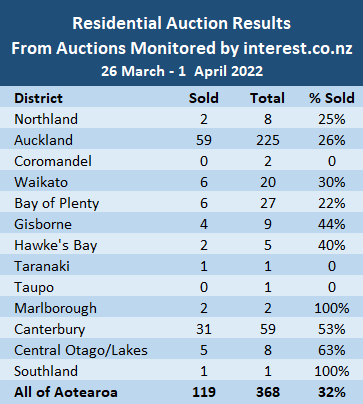

Auction room activity seems to have found its new normal at the end of March, with both the number of properties being offered at auction and the overall sales rates tending to flatten out.

Interest.co.nz monitored 368 residential property auctions last week (26 March to 1 April), up slightly from 360 the previous week.

The overall sales rate also increased slightly to 32% last week, up from 29% the previous week.

Auction activity remains strongest in Auckland but it's also where the decline in the percentage of properties being sold under the hammer first set in, with around a quarter of the Auckland properties being offered at auction typically selling on the day.

That malaise has now spread to the Bay of Plenty where the overall sales rate at the auctions monitored by interest.co.nz was just 22% last week and 18% the week before that. That's well down from sales on three quarters or more of the properties offered which was common just a few weeks ago.

Similarly, fewer properties are being sold under the hammer in Canterbury, which has enjoyed some of the most buoyant auction sales rates in the country over summer. But at the auctions monitored last week the overall sales rate only just scraped past the half-way mark.

Central Otago-Lakes remains the only place where auction activity could be described as buoyant, with an overall sales rate of almost two-thirds last week.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz and the results achieved, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

109 Comments

Auctions are dwindling.

The head of JPMorgan Chase, the largest US bank, warns that interest rates are likely to climb “significantly” higher than markets expect.

https://www.afr.com/companies/financial-services/jamie-dimon-s-blunt-wa…

7% interest rates this year is Guaranteed. -30 Crash in home prices by december.

RESILIENCE is the name of the game

Nothing is guaranteed, but I agree that 7% rates are likely. Especially on the longer terms.

We have global inflation, at higher rates than we have seen for 40 years.

It is wake up and smell the coffee time.

The Pendulum Swings is Guaranteed.

Please stop saying that.

No.

I find it quite a useful phrase. The repeated simplistic arguments give an indication of a lightweight contributor you can safely ignore - just like TTP.

This is the property market. Not a pendulum, in case you have failed to notice.

When Mortgage Rates are artificially moved in one direction for a long period of time then the market will correct itself, and even go further . Interest rates will swing back the other way.

Mortgage rates (I assume you mean interest rates) have not been artificially moved. Any movements in interest rates have been actual movements. There is no such thing as an artificial movement in interest rates.

This pendulum was pulled by emergency low rates now its gone it will hit new highs very quickly wiping out all who are over leveraged.huge amount of houses coming on market sale is just beginning.

Do your...ears...hang low, do they wobble to and fro,

Can you tie them in a knot, can you tie them in a bow?

Are you saying that borrowing up to the eyeballs to buy houses, european cars, boats, holidays, motorbikes, camper vans, car grooming, pet grooming, cleaners, gardeners, lawn mowers, security, $1000 plants on Trade Me, over priced art, restaurants 5 nights a week and then working 14 hour days to service the loan is going to have to stop!

The 14 hours per day part stays.

The 14 hours per day part stays.

Bingo! But instead of working 14 hour days to support an excessive extravagant lifestyle you are fighting just to keep a roof over your head and food on the table.

b-b-but the Hosk said this morning that sales & prices were up?! Geez it's confusing ...

Ahhhh Hosking. I think now he's pretty much the only reason I would vote Labour again 🤔

Yes, but the Hosk is a disciple of the Church of Ashley. Never let facts get in the way of faith. Amen.

Ahhh Hosk..I do enjoy his radio show. Add in declared property investor and friend of A Church. #vestedinterest.

He knows nothing about finance and economics, and is in the pocket of the RE sector.

As I said yesterday, average prices are slightly up as per CoreLogic, only because the composition of sales has oriented more to high value properties.

The REINZ HPI will show something quite different.

HM, the composition of sales is moving in the opposite direction to which you suggest.

"... with properties valued at less than $750,000 making up nearly a quarter (24.3 per cent) of all sales."

In February, properties under $750,000 accounted for 21.5 per cent of sales, while in January the figure was 18.1 per cent.

How about properties under 900K - 1 mill?

900K - 1 mill is a low value property now by Auckland standards.

Thoughts, The Way?

What if properties valued between 750K to 1 mill have gone from, for example, 30% of sales to 22%?

That would have a big impact on sales composition, right???

If we're talking assumptions then anyone can say anything. Best stick to facts.

Unless you care to share some data to back yourself up?

I am merely presenting you with a hypothetical proposition.

But unless we know the data - and we don’t- then we don’t know the answer. Yet.

I don’t have the data, but strongly suspect there has been a drop away in sales on values between 750k and 1 mill. Which would be distorting the values in the data we have seen in the last couple of days upwards.

But the REINZ HPI does have all that compositional data, so as I keep saying, let’s see what that tells us next week…

The latest REINZ data is only two weeks old. Do you discount that available data as well as the corelogic data?

Just because you discount data doesn't mean it doesn't exist. Relying on tomorrow's data to prove your point is futile.

It's three weeks old, and it shows prices in Auckland down 5.5% over the past three months...

Not "prices" but rate of price growth.

Its not rocket science, look at the data and see how it all adds up. Its all there for you to understand or not.

Oh God.... are you dumb or just being a troll?

I'll add you to P8 as someone I won't bother engaging with.

What has he said that is dumb?

HouseMouse is quite right - the REINZ HPI shows Auckland prices have fallen by 5.5% so far this year. Nothing to do with the 'rate of price growth' falling - the actual prices have fallen. Houses are worth less than they were in December, in Auckland and most of the North Island.

https://www.reinz.co.nz/Media/Default/Statistic%20Documents/2022/Reside…

It appears The Way is getting some of his numbers from the CoreLogic data series, which lags REINZ by a couple of months so has only just picked up on falling prices.

MFD, I appreciate what you are showing here. But average or median prices do not equal the actual sales price of a house.

"Barfoot & Thompson Managing Director Peter Thompson said predictions of price falls were a little premature, but was cautious on where prices might be headed."

"While the sales prices in March are the third highest on record"

"Overall, the rate at which prices are increasing is declining."

Well, they are obviously composed of the actual sales prices of houses. Hard to generate stats about house prices without feeding in sales data.

By yes, average and median prices are noisy signals and impacted by sales composition. Luckily, I linked to the House Price Index report which is a little more robust (although obviously still noisy in a tiny market like NZ).

I see we're onto B&T data now after your edit, increasing our statistical noise from the REINZ data as we only look at a portion of sales.

This data release showed a ~3.5% fall in average house prices since the December peak.

"Barfoot's average selling prices in March was $1,234,572, up $38,000 from $1,196,036 in February, but down just over $44,000 from the peak of $1,278,647 set in December 2021."

And a ~4.9% fall in median price since the November peak.

"The median March selling price was $1,180,000, up from $1,122,500 in February, but down $60,000 from the peak of $1,240,000 set in November last year."

'Overall, the rate at which prices are increasing is declining."

yes, according to B & T's data - which doesn't account for compositional changes in sales - house prices have not declined, but the rate at which prices are increasing is declining.

I'm not disputing that.

What I'm saying is that the most reliable indicator, REINZ's HPI, which accounts for compositional changes in sales, has shown prices have DECLINED by 5.5%. That's completely different to house price increases declining in their rate or speed of growth.

We'll have to wait till mid - late next week to see their latest data.

HouseMouse is quite right - the REINZ HPI shows Auckland prices have fallen by 5.5% so far this year. Nothing to do with the 'rate of price growth' falling - the actual prices have fallen.

Exactly - get it now 'The Way'?

Thanks HouseMouse and mfd. I too go on the same crusade when I see others falling victim to to plethora of (often low quality or lagged) data on the housing market. REINZ HPI all the way.

Housing will be hit hard in NZ, interest rates are going to climb will take a few months to work into market but once the ball starts descending and fear hits market people with average wages and million dollar mortgages will go under very quickly this is why stock levels are climbing smart people can see this coming and don’t want to lose deposit and be in negative equity for years.

If you listened to the clown chorus and borrowed upwards of million dollars for a lousy Auckland box there are certainly some interesting times ahead.

Be quick to declare bankruptcy. No point dragging it out.

There actually is no point in dragging it out. Get yourself cleaned up now and into a good position where you can borrow again when prices are low.

Very good point Mr Landers.

Just checking, you actually think if people have borrowed upto or above 1 mil that they should just sell now or somehow they will become bankrupt. Genuinely curious to know why you would say something like this.

When interest rates went to 20% in the late 80's to crush inflation. Your mortgage was probably only 50k on a 60-80k house. So 10k in interest. Your salary was probably around 20k. So the interest took half your pay. Pretty bad. Now the equivalent Gen Y is making 80k a year. FHB mortgage is 1 million. Interest payments at just 6% will account for their entire net salary.

Westie, that's a fair thought based on an extreme scenario. I don't personally think we will ever see that 20% again.. Hope not. But yea if there were no options below say 7% that would created some extremely tight budgets. Have a good one

People making 80k are not given $1million mortgages

Late 80's, I was there. 1st house purchased 1986, for $75k. Salary was about $25k but went up to $50k soon after (new job). Mortgage about $35k, from my POSB Home Ownership Account. Rate, I forget, probably a bit over 10%. Also needed a 2nd (vendor) mortgage of $10k @ 20%. Never gave any of it a 2nd thought, I was happy as. Got a couple of flatmates to help with cashflow, we all had a great time.

Woohoo finally...!

Housing market risk is increasing and not looking like easing any time soon...

NZ Bond yields are a hair away from inverting which spells trouble in the debt markets... http://www.worldgovernmentbonds.com/country/new-zealand/

You can clearly see a dramatic shift in the last 6 months in the bond market as it is overlaid on this chart

Debt markets are getting anxious which should worry everyone if you know anything about how debt impacts the world now and how sensitive affordability has become due to very high house prices

If interest rates go to 7% a $900K mortgage will cost you $72,000 after tax per year over 30 yrs which is $1300-$1400 per week

Even at 5% it will cost $58,000 p.a. over 30 years which is $1,114 - how is this going to play out on household budgets?

Average NZ income is still only around the $57K mark... although clearly only higher income households will be able to buy a $1mil house anyway but still its a big cashflow commitment

Auckland house sales defied market expectations by increasing sharply last month, new figures from the city’s largest real estate agency show.

Barfoot & Thompson’s figures showed the region’s average and median (and actual) house prices rose last month.

Thompson said many market analysts would be surprised by the prices achieved because, contrary to economic forecasts, they showed resilience rather than declining.

https://www.stuff.co.nz/life-style/homed/real-estate/128271482/surprise…

I’m curious about this one. When I look at what is selling around me, it’s the high end stuff only. The $3 million plus stuff where the buyer probably isn’t going to be too impacted by economic ups and downs. I wonder if this is impacting? It would be interesting to see a breakdown of the numbers

100% I think these results could be skewed, at the lower end with the new bank rules and serviceability tests the borrowing capacity of the masses is being severely limited which is why there are fewer buyers

"... with properties valued at less than $750,000 making up nearly a quarter (24.3 per cent) of all sales."

In February, properties under $750,000 accounted for 21.5 per cent of sales, while in January the figure was 18.1 per cent.

"While the agency’s figures appeared to go against recent forecasts, CoreLogic’s latest house price index showed Auckland prices were up 1.4 per cent to $1.52m for the month of March."

Lest we forget, those 3m buyers 2 years ago were 1.5m buyers. I think market timing (or time in the market) rather than actual wealth (ie cash) is the determinator here.

You would think if your savvy enough to afford a home over $3 mill, you would still want to save money anyway you can. Its like the Dragons Den investors, they negotiate hard to have as big a chunk of a business without giving more cash. Its over 11 bucks a beer now in Auckland just for a small bottle, need all the cash you can get. Best these higher buyers get with the program and wait for the inevitable hard landing and snap up a bargain.

The Way - Hi Tim. I notice you have deleted that youtube video where you talk about referring listings to Barfoot & Thompson's and Vice Versa.

Certainly interesting times.

Average time on market and inventory levels also up, and medians stil down over the past 3 months from peak.

26% clearance in AKL. Pathetic. Troubling times if your looking to sell

5 our of 8 in Queenstown lakes. It's hardly a reliable sample to then have in a headline.

I thought that too, but then had a look at the link and counted back the last 30 auctions. 18 sold with 12 passed in. So 60% sales rate. I checked further and found of those 12 passed in, 7 were confirmed as sold post auction. The Queenstown market is hot and will probably become sizzling when the Aussies start arriving.

Building firm placed into liquidation

https://www.odt.co.nz/star-news/star-business/building-firm-placed-liqu…

hhmm dunno, you may be right. I'm guessing you are talking retail rates? Lets say retail rates are 4% today, BNZ has that 1 yr fixed as of today. There are 6 remaining OCR rate meetings before the end of the year.

So if they did 50bps at every meeting between now and then you would have your 7% retail rate.

i.e. 4 + 0.5 x 6 = 7%

I just can't see them doing 6 double rate rises in a row. I reckon maybe 2 x 0.5 and 4 x 0.25 taking us 6%.

Even 6% will be catastrophic for many FHB from 2021. A million dollar mortgage will need 60k per year just to service the interest. That is an entire 80k salary completely used up to pay interest only. Parents who have acted as guarantors will be in trouble.

Do that number again on a P&I loan. Even more pain.

P&I stands for 'Painful Indebtedness', right?

Indeed. Interest only is unlikely to be renewed, making cashflow look even worse. The add less interest deduction, no depreciation, skyrocketing interest rates, and inability to exit without paying 39% tax...stress. Anyone caught out by this can look in the mirror, and punch themselves in the face. Welcome to the downside risk of gambling.

Popcorn.

Banks haven’t lent $1million mortgages to people on $80k. At least use a realistic figure in your examples.

He is referring to 1 Salary being used up. Therefore there is 2 salaries. But the real point of his post is to show how a 80K salary would be completely used up just to service the mortgage payments. And that was for an interest only loan. I hope that helps Albert2020.

Exactly. They have probably lent 1 million to couples earning 160k combined. RBNZ DTI figures for 3rd quarter 2021.

Total lending to FHB in Auckland with DTI > 7 was 297 million. Spread over 331 borrowers. Average of 897 k each.

If D is 897 and the multiple is 7 That makes the combined I 128 k.

At 5-6% interest. Those people are in a world of pain. Why do you think the banks used the new regulations to crack down so hard on new lending in Q1 2022. They could see they were creating a monster. They had to stop themselves.

Whats better that that. Q4 2022 354 million lent to 291 Auckland Owner Occupier borrowers with DTI > 9. Do the maths on that.

For those who follow my Hutt Valley updates -

Yesterdays link here

Looked at some further data last night on time on the market in this region

20% (134) of the 670 houses on the market have been on since last year ie over 3 months they have been listed for. 56 of the listings - so roughly 40% are new builds.

The data above doesn't include the 30 or so houses that have relisted with another agent.

If as a buyer you know its taking a long time for houses to sell and the longer it takes the cheaper the house will become - why would you rush in to bid at auctions when you can watch it pass in and then in a months time offer a low price.

Here's Yvil's favourite Tony Alexander. Of course he would never admit he was brutally wrong (He predicted in January 2022 that house prices would rise 5% this year). But at least, unlike most, he understands that the development sector is going to slump - something I have been talking about a lot for at least 12 months...and he's also a rare economist who is not so bullish on the OCR, like me. So I do have a little bit of time for him.

https://www.oneroof.co.nz/news/41201

Perhaps a premature judgement on Tony Alexander's forecast? Auckland prices are up 6.5% in the first quarter. National prices are up 3.2% for the first quarter... So he's not wrong yet.

Maybe, but probably not. He’s already said elsewhere that prices are down 5%, and I am sure REINZ’s HPI will show something like that.

He was referring to a 5% fall in the rate of price growth, not a fall in actual prices.

Bullshit.

He said he expected average price rises to be 5%.

you are full of it. Are you CWBW?

Change your understanding of "prices" to "price growth" and then reread and understand his statement in a new light.

And what's with the accusations? No need for that thank you kindly.

Whether you are CWBW or not, like him you are clearly a property spruiker / troll.

Or maybe you are P8, another commenter who consistently mispresents.

Here's the link below to Alexander's Janaury comment.

Quote:

'my best guess is that on average New Zealand house prices this year will rise by about 5%.'

https://www.oneroof.co.nz/news/tony-alexander-cant-get-a-mortgage-dont-…

Here is his full sentence, including the bit you left out:

So, much as I personally wouldn’t assign more than a 10% chance of this prediction being correct, my best guess is that on average New Zealand house prices this year will rise by about 5%

Unlike you, I find him modest, admitting that economists get their predictions often wrong. The reason I like him is because of his "at the coalface" surveys and graphs. I don't care so much for his or other people's price predictions, I prefer to look at the surveys and graphs and come to my own conclusion

And I'm curious as to who's upvoting you, as you are so obviously wrong.

Tim Mordaunt and his 4 fake accounts.

Pathetic responses. If you cant argue the facts you attack the commenter.

Sad Behaviour.

Because the commenter - ie. you - is obviously being a troll, and deserve it.

See ya, I am not engaging with trolls...

I'd suggest if you cant deal with data and facts then it is quite obvious that it is you who is acting like a troll.

I second that

Of course you would, you are 1 of the 4.

I really don't think they are the same person.

But they all have very similar minds and attitudes. Not very clever, and property spruikers. They seem very biased.

Probably very exposed, and worried.

Mouse I'm sitting really comfortable thanks. I just disagree with extreme views in either direction. Comments like house prices will fall 30% fact are just rubbish without saying in my opinion it may happen. I also think it's arrogant to say the market can never crash(whatever that actually is) and I also don't care for people who resort to picking on grammar. I for one think all the agro on here is 2 years of external stresses being vented in an environment where there is no actual consequences, punching away on a keyboard and actually thinking anything on here matters. That or this site attracts some real a holes haha. Either way, way to much time being spent thinking of ways to up the next comment. Good luck all the best and lastly it's not the warriors year.. 😉

Says the guy who doesn't know the difference between 'their' and 'there', and 'your' and 'you're'...

.

Yep, you guys are really annoying, so yeah your (not you're) trolling has worked!

but... at least I am right. You guys are totally clueless!

It's better not to worry too much about the house price correction underway, Luke, there's nothing you can do to change it, but your destiny is partly in your own hands - you could sell up your investment properties now before it gets too late and the market really sinks.

Maybe if you listened to me mid-late last year you could have sold up when the going was good, and before the house price collapse started.

But, everyone is responsible for their own decisions.

Mouse I have my home and two rentals, all in Auckland with a total mortgage under a mil, I have done well over the last 20 years. Personally a collapse wouldn't bother me, empty rentals wouldn't bother me although it would be annoying. In my opinion you are extremely arrogant making comments that I'm clueless. You don't know me or anyone on here. Take a breath and stop attacking everyone that doesn't follow the script you adhere too

You are either really dumb or a troll. Or both.

I've answered your responses enough, if you still can't understand the difference between price decreases and decreases in the rate of house price increases, then sorry I can't help you...

Have a nice evening CWBW

HM, what's with the anger towards people who have a different view to yours?

Having witnessed real estate sales over many decades I can say unequivocally that for the majority of the time houses have always been sold with an advertised price, or with a price with the words "or offer'' or "negotiable" tagged on. Only mortgagee sales, or the rare ultra-specially-desired properties were auctioned. There was a stage when houses were advertised within a given price-range but that was very short-lived.

The feeding-frenzy we have been through is unparalleled and is due to two factors; unprecedented immigration of immigrants with access to money and ultra-low interest-rates brought on by Covid.

Real Estate sales persons will from now on have to use real selling skills rather than being purely a listing agent. This sea-change will shake many sales persons out of the industry.

Sales persons will actually have to work harder on such things as qualifying prospective clients which means "sitting them down" and talking to them at length in their own homes, perhaps until late at night.

Many current sales persons won't have the inter-personal skills and character to be comfortable with this.

They may have to actually drive prospective purchasers around to show them several properties they have on their books instead of just turning up in their flash car at the front gate of a listed property and expect the prospect to turn up and follow them round in their own car. Yes, this what sales persons had to do in the past.

They may have to bring out of town prospects home for tea! The wife or husband will be mad at this intrusion but will have to suck it up.

All depending on the disappearance of Covid or the learning to live with it.

Yes, two years of madness and everybody seems to have forgotten what normal conditions look like.

Been closer to 20 years of madness - last two years just the icing on the cake (or possibly a blow-off top).

Yes, absolutely!

Indeed. They have enjoyed a very golden period, and now it clearly is not that. May they enjoy the time as the meat in the sandwich between sellers fantasy expectations, and whats kiwis surviving hyperinflation can afford. A very big gap.

This is exactly what Tim Mordaunt TTP , the way - are so scared of. Losing the staff.

Unspeakable horrors may occur, like having to drive a Japanese car.

And cut back on the lattes/smashed avo on toast.

Another interesting stat that I'm tracking is total rentals on trademe. 4th November it was 8608 and now it is 10014 which is a 16% rise. It's actually gone up by 270 in the last two days.

There have 3092 more departures than arrivals in the first 5 days of April. Which is a loss rate of 18,500 per month. Now much of this will be holidays now so it's not very reliable data. But combined with our very high dwelling build completions it could explain why available rental volumes are increasing.

Increasing rentals could lead to rents falling, reducing the value of rentals. Rental vacancies will be the first signs that the housing shortage is no longer there, then the whole picture of the housing market changes, I think. We'll see.

Ive been told that we have a shortage of houses, and all the english folk are coming home with their squillions. Be quick.

Fully aware that the "plural of anecdote is not data", but of three fairly close friends, who returned from the UK within the last two years, 1 has already packed up and gone back, the other two are making plans now. The social life has pretty much returned to normal. Granted only one has a family, but still, that's indicative.

Unless you own a London home, selling a UK house doesn't get you far in NZ. I'm selling a semi detached 2 bed house over there right now for about 350k NZD, in a city the size of Wellington. Well located with a big garden.

Sounds like they had fewer investor foxes guarding the policy henhouse.

Sounds like a good time to buy and build equity without being investor rorted.

Aware of several Uni graduates with four years work experience and their partners heading for the UK as well. One couple gone already and the other about to leave. Math of living in NZ does not work, it just props up Mi Lord Speculator.

Collectively 72 years of tax supported education and healthcare now lost as future tax payers, well done Mi Lord.

Makes good sense...why stick around just to fund landlord subsidies and universal welfare benefits?

Might be a tough year or two for the people farmers.

Jesse - i keep Data on this for the Hutt valley only (I have 12 months data) - current rental stock is 171 rentals - this is up from 121 this time last year - 40% increase

Rentals have consistently been this high now for over a month. It seems to be driven by a large number of new builds finishing and available for rent. A handful of these new builds have been offering a weeks free rent to get them rented.

Approximately 31% of all rentals have lowered their price since listing with an average $46 reduction in rental price.

Nice research! I started tracking NZ rentals in August. Will be interesting to see how the official long term migration numbers look around the middle of the year. I'm expecting April and May to be large outflows with the Northern hemisphere summer on the way.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.