The much anticipated decline in residential property values appears to have started in February, according to the latest data from Quotable Value (QV).

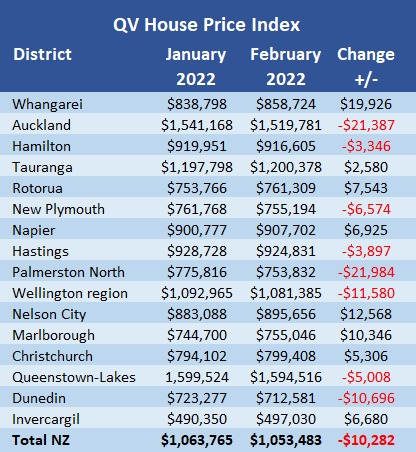

According to the QV House Price Index, the average value of all homes throughout New Zealand declined to $1,053,483 at the end of February from $1,068,765 at the end of January. That's a decline of $10,282 for the month.

That reflects falls in average dwelling values in Auckland, Hamilton, New Plymouth, Hastings, Palmerston North, Wellington Region, Queenstown-Lakes and Invercargill, while average values in all other districts continued to rise, although generally at a slower pace than previously.

The biggest monthly decline was in Palmerston North where the average dwelling value declined by $21,894 in February, while the smallest decline was in Hamilton at $3346.

In Auckland the average dwelling value fell $21,387, and in the Wellington Region it was down $11,580.

The slide in values appears to be particularly well established in Hamilton, Queenstown-Lakes and Dunedin, where average values have now declined for two months in a row.

However given the very strong growth in values that occurred last year, the drop in values so far has been comparatively gentle. Although the national average dwelling value dropped by just over $10,000 in February, it would still need drop by more than $50,000 to go back under $1 million.

That may not be as unlikely as it seems.

The QV House Price Index is a rolling three month average, and house price growth, which feeds into the HPI's average value calculations, was particularly strong up until the end of last year.

That means the value falls evident in February's figures would have been mitigated to a significant degree by the strong price growth still evident in December.

"The strong December numbers are masking what's really happening out there," QV General Manager David Nagel said.

"There are less buyers out there now, with the tightened credit rules and rising interest rates taking a number of first home buyers and investors out of the market altogether.

"Increased listings from both new builds and existing homes are providing the dwindling buyer pool with ample choice and this is putting downward pressure on prices.

"It's taking a lot longer to sell a house this year, with open home attendance and auction clearance rates significantly impacted.

"While part of this may be attributed to Covid-19, primarily we're seeing a residential property market that has peaked and is searching for the new equilibrium, Nagel said.

That makes it likely that the slide in average property values that began in February will intensify over coming months and spread to other districts that are currently still showing growth in values.

The comment stream on this story is now closed.

86 Comments

All things considered the housing market has been more resilient than I expected. Runaway inflation hasn't triggered the short-term impact I expected it would. Maybe it was so long ago it was out of peoples memmory but last time CPI inflation was at this level Reserve Bank rates would have been over 10%, I think?

That said I'm still glad I'm not holding any investments in local housing. Something has to give and there clearly won't be a smooth landing.

Early days - it’s really what happens over next 6 - 12 months - I predict 20 - 30% down on Dec.

If certain assets are ‘markets’ nobody should be surprised if prices go up and down - not a one way bet surely?

Look at the up to date data - this stuff is stale as last week's bread. The REINZ figures due out next week will likely show a third consecutive month of declines.

Yes, but don't bother reading the REINZ commentary. Last month in our region all the indicators were heading downward but the commentary was all positive. It was like they copied and pasted last years comments.

Smooth landing for the regions I think. I have given up predicting large drops in house prices it simply doesn't move as you expect it would.

We've been living on borrowed time and printed hope for the last 12 years.

Those who got in, cashed out, paid no tax and made a killing have done well for themselves. The rest of us who were in the following generation now just have massive mortgages and soon-to-be devaluing homes. The party couldn't last forever, but the people running it made damn sure it ran just long enough for them; the rest of us couldn't put our lives on hold forever waiting for a return to sane prices, especially when the government is prepared to almost anything to stop that from happening.

The flow-on effect of smaller and deferred families, a huge drop in discretionary spend and an outright flogging of the middle class is going to have repercussions for decades to come. Buckle up.

You forgot to mention the collective debt.

On slightly more housing numbers there is now double the total debt owed. Hence the $6B plus that the banks are sucking and will continue to suck out of the economy and it will grow bigger for absolutely no gain. We can blame government all we like but but really it's a collective choice we have made.

I'm not sure how 'we all made' this choice. Like I say, I wasn't born early enough to plunder housing for tax-free gain, but I either had to play the bounce around flats game while prices exploded and put off a family even longer, or bite the bullet and take on stable accommodation at some point. Not much 'choice' there, realistically; just choosing between the lesser of two evils. And all the while, being lectured about how it was just a case of having to work harder or have fewer takeaway meals (bit hard to cut back on zero) and then everything would be magically fine.

It’s a cruel situation that younger people shouldn’t have had to face. Yet there was for the most (with exceptions) little to no interest in actually doing anything politically to resolve the problem. There still isn’t…#shameful

Right...now, young Kiwis, get out there and work to pay universal welfare benefits to older property investors! Hop to it!

Collectively maybe a better description. I failed to go down the property road and will pay a price as I head toward non-retirement without a house.

We do have to accept that it's a democracy we live in and and our general direction is a majority decision.

Yes, it's 'Us'.

In a democracy that doesn't mean everyone, it means the majority. We get what we want, and we get what we deserve.

As long as humans walk the earth, self-interest and short termism will rule.

"we have all made" lol

Renters included? People that just need a roof over there head?

At least it will be safe to vote TOP now as there won't be any equity for them to tax. I like their other policies.

“The flow-on effect of smaller and deferred families, a huge drop in discretionary spend and an outright flogging”. Like renters have had for many years now, right? Though without the security, having a place to call your own etc. Its not fun. I wonder how long before rents and mortgage payments are roughly similar again.

I was actually believing NZ was different, and we are nuts, to have such unaffordable housing. Now I hear from estate agents that people are afraid to pay more and see house prices drop afterwards. Is it smooth like a steep incline of a ski jump. First it was FOMO now is it Fear of losing out. NZ'ers are certainly not logical home buyers.

Markets move in cycles as credit expands and contracts. The gleeful headlines tracking month on month movements up, down or sideways, what's the point?

CWBW alive and well? I'm concerned.

I'm concerned for TTP

He's been trying to sell his penthouse apartment in Palmy since August.

https://www.trademe.co.nz/a/property/residential/sale/manawatu-whanganu…

Hopefully he glances over the fact that Palmy had the biggest drop nationwide

You don't often see penthouse and Palmerston in the same sentence !

Unless it's magazines under student beds.

Magazines? Haven't they been replaced with an incognito tab in the browser.

By reading the comments here you would have thought that house values had dropped by hundreds of thousands already...

Some are saying Auckland prices are down 10% which is over a hundred thousand dollars. Not an insignificant sun for younger people trying to save a deposit (nor principle to pay the next 30 years). We should all be celebrating the move back towards affordability (in deposit terms)

People are saying it but it hasn't been reflected in the data yet. It's refreshing though to finally see an average price drop, all be it just $20k in Auckland...

"The strong December numbers are masking what's really happening out there," QV General Manager David Nagel said.

I wouldn’t look to these figures to get the most up to date picture of what is happening. REINZ HPI is out next week which provides a bit more granularity, but also obtains data when the sale goes unconditional . I believe QV is similar to core logic in that the data is captured when the transfer of ownership is completed

Tony Alexander says in OneRoof today that prices are down 5%, so far. Which sounds about right to me.

He's still sounding far too bullish in terms of where prices go to from here.

If him and Ashley Church are the 2 most qualified property experts around…. I reckon a couple of us should get some badly fitted suits and curly brill creamed hair and set about guessing.. based on “cyclical historical data”. It’s like having a pet grizzly bear and saying it’s never bitten me, right up until the moment it rips your head off

Haha funny

Rates have a big chunk to climb yet to have any chance of of restraining inflation. The bubble will leak until the banks start mortgagee sales. Then it's all on.

Mortgagee sales will take a while to culminate.

Households struggling with stretched budgets and higher rates will be forced to cut back on discretionary spending. That could spell a death blow to hospitality and local tourism sectors that are already on borrowed time, and RBNZ cannot print their way out of this mess.

Kickstarting low-skilled migration could help businesses cut wage bills but high migration will put further upward demand pressure on consumer prices.

If the RBNZ wants to run its money printers again, it should follow the Aussie Libs' (or was it another party?) plan of a per-adult grant: for FHB, to reduce debt; for low-income families, to help get them through hard times; for property speculators, to be applied to their portfolio debt; for all, to reduce overall debt.

Per adult, not per property. Speculators wouldn't be protected and coddled from all risk, as they have been to date.

Lagging indicator. Prices in Auckland and Wellington are already 10% down on peak prices.

If you manage to sell them, that is. Inventory growth seems to be as infectious as COVID.

Just installed: New steepest slide in Auckland, aka Property prices

This Weeks Hutt Valley Update ( for those who have seen my weekly updates)

594 houses on the market (at the beginning of Nov just 320 houses were on the market and that was considered a lot). Likely to break the 600 mark today or tomorrow.

Still waiting on REINZ data but it looks like just 30 a week are selling - so that's 20 weeks stock available. Average sales per week in 2020/21 were 40 - so at least 15 weeks stock if using last years sales numbers.

380 of the houses have been on the market for over 30 days - 64%

174 of the houses have been on the market for over 60 days - 29%

238 of the houses have a price on them - average price reduction since listing is 74K - with a number of houses dropping prices by up to 300K - one has dropped 400K from $1.9M to $1.5M

I started recording QV valuations on houses for Sale in early Dec and those same valuations have dropped by 60K since Dec with an average 5% reduction in value. Approximately 20K a month is coming off the valuations.

Rental Market

Meanwhile the rental market has 155 properties for rent (this is quite high typically the number properties for rent are 110-120 at any given time

A number of brand new townhouses are coming to market - of which are handful are offering the first week rent free in order to get them rented.

in the last month Five houses that were for sale were removed from the market and put up for immediate rent.

^ Best poster on Interest. Thanks for sharing.

thanks Fergus- the hutt valley feels like the canary in the coalmine- its been named by corelogic as one of the 4 NZ housing markets most likely to correct - but its also fascinating how quickly its correcting

I put it down to lots of supply (due to big blocks been converted into townhouses), cheap enough for first home buyers, but also some high value suburbs like Petone, Eastbourne and Woburn, demand falling combined with 50-60% price increases since 2019.

Don't forget the new ones that have come up since mid-last year are considerably smaller with zero open spaces.

Drive around Hutt and you will see plenty of newly-built shoebox apartments that open on the street. These come without parking spaces but just enough land to secure your bins.

In November last year, one developer listed their 1-bedroom townhouses in Taita for $700k. We're talking 1-2 decile schools in a neighbourhood dotted with people drinking beer on their front lawn on a Tuesday morning.

Agree - the ones on high street in central hutt are just awful - zero character.

Nice work mate. Are you seeing any price reductions on offer for any of the new townhouse projects?

I have seen price reductions in the order of 5-7% on a few townhouse projects up here in Auckland.

Off the plan sales are stumbling big time.

Sorry thats the one area I don't record the pricing for - I only record prices on the existing houses - mainly because I also do a comparison with the RV's and the QV. New houses have neither.

What I can say is they still seem to be selling okay I can tell this from the "sales data", although only about 15 sold in Feb which could indicate a slowing. It should be noted there are fewer houses selling with big blocks ideal for development (than there were pre xmas) and fewer Development approvals made by Hutt council- which would indicate that there may be an oversupply of houses or developers and waiting due to the costs/ risks of building at the moment

Hutt City is due for rating revaluations this year I think.

That will be interesting if they revalue at higher than current sales prices. QV might have to deal with a lot of objections.

Masterton: 12 + Months ago when we were initially looking to upgrade, the number of listings (all property types) on Trademe typically hovered around 100 to 120. Houses would be sold within 2 weeks, open homes were busy.

Today there are 221 results. Starting to see more "priced reduced / was xx now BEO xx" listings. There's a few properties that were for sale when we sold in November that are still on the market. Good first home buyer properties less than a 10 minute walk to the train station to Wellington. The property we sold had 3 open homes, 4 people in total showed up and we received one offer at Deadline.

Fantastic as always

ikim I would gladly subscribe to your newsletter if you had one.

Unfortunately not, you could call what I do a part-time hobby : - I have an economics degree and Housing markets are a fascinating part of Macroeconomics, mainly because it creates wealth perception which drives consumer spending. )

I was a bit frustrated with the data coming out of the market (from economists and real estate agents) and thought I'd check for myself what was really happening . I started recording my data this time last year and have added to my metrics significantly since Oct when I could see the housing supply really increasing.

It's a manual process hence why I only take a small segment of the market- the rest of the market is way too big to do that, but NZ has lots of data in different places that can be pulled together to form a picture.

Enjoy your posts. Actually growing quite fond of Hutt Valley.

I am just not seeing a major correction here. If one was to happen it will be short lived as time and time again RBNZ has swooped slashing interest rates and LVR ....... very skeptical.

Could be, but if Orr slash's the OCR again all imports take another massive price hike. $5l petrol anyone and rampant stagflation. This is the rock and a hard place that many now face. NZ is no different.

Wasn't his excuse that his remit is not housing. So if its not housing, then he should follow this. Unless something has changed.

"We use monetary policy to maintain price stability and support the maximum sustainable level of employment as defined in the Remit. The current Remit requires the Bank to keep inflation between 1 and 3 percent on average over the medium term, with a focus on keeping future average inflation near the 2 percent target midpoint. We implement monetary policy by setting the Official Cash Rate (OCR), which is reviewed seven times a year."

Yes but he also has to worry about the solvency of the banks and the consequences on a housing crash would be very severe - which he can cause by raising rates too quickly obviously. Then again, they created this mess after doing insane things like removing LVR's and dropping rates to zero and seeing house prices rise 30% in a year so I feel little to no pity for them in their role and the corner they have backed themselves into.

I know I am a broken record, but residential construction is extremely fragile right now. Yes the data is still strong but it's lagging.

Aggressively hike the OCR and the sector is goneburger, and watch unemployment soar.

Having said that, unemployment is ultra low, maybe the path of least regret is to hike aggressively, then pull back if the impacts are getting ugly?

I think if the Fed raises then they will follow. As 2000 and 2008 show, the Fed really don't care about markets.....even though recent traders will believe otherwise. They have raise rates to counter inflation in the past during those periods and the markets have subsequently crashed.

Could well be right. And my bearishness on the OCR could be very wrong. If I am wrong, then the economy is going to be in big strife. And the housing market.

I think it depends how quickly the recession results in deflation. If oil and food prices continue rising through the recession as a result of external issues...then no idea what might happen.

Not necessarily pull back... Just hire them all into Kainga Ora as a start of a new Ministry of Works. Get them working on both infrastructure and new housing supply to start resolving the big problems we have in housing. Work on the problem of housing affordability just as we used to do in the post-war decades when the idea was to enable average hard-working Kiwis to afford a home, not to enable young Kiwis to pay ever more for the same houses.

I don't know - the world seems to me to have changed. I've got a funny feeling that if oil prices go through the roof - eeeks. Americans are complaining like mad at the moment - and that's only the COVID-affected supply issues that are causing the relatively minor hikes. Next shock re Russian supply will be a bit of a big boom, I think.

With the war now tacked onto what looked like the end of Covid, this "short term inflation" is now long term inflation and its not going away anytime soon. Prices simply never return to where they were, look at petrol prices in 2008 when oil was this price now and compare. Something now has to give, the market is unrecoverable without some sectors taking a hit.

I think Orr will consider a 30% fall in house prices a soft landing, and if it happens it will likely be spun by many as such.

It only wipes out the last 18 months rises which were artificially stimulated by the RBNZ slashing the OCR, LVRs etc when they didn't need to.

Is going back to 2019 values a disaster?

Yes, it wipes out paper gains, and equity if you leveraged and bought within the last 18 months. But that's a small percentage that will unfortunately have to be sacrificed for the wider economy and inflation.

Re: the Banks - it will be like when dairy farm values took a big hit a few years back. The won't want a rush of supply and mortgagee sales for owners underwater. Owners will be fine and banks will let you keep your home as long as you can keep paying them the interest. That's all you are basically doing for the first 10 years of a mortgage anyway.

So it will only get interesting if retail rates go above their stress tests of 7% and inflation gets so embedded in everything and so rampant that it cuts hard into your ability to service your debt.

The other view, is our economy is a house of cards built on a belief that house prices can never fall and as such the impacts of the reversal of the 'wealth effect' will wipe out confidence in the whole ponzi scheme that has driven us to having most of the highest unaffordability metrics in the world.

Unfortunately our mainstream media has been a propaganda machine for the housing industry saying a crash (more than 20% fall) could never happen again (like it did with a 38% fall in the 70s) and prices only go one way. They even admit as much.

Ashley Church, July 2021 - "If I look back over my various OneRoof articles over the past few years, it’s apparent that a sizeable proportion of them are about the possibility of a housing market crash – or, more accurately, me responding to claims that a crash is imminent by reassuring readers that it isn’t."

https://www.oneroof.co.nz/news/ashley-church-everything-you-need-to-kno…

I think that's what we should really be waiting to see.

Yes it's the wider economy ramifications that are the biggest concern arising from a house price crash. The majority of our domestic economy has been predicated on a rising property market.

It will be very ugly, but we need this crash to reset things. And learn from.

I learnt a lot from the problems in 06-08, it totally informs my worldview to this day.

I learned a lot from losing $40K on a house in the UK in 2008, and seeing the Ireland housing crash. But I was always told that NZ was different and lessons learned overseas didn't apply here. Fortunately I didn't listen to the likes of TTP so I bought within my means and kept my debts low. Being risk averse means missing out on the boom times, but hopefully keeping a roof over my head in the tough times.

The thing with ttp, he is not giving his opinion but pushing his agenda.

The fact that he's so bullish property long term... yet, still trying to flog his apartment (after it failed to sell Sept last year) should give you a clear view on his opinion of what the market is really doing. As chairman of a nationwide chain of RE agencies, he can see it daily at the coal face.

It's like Adrian Orr stockpiling fuel, gun's and gold!

Chruch more or less implies that a crash is due and gives an example of the mid 70-80 crash post the doubling in the early 70s. "But don't worry, over the long term it will bounce back" he quotes.This assumes you survived the following decade of tough times including the 87 crash. Probably fine if the yield support the debt, but problematic if you just focused on unrealised capital appreciation.

"Unrealised" being the key word.

He said a crash was 'highly unlikely, although not impossible'.

The use of the word 'highly' was ill informed.

.

Agreed. Last years gains were all totally artificial from Orr's poor decisions on lowering deposits, and stupidly low interest rates. If rates get to seven, and IMO they should already be there, then that combines with rampant inflation will be very difficult for many to deal with. Congrats Mr Orr, a real mess with the best outcome being extended Stagflation.

Creating stagflation should result in the immediate resignation of any RBNZ Governor.

With my valuer hat on, and my dad and uncle hat on, the market clearly needs to fall at the same rate it climbed at last year (around 2% per month) throughout this year, and this would only be a moderate correction.

What should happen after that, is for it to stay flat for up to 5 years while inflation ticks up at 2-3% per year, sending the correct message that successive governments have been too afraid to say- that is, the housing market's primary purpose in a fair society, is to house people, and is no place for speculation.

Will it happen, without state interference with another election coming, unlikely. The only glimmer of hope is that our govts (Nat or Labour) dont really have the skills to truly manipulate markets as there are too many moving parts. A good solid correction which frightens speculators away for a long time would be the best thing for our society. I really hope and pray it happens.

Don't think the housing correction is going to happen. We are going to suffer instead from high inflation and food and fuel prices going to the moon. The RBNZ has to choose a path now because it cannot save everything this time. Clearly its already deliberately dragging its heals on raising rates so the decision has already been made, its save the housing market.

I've got some bad news Carlos. It's not going to be one or the other. It's going to be both.

I guess we only have another 3 or 4 months to find out. Hardly a crash at this stage of the game but its looking like a dip.

It seems like you've really convinced yourself that a housing correction isn't going to happen! On the basis that you thought it would in the past, but it didn't.

Well, this time it is different.

Time to re-evaluate, Carlos.

Been here before HM when it should have crashed 25% and look what actually happened. As above, lets see where it actually is in 3 to 4 months time.

I think it comes down to how much the RBNZ hike the OCR.

If they are timid, as per my prediction, then it might just be a correction.

If they are aggressive, as the vast majority think they will be, then I think a crash is all but guaranteed.

It's amazing how optimistic the property DGMs are...how many times over the last couple of years have Orr, Robertson & co protected the market? They've done the opposite to what they should of and are never held accountable.

Current housing prices and valuations are a farse, full stop.

Even while adopting a "conspirancy theory" that helps the people in charge it is a ticking bomb. Even for them.

If anything, they will give to hemselves the time to exit first.

We got space, a lot of it, scarse population, negative birthrate, negative migration of well paid talents, 3-5 years of new builds to come, superlow unemployement (which means that can go only down), home ownership mostly represented by old dying generation with less and less political influence, remote working is a reality (who cares where you live as long as you have wifi)

Game over

I find the increase in the RV of only 15% in the Waitemata area really hard to believe, prices have gone nuts and my own house has increased 53.3% as an example

You can dispute it and get your RV higher than everyone else to pay more rates?

Queenie only taking a $5k hit, probably off a low sales base. This stuff is kind of numberwang.

Yes indeed, all smoke and mirrors as not much quality available on the market down there in Queenie at the moment - I know as have been looking to buy. The next auction will likely have a 70% plus clearance rate and that will put the above figure in positive territory again soon.

Had another visit to Te Awamutu today and visited as usual the new Frontier Road subdivion.

New 3 bedroom home with 2 bathrooms with 1 and a half garage $980k.

Insane yet in 2/3 years the whole subdivision will be full of million dollars plus homes.

Wow...that is incredible. And utterly dependent on personal car travel.

I guess they do have a train station that could be reopened in future...

What about the possible impact of demand from people /expats coming home to escape the carnage overseas and seeing NZ as a little haven? I sure am hopeful it doesn’t end up in a 30% decrease but I suppose I am relatively young and should just buy the dip.

safe from what? why would expats be coming home? for massively inflated house prices? for lower wages? or maybe for the highest per capita covid case numbers on the planet? or maybe to be closer to the retirees and beneficiaries.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.