By Greg Ninness

There’s a glimmer of hope on the horizon for prospective first home buyers with the national lower quartile selling price declining in April, according to interest.co.nz’s Home Loan Affordability Report.

The decline was small, but its significance was underscored by the fact that lower quartile prices declined in the Auckland, Wellington and Canterbury regions, along with those for Bay of Plenty and Manawatu/Whanganui.

According to the report, the Real Estate Institute of New Zealand’s national lower quartile selling price declined to $591,000 in April from $598,000 in March.

Although that’s a very small drop, it’s significant because the only other recent declines occurred in January this year, when the market was in its Christmas/New Year hibernation, and prior to that in May last year when the housing market was severely affected by a COVID-induced lockdown.

The decline in prices was particularly significant in the Auckland region because the lower quartile selling prices in all seven of its main urban districts – Rodney, North Shore, Waitakere, Auckland Central, Manukau, Papakura and Franklin were lower in April than in March.

The price trend was more mixed in the Wellington region with prices down in April compared to March in Wellington City and Porirua, but up in Kapiti and the Hutt Valley.

Other cities to record a decline in their lower quartile prices in April compared to March were Tauranga, Rotorua, New Plymouth, Whanganui, Christchurch, Timaru, Queenstown and Invercargill.

The lower quartile price is the price point at which 25% of the properties sold each month were below and 75% were above, representing the bottom end of the market that is of the most interest to first home buyers and investors.

The decline in prices at the bottom end of the market in April raises the possibility that the tax changes for residential investment properties announced by the Government on March 23, could be starting to have an effect and the market may be at a turning point.

However one month’s figures do not make a trend.

Because the size of the decline was small at less than $7000 for the month overall, it could probably be characterised as more of a stalling in the upward price trend that has been apparent for most of the last year, rather than the start of a decline.

It will likely take another couple of months before it becomes apparent whether April’s figures represented nothing more than a blip in the upward trend, a flattening of prices, or the start of a decline.

Aspiring first home buyers will obviously be hoping for the latter, especially if they live in Auckland.

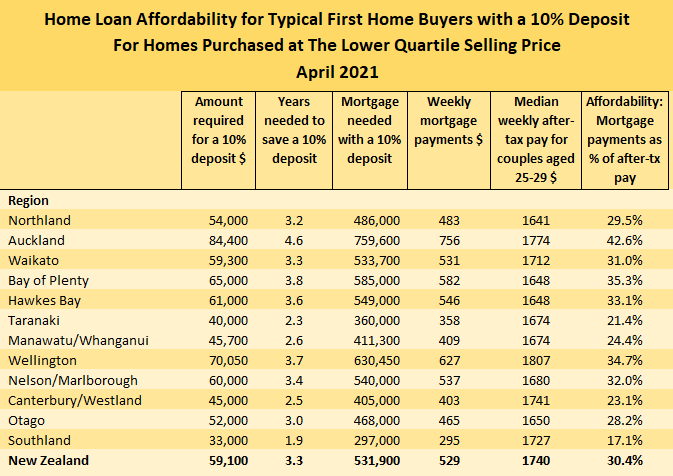

The Home Loan Affordability Report shows first home buyers in Auckland would need to save $84,400 for a 10% deposit on a home at the region’s lower quartile price of $844,000 in April.

That would take a couple working full time at the median rates of pay for 25-29 year olds in Auckland just over four and half years if they were able set aside 20% of their after-tax pay each week, which would be no mean feat.

However their problems wouldn’t end there, because if they were able to scrape together a 10% deposit, the mortgage payments on a lower quartile-priced home would chew up 42.6% of their take home pay, putting it squarely into unaffordable territory, even though interest rates are at record lows.

That would leave them especially vulnerable to any interest rate rises.

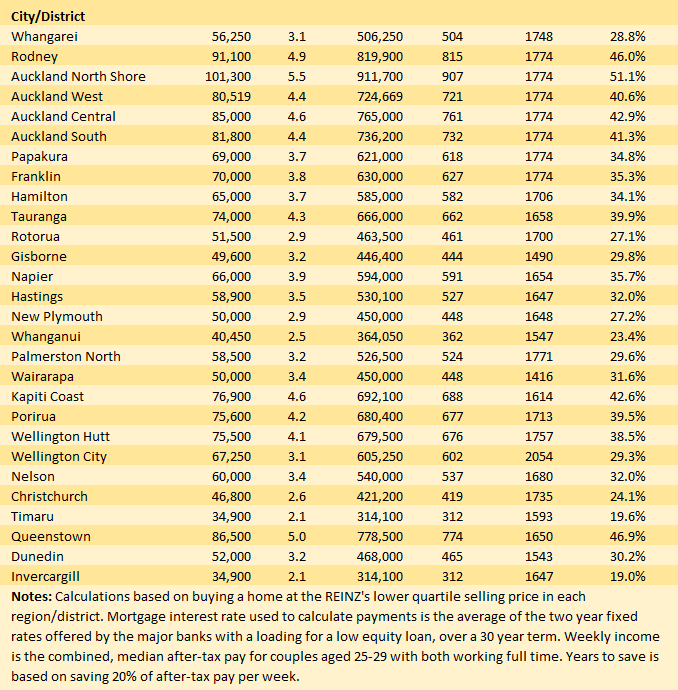

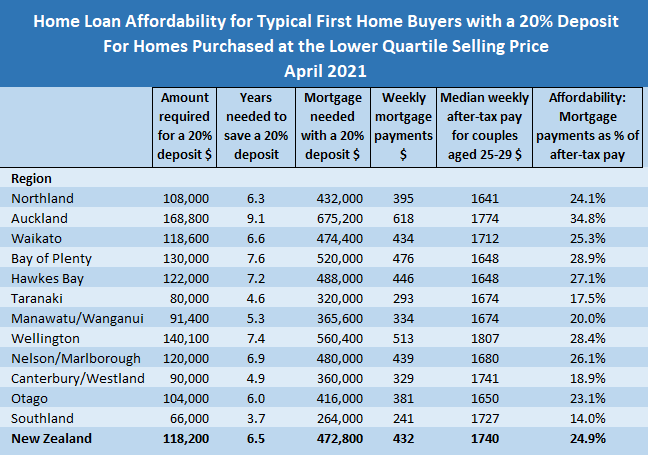

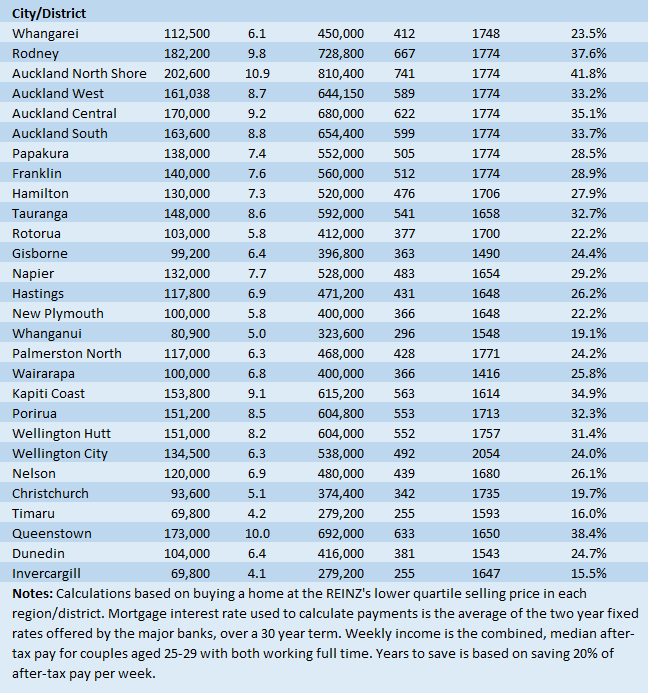

The tables below show the main affordability measures for buying a home at the lower quartile price in the country's main urban areas, with either a 10% or 20% deposit.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

138 Comments

Its doesn't seem to be falling in my area. North Waikato and Franklin are still seeing some ridiculous prices being paid. A modest house in Tuakau sold for $990 000 this week. Homes estimate $730-$800K. Very few houses for under $700 now, this is a big change in the last 6 months. The local school Tuakau college is a Decile 4 (great school though), this is not a rich area. What hope is there for local home buyers or renters. The spread of the super city is causing damage in North Waikato.

Its doesn't seem to be falling in my area.

The good thing about data is that it gives a counterpoint or an anchor to 'I reckon'. And because you're seeing 'ridiculous prices', this is potentially not a good sign and that the bubble is rampant across all price levels and could spell massive pain for individuals, h'holds, and the wider economy.

Yep, people are escaping the super city because they can't afford houses there. And so the problem just kind of spreads. RBNZ and government, this is your mess, take a bow.

RBNZ and government, this is your mess, take a bow.

Culpability for the mess might be a bit wider than these obvious targets.

Govt sets the parameters that we all work under so yes this very much is their problem. Of course they can slam the public with more costs to steer us away from buying homes either as investors or as occupiers in the short term. But house buying will return eventually so that approach will not work longterm. Reduce bureaucratic nonsense and reduce governmental overcharging, then watch house prices tumble

They're culpable for bubbles I agree. But that also includes commercial banks, media, and the general public.

150k in gst on an 850k house makes 1 million

Council reserve and development contributions 100k

Water meter 20k

Theres 270k you can knock off the cost so million dollar new house becomes 730k and 750k old house drops to about 500k. Affordable homes again!!!

150k in gst on an 850k house makes 1 million

Council reserve and development contributions 100k

Water meter 20k

Theres 270k you can knock off the cost so million dollar new house becomes 730k and 750k old house drops to about 500k. Affordable homes again!!!

Fake news

Not sure what you mean by fake news. Just look at the Barfoot sold prices for the past few weeks. You can also see sold prices on Homes.NZ. If you compare auction sold prices over the past few weeks with those paid in spring 2020 there has been a big move up, many streets are seeing the ceiling values broken. Agents are promoting Tuakau as if it is Auckland rather than Waikato. I'm hoping that we are in Bull Trap territory. I own a home but think we need to see a 20% price drop minimum. The level of borrowing is crazy.

Lots of keyboard warriors, means nothing. House prices will continue to go up this year, maybe flatten off next year. More blah blah crap.

I'd like to see prices ease off a little too. Then I'd also like to be treated fairly by Govt housing policy. Maybe too much to ask on both counts. There isn't enough supply, and none of it is affordable. Govt are only increasing the housing shortages. They don't seem aware of it either.

Given the Govt induced price increases over the last year, that ain't gonna turn around at the drop of a hat. So on it will go for at least another year or two,

Dave, I'd suggest that the Auckland Council and their RUB have contributed more to sky-high house prices in Auckland than central Government or RBNZ. The creation of the RUB to create population density in order to have a public transport|train system that doesn't rely on subsidies from Auckland Council, has led to supply issues and therefore price increases. I understand that this is only one of the reasons, but it is a good chunk of the reason.

When the "lower quartile" home in a dull rat-hole like Auckland is closing in on a million dollars there is no hope.

A lot of financial trouble is brewing for those that overpaid.

Brock

The important factor is the ability to service one's mortgage. A home is a long term investment is and short term fluctuations in the market are irrelevant . . . . same house whatever the market does. However, those with mortgages need to keep a weather eye on interest rates which Reserve Bank has indicated have a likelihood of some upside.

As for "over-paying" . . . well at this stage Treasury, RBNZ and Robertson see some upside of 0.9% this year and then 2% in the short to medium term. While there is no certainty in the market, I would be putting more weight on their outlook rather than the anonymous keyboard warriors on this site calling significant drops . . . one may need to get used to the fact that house prices may remain around current levels.

The dilemma for potential FHB is that rather than mortgage affordability, the greater issue is the size of the deposit.

An important point is the servicing one's mortgage at these price levels and low interest rates is very difficult.

If 2% is the expected return, I'd rather have money being more productive elsewhere. A house isn't everything.

Jesse

A couple of points:

If one is looking at returns, then 2% house price inflation is a 10% tax free increase on one’s 20% equity, and 20% increase on a 10% equity. You are not going to match those returns other than in a speculative high risk investment.

To match an 2% increase on a $800k home is $16,000 pa - that’s $16k increase.on after tax income.

Make sure you don’t end up swimming against the tide.

There are lots of investments that knock the spots off housing. You just have to educate yourself to the wider world. The universe is literally full of opportunity. To get hung up on one tiny market in that universe is nuts, especially when as you say, the only advantage is temporary ease of leverage. Try applying leverage to price moves on the negative side in your projections if you dare.

Aren't you forgetting about the interest that needs to be paid on the 90% loan? Then there's rates and maintenance. Surely that wipes out the 2% gain.

No I don't want to be caught swimming naked when the tide goes out.

That Warren Buffet quote was too easy to use here, I'm not actually that negative on property I just think at this time there are better places to have money invested. The place I'm renting is great :)

Jesse

You choice and genuinely best of wishes.

The 150,000 FHB over the past three years who purchased homes under the same conditions of uncertainty however would tell you that they don't feel that they are swimming naked.

And don't moan when the landlord knocks on your door giving you notice because he/she has decided to sell and take their capital gains into those areas of better investment you refer to (whatever they may be).

Thanks for your wishes Printer8 - I know I'm going to be just fine.

And no I won't moan if the landlord sells - that's just a risk that I'll accept if it happens. I too can knock on their door saying I'm moving to another city or country - this flexibility has lots of value to me.

Jesse

Great to see you weigh up the positive and negatives and what is important to you in terms of your particular values. There are always risks, compromises and costs but in coming to a decision, one's value will rightly influence that decision as to what is right for you.

So, sound decision making so I wish you well also.

Hi printer8,

That's a very clued-up response (11.27am) of yours to Jesse.

Further, I'd much like to hear from Jesse: exactly what are those areas of better investment???

TTP

I’m not Jesse but I guess it depends on whether you are talking historical or future. Housing has been great but surely it has done its dash. Interest rates can’t go much lower, prices and rents can’t go much higher.

Jimbo

Agreed.

Talk of significant capital gains from house prices will be simply reminiscing at the BBQ for a number of years to come.

RBNZ and Treasure opinions regarding the next three year support that.

You are wrong because you make more than a 20% gain if the house goes up by 20% (original post), here is the maths say you by $1,000,000 home 10% deposit so you invest $100,000 the house goes up by 20% you house is now worth $1,200,000 you paid lets say 3% in maintenance and interest, on the whole million that's $30,000 (no rent received) so you made a 170,000 profit on your $100,000 investment that's 170%, while other investments outperform housing in the 20% gain there are very few investments that a bank will lend you large sums of money to leverage your investment in the same manner. Of course if house prices go down you are screwed, well you go bankrupt and try again later, let the taxpayer bail out the banks that lent you the money.

If one is looking at negative returns, then 2% house price DEcrease is a 10% tax free loss on one’s 20% equity, and 20% loss on a 10% equity. Leveraging works both way, mate. By the way, using your example (which is flawed anyway, as you are comparing a one-off gain with an ongoing income), to match an 2% decrease on a $800k home is $16,000 pa - that’s you need a $16k increase on after tax income to compensate for this loss.

By the way, margin lending has nothing to do with the inherent risks associated with what your partially borrowed funds are invested in.

This post is an example of financial illiteracy, and financial illiteracy of many kiwis is the reason why they are stuck with a 19th century mentality whereby the best investment is in housing. This is why we have a stagnant productivity and an economy over-reliant on parasitic residential housing speculation, rather than on real productive investment and innovation.

Housing / land is a pretty damn good investment: an almost guaranteed demand and fairly limited supply is quite unique. However because of this and favourable tax treatment the prices have got out of whack: even at current low rates investment properties have a very low return after costs if not negative, which means it has become purely speculative and FOMO. In the past I would have said leverage is much safer in property than other investments, but now it seems just as dangerous or maybe even more so.

Exactly. Success is NZ is to leverage up and sit back making tax free capital gains. If you've got a brain to do something innovative - you can take a back seat.

fortunr

Agreed; "2% house price DEcrease is a 10% tax free loss on one’s 20% equity"

But remember housing is long term and short term fluctuations are irrelevant . . . same house, same mortgage repayments.

As posted, I have experienced three periods of short term falls in house values . . . but it is not about short term. Look at 2% pa long term returns . . . and that is consistent with Treasury and RBNZ outlook.

Despite what many may think, I'm not being bullish; since October last year that increases were not sustainable and even then said that some correction could be likely.

Doesn’t that apply to other investments too: for example a diversified share portfolio is probably just as safe as housing over a long term. But I’m not convinced that borrowing a lot of money at historically / stupidly low interest rates in the hope that rates stay that low is that safe in either case; it will probably be fine but there could be some very big losses too.

Thanks for calling this out. A correlation was found between financial illiteracy and mortgage equity withdrawal in some academic research after the GFC.

You seem to be acting as patrician tutor on here, trying to correct everyone who does not fit your views

mike

If you are referring to me:

Substantiated debate is not about correcting people; it is about testing views and people coming to their own conclusions.

Sorry, but predicting the NZ housing market on the basis of the alignment of planets - such as you have done - is definitely a view that doesn't fit with me and needs and should be challenged.

Yes I was referring to you and not referring to your challenge to me, no.

I have no problem with that, and it is all t the good.

Simply my comments were reflection on general tone of contribution on this site.

Indeed. The trouble brewing is mortgage affordability as rates increase. Imagine being on the hook for a lifetime of debt for a rat-box in some low opportunity backwater.

Many people are wising up to the fact that NZ offers a beer lifestyle on a champagne budget and will be voting with their feet in the coming months and years.

Where will they go ?????

Traditionally it has been the rest of the Anglosphere and Europe that attracts bright and motivated people.

That was then. Why would they take a Kiwi with an average degree from one of our now average universities when you can get an Indian, Chinese or East European graduate with a top degree from a university with higher ranking than ours? Excluding Australia which takes any Kiwi only our very best will be acceptable to the Anglosphere and Europe.

No shortage of kiwis living overseas. We are the second best country in the world at driving our best people overseas.

In the past when I was a POM that was true and maybe it is true today (ref Kiwis who moved overseas at some point in the past) but for current ambitious Kiwis looking for a future in the many OECD countries that are wealthier than us maybe the door to that opportunity is closing.

Light beer at that.

Average price increases of 0.9% annualised mean that some house prices will be falling.

A home is a long term investment is and short term fluctuations in the market are irrelevant

Not according to Adrian Orr. He stressed that housing is a 'consumption good.' Do you disagree with him?

I disagree with him (not just on your question either!). If you rent accommodation then the consumption good view is fine. But OO houses are often viewed differently by purchasers. It is seen as an appreciating asset (whether it is or isn’t is beside the point), in particular the land, and/or as a hard store of value, that can be leveraged for future debt into further asset purchases or business development. Financing this particular activity can then be achieved at much lower costs than other consumption goods. Orr may be right in theory, but in practice OO housing isn’t a consumption good and basing policy on an unsound assumption will produce poor outcomes.

So you think that housing is not a consumption good because of public perception? If the public disagrees with Orr about the different between a consumption good and an investment, why is he in a position of power over regulating the money supply seeing that housing and money supply are intrinsically linked?

I didn’t say that. I just explained that market participants are not operating as if it is a consumer good, they are behaving as if it is a capital good.

Is that a problem? Does Orr think the public is wrong-headed? What are the consequences?

....... "a dull rat-hole like Auckland" ........

Sounds like you've become pretty disaffected, Brock.

Time you moved on, I reckon, and made way for the enthusiasts.

TTP

The only enthusiasts left are boomers, migrants from non-first world countries and the terminally stupid.

Very sad.

These wealthy boomers think they are 'winning' because they are 'getting ahead' of other poor Kiwis. They need to travel outside of their small backwater and realize that they are far from winning globally. NZ is going backwards.... fast!

Groat

"NZ is going backwards.... fast!"

You have stated that a number of times and have posted on numerous occasions that you are getting out.

I have always found that those who are successful, rather than simply moaning, they not only look at the options but most important have the initiative and confidence to act . . . . you seem to be lacking the required personal attributes.

I look forward to your bon voyage party . . . but it seems I could be waiting a long time.

Cheers :)

I moved to Perth and am now on $250k doing FIFO in the Pilbarra. I will be ok (but only because I left NZ).

I guess nobody told printer8 he wasn't invited.

Printer8 is the sort of guy who would turn up with a bottle of $10 plonk and then drink all of the top shelf while babbling on all night how much is house had gone up in value.

frazz

In this case I would willing with pleasure shout everyone the top shelf. :)

Brock

I was aware of Groat's Australia move.

Only difference was that a week or so back it was "going to" and it was a $200k job.

I would have thought someone who had made the decision and made the move would considered themselves far better off, and having a high paying job, would be both positive and focused on and enjoying their new life rather than being bothered with repetitive bitter, moaning and slagging-off posts about things back here in NZ.

Personally, I find it difficult to pass Groat on my smell test . . . if doing any sort of business with him, I would be walking away. That's just my feeling.

Judging people when you know very little about their personal circumstances is an ugly habit.

Heaven forbid a FIFO worker posts on the internet instead of going outside to count the flies.

Trouble with FIFO is you pay 2 lots of rent

Nothing wrong with a FIFO worker posting on the internet. But when every single post is bitter and negative that's strange for someone who's walked into a $250K job.

I am on a 20/8 roster and earn just over $1000 for a 11 hour day. The company are throwing overtime at us at present so I am probably on even more now. Money is no longer a worry. If you think my pay is abnormal, you need to check wages in oz for multi skilled electricians who are willing to work FIFO. The work is hard and the hours long. Working away from home is not easy but I am being rewarded for my sacrifice. Something unheard of in NZ. The only people rewarded in NZ are those who do nothing and just leach from other peoples hard work.

Well, Groat

You have every reason to have a positive outlook on life then - Australia: high wages, cheap housing, great weather . . . . but what is with all those negative waves.

You need to get over all that negatively, get on with life, enjoy the sun and smell the flowers.

..... and keep quiet and let the exploitation of hard working kiwis go on unchecked. We need more commentary on the absolute failure of this trecherous government and we need to let kiwis realise their is still hope elsewhere. NZ is not a safe place for the poor. There are too many parasites wanting their fill.

NZ has plenty of opportunities too. Pretty much every IT contract worker in NZ is earning an hourly rate at least as high as that FIFO contract.

Rubbish.

IT and trades are not a like for like comparison. And most IT workers DO NOT earn 200k+ PA.

I do.

But I've developed this 1000k day rate earning potential after 15 years experience, 5 years of uni and completing multiple post uni industry certifications.

They don't give out high paid IT roles in cereal boxes. The majority of IT workers are on 80k - 120k working perm roles either internal or for IT consultancies.

You are not comparing like for like. IT is a relatively new industry so it’s averages are skewed by a larger proportion of people with lower experience levels. If you look only at degree qualified IT professionals with 15+ years of experience you’ll probably find a lot on 200k+.

I purposefully wrote "IT contract workers" and "hourly rates". Groat mentioned $1000 for 11 hours so that's $90.90/hour. Most contract rates are higher than that. Sure, most contractors are in their 30s and 40s, but there are plenty in their 20s as well.

I think that IT contracts and trades are a fair comparison in this case because FIFO workers are specialised in areas of demand. It's not like any kiwi in a regular job can more to Aus and make >$200K for the same job - you need to be doing something specialised and in demand for that for that to work.

There's nothing wrong with looking for better opportunities overseas. If one's particular skills and experience pay more elsewhere and you're in a position to move then by all means do it. But there are plenty of good opportunities in NZ too, if you've got the right skills.

Well said, Groat. The narcissists find it unfathomable that someone doing well personally, would be capable of caring or even wanting to do anything about the suffering of others. They want you to just shut up and let them continue to benefit from it. Remaining quiet is the last thing anyone with a conscience should do. There are so many people suffering in silence here, with no media that genuinely and consistently gives voice to the frustration, anger and despair they are feeling. We need more people that are willing to make noise and demand change for there to be any real hope.

SuperGroat, flying through the skies with his cape, helping poor Kiwis after having fled NZ, by posting on Interest, what a hero !!!

Another quality contribution.

Yep, good on ya. P8 making assumptions and talking rubbish as usual.

Mrs TP

When you have sixty plus applications for a rental and you have done that many, many times for your self and others you have to learn to judge people pretty accurately . . . . and I have been recognised as pretty good at it.

As for any one-off explanations - such as why the rent is late - one also needs to have a developed a very good filter and consider the wider personality and take it with a grain of salt . . . and I have a pretty good track record of doing that.

Personally, I have difficulty marrying together Groat having a life of sunshine having moved to Australia, having a high paying job and intending to move his money to Australia (as previously posted) to buy a far better and cheaper house, together with his daily dark posts about the situation back here in NZ.

Maybe if now that things are so great for Groat, we won't see him every day waking up with a seemingly black attitude and besotted with posting doom and gloom about things back in NZ, a situation which he says has left behind . . . that is normal behaviour.

So when the Jews reached Israel they should have forgotten the ills that had been perpetrated onto them by people they once lived with as neighbours? Get real P8, what the rich old New Zealanders have done to the poor and young is not going to be easily forgotten. They went too far this time. Expect repercussions for generations to come.

Groat

One good thing . . . at least you have got into a little bit of debate rather than the typical hit an run dark daily post.

However, you still need to question yourself about a need to climb out of that deep dark black hole. You concern me.

Thanks for the concern P8 but a one way ticket to Oz got me out of that black hole. Now, I want my fellow kiwis who have given up all hope to see that there is still hope out there. They deserve a chance too.

Groat

50,000 FHB in the last 12 months would disagree with you . . . and according to RBNZ data last November and December were record high number since they first published data in August 2014.

Do you think those 50'000 FHB's are happy they have just paid way too much for a typical kiwi shed? Do you think they are happy they can no longer afford to go out for dinner or go to shows? Do you think they are happy that they cannot afford to have children? Do you think they are happy to be completely trapped and petrified of interest rate rises or the possibility of losing their jobs. What a situation those poor people have been forced into by a trecherous government.

Groat

They never had to buy if they were unhappy. Some have seen significant capital gains over the past year . . . so yes - they were happy to buy at the time and are very likely happy now.

Keep in mind that mortgage payments and outgoings are not that much higher than rent (the deposit is the bigger hurdle for FHB) - so don't assume that they can't afford to go out to dinner, cannot afford to have children, not being prudent about possible mortgage rate increases. Worried about losing their job - well that is no different if one owns a home or is renting.

And are they forced into it . . . well that 50,000 decided to buy a home and have every opportunity to sell if they so wish. Not forced into it, nor locked into it.

Those who could have bought a year or two ago and didn't, well they won't be so happy. :)

P8, you're dreaming if you think that recent FHB are 'happy' about the situation. For most of them it was a choice between being pretty f**ked financially due to having a stupidly big mortgage or being really f**ked financially due to having to pay stupid rent for an indeterminate amount of time before having to take on an even stupidly bigger mortgage.

Couldn't agree more al123. P8 you are so out of touch with how trapped the young of NZ feel it isn't funny.

Read the room (and country), P8. I earn within the top 0.5% of people in NZ and I'm still not blinded to how utterly f****d things are for the younger generations. And this is all backed up by data, not just negative sentiment. Get a grip.

Lol. Yeah I'm sure those buyers were all super happy about it too. Most I'd wager either got a gift from parents, or had such a hard slog getting there that they are just as feed up as non house owners.

Great. Assuming they did not over-pay relative to the cyclical nature of equity and the likely downturn if NZ does NOT get the supposed 3% GDP growth and b all inflation rosy scenario forecast.

There is more internal migration out of Auckland than in. Been that way for years.

Perhaps TTP has the minority view.

To be fair try driving around in the morning and the evening.

Not to mention feckless Phil's 5% rate increase next year or the lack of water now and in the foreseeable future.

If I could get my eventual pension transferred to Oz I'd seriously consider it.

You CAN get your pension transferred, BUT in AU it is means tested, done through Centrelink, so while they suck it out of NZ you might not get it all

It's certainly nowhere near as dull as Palmerston North.

In the long run, it would be cheaper to let house prices fall and the govt assist those who are in danger of ending up in negative equity than forever having to top up with accommodation supplement.

PA

That is not going to happen . . . the reality is whether one likes it or not is that stable house prices is seen to under pin a stable economy. The past year should be a clear indication of that.

Contrary to popular belief, it is not impossible for house prices to drop and drop significantly.

I recall the governor of the reserve bank repeating this point for the benefit of the dim witted only last week.

Brock

I have no issue that house prices could drop - I have experienced that on three occasions. I have previously posted that I purchased a rental property in 2008 and during the GFC saw the new RV go 10% below what I paid for it but sold in 2016 for a significant capital gain.

Yes there is the fear house prices will drop and for over the past six months I have posted that I wouldn’t be surprised to see some fall this year. However, what many don’t seem to comprehend is that a home is about long term . . . forty years and more with stepping up in that period.

Besides being about long term, for the potential FHB there are some other points to really consider.

Firstly, a home is not purely about dollars. There is considerable intrinsic value and social security. Not long ago someone was posting that they were given notice when there wife was seven months pregnant- not an ideal time to having to find another rental and having to do a shift. Nor great for kids possibly having to shift schools and establish new friendships.

Secondly, the onset of Covid last year posed considerable real risks for the wider economy, employment and house prices - unfortunately those that held off due to these fears now find houses over 20% dearer. Timing any market is widely considered as being folly.

Thirdly, even if there is a concern prices were to drop by 5% or more, then that is within the range of buying well and buying poorly and that is of equal concern.

And lastly, both RBNZ and Jacinda have both stated that stable house prices are important. Is RBNZ going to take actions that are going to considerably undermine previous actions supporting housing for wider economy reasons just to see that work undone?

If I was currently a FHB, while there is lots of uncertainty, I would not being paralysed by fear and uncertainty. Banks have a vested interest in ensuring that their lending is prudent . . . . and they are more astute to the future of the housing market, interest rates and the wider economy than the dgm anonymous keyboard warriors of unknown experience and qualifications.

Rather than the market, as posted above I would be considering the ongoing servicing of the mortgage and would be prudent in paying down debt.

When the market falls it will be for reasons beyond the control of the government.

Whether or not prices go up or down from here who knows, but the risks are building for the downside.

Nobody in their right mind should be thinking about living in Auckland for the long term the way it's going.

Yikes ... Do you live in Auckland? ... are you planning on staying or getting out

Getting out.

P8, who somehow is not an anonymous keyboard warrior, but everyone else is? fails to understand that house prices only kept going up because mortgage rates where artificially dropped by the RBNZ. P8? Real name? Must think this had no affect? Bizarre.

Groat

Unlike you, my comments are substantiated.

Something for you to learn to day and you might put into practice; when one makes a substantiated statement referring to supporting information such as RBNZ and Treasury that is very very different to unsubstantiated statements such that house prices are likely going to fall by 50% as posted by some.

Given your standard of you repetitive unsubstantiated comments it would be great if you could take that on board.

Brock

Re: “Getting out”

Many have already.

However don’t think that this is unique to the current time.

Because of a range of issues, many have previously got out of Auckland to both Australia and the provinces. You will recall Muldoon’s comment of the early late seventies/early eighties when emigration to Australia was particularly high.

I got out of Auckland 35 years ago for the same reason - house prices. I have previously posted that one of my sons got out of Auckland six years ago: one of four in his team of six who did and now (at 35) owns his own home and a rental property and the three others have their own homes while the two remaining in Auckland continue to rent (and as an aside, face issues of twice daily one hour travel times to and from work).

Many young move from the provinces for better opportunities and that has been significant for well over the past fifty years.

Numerous immigrants to NZ do so for the same reasons - looking for a better life and conditions.

So if you think for you, I genuinely wish you well and those that have spent time overseas tend to do well from that experience . . . . but that choice is nothing new or particular to the current time.

No it's not new. But it's never been as bad as it is here now.

I got out quite some time ago and did very well only recently making the mistake of returning for family reasons.

The problem with Auckland isn't only the housing costs. It's a bland and dysfunctional backwater with lousy infrastructure and a much higher opinion of itself than is actually warranted.

I too moved back for family reasons after being in oz 20 yrs and did well over there also now dual citizen been back about 3 yrs miss oz feel the standard of living and healthcare here very poor by comparison

I have had 4 friends or business associates move back to Auckland from Melbourne (2), Singapore, and London. All bought mega expensive houses, 1 remotely via video chat, and all are intending to be here long term for family reasons. Now, I’m not saying there is a flood or will be a flood of returning Kiwis, but I am just pointing out that there are some skilled and knowledgeable people that are returning and/or view Auckland as a very desirable place to live. You may not share that view, but that doesn’t mean that your view is the predominant one.

I moved back recently too. Most of the smart, knowledgeable kiwis I knew overseas had the opinion of nice to visit home, but wouldn't want to live there.

Would like to know where (in which suburbs) your associates purchased their mega-expensive homes

Westmere, St Heliers, Point View, Whitford.

I can completely understand people buying remotely site unseen. I can also understand these people selling again one month later when they have seen the state of the house they paid 2 million for and when they have driven around Auckland and seen the social depravation growing exponentially each day. Empathetic rich people would not want to be a part of the problem and would leave as soon as possible.

Social deprivation, and gaps between the have and have nots been growing globally for 10-20 years. This is not a new phenomenon and while inequality in NZ is certainly more visible than many of us are used to compared to many other places it is still incredibly egalitarian and attractive to people who have lived in those places.

The world bank seems to think that something like 10x the population of New Zealand are net leaving poverty each year to join the middle class (https://blogs.worldbank.org/opendata/global-poverty-reduction-slowing-r…) . What we are seeing in NZ is a bunch of people in the top 20% of the worlds highest income earners (dole puts you in the top 20%, minimum wage puts you in the top 5% after adjusting for cost of living. https://howrichami.givingwhatwecan.org/how-rich-am-i?income=41000&count…) grumbling because their relative wealth is going down.

Houses themselves may be a fairly safe long term investment, although you are banking on continued population increase which may or may not occur. But borrowing money long term for any investment has significant risks right now: inflation and increasing interest rates. If you bought an investment property right now that barely makes a profit you would have to top up the mortgage payments every week for a long time if interest rates went up to say 7%. It could be a pretty painful long term investment.

They've been on the wrong side of history before. I'm waiting to see how long before they realize they shouldn't have gone to OCR 0.25 and now won't accept the fact that inflation exceeds the target

Is housing the only purchase where the dollar cost of the purchase is considered completely irrelevant?

It's all about serviceability of the loan as printer8 states. The article notes the $7000 drop as small, and relatively it is but it's still around 300hrs of work for the average person.

I guess that's what you get from a guaranteed never drops market.

'Glimmer of hope'. Nonsense.

Escape flight price drops are the only glimmer of hope kiwis can wish for these days.

Robertson & Jacinda have done their job, they've made a massive impact on housing affordability with a whopping $7k decrease. FHB's can stop complaining now, take advantage of this prime opportunity.

Actual impacts will obviously take a lot longer ( minimum of 6 months ) to begin to evaluate.

My advise to any first home buyer: Take your advise from reputable sources and do not listen to the extreme points of view in the media or some of the people commenting on sites such as these. These people are mostly being driven by emotion.

( second part of comment not aimed at nifty btw )

At the end of the day you need somewhere to live. We've seen negative equity before. Whilst this is demoralizing you're not at the mercy of a landlord, rentals will become scarce and more expensive due to govt policy on deductibility and you're working toward ownership of a physical asset.

When you do retire if you don't own you're own home life's tough renting on a pension.

Wellington doesn't inspire much hope these days, as potential FHBs. And it would take a lot more than this to do so.

However, browsing property listings in certain parts of the UK and Australia gives me some hope of a better future.

Oh if you can easily move to Australia you should definitely do it! When you get there you'll realise how little NZ offers for young people.

Its not just young people its most of the population.

By comparison our Healthcare is subpar.

Wellington doesn't inspire much when Parliament is based there.

I would be off if I wasn't already committed. Honestly if you have the choice, NZ is horrific for the young and very quickly it is also becoming bad for the those in their middle years who are paying enormous tax to support enormous stupidity.

Would need to crash for FHBs to have a chance

It may crash when supply gets ahead of demand.

Anyone that has bought a highly leveraged investment property in the last year or two should be shitting themselves right now: they just got a 33% tax increase and now there is a reasonable chance of inflation and interest rate increases. I can’t understand why they aren’t all selling up and taking the profit while they can? Surely the risks are quite considerable right now (although not the first time I have thought that so what would I know)

Anyone who bought a rental in the last year or two now has massive equity which they can do stuff with. Rents have skyrocketed thanks to govt policy and a pre existing investor will never get the same return on a rental from a year or two ago compared to post 27 March.

So I really can't understand why, so long as they can service the loan, which you'd have to be an idiot not to with such low rates and high rents, would sell now?

Depends on whether you think the low rates will last. Any significant rise will probably trigger a house price crash while also making the investor top up the mortgage payments. It’s a big gamble don’t you think? And where is the upside? Surely houses and rents can’t go up too much from the current highly unaffordable levels can they?

Rents are not high compared to the value of the property; yes it is probably an ok yield on what they did pay but not on the current value that they could invest elsewhere. Although I guess they can’t sell now as then they would have to pay CGT.

To me it feels like someone going to the Casino, hitting the jackpot, and then being too stupid to cash up and leave.

Depends whether the investment properties Jimbo mentioned are rentals or capital gains vehicles. There's plenty of people buying (collecting is a term I heard) property solely for the purpose of capital gains to better any returns they'd get in TDs. Some of those properties are left empty. If this is seen as a peak by the "collectors" they will have different motivations to sell compared to some landlords.

"massive equity which they can do stuff with", do you mean they can use equity as collateral to take on more debt for consumption or property speculation? That debt still needs to be repaid and will incur interest charges. It further pushes out your term to clear debt, and/or reduces the equity payout you will get on sale of the property. More debt means more risk, particularly with rising interest rates. People need to remember their lessons on smart debt and stupid debt.

https://www.smh.com.au/lifestyle/equity-withdrawal-what-are-the-risks-2…

The reserve bank gov warned house buyers not to look at the current rates, but what rates could go up to. But many NZers will borrow up to their maximum which is human nature. Then they will potentially overpay just to get on teh housing ladder, due to the lack of supply, as they are likely bidding against multiple people. This is even worse in areas that have Deadline sales or Tenders. It isn't so bad in Auckland because houses are usually sold at auction, so the bidding is fully transparent. If I was a first home buyer I would b fearful of overpaying at the moment. The amount some are borrowing is insane.

I totally disagree with the headline for this article. How ridiculous to even ponder for a moment that house prices may be entering interesting price levels for first-time buyers. Those who believe they're getting a bargain at one/two million dollars or paying $600,000 for a shoe-box one bedroom kiwi build need to check their salaries and weekly expenses. House prices have their foundations on the moon, however salaries and a heavily subsidized economy is what exists here on Earth. And surprise, surprise.... people with their feet on the ground are tuned in to the Reserve Bank which is telegraphing (in advance) interest rate rises from next year. So expect to see meteoric-like trails of burning houses re-entering the atmosphere from the second half of next year on-wards!

Good point pathos it’s not just NZ it’s the world’s central banks who are going raise rates to protect currency if rates go up 3 to 4% I would think a lot of people would go under.You have to wonder if this is just a set up so they can Aquire assets for huge discount when shit hits the fan.

Yes, l have also wondered about their golden opportunity to buy up everything for pennies on the dollar. Personally I believe that is exactly how it is intended to play out. It might

have the appearance of a "buy out" to save industry but private ownership will never return.

Will be interesting to see arrival and departure stats now border with oz is open to see how many kiwis have left long term for oz.or elsewhere

Ive been attending Auctions in Christchurch and from my observation the heat has come out of the market across the board. The bidding wars are simply not there.

Wellington City selling very strange properties now. Badly built shed with 500k of problems still going for 1.2. I think, um winter, and also a lot of garbage selling for a fortune is the real reason for the ‘slowdown’

DP

Now might probably be a good time for first homeowners to buy, but given Auckland prices are so crazy you are far better off coming to Whanganui where you can find a booming local economy and very affordable housing. If you are looking for a houses for sale in Wanganui I highly recommend https://www.whanganuimansions.co.nz Whanganui is a great place to live and bring up a family.

....... if you are in the mongrel mob.

"Join the gang, move to Wanganui" Actually I agree it's not a bad town, with many beautiful historic homes. Beneficial climate.

Plugging ones own business for free! You should pay interest.co.nz to advertise, not rip them off. Are you also the type that puts homemade signs on traffic poles. Nothing against you personally steve however what you did is wrong

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.