalemate where despite the wails of their stakeholders nothing really changes and TPM, the Greens and previously NZ First are beholden to special interests only.

Primary needs, like food is more important as well as Health. When big natural disasters strike, current manipulated shelter needs still seek refuge even to a temporary/make shift shelter. Begging for food ransom, can't eat/drink $, and surprise.. for health still need to get it from somewhere/someone for help. BTW, OZ banks are really more prudent in OZ as compare to the NZ bunch.. that's why the cartel in NZ lobby so much against CAR, TD guarantee and bit shy to do independent fact finding commission .. oh yes, forgot they're.. conservative & prudent, so much so can be seen by the current average loan risk debt exposure ratio..ehem. - It is indeed more rewarding to put accurate timing of Cancer spread prognosis, rather than.. easily manipulate vested interest view of what life is all about.

100%, hopefully! As Reserve Prices recognise the icy winds of change are upon them, and they reflect that.

"First out, Best out" and all of that.....

Orr better cut that OCR ASAP!

He can cut it, but has to bring on DTI, scrap IO, hike LVRs to 50% cash only.

Oh God I hope so. I really want to be able to say I saw a negative OCR before the end.

The banks have spent all that money getting their nerds to change interest rate fields to handle negatives - would be such a pity to waste the effort.

Mate just sold his finished but not amazing villa in Newtown for 1.5 plus a nice chunk of change. 20 bids. Most around 1.5. Still plenty debt out there ready to buy.

That is Wellington for you. Open home queues down the street. Agents are saying Wellington is the new Auckland. Jacinda thinks only Auckland has a price problem as she saw an open home across the road from her house

Jacinda was just humble bragging.

Plenty of overpaid bureaucrats to stoke the bubble in Wellington!!!

With generous maternity leave options, it's a no brainer!!!

A p22m2 section in Foxton sold last week for $360,000.00. This in Foxton-not Remuera! Yes, there is still a lot of money looking for a home!

Orders to Orr from his masters - slash LVR and OCD

Its going down, down, down.

Under 50% next week.

NZ Biggest Ponzi schemes be taken down by the red team.

Well done team from all New Zealanders.

What great leadership.

You could have been this good JK

Term deposits dropping at $3b a month too....

Only forty eight more months before the tank is empty....the prop stops and you nosedive

Can’t keep interest rates low for too long

Where are all the term deposits going?

If the money is pouring out its not going under the mattress with those numbers so its going into........assets like houses. I guess there are unintended consequences to interest rates falling and those with money that can see the housing market rocketing.

Interest Only loan should be stopped only to contain the unintended consequence but by not acting on interest only loan, it seems that it is not unintended but intended consequence with face of unintended.

Quick drop the OCR

If the interest rates on TD's get any lower its all coming out and being spent on a new Porsche. May as well enjoy it before everything goes to hell in a handbasket.

There is a scene like that in "On the Beach" as the radiation reaches Melbourne:

https://en.wikipedia.org/wiki/On_the_Beach_(2000_film)

"Osborne races around the Phillip Island Grand Prix Circuit and finally crashes his car at Turn 10, resulting in a fiery death."

That movie was one of only two I have seen that I regret watching - truely shocking.

The other was Melancholia:

https://en.wikipedia.org/wiki/Melancholia_(2011_film)

Take my advice - don't watch them, even if 10 year bond yields hit 15%.

RE lobby active and is covered by all main street media (as supporting as is free content - not paid ) :

https://www.nzherald.co.nz/business/new-zealands-new-housing-policy-is-…

https://www.newshub.co.nz/home/money/2021/04/call-for-govt-to-allow-ded…

Never seen all media channels going out at the same time in support of average Kiwi and FHB.

Pressure and blackmailing by lobbyist is on for govetnment to backtrack on tax change and if not atleast try to stop other measures in pipeline - DTI and Interest Only Loan.

PM has an opportunity to reset the advantage that investors have over fhb and than let game begun with no interfrence by providing level playing field to all.

Remove interest only loan

Agree that interest only loan should also be removed as Jacinda Arden said that she wants to remove all advantage that investors have over FHB and interest only only is BIG advantage as it multiply the purchasing power of Speculators over FHB.

It does not matter, if house price is high or low, interest only loan should go for level playing field for all TO BE FAIR and Jacinda Arden believes in fairness.

It will be a shame and social crime if Jacinda Arden backtrack or hide behind any excuse or rbnz.

Are you 3 identities all one and the same?

I suspect so...

At this rate of decline my property might crash back to what it was worth at Christmas ☃️

Percentage of success may be declining but house prices are still high which does not help FHB :

https://www.oneroof.co.nz/news/39249

Sales and price growth rates next few months are expected to slow as we enter the slow season. Using the data this month and the next few as a gauge on policies or contractions and there will be multi-collinearity error.

Refer to the annual trends to infer seasonality.

The Labour camp isn't that dull after all.

Agree are smart to create smoke and deflect.

Real Shame that had an opportunity to rise as a leader and change NZ - reset that everyone is talking but alas greed prevents ...

Total sales in Auckland March 2020: 3999

Total sales in Auckland March 2021: 4137

Now consider that a week of March 2020 was hit by lockdown.

Sales up 3.4%

last 3 months down 1.47%

3 months prior to Xmas average was up 37% pcm

The mania is over.

Reversion to mean is upon us.

Expect further drops in sales growth between now and June, when should be back to normal average sales rate of last 12 years.

Price? Well, that depends on consumer confidence and inflation, as well as the investors impact.

Everyone guessing but I expect prices to only rise 7-9% in rest of 2021

People should be a lot more wary of projecting 3m growth of prices and converting it into an annual rate.

Ditto GDP

Yes, interest rates are the elephant in the investment property. One positive side effect of the tax changes is that it might make many people who are over leveraged get out now before 6% mortgages totally ruin the equation. Three rates hikes at least in the next 18 months seems to be widely anticipated.

Anticipated by who?

I'm curious about this... Why would Orr raise rates?

The RBNZ seems to prefer to "look through" any inflation that is supply driven. And we're not getting growth from our monetary policy.

Obviously we're a price taker vs. the US Fed...but I struggle to see us raising rates. Seems like we're just going to put more and more people on MMT welfare alongside property investors.

your assuming it will be the RBNZ who lifts the OCR and not banks who lift rates because wholesale funding costs are rising. Another bank has lifted term deposit rates for 12 months today and HSBC raise rates last week on 12 month fixed terms so it looks like the banks are starting to move even if ORR sits on his hands

Thanks, useful insight.

an investor mate of mine who has 6 rentals, 1 freehold, the others highly levered mentioned he will have to sell 1 in the next year or 2. I wonder if this will be the same for other landlords . . . .

TOdays auction results were staggeringly bad. Best result was 54% sold the worst was 30% - just 6 out of 19 - dozens were passed in with no bids - and this occurred across all the rooms. The later in the auction a house went on the block the less bids it attracted. I think we may have reached a buyers market with these sort of results

One more week of devastating clearance rates, watching 5 properties myself, all went to auction and none sold last week, now all have asking prices or go by negotiation.

You are wasting your time selling by auction these days, agents of course will try to convince you since it is in their own interest.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.