Housing confidence has dropped to a 26 year low ASB says, with the bank declaring the housing boom over.

According to ASB's latest Housing Confidence Survey, the number of people who believe it's a good time to buy a home is now squarely in negative territory.

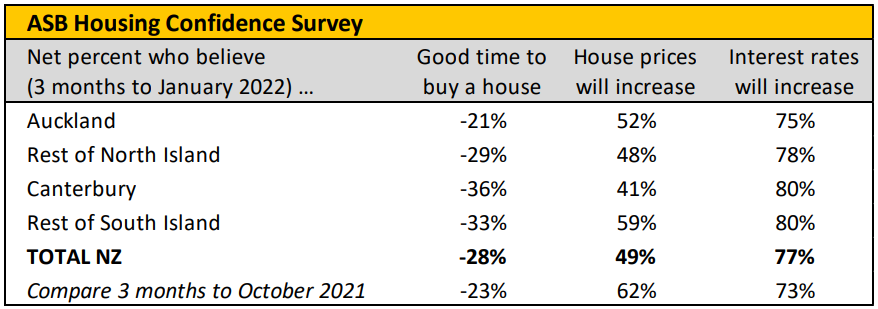

The survey, undertaken over the three months to the end of January, found that 28% more people believed it was not a good time to buy a house than thought it was a good time to buy.

That was the lowest level of housing confidence in the survey's 26 year history.

Conversely, 77% more people thought interest rates would continue to increase than thought they wouldn't increase (see the table below).

"The housing boom is done," ASB senior economist Mike Jones said in his report on the survey's findings.

"The weight of recent housing data and the thrust of views from the economic commentariat increasingly point to a period of modest declines for NZ house prices.

"We've long warned that 2022 would be the year the shine comes off a little.

"But while the boom might be passing, there's still the hangover to deal with.

"Buyer sentiment hit the lowest level in the 26 year history of our survey this quarter.

"Stretched affordability, rising mortgage rates and tightening credit are not the makings of a happy home buyer.

"Respondents who think it's a bad time to buy now outnumber those saying it's a good time by five to one," Jones said.

However he did see the possibility of market sentiment turning again by the end of this year.

"If house prices do back pedal a little this year and wages jump as we expect, housing affordability should look a little better by the end of the year.

"The Reserve Bank is already well into its work in removing the stimulus that helped push housing and broader inflation to such heady levels.

"Respondents to our survey overwhelmingly believe there's plenty more work to do.

"A net 77% are expecting interest rates to keep rising over the coming 12 months, a record high," he said.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

92 Comments

"However he did see the possibility of market sentiment turning again by the end of this year."

I guess a 0.1% chance is still technically a possibility.

The banks are hell-bent on trying to control the narrative to wish into existence a soft landing. But all the signs are pointing to solid bedrock not feather pillows.

Personally I think Housing is a Confidence Trickster Ponzi Scheme.

Banks love to have you at their mercy for 30-40 years...I think they call it a Mort-Gage.

That is why they fiddle about with the munny supply. ....to make Billions....on Paper.

Borrowers should be told the latin origin of the word mortgage- it is "death-pledge"

Je pense que l'origine est plutôt française: mort = death, gage = pledge

C'est bien ça

..more like a Mort - Cage.

Mor- Daunt

Brilliant - and not lost on me.

"Rort-Gauge"?

The on-going shortage of dwellings, favourable labour market conditions and house-owner determinedness to keep their property will signify the current downtown as a correction - and not a crash.

Nonetheless, their will be good buying opportunities for counter-cyclical investors - with an eye for a bargain. 🤠

TTP

Bahahahah

Yeah, bargains like a penthouse apartment in Palmy that doesn't have views of the windmills.

Determined home owner Darryl will feel 'the serenity' of a dead central city but he won't be able to marvel at mans ability to generate electricity.

But in 20 years time he might be able to say it's worth almost as much as he paid for it.

and they will be able to listen to the serenity.

LOL,

we got to the point a couple of years ago where the Herald would run headlines like "couple aged 26 and 28 bought their own house without any parental help"

It was like they should be NZs next Y-list celebrities doing live personal appearances at O'Flanagans Bar in Papakura - "look its the girl and boy who bought a house all on their own - get a selfie!" "I love what you did only eating oats for 2 years"

When all the Mums and Dads have tapped out at the top, when its gone too far, you know its a done game.

Based on the experience of the past few years - if the banks are stating that the boom is over - you can safely bet its not!

Hmm, "that is why they fiddle about with the money supply". Really Alter? "Banks" fiddle? No, they don't. The Reserve Bank of NZ fiddles, commercial banks have nothing to do with it.

I love how 52% still think house prices will increase.

Oh sweet summer child. Reality about to smack a lot of people in the face.

*Net 52% think house prices will increase, i.e. 76% think they will increase and 24% think they will not.

Even dumber.

Don't be too hard on them, the narrative has been drummed into people by the MSM, banks and the Real estate lobby over the last decade.

Of course Toye, and you know more than the majority of people I guess.

All depends whether we get wage inflation or not. If people realise that 25 south pacific pesos an hour no longer cuts it and push for more pay, then rising incomes make servicing the increasing mortgage payments not so bad, and prices stabilise.

Hope springs eternal reality is a bitch.

It doesn't affect me personally, I'm doing well lately thanks. A promotion and large pay rise, and aggressively paying off the mortgage before that mean we aren't in any way worried.

But inflation is here, and it will feed through to wages, the only question is how fast. Everybody I know that has gone job hunting lately has scored significant increases, so it seems skilled middle income and above earners are doing okay, just not too sure how things at the bottom are. I'm wondering how long before teh public sector pay freeze gets defrosted, once that floodgate opens its all on. Every Mcdonalds i've visited in the last few months (a few too many tbh) has been advertising for workers, how long before they have to raise wages to get the staff they need?

Shore thing - Same % as voted for this clown Govt so no surprise.

Deluded masses!

Property is the opiate of the people!

I'm still going single digit growth in house prices for Tauranga for the whole of 2022. Not really bothered if I'm wrong, its a prediction. What I know is its not going to drop back to below what I paid for it so its doesn't really matter.

I was more interested in the 23% who think interest rates wont rise.

I wasnt sure i f the people answering meant for them personally as they either didnt have a mortgage or had locked in for 5 years - or they just lived an a world with no newspapers and no TV

Expect to see mounting pressure on Prime Minister, Ardern.

We have a huge amount to thank her for - excellent, responsible management of Covid - and she deserves to see out the current Parliamentary term.

But the forces of change are becoming evident....... Things will become tougher between now and October 2023 - and ripe for a change of Government.

TTP

If the government is getting the blame for circumstances beyond their control, can they now claim credit for fixing the housing market. Much of their core vote wanted falling house prices. The majority of NZers are not property investors.

Pretty dumb comment Waikato. NZ home ownership rate sits around 65%. So the majority of homes are owned by non-investors. So to say Labour's core vote wanted house prices to fall, is nonsense.

Prefer Labour to National just based on now and hopefully a large drop in the house market. Not to mention Covid response has been great from my perspective, triple jab myself , kids have had shots. Overall pretty happy. Just wasn't happy with Orr and the huge uptick in house prices not to mention huge amount of immigration continuing from Labour. But if I was judging today, based on Covid and rampant inflation, I'm not sure how much National would have done better other then try and make Luxon richer with his 7 houses, increase immigration to aid business's that want cheaper labour.

Excellent, responsible management of CoVid? There are many that think otherwise TTP. Massive government debt, rampant inflation due to Government printing billions of $, societal division among other things that were not so responsible and not so excellent. Future generations are going to have an insane bill to pay for the excellence and responsibleness of her response.

And contrary to you, I think she is the most inept PM we have had in my lifetime (which stretches back to Nash). I'm not sure I have ever seen someone so out of their depth in any senior position (same could be said for pretty much every member of her Cabinet). She's actually an embarrassment.

This turn in sentiment is long overdue- NZs fragile economy has been too reliant on housing for too long. The other risk is of course reliance on China for dairy. Kiwis dont seem to realise how much at risk we are. It is high time we diversified, especially with Chinas desire to advance across the South Pacific. Upset them and then how will we balance the books?

Add to dairy, red meat and logs. And unfortunately there are very few alternative willing buyers.

Just shows the lack of financial literacy in NZ. People don’t seem to understand the linkage between interest rates and house prices. I can’t see how you can have interest rates heading towards 5-7% and yet people still think house prices are going to keep rising.

If you think there is a lack of financial literacy in understanding the link between interest rates and house prices, well these people look like geniuses compared to those that not only do not understand the link between restrictive policies(most noticeably land policies) and house prices, and those that also refuse to acknowledge the link because it gets in the way of their vested interests and/or idealogy.

And that interest rates play a far minor role when the other restrictions are removed, as is shown in jurisdictions that have presumptive rights to build.

Even fewer see the looming liquidity crisis + recession = something very ugly.

Really ? I think if you check the historic long term average mortgage rate its at least 6% and house prices have done nothing but rise for the last 40 years. Something really big has to upturn the apple cart and its possible that we are seeing that with the war in Ukraine and we are all in 10 times the trouble we are now if this thing escalates and the apple cart will be hit by a ballistic missile.

Any stories out there of purchasers managing to use a sunset clause in their favour yet?

Love the picture. A cute house with good bones needing a small makeover? And really affordable for first home buyers at only $1,500,000.

check out all that indoor/outdoor flow, you can take that to the bank!

"Well Ventilated Character Home" seeks inspired young couple for minor renovation, you will be sitting on a goldmine. Secure your future now!

You forgot open-plan living. And stunning ...

Would have made a great rental if this Government hadn't insisted on making homes warm and safe!

And without all those pesky regulations the rent would have been $2 less a week too.

I know. We need our Freedom back. The freedom to charge what we like for a freezing fire trap and the freedom to make money out of people desperate for a roof over their heads.

I don't know what this country is coming to ;-)

Or EQC and/or insurer.Combination of deferred maintenance & cosmetic damage, well under cap. Here’s $115k & consider yourself lucky.

Well, it's all over baby blue, the FHBs have at last achieved their goal. Well done. I genuinely believed this wouldn't happen so quickly; so well done Jacinda and her government. The opposition would never have wanted or been motivated to do this.

So fare thee well FHBs and enjoy your new home.

I suppose you all want to live in Ponsonby. Be realistic. Perhaps Glenfield or Pakuranga to start with.

And also thanks to Greg whose job is now done. Thank you Greg for all you have done on behalf of the FHBs.

Now can we all talk about something else.

I like to see people talking about this one, and I like to talk about it too. The best part of a bad dream is when you wake up.

You are free to not join the conversation if it bores you, of course :D

If the OCR touches 2% in the next three announcements, then this winter will push back the property price from 5% to 7%.

Dare I say for every 1% increase in the OCR there will be a 10% decline in prices for the average Kiwi home. So thats 100k off each full percentage rise, roughly .

And with inflation running at 5-7% by then, net zero effect on real house prices.

Faced with the new reality, the next stage for the denialism crowd is accepting that the end of a boom does not end with a levelling off at the peak - but a roller coaster back down to earth.

Well, there are still some strong spruikers trying to hold up the market..

The data presented here have little value as they were collected in the period November to January. the world has changed since then.. Tony Alexander's data are much more up to date.

KeithW

Dead right, the narrative in main stream over those three months was still largely positive spin. Next three months will be a 360.

Even if there is a price correction, the main point that is still overlooked is the underlying dysfunctionality that allows a boom and bust system remains.

All the politicians offer is just a rinse and repeat once the dust clears.

Capitalism relies on boom and bust cycles. Constant growth isn't sustainable as the money runs out. Gordon Brown once declared the end of boom and bust in the UK, he was wrong. Once prices look like a bargain and yields return, those with cash will start to buy and the market will pick up again. Could be next year, could be in 10 years.

'Capitalism relies on boom and bust cycles.' No, it does not, any more than any other 'ism' does.

Historically up until the early 1990s, house prices had always been around 3x median income multiple, ie affordable and stable house prices, and still are in other jurisdictions.

There is no universal law that states there has to be a boom or bust. Yes, there are cyclic supply and demand cycles, but it's Govt. policy that dictates how closely the cycles match each other and therefore have any deviation from a low median multiple.

I am not against Capitalism, it is probably the least worse option. But once housing becomes an investment vehicle, it drives speculative behaviour. Name one commodity or share market that hasn't gone through boom and bust. People can make lots of money if they get their timing right, the late adopters get their fingers burned. Governments didn't start Tulip bulb mania or the .com bubble. Housing has been driven by greed enabled by cheap money. The music was always going to stop at some point. It was the timing that was hard to predict.

I get your point, but allow me to say that whilst it is a common point is not completely correct, and not shared by all capitalists at all

"Most, if not all, booms and busts originate with excess credit creation from the financial sector. These respondents, incorrectly, assume that this financial system structured on fractural reserve banking is an integral part of capitalism. It isn’t. It is fraud and a violation of property rights, and should be treated as such."

https://mises.org/library/confusing-capitalism-fractional-reserve-banki…

Interesting article. So the banks are to blame for running a ponzi but people choose to blame the government for introducing the CCCFA as it spoiled their fun.

glad you liked it :)

Banks are running on fractional reserve and the money is not anymore something that you have but something that somebody owe. The system runs on debit and the future is what we buy or sell.

I am not sure CCCFA had a decisive role, but if it actually slowed down this madness is not too bad.

Current government is just one government. Every central authority will do everything they can to grow in their influence, since the beginning of time. People actually want it, but they complain when they see the consequences.

Mises is a good one if you are interested in the Austrian School line about capitalism.

Anyways, yes, what we have today is more close to a dystopian socialism than capitalism.

The CCCFA just added in a dose of personal responsibility to bank directors rather than them being able to rely on outsourcing all risk ultimately to taxpayers. They really didn't seem to like that, though given their completely responsible lending prior to the law change it should have made little difference.

A dose of personal responsibility? So Bank Directors should (1) take the risk when lending on a home, (2) take the financial hit when a borrower fails and the house is sold at a loss and (3) take the blame when the borrower fails?

How about the borrower takes personal responsibility? The CCCFA was bought in to control 3rd tier and below lenders, but as with pretty much everything that Labour touches, they screwed it up and captured ALL lending.

Its a sorry state of affairs when there are people posting that someone else has to take the blame for other peoples stupidity.

Very little socialism involved. Crony capitalism is the game.

You are confusing cycles in general with boom and bust causes. They are not the same. Even affordable housing jurisdictions have supply and demand cycles, but that does mean their prices have boom and bust cycles also.

It only becomes a price boom and bust where Govt. policies allow cheap money that is put into the housing to profit from such investments. Greed has nothing to do with it. Where the right housing policies don't encourage that type of speculative behaviour then you don't get boom and bust.

If the right Govt. policies are put in place then the supply and demand cycles will almost lie on top of each other ie supply will equal demand, almost at any part of the cycle. But if the wrong policies are put in place, then they get the speed wobbles and become countercyclical, one moment too much demand and not enough supply and then vis versa, with only two small moments in time at the crossover points when the supply with equal demand (on the way to a bust), or the demand will equal supply(on the way to a boom).

Economic theory says this will happen, and you can see it happening in reality, in the present, and historically.

For example, you can compare California with Texas, two states within one country but each has different land-use policies. Texas median multiple is less than 1/2 what Californias is, and this historical low has resulted in very stable house prices, with no boom or bust in prices, especially in comparison with the likes of California, and when other variables between the two have been the same with cyclical supply and demand in immigration, interest rates etc.

The trouble with NZ et al is that we compare ourselves with similar loser housing countries worldwide and think that is the housing universe. If we wanted to have truly affordable housing we would copy what those countries/jurisdictions that have truly affordable housing do.

Good, let it burn

'Modest decline'.

I did a quick survey of homes for sale on Trademe in my home town - 10% of them were last sold under a year ago, 25% were last sold within 3 years.

That means either they bought to flip them, or they're FHB's realizing they paid too much and are trying to sell to get their money back.

Might just be me but 10% seems worryingly high.

850 Hawkes Bay residential properties on Trademe right now. I've been watching the market here since early 2016 and that's an unheard of number. Seems like specuvestors are in full panic mode.

On the flip side, a family member just moved back from Sydney with his wife and young children, and he'll be looking to buy soon. Might have timed things perfectly.

Lower Hutt was around 190 properties last year. Today just passed 600.

I've been using Oneroof to watch the market. I have categories for Keen, Curious, Sold, Withdrawn. There are an inordinate number of properties not moving in my Keen and Curious categories this past 6 months. Properties I requested price indications for, that were crazy out of my desired range, are now being re-listed and/or falling into lower ranges when I do price range searches on the other real estate sites. Yay! I might miss some by sitting tight but with several hundred in my list, the right one will drop into a range in the next 6-12 months that will make it worth while enquiring and bargaining for I'm betting.

Nice hopfuly snap up a few good buys in the next few months, then see how we look in 12 months or so, if not 2/3 years time it's all gravy.

"Nice hopfuly snap up a few good buys in the next few months, then see how we look in 12 months or so, if not 2/3 years time it's all gravy."

THERE IS NO SUCH THING AS A BARGIN IN A FALLING MARKET !

Said the person who came down in the last shower 3 days 23 hours ago.

Writing it in CAPITALS doesn't make it true. A silly post of course, I would gladly buy a Ponsonby house for $1 right now, I would actually buy the whole suburb!

Leveraging equity that will be disappearing down a black hole?

Where I live which is a provincial capital there are a lot more properties coming onto the market by the day. Executive homes, lifestyle properties and the usual crappy homes that have been rentals. Fear is starting to hit the market as people realise sentiment is changing. Homes NZ have put up new values today. One property I have watched for some time is a townhouse in a very good location in Wellington Central. Down $300k today on Homes NZ. That is huge. Maybe the vendor should have taken my daughters cash offer last week instead of being greedy and taking the higher offer from the people who need to sell their existing home before they can proceed. Interesting times ahead. All first home buyers out there still looking hold onto your tickets, be patient and think that rent is thousands but the drop in house prices to come will be tens of thousands at the very least. You probably will not get the bottom but when you buy it will be cheaper than it currently is.

Haha your not my accountant son, I'm in a postion that equity is neither here or there. Jog on now. Fyi if your cashed up, a falling market is indeed a good time to buy.

Sure, if you aren't highly leveraged on assets now dropping in value, then yep good for you, good opportunities will be out there.

It also of course means you're losing value in your debt free existing property assets.

So a slumping market is a double edged sword, right?

100%, however if lossing 10/15% is going to cause you financial hardship then they shouldn't be in property. If it drops 50% and interest rates go up to 8%, then yea that will hurt. However I'm not a doom merchant like alot on here so I'll remain positive we won't see that.

Be quick....to rush to the nearest pharmacy. Pepto pills for the win!

So what will the government do this time to save the property market, given aggressively cutting interest rates is not an option?

50k hand outs for FHBs in this year's budget?

Most probably remove LVR, that one is easy.

Less easy (given electoral base) revert interest deducibility.

In the short term it will sustain the housing prices... for some more months

I'd prefer none of them to happen, of course, but it is highly probable imho (at least for LVR)

Ohhh, look at that picture, not only are houses about to collapse into a heap, they look like they're getting haunted as well, lol

How are wages going to 'jump' enough to offset the negative sentiment that is just starting?

Public sector pay freezes, 'short'-term inflation expectations of 7%, inevitable interest rate increases, the lingering COVID hangover (i.e. full tourism probably not resuming until 2023), the war in Ukraine...all seems pretty wishful thinking to think the housing market will turn again at the end of the year.

Would have to be some pretty significant average wage increases (probably in the order of 25%!)

Perhaps they think the inflation impact is 'transitory....?'. Where have I heard that before?

For every 10c increase in the price of fuel, it's about the same as a 1% increase in the OCR for taking money out of the economy.

Less money for no gain.

Next we'll see the rise of the 150 year mortgage, so housing costs will stay the same, and the best your kids have to look forward to is YOUR mortgage.

I think it would be a good time for those with the money already sitting in the bank sitting there looking for a home.

Not so good for the borrower.

I have noticed that interest articles in recent times tend to only focus on bad news (or I suppose good news depending on how you see it). For example today there was a good article from a Agent on news hub talking about the return of expats and also the cccfa is to get new guidelines removing some of the artificial demand dampening.

Are these the same "professionals" that predicted a 20% drop in house prices in March 2020? They actually went up by at least 20%, so they where only out by a minor matter of 40%. I never realised that so many people can predict the future. Here's one more for the rubbish bin: 7% inflation - yeah right. Turn off the TV, turn off the radio, turn off the newspapers. You will feel better.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.