The number of homes auctioned by Barfoot & Thompson was unchanged at 165 last week (12-18 June), exactly the same number as the previous week.

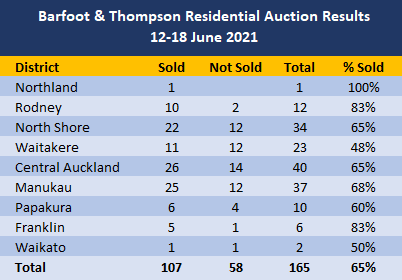

That's down from more than 200 a week over autumn and more than 300 a week in the peak summer months, suggesting activity is settling down into its winter groove.

However while the number of properties being auctioned has declined, the sales rate has pushed higher.

Last week 107 of the properties offered were sold under the hammer, giving an overall sales rate of 65%, up from 60% the previous week.

Over the last couple of months the sales rate had been hovering just above 50%. So in the last couple of weeks the ratio of properties selling at auction has increased from about half to just on two thirds.

That is heading back towards sales rates of up to 75% being achieved in the peak summer selling season.

So while the market has quietened in terms of the volume of properties being auctioned, the sales rate has firmed.

At Barfoot's major auctions last week the sales rates ranged from 48% for Waitekere properties, to 83% for those in Rodney and Franklin. (See the table below for the district by district breakdown).

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, and the results achieved, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

60 Comments

Contrary to some posting otherwise, it would seem that Yvil's observations last week regarding high clearance rates were correct.

It has been made abundantly clear to me over the last weekend by multiple posters that this forum is no longer a place to exchange ideas and help each other but a place to vent frustration, complain and blame.

This is not my idea of participating in discussions and I will therefore now stop posting (but still reading Interest's great articles).

Good luck to you all!

Yet your only comment in this thread is a rant. Goodbye.

CourtJester

Yvil has consistently posts substantiated comments that more often than not prove correct. Pity you didn't consider Yvil's comments last year. That has cost you big time.

Look in the mirror and you will see one who rants (i.e. making unsubstantiated claims). . . and this comment of yours is tantamount to bullying.

"making unsubstantiated claims" - Any particular examples you'd like to talk about?

"That has cost you big time" - How so? Is a loss of unrealised capital gains really a loss? As I wasn't looking for gains, but rather a nice home to live in - but not at the cost of my own financial stability!

You probably didn't invest in DogeCoin a year ago. That has cost you big time.

"Pity you didn't consider Yvil's comments last year. That has cost you big time."

It's this sort of comment that makes me think not worth to come back and comment. It's a pretty bad advice in my opinion to encourage people to invest based on what happened in the past.

Remind us what Yvil said last year? I thought he was quite bearish on housing in the short term, like everyone. He even sold his house, which reinforces he was bearish...

Lets be clear we are in a market where predictions by pets and toddlers are frequently and consistently correct. Discussion about whether that is a market we should have and the damage it does to the people of this country and the economy should be on the table. But right now I trust and have more scientific backup in betting with Lupin and that Lupin has a better strategic plan for the country than Yvil.... and Lupin likes eating earwax.

.

Comment makes no sense, gets 15 upvotes, yeah the butt hurt is real.

Yvil

Do not be bullied; one can ignore it but with any bullying it is best stand up to it.

One can be critical of people's views and posts, that is debate. However it is arrogance and bullying when the likes of al1123 to dictate as to who should leave the site.

Unfortunately many now posting have a definite bias, and the quality of posts has deteriorated considerably. It is important that balance needs to be given to that.

As posted above, despite comments to the contrary your observations at recent auctions proved correct and support this need.

LOL a bully telling another bully to stand up to bullying. Top notch comedy from both of you.

"many now posting have a definite bias" - Hasn't that always been the case? In any forum, ever?

"It is important that balance needs to be given to that." - yet you guys ridicule everyone who was on a different opinion than yours... The irony.

Let's not forget that Yvil sold a house last March, as he predicted that to be the peak at the time - missing out on 30+% gains in one year. By the way this is the first time I brought it up, although could have done so every time he commented since then - as that seems to be the norm here.

True CourtJester, but things didn't look good at the time and he was having a dollar each way bet and was reducing his overall exposure to the property market. He did what any multimillionaire would do if you had that luxury.

I agree, and he probably made huge capital gains anyway. I would've sold too if I had multiple properties.

My point is rather that he was just as clueless as anybody else here re the direction of house prices.

That’s not a very fair assessment, mostly he expected things to be fairly resilient and was otherwise uncertain about direction, which is a much better prediction than most:

by Yvil | 1st May 21, 2:51pm

"Well that's clearly incorrect, house prices are not only, not declining, they are at all time highs. They may or they may not decline in the future but we don't know this now."

P8, please stop lying about me. I did not bully anyone, nor did I attempt to 'dictate' who should leave the site.

Is a different opinion 'bias'? I own a home, I am not a potential FHB, but I know what it's like and how monumentally hard it is. You know, a thing called 'empathy'.

I have nothing to gain from house price increases slowing, other than thinking there might be some kind of slim hope for my children.

If anything, I should be biased towards wanting house prices to continue to soar.

The most frustrating thing with Yvil is his insistence that buying a property is within everyone's powers, it's just BS. There's no acknowledgement from him that actually buying a house was much more accessible for the average income earner when he bought.

A total lack of empathy at play.

I think it's so sad what our country has become - dog eat dog society based on self interest

I couldn’t agree more HM, I too own my home (well the bank does) and if anything I should pray and hope for house prices going up not down but I’m rooting for it to go down because I know the struggle it was for us as decently paid professionals was. I can see couples our age who are yet to buy a home struggle with their mental health being torn to shreds in just my workplace. The race to save for a deposit is tiresome.

I value some of Yvils insights but the lack of empathy, I told you so, I was able to do it then so should you (never mind DTI now is crazy compared to when they would have first bought and they used leverage to buy more and more) to outright condescending statements and putting others down is incredibly difficult to keep bearing.

My granddad would say in my day 20 pence got us so much. Get over it grandpa, 20p means nothing. That same 20p in today’s value will also mean nothing. To pay our mortgage we have 3 jobs between the 2 of us and these condescending comments from property investors with their multi properties milking the tax payer through accomodation supplement is rather getting tiresome.

New Zealand is not what it used to be. Kindness what? Arrogance, narcissism and greed is tearing our society’s moral fabric.

Agreed. A little acknowledgement that pointing out that house buying is really hard even for hard workers who are more than willing to compromise is not 'whingeing' or 'whining' would go a long way.

Good luck to you too! Yvil! I've actually stopped commenting on property section too as it's mostly just real estate agents and house owners sharing their opinions and bias views but not really touching on some other issues could effect housing price and housing investment. But I still come back sometime to read some interesting comments.

Likewise Yvil. Unfortunately, Interest comments have deteriorated to the point you could be reading facebook and that is damning, so I will join you. Gingerninja has gone as well I have noticed. Ka kite.

I agree with that. Definitely deteriorated.

Such a shame the DGMs have hijacked interest to spray venom at everyone that doesn’t follow their views.

I should qualify that my comment is directed at the comments and in no way towards the site itself. I rate the journalism and service the Interest team provides very highly and will continue to read obviously.

This is precisely the type of comments which deteriorates the discussion.

Hi Yvil, I have always liked your comments and I fully understand your decision. It will be a great loss as you are one of the few people, whose comments make sense and I have identified with majority of your opinions. It will be boring from now on. Just lefties, dmgs and unsuccessful people commenting, complaining and hating everybody who is not like them. I am joining you. No more comments from me either. All the best mate and many more successful years to come.

That's a shame. Yvil seemed to have a good logical mind, perhaps just lacking empathy at times.

However, the consequences of the social contract being abandoned in this country is going to ripple out far beyond frustration on internet forums. Enjoy the safe space while it lasts.

That’s a pity, you seem to be one of few that add balance and foresight to this site. Don’t be away too long now.

Agree

Where have the 5 amigos gone?

ALittle Member for 3 years 4 months

taimaiakka0 Member for 3 years 3 weeks

richard1965. Member for: 3 years 2 weeks.

stuart-something

Like a mutual admiration society they act in unison, spraying identical comments that dont contribute anything

They post comments bagging Jacinda, Robertson, Orr, RBNZ, and within 5 minutes have 5 upticks

Must be the one person with multiple personalities

They are collectively absent today

taimaiakka0 Made a comment at 10.01. You can see it below this comment on this article.

Thank you Yvil, all the best. Those who remain will try to make this a better place in your absence.

That's a shame. I didn't always agree with your comments, but always appreciated your input. All the best.

Bye.

Very loyal and vocal advocate for the leverage up they are not making anymore party. Which ultimately is a model founded on profit from exploiting renters through ever increasing rent. Rent set based on increasing debt leverage and further exploitation of the failed supply chain and poor council admin processes vs. the underlying economics of income. Well things are changing. Boris, Trump, Brexit and DTi were all impossible according to this group. Respectfully what they may not appreciate is that the exploited have become a bigger voting group that the leverage exploiters. Even the "younger" economic refugees in Australia get a vote. Fortunately we are still a democratic state were every working age head has an equal vote.

TTP is also contemplating quitting posting here.

TTP

See above. Propertytalk will be your home away from home.

No worries Yvil, guess you can keep posting as Printer 8...

Market is hot and will remain so ......Government and RBNZ wants so will it be.

It's very sad indeed this intergenerational wealth theft we are perpetuating on the young. A sad state of moral character in our country.

Morality is a mental construct. This country is made up of individuals with differing morality models and standards. To say this country have a standard model impinges on individual freedoms and democracy.

Some people loves sex, some other money. Some loves violence and yet others loves being holier than thou.

If there is ever a standard, its the individual freedoms guaranteed by the state.

If there is ever a standard, its the individual freedoms guaranteed by the state.

There's nothing free about the property "market".

More to the point, individual freedoms guaranteed by the state depend on a level of lawfulness. Contemporary accounts of inflationary periods in Austria and Germany highlighted that if you feel free to destroy generations' wealth, their reasons for abiding by these laws that give you "individual freedoms" reduce. Why should they respect others' ownership of wealth when their own wealth was destroyed by the state/financial sector?

Society needs a bit of reciprocity, mutual benefit and balance. Without that, it's less stable.

The last time I checked, buying houses is absolutely legal. To suggest the lawfulness of an act is subjected to further interpretation based on ambiguous moral authority rather than the parliament is pseudo-legal and the style of woke. The latter is the true reason why our island is ages behind the rest of the world in every aspects except for woke.

Missed the point: a free market is one in which prices are allowed to go both up and down, not one subsidised and protected in many ways from price discovery.

Blather about woke is mere blather, and everyone is aware law is distinct from morality.

I agree Rick there are certainly subsidies and protections for the housing market, the central planning exercised by the RBNZ ensures this. Having said that even without that interference price discovery would simply have a lower floor, the limited supply of housing to the demand would still mean it was expensive.

It's never a cheap purchase, yeah, but without the amount of support we give it now in subsidies, monetary support, tax favouritism and zoning constraints we'd certainly have far more affordable housing. All of these preserving high prices and portfolio wealth instead of a free market.

We at least may as well openly acknowledge that we know how to make housing affordable, it's just not our policy to allow that and it hasn't been for a while now. It's a wealth transfer scheme more than a free market.

Yes- and its particularly galling that the beneficiaries of this intergenerational theft seem to be of the view that the wealth they've gained from it somehow makes them morally and intellectually superior than those they have effectively stolen from.

......just sitting on the hill ...smoking peace pipe ...mmmm ....looking..... watching ....observing ....where all those buyers.at these market prices, for all these townhouses of 6 or 8 replacing the ol' state house on that big section ? .....also heard via the smoke signals across the valley that the margins on these developments are reducing day by day ..... interest rates are yet to rise ........ the bank always wins .... what a way to run a country based on fear and greed ...... ponder that ....

Talked to several very active building suppliers and developers yesterday. They are seeing every cost rising. One called 20% by year end, the other say 10% this year and 10% next year.

Interest rates staying flat anyone...?

Not really sure about the value of percentage sold statistic and its direction - at least not in isolation. A higher sales rate could be an indication of sellers being more willing to accept the offered price. Perhaps thinking that they'll not get a better price than right now. Equally, it could be a sign buyers getting more desperate.

Its time Interest.co.nz had more input from the moderator and posts got deleted. I belong to a couple of Forums and none of this personal stuff would be tolerated. All posts need to be kept on subject or they are gone. Personal attacks are a no go zone. If you cannot add something constructive, keep quiet and just read, maybe you will learn something from someone who has been there and done that already.

100% agree. I've been reading the posts and comments for years but almost never comment myself. My mistake was using a women's name. Cue "make me a sandwich".

It's going to be a hot summer, I still forsee 15%ytd Feb to Feb 2022 possibly more

You are probably not taking into account growing interest rates, recent government changes affecting investors, LVR restrictions and likely introduction of further DTI ratio restrictions. It will be a very different summer than last one, but time will tell.

Yup I am, even with a 1% increase its cheap money

Growing interest rates.. only if you fall for it and take the long fixes, at the short end they are still heading down.

True but only for short term rates like 1 to 2 years. The worry is where rates will be in 1 years time. I would still have been taking a 5 year fixed. Its piece of mind and you can plan for the payments.

My reasoning is this: I've done a thorough budget and can comfortably (including having money for travel, renovations that are a want rather than need, etc) afford my mortgage if rates went to 6%. Given that, im comfortable taking the gamble on short term rates (I think!).

Nah I’m happy rolling the 1 years. They are much less than LT rates and look to be staying that way and even going down further.

Everyone’s talking rising rates so the banks plY on people paying premium for the longer term certainty but they miss the cheap rates that will be around a while yet as a result.

That’s my view but I could be wrong.

We're coming off 3.79% and going to 2.35% and increasing payments. We'll survive if rates go to 5%, but would probably move back to the full term of our mortgage, but many would be tightening their belts hard if the rates start going into the high 3s, low 4s, no more renovations, new cars, eating out etc, and there goes "maximum sustainable employment" so the RBNZ would have to kill off any further rates increases.

Other option is inflation is strong and leads to wage inflation, which makes the increased mortgage payments affordable anyway. Thats probably the best answer for recent buyers.

Nobody takes a mortgage for 1 or 2 years so your argument does not hold. Eventually you will have to choose a rate that is higher than those we have now. There's no doubt about that.

And wages rise, so the cost of servicing the mortgage remains affordable,

I really wish you would be right. A couple of percentage points in the interest rate can result thousands dollars a month, so it will be hard to keep the pace.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.