Activity continues to cool in Barfoot & Thompson's auction rooms as the market heads towards winter.

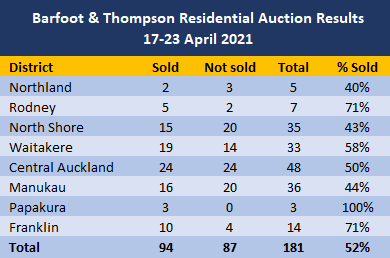

Interest.co.nz monitored 181 residential properties auctioned by Barfoot & Thompson in the week of 17-23 April, down from 269 the previous week (10-16 April).

Of those, sales were recorded on 94 properties compared to 122 sales the previous week.

That gave an overall sales rate of 52% in the week of 17-23 April, up slightly from 45% the previous week.

It is not unusual for auction activity to start to quieten down in April, with March usually being the busiest month of the year for the residential property market.

The timing of the Anzac long weekend is also likely to have affected auction activity last week.

Within the districts where at least a dozen properties were offered at auction, the sales rates ranged from 43% on the North Shore to 71% in Franklin (see the table below for the district-by-district breakdown).

Details of the individual properties offered at all of the auctions monitored by interest.co.nz and the results achieved, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

37 Comments

In today's auction - Barfoot sold 15 properties out of 36 properties that were in two room from 10am to 12.00 noon for Manukau region in Highbrook.

Though sale percentage is low (appox 42% but same as last week for Manukau as per above data) but few houses that were sold, went for top prices and it did not reflect any downturn or slowdown in house prices.

Also possibility of some houses being sold just after auction or in a day or two.

Another 31properties in Auction from 1pm.

52% sold is a sign of healthy market considering properties get sold about half the time based on the sellers' asking price.

It's a sign of a very sick society considering the gap between what people earn and the asking prices for housing.

The "market" is mentally ill.

When this article says the properties that did sell went for healthy prices, i was observing the bidding live and was gobsmacked at the absurdly high prices bid for extremely average and quite elderly properties with just about zero quality attributes. I guess some people do have more money than brains still.

Who are buying these houses. Unlikely FHB's. Unlikey retirees unloading TD's.

Unlikely downsizers.

Possibly upsizers with cash

Punters and speculators ?????

Two otherguys for that very reason RBNZ should act on speculators.

Anecdotal but a mortgage broker I know who's been in the game for long enough to know says he's never seen so many people breaking and refixing long term at the moment. This whole situation is fascinating and you really get the feeling a bunch of people are going to lose their shirts in the next couple of years.

7 sold out of 21 so far at the Central Auction room sales today. Some bids seem to be one buyer vs the sellers reserve. Not sure why you wouldn't walk away if you were the only bidder and negotiate later, or wait until next week when it will be cheaper still. It doesn't look as though the auctioneer is enjoying herself today.

Yes, I've seen this many times, and I've also seen the amount of pressure the agents put on that sole bidder to raise their bid - it's terrible. I've felt like standing up and shouting, "Don't listen to them, you're the only bidder. Stop now and negotiate later". But they keep going.

Do Ray White publish their auction results anywhere?

Simple the announcement from labor was late and ineffective to reduce house price by any means. The prices are now at a benchmark where it will not go down easily, bad for FHB's.

People who waited will have to wait for longer until interest rates go up substantially, which doesn't seems to happen in near future.

FHB are screwed either way. House prices are not coming down and interest rates will be going up. Even if house prices dip then increasing interest rates just take up the slack. Financially you will be no better off each week, your mortgage repayments will be the same. You still need to have the long term vision and a decent salary to get started.

I agree that there is a strong relationship between asset prices and interest rates.

If mortgage rates increase notably, prices absolutely will come back to planet earth, and without the speculative froth it may be a more violent correction than many anticipate.

I think you are partly right. Interest rates will be going up in the next year or so, house prices are already on the downward turn. Anyone who bought in the last 12 months should be nervous. Still some silly bids being made. Buyer beware. I am an owner occupier and would be happy to see my house value fall by 25%. I have no intention to borrow against it and the value is meaningless if you want to buy again in the same market.

Carlos' point was, I quote "House prices are not coming down"

That is why he was partly right, he was right about interest rates but I think he is wrong about house prices. I could have worded it better.

I’d love to see house prices come down.

But in what world do interest rates go up. Our government is up to their eyeballs in debt. The Reserve Bank has been buying the govt debt through large scale asset purchase. The largest asset class in the country (circa $1.5T) is reliant on price appreciation and low interest rates.

Unless the reserve banks remit changes to crippling the country. They’re not going raise rates as it will bankrupt the govt and the only thing keeping the economy afloat (property). because as a nation we’re a one trick pony.

Very smart comment mealsonmeals

I think you’re right. And everything will be done to keep interest rates low for as long as possible. But inflation is beginning (everyone except central banks can see that). By next year, it will well and truly be underway. And if it catches fire, the central banks will be forced to act and they will probably act too late but with a “least regrets” approach where they detonate the equivalent of a monetary nuclear bomb. This will take some time, but 2023-2024 for sure will be interesting.

Agree. There has always been inflation well above the 1-3%. The problem is CPI is flawed as a measure of inflation. It also doesn't factor in any asset price inflation (ie housing) among others things. I'm not sure there are many out there that feel their cost of living is only going up 1-3% or feel it's getting easier to be a FHB. Conservatively, it's more like 5%+ (housing, power, avocado on toast).

Indeed. 2023-24 is also when the banks FLP funding will mature so will be an interesting watch.

They have an alternative to raising interest rates - they can restrict credit.

Do you guys care to share any substantial arguments why prices are not going down? I can give you a few to support the opposite, such as that the FOMO which caused the spike in prices due to reintroduction of LVR restrictions is over plus investors are pulling off the market after recent tax changes. These are two very important factors we should not forget when making predictions, but you guys seem to say just what you would like to happen instead.

"FOOP" new acronym. Fear of over paying. It's being noticed here and there.

Couple of theories. Prices aren't "going down" because vendors are not at a stage where they want to accept reality, and as you say likely an element of existing FOMO surging forward. Depends on how long the FHB backlog is.

A sale has a price recorded against it, a lost sale doesn't. If only there was a way to measure the "spot price" of a property, i.e. the price at which a property that fails to sell would achieve a sale through a Dutch Auction.

A couple of things against your argument are 1) vendors will eventually have to accept market value and 2) not just investors but also FHB are pulling out of the market which is bringing demand to lows we haven't seen for a while.

I think you are both right on point 1 - Most vendors reluctant to come down to meet market, but naturally over time if buyers don't move their offers up then more (not all of course, or all at once) sellers would move down.

Median and average prices will hold up (other than monthly REINZ that adjusts for stock sold). As less lower priced stock sold, as sales skewed to owner occupier sales, rather than investment properties. So in reality prices will decline, but statistics will show prices holding up.

AJ, agree but it is better late than never in my humble opinion. Reality will meet sellers at some stage. May be staggered, there might be a few who just hold on to the ideology of insane prices but at some stage they will adapt/adjust, specially if IO loans are a thing of the past.

Between 2017 and 2019 there was a stalemate. Prices felt high, but vendors wanted it and properties eventually sold near expectations. Low interest rates and low unemployment probably kept things stable. I thought COVID would be the thing that ended that stalemate, but it didn’t. In order for prices to drop, we’ll have to see sellers forced to sell or be fearful about hanging onto surplus property. Otherwise, prices will remain relatively stable.

If we want price stabilisation or even prices to come down to affordability, immigration tap needs to be turned down significantly. For starters the government can scrap the study to work visa and see the difference it makes. It will make NZ almost breathe again.

ahhhh ....just the usual seasonal blip, as the weather gets cooler, market activity cools off.

Nothing to worry about here - just relax folks, with "kind" Cindy at the wheel, a smooth trajectory into "slow and steady" house price growth awaits, backed up by our very low interest rates, at least for the next 5 years.

A steady stream of overseas Kiwis (all with a hefty deposit/cash) wishing to return home, an overall shortage of good existing houses, as well as quality townhouses in the more urban areas.

Cindy and Grantee have it all under control, why we have Utopia coming up, with so many experienced and educated people wanting to move to Aotearoa with their whanau, while their skills and acumen will bolster the economy with their innovation and "out of the box" thinking, why not forgetting our Kiwi ex-pats returning with very similar skills, plus their local knowledge, only to enhance our overall productivity.

This market will be held up at "all costs" , so just relax people and enjoy the highest house prices in the western world, as compared to average incomes :) ........ahhhh true economic bliss.

Agree :)

You have to understand there's been many changes to the market than just a season change. This is unlike previous years (aside 2020) due to LVR reintroduction as well as tax changes.

I really don't get how these number can be over 50%, as others comment I am seeing more like 25% clearance. Regardless, it is a very poor result if you are intending to sell your house given all the associated costs and extra time it takes to sell.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.