House prices are high. The news is full of stories about how hard it is for first home buyers to get on the property ladder.

By any measure, it isn't easy. But then again it has never been easy for first home buyers. 'Never' have they had savings enough for a good deposit. 'Never' have they had incomes that don't make the early repayment obligations stressful. Those two conditions have been facts-of-life for the 70 years or longer that the modern home loan market has been around.

Contrasting this is cheerful and optimistic advertising by banks making it look like buying a first house is a straightforward process.

Unfortunately we don't have reliable, consistent data on any of this over that full 70 year timeframe so we can check these core tests of first home buyer stress.

We do have home loan affordability reports, and they don't show excessive stress. They started in 2002, so it offers almost a 20 year view.

And that is because loan serviceability stress is not high because interest rates are low.

But, but, but ... the sceptics respond. The real stress has shifted to the ability to save the deposit. Fair enough - it is a real stress.

However, the Reserve Bank's C31 data series does allow us to look in some detail at what has happened to borrower loan take-up since August 2014, almost a seven year view. Have the deposit saving difficulties actually held back first-home buyers?

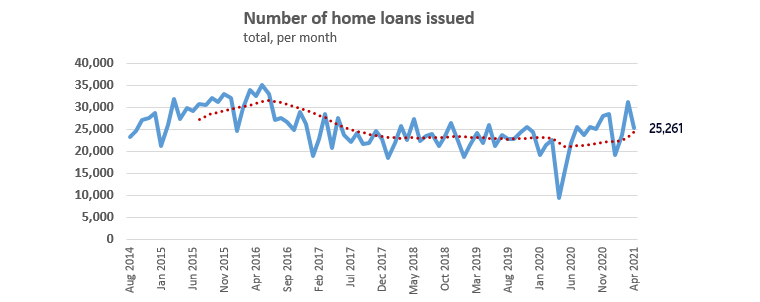

Let's start with the big picture. For the past three and a half year, banks have issued about 25,000 loans per month. And that level of activity has been remarkably stable.

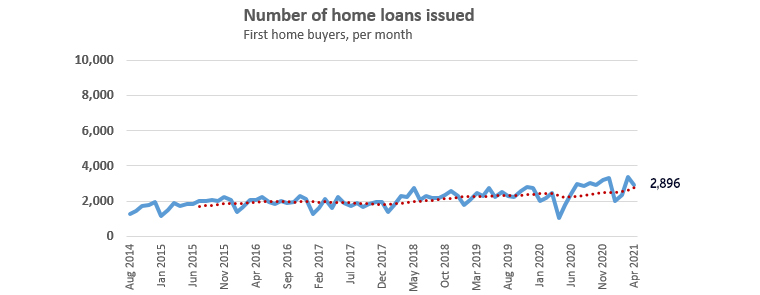

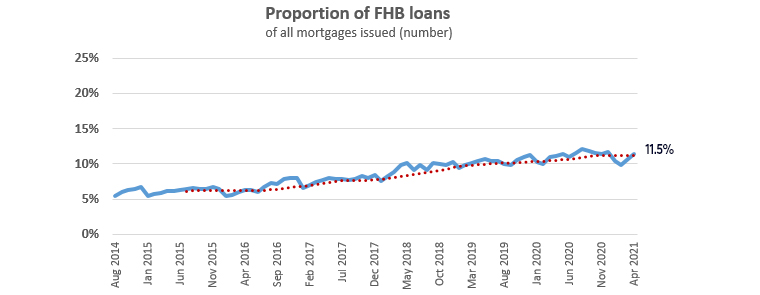

However, the proportion of these loans going to first home buyers is up to 11.5% and that is near its series high.

For all the stresses - income, repayment, or deposit - it is clear that double the number of loans are now going to first-home buyers in 2021 that they were in 2014, and this gain has been steady and consistent.

It is hard to claim that first-home buyers are under more stress now than seven years ago. In fact, they are under less, according to this evidence.

One reason may be because of KiwiSaver. Balances approaching $100,000 for members who started in the scheme at 18 in 2008, would give someone who is 31 now a base large enough to build a credible deposit. Especially if they also saved some of their take-home pay for this purpose. This clearly won't be everyone, but it does appear to support the almost 3000 people per month who are currently getting first-home buyer mortgages.

You can still argue that 3000 successful first home buyer borrowers per month leaves many who want to buy behind. And that is a fair point even if it is unrealistic. If they don't have a household income large enough to either save or afford the home loan repayments, then artificially encouraging them into buying in this housing market would only create other stresses. Like juicing up an already juiced up housing demand, like adding to excessive demand for housing construction that is pushing up materials prices, like encouraging stressed buyers to take on more financial risk.

Slow and steady is helping an increasing proportion of new homeowners get on the property ladder. Keeping speculators suppressed on the demand side of the market pressures is clearly working to a sufficient degree that is allowing more first home buyers to win, and win in a housing market that is full of unjustifiable distortions, especially distortions around regulatory settings (like school zoning, RMA, council inefficiencies, NIMBY pressures, etc).

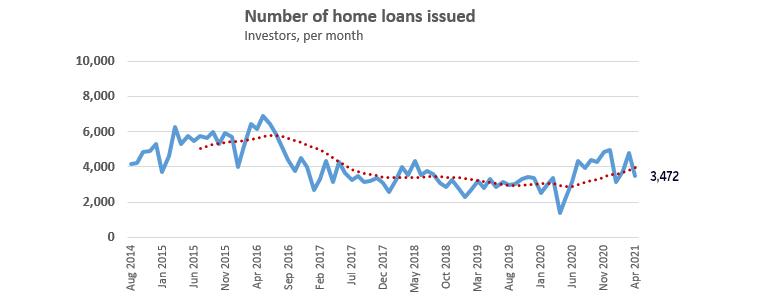

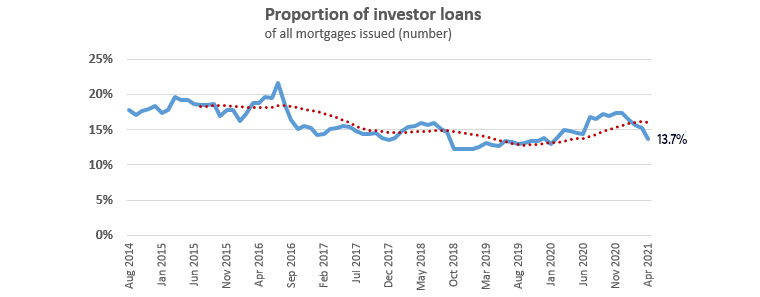

The same data is available for investor loans. This group has been subject to regulatory focus and that has changed loan issuance activity. Certainly it makes it a more volatile series.

Investor loan activity is now running well below the running 12-month average.

59 Comments

So basically those people who have made buying a house their number 1 priority are still buying houses, funny that.

Mortgage Serviceability isn't the problem, it's the deposit.

Rather than starting at age 18 David, I think you would be better to start at age 21 or 22 in terms of Kiwisaver payment assumptions. Many people leaving school at 18 will struggle to put much if anything into Kiwisaver due to low wages. And then of course most people graduate from tertiary education age 21-22.

But you make a good point, kiwisaver has been a big factor assisting people into home ownership, it was for me.

Thank you Dr Cullen!

Fair enough. So they may be 33-35 when it gets near $100,000. There will be a wide range. Also, I don't think Michael Cullen was too keen on the KiwiSaver-for-house-deposit, I think it might have been Peter Dunne.

The problem is the deposit gets bigger and bigger with time.

My 22 year old son has just started his first job out of uni as an engineer. Let's say he gets 100k together by age 35 with his partner. Let's be generous and say 150k, allowing for wage inflation. If we assume that the average house price is $1.7 million in Auckland by then, that is not even a 10% deposit. And the serviceability would be awful, even though wages will increase (and so will the cost of living...) interest rates won't come down.

It's all about the math, and it's only because interest rates have fallen and fallen in the last 10 years that we have the current situation of some hope, at least in terms of serviceability.

We don't have that buffer moving forward.

Which is one of the reasons I think a doubling of house prices in the next 10 years is unlikely.

You have started with a premise that house prices will rise about 70 percent. They could equally go down and your argument would fall apart

True indeed.

But my premise is based on, by recent standards, moderated growth in values.

You've just described the conditions that bring about a collapse, too many who believe the housing market will never fall ... it is probably not imminent but one day there will be a decent recession, investors and owners will be faced with lack of cashflow and sellers will be forced to make decisions. IMO we have built stop banks using QE to hold the wall of water from wrecking the place, all it takes is a small crack and it will give out

thats what happens with ponzis

There gets a point where it cant expand anymore and the capital gains disappear.

The NZ housing market is way overpriced and many are banking on future gains rather than a roof over a head or a reasonable yeild on the investment.

That means when the time comes there will be a massive correction.

Do the maths, houses going up 20% a year, wages 2%. Easy as that

The "big correction" isn't coming, flat or even a slight dip maybe, but this bubble pop simply isn't coming. My guess, 10/15% this year, flat next year, then maybe flat/-3% 2023 and same for 2024,

As above KiwiSaver has given a whole cohort of people who would never have saved a deposit on their own volition the chance to buy. A couple in Auckland earning no more than $150k between them who have been in KiwiSaver 5 years each, buying a brand new home in Auckland for $700k (yes I know comes with own issues) only need $21,650 saved. based on First Home Loan 95% loan $665k leaves $35k needed plus 1% underwrite fee to Govt $6,650 total $41,650. $20k First Home Grant government gift leaves only $21,650 needed. Need to come up with legal costs say $2k plus valuation another $1k them selves (and the bank might give them a couple of $k at settlement) and they're in their own brand new McMansion. Repayments about $615 per week plus rates say $50 week and insurance $25 per week. Maybe some body corporate or tenants association ongoing costs. Yes interest rates might go up (but no-one really knows) making it harder but i suspect political fallout will curb that to some degree.Read accommodation supplement available for home owners as well as renters And maybe they will go into negative equity for a few years but really so what? The banks don't for-close because of theoretical negative equity. In their books the house is worth what it was purchased for and that doesn't change if they just keep paying the mortgage. Is this all better than paying $650 week for some run down cold damp dump? For a lot of families it is

And when interest rates go up?

See the faces in the picture at top of article.

exactly - never mind the facts , look at the stock pictures.

Missing a vital point: the average age of those who count as FHB.

If FHBers are getting older as a cohort, that would suggest it takes longer for people to get in a first home.

It take people later to get around to doing everything, how many 22yos are married now, vs the same ages in the 80s? Hell, at 22 you've probably just entered the workforce now after Uni/Tech.

And then 10% of your gross pay is going towards the student loan for 5 - 10 years.

12% of net pay. Not gross.

No, its gross, 12% of gross over the threshold ($390/week )

Nope. It's definitely 12% of net pay after PAYE comes out. The gross income is only used for the threshold which has now been adjusted to around $21,000. If your gross income is over the threshold, you pay student loan with 12% of your net income deducted.

It's why student loans should be wiped for citizens who remain living in NZ for three years after graduation. Imagine how much more beneficial that 12% would be to the wider economy than going to the government.

Precisely. Of course it is never easy for anyone to buy a first home, because most people buy a first home as soon as it is remotely financially feasible for them to do so.Talking to older relatives, they did all the things that young people are doing today - bought in less desirable suburbs, raided their pensions funds, gave up the car, etc. The difference is that they were doing all these things in their early to mid twenties, and often on one income, and the 'less desirable' suburbs were within commuting distance of Auckland/Wellington CBD, rather than (say) Masterton or the outskirts of Hamilton.

The CoreLogic First Home Buyer report that came out last month said the average age of a FHB in 2021 is 34. The same report had the average age of a FHB in 2016 as.....34.

Yes but this refers to all of NZ not Auckland or North Shore or Rodney

Given the amount of complaining on Interest, I didn't expect that the proportion of FHB has doubled in the last 7 years, which btw, is great.

Wonder what proportion of those FHBs have got help from their parents Yvil? I bet it's quite high.

Ahh ... The Bank of MaD

Read recently a survey of mortgage brokers reckoned ~75% and banks reckoned ~50% are getting 'some assistance from Ma & Pa'. The difference I'm guessing will come through in gifts from Ma and Pa which the broker sees but the bank doesn't.

Interest FHBs are a tiny but emotional and vocal group.

Most that have bought no longer care about posting on forums anymore as they are happy to have their own roof over their heads.

Looking at the household debt plot its never been easier to service a mortgage

The difference in the struggle now is its a 35 to 45 year process compared to historically much shorter one and instead of being aided by falling rates FHBs now have to struggle against either rising rates making initial hard stretch seemingly indefinite. Or the economy flatlines and we get low rates forever and then everyone struggles.

If rates do return to historial norms the value of the house (using say median income multiples) will be lower that what you bought it for. There won't be any opportunity to invest in anything else as everything you had went to pay off the mortgage.

Many people are laboring under the delusion they can/will be able to afford home ownership.

Under the current settings, to use an idiom; people will "do-their-heads-in" living under such false hope. Settings may change but as this is out of the control of the individual, I suggest those 'priced out' change their desires.

Focusing on increasing income, savings and skills would be a more healthy avenue for many.

Think you need to include some analysis on FHB with gifted deposits. My guess is this makes up a decent chunk of FHB.

Yes exactly, see my comment above. Anecdotally, it seems that it happens a lot, and many are reliant on it. To be honest I got some help, wouldn't have been possible without it.

Too bad if your parents are of low to low-moderate wealth.

Therein lies the problem. Massive increase in social inequality due to the mum and dad help issue. And we have a labor govt - I cant understand why the Unions are silent?

Intergenerational inequality is getting perpetuated in a big way.

There’s social inequality from parents wealth in every avenue you care to look at and this is no different.

That is life Amigo.

Sure, but wasn't the great achievement of the West in the post war period to create societies where everyone, or at least most people, had a fair chance in life?

That's most definitely not the case anymore, and as a society we are the poorer for it. In my opinion.

..being completely ignorant to the fact this was not how life was In NZ and has been perpetuated in the last decade plus by deliberate policy.

Fine for many of us, self included. But open your eyes and look at the state of social unrest, feeling of hopelessness and out right theft from savers to asset holders.

I know of many very stressed and mentally exhausted middle aged savers who are working their arses off and yet go backwards,. In the meantime their leeching disgusting landlords get gains for sitting on their big fat arses. Getting near time to bring out the nooses.

Allowing first home buyers win! Unbelievable.Overlooking the great big fat difference that for much of the past interest rates had a ton of room to fall (from 19%) and wage increases were slow and steady.

Spin it like you want...but buying a home in NZ is a s##t show.

What's that saying...lipstick on a...

David

Great to see number and percentage of number of total mortgages referred to - it has been common practice for interest.co to refer to $ value and $ percentage.

As I have previously posted, that by using $% has meant FHB activity has been under-reported and of course longitude values have little meaning in a buoyant market. Those posting above noting surprise at FHB activity supports this. I have regularly quoted that the number of FHB is at a historic high levels despite the doom and gloom.

The outlook for FHB is unfortunately not good; the signs are that things are going to get considerably much harder for FHB over the next few years.

Although serviceability may not been a significant issue (mortgage very similar to rent) compared to the problem of house affordability (deposit) these two are going to be come a double hit.

Indications from RBNZ re future of OCR and recent upward movement of longer term bank rates indicate that mortgage payments are going to see considerable upside - serviceability is going to get worse.

As for affordability, this is unlikely going to get any better in the short term. RBNZ, Treasury and Robertson see moderate increases in house prices over the next three years so difficulty regarding affordability is not going to improve.

If those slagging Orr on single issue of house affordability took the time to consider the wider rationale for RBNZ actions, then they would see future RBNZ actions are unlikely undermine the current housing market.

That would be good news for FHB wouldn't it p8? Rising interest rates will be higher return on savings while saving for a deposit, while if financial theory of discounting future cash flows with a higher discount rate, means a fall in asset prices.

So if the theory is correct - rising rates are great news for potential FHBs.

IO

Don’t bother if you can’t add something constructive.

Either obtuse or Year 9/3rd Form Maths is beyond you. .

Asset value = sum of discounted future cashflows, if you increase the interest rate you decrease the asset value.

What IO is saying is pretty much mainstream; basic stuff that even you, P8, should be able to understand. You can try and google it if it is beyond your current intellectual capabilities..

In Auckland with average house price of 1.3 million ....

Even if deposit of $300000, still a loan of million dollar will be and should be stressful. If not now than in Future unless RBNZ has decided to support home owners forever.

Imagine trying to save $300,000 while paying off a student loan and paying rent and getting 0.25% on your savings, then the government taking RWT from the interest paid on that....

Most FHBs should be looking at townhouses, 650-750k

Ahahaha. Last year's prices.

You could always move away from Auckland . Its not the benchmark for all things housing. Thats why most of FHB's and market commentators are struggling. NZ has what we economists call a structural housing problem. Like any market the wise move away to areas where pay is similar and housing cheaper. The rest is cosmetic stuff as in i WANT to live in Auckland. Simple thing is most cant afford it so get over it and move

Looks like the number of home loans issued has remain stable since 2014 while NZ has added an extra 600,000 people.

Here's a useful test to find out if buying a first home is harder or easier: assume you are now the age you were when you bought your first home. You have the same circumstances (job, savings rates, etc). Add student loan if you would have needed one. Could you buy your first house at today's prices?

Have you considered FHBs are accessing their parents funds in greater and greater numbers to get a deposit?

Is it true there is a propensity for Maori and Pacific Islanders to be lower in the socioeconomic strata? Are they not hit harder as they don't have parental wealth to tap into? Is juicing asset prices by lowering interest rates by the RBNZ a therefore implicitly racist policy? Is the RBNZ racist?

The RBNZ racist? What the actual.

The demand for racism far exceeds the supply as evidenced by another muppet going out of his way to generate it. I’ve heard it all now what a disgrace.

Not directly racist but potentially a case of indirect institutional racism.

The RBNZ's policies are worsening inequality and as a result leaving more Maori, as one of the poorest groups in NZ, further behind.

By this logic, anything that hurts the poorer half of society is racist. Personally I don't like the focus on institutional racism. If direct racism were removed and there was greater wealth/social mobility it wouldn't exist

Have you considered FHBs are accessing their parents funds in greater and greater numbers to get a deposit?

None of this shows that it's 'just as easy' for FHBs to buy; just that they remain desperate enough to stay in the game despite its being harder.

As others have said above; we're talking longer mortgage terms, on dual incomes, for worse properties. It is going to be a staggering drag on the economy going forward; a large cohort who won't be spending much, starting risky businesses, or investing in anything for decades to come because of the size of the mortgage they have to service.

The real problem I have with this analysis is it looks just at serviceability and deposit requirements and ignores the absolute value of the loan being taken out as well as the value of that loan relative to earnings.

If interest rates never ever move at all whatsoever in either direction over the life of this loan then that's a fine assumption but I don't think it's reasonable to assume no change in interest rates. Especially now that China looks like its becoming an exporter of inflation rather than an exporter of deflation as it broadly has been over the last boom period.

Debt magnifies both gains and losses, the higher the degree of leverage the larger the magnification. Couple % point increase in interest rates could wipe a significant chunk of value off house prices (asset value = sum of discounted future cashflows, if you increase the interest rate you decrease the asset value) at which point FHB would be deeply in the red, could easily even be 2-3x their income in the red! Which is a lot, considering house prices used to be 3-4x incomes... essentially by forcing FHB to take on this much debt we're increasing the volatility of their expected lifetime wealth significantly.

I bought 18 months ago and I don’t think I would be able to buy now, at todays prices.

Or if I could buy I wouldn’t have much of a life due to my mortgage being probably $200k larger.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.