House prices may have already fallen further than some figures suggest, according to the Real Estate Institute of New Zealand's latest House Price Index.

Many measures of housing prices are based on figures such as medians or averages.

While these can provide a useful indicator of price movements in the market, they can also be influenced by changes in the mix of properties being sold from month to month.

For example if the top end of the market is more buoyant than the middle and/or bottom of the market, that can push up median or average prices even if the prices of individual properties aren't moving much.

That appears to be what is happening in the housing market at the moment.

The REINZ's national median house price was up by 0.6% in March compared to February, which followed a 0.6% rise in February from January.

On their own, those numbers suggest prices have continued to rise at a relatively modest pace since the beginning of this year.

However the REINZ's House Price Index tells a different story.

The HPI adjusts for differences in the composition of sales each month, to give a better idea of overall price movements.

The national HPI showed a 2.1% decline in March compared to February, with all but two regions (Otago and Southland) showing declines.

The HPI figures also suggest that prices has already been in decline for the last few months, with the national HPI in March down 2.8% compared to three months earlier.

But perhaps the most telling figures are those showing how much the HPI has declined from its market peak in each region.

The timing of market peaks varies form region to region but for most it was around November last year.

Nationally, the HPI is down 4.3% from its peak, with the biggest falls occurring in the Auckland and Wellington regions with the HPI down 7.8% from its peak in both regions.

Otago is the only region where the HPI is still increasing, finishing on a record high in March.

And over the three months to the end of March the HPI had declined in eight regions, increased in three and was unchanged in one.

That suggests the decline in prices is now widespread and is gathering pace.

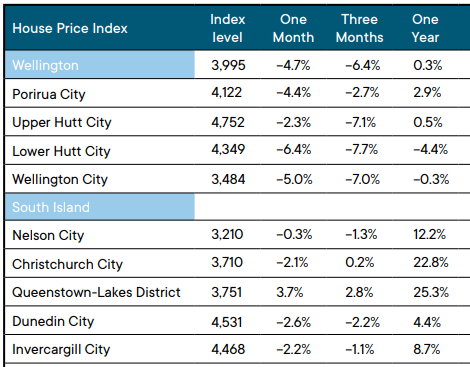

The table below shows the movement in the HPI in the main cities and urban districts over the last year.

The only places where the HPI didn't decline last month were Papakura in Auckland, Rotorua, and Queenstown-Lakes.

However picking how far and how quickly prices might decline from now on is of course fraught with difficulty.

As ANZ senior economist Miles Workman noted in his report on the latest REINZ figures, identifying the factors affecting prices, such as rising interest rates, tighter credit and the removal of interest deductibility for investors, is pretty straight forward, but gauging the likely timing and magnitude of house prices falls isn't so easy.

"The animal spirits component of the housing market can be wild," Workman said.

"FOMO (fear of missing out) appears to have given way to INPT (I'm not paying that), aka FOOP (fear of over-paying), aka FOBAP (fear of buying at peak).

"No matter the acronym, it's all the same: animal spirits have changed direction, and that has the potential to surprise even the best house price models," he said.

REINZ House Price Index March 2022

149 Comments

The valuations didn't make sense with 2% mortgages and they certainly don't make sense at 7%. Still a long way to fall from here before net rental yields are in line with the long term averages.

At 2% mortgage rates.... I can kinda understand why prices are high https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-household-debt

In The inflationary 1970s, basically Housing prices went sideways but in real terms declined by 40%..ish.

It was incomes that rose in that decade, making housing more affordable again.

Maybe this time round... if inflation continues and wages rise strongly .... history will repeat ?

Depends how RBNZ and Govt handle things over the next few yrs.. ( My guess is that in the face of a recession the Govt will spend and the RBNZ will print.... ), which might give us one more, maybe short, upturn... before we have some kind of crash...??

just guessing here...

In the 1970's New Zealand was a virtually closed economy with monopoly companies staffed by unionised workers. We are fully exposed to global competition now. White collar and blue collar. Just because you need a 30K pay rise to pay your new mortgage interest rate and maintain your lifestyle. It dose not mean your employer can afford to pay you that.

Westie - given the shortage of workers, employers who cannot afford to pay workers substantially more need to shut their business. I agree with Tony Alexander on this point. NZ has become a very low wage economy with many businesses relying on cheap labour, whilst failing to invest capital or in their employees to improve productivity.

Yes a decade of real wage stagnation offset by falling interest rates and some tax cuts to free up existing incomes for discretionary spending. While boosting the prices of assets to make people feel richer. What do you think happens when interest rates start rising?

Spending will contract. SMEs that are exposed to competition will fail. Many of those businesses have loans secured against property..

Wrong as far as wages go.

According to The RB last 10 years, 2012 to 2022, wages are up 36% but prices up only 19%.

Facts.

Housing however is up 148% in the same period (according to RBNZ)

Yeah and what policies were implemented between the 80's and 2000's?

Was our quality of living really improved by cheap consumer goods and materialism on steroids?

The rise of corporate rule and the end of the working class that built NZ. "Free market" policies weren't implemented for the people.

The real question is who's serving whom?

Yes. 'cheap labour' for employers includes employees who receive 'working for families' tax credits. The only true taxpayers are high income earners and everyone without kids. A great rort for employers.

Just because you need a 30K pay rise to pay your new mortgage interest

Give out false and misleading figures and suffer loss of credibility

If you are already earning over 70k a year. A 30k pay rise is 20k in the hand. a 2% Interest rate rise on a 1 Mil mortgage will suck up 20k per year. There will be plenty of people in this situation. Some of them wont get a 30k pay rise.

2 percent interest rate rise huh, is there anyone you know in that boat. Along with a 1 million mortgage on a single 70k gross income. Quite simply.... No

A 2 percent int increase from 4 to 6 percent takes repayments up 1200 ish per month. 12 x 1200 is 14400 not 20,000

Those with false and misleading figures are like cheats. They do not prosper, your analysis is rather lacking

2% of 1 million is 20k. Try it on a calculator if you don't believe me. In July 2021 when one year special rates were bottoming out at 2%. 99 Auckland borrowers without any other property as collateral were lent a total of 96 million dollars. Giving an average mortgage of 969 k . With average combined income to service of 107k. Some of those mortgages would have been over 1 million and some of them would have fixed for one year only. When the re fix in July 2022 they will be paying over 4% to fix for 1 year or more. That's one small group of borrowers in one month.

Likewise try it on a mortgage calculator. You clearly do not know how mortgage repayments work so you might, though doubtful, learn something

I hope you are not a property investor. If you only believe mortgage calculators. Go to ASB mortgage calculator. Put in loan amount of $1000000 and set the interest rate at 2%. Interest only terms. Forget about principal payments. Just like these borrowers will have to. You will see fortnightly payments of $770. Multiply that by 26 (fortnights in a year) You get $20,000. Now repeat @ 4% and you will see the payment amount has doubled. That's how math works.

This is start of a spiral downward in house prices it will hit bottom once average wage earners can afford to buy a average house, so in Auckland a long way too go. Interest rates are still at emergency levels and inflation is sky high could be type of crash that goes into history books returning house market back 10 years.

I see it more as a 'correction' than a drop. After an out of control frenzied 30% rise, 10% correction is a good thing.

10 % ? .... pah ! .... baby , you ain't seen nuttin' yet ...

Yeah...cuckoo land thinking for sure. That exit door gonna be jammed pack within a couple o weeks - and there be nuttin nanny gummit can do. Weaning time for the titty suckers.

PM's, oil, uranium is where the action is....

PM's, oil, uranium is where the action is....

Fertilizer

Fertilizer problem solved ... as house prices are starting to fall there's plenty of investors & last in FHB's starting to poo themselves ...

CRP.

My intuition is telling me that we are heading into very volatile times, nobody is going to be immune from what’s to come, and really what has to come. Our housing market decoupled from reality years ago. The havoc it is causing in NZ society now is something I never really believed we would inflict on each other.

Never the less here we are, I hope it’s short and painful rather than long and drawn out. Framed against all of the Global uncertainty I don’t believe we can avoid a major crash now, everything feels too out of whack. Time will tell I guess.

Were banks actually stress people at 7%. I heard the stress tests were between 5-6% ish. House prices are largely based on the weekly service payments on a mortgage, so if those increase, then I can't see how people can afford to pay these high house prices. Already asking prices on my trademe watchlist have dropped 10% in some cases.

Of course they are. Less buyers. It’s hard for many to get finance. And everything else is getting more expensive so people are getting more cautious about what they are trying to borrow even if they can. Fear is worse than greed. Watch some price drops occur as panic settles in.

Spoken like a true agent… fear worse than greed… I’d say rational fear vs blind greed.

Huh? Nothing in that statement was overly agent cliche? Why the snarke?

The vaunted resilience of the housing market seems overstated.

If recent trends continue we could be in for a hard landing.

- LCC

Shouldn't you be called uppercase capitalist?

CamelCaseCapitalist would be even better

camelCaseCapitalist or PascalCaseCapitalist...

Just wait for the SCREAMING_SNAKE_CASE_CAPITALIST over the coming months…

Any landing you can walk away from is a good landing.

I suppose if you wanted to be really optimistic, the HPI probably expects a strong market in March, and adjusts quite heavily downwards if there isn't one. So perhaps a 7.8% fall in the HPI shouldn't really be interpreted as a 7.8% fall in prices, but rather that the market is 7.8% off where we would expect it to be.

I don't think the HPI is a seasonally adjusted index.

You're correct HH, it isn't.

Oh? I learned something today, then. Thanks for the clarification.

A price index is a statistic based on actual events, sales, rather than future trends or assumed trends of a period.

An article yesterday suggested the HPI is adjusted based on something to give a clear indication of price during different buying patterns. I assume they use some Valuation.

In short, assuming the median and average were $1mil from feb on properties averagely valued at or around $1mil. If all sales were exactly $1mil over march, the median and average would not change. It would be $1mil. However, if the properties sold were valued at $1.1mil, the HPI would drop as more expensive goods are being sold at a lower price.

This is what some commentators on this site are assuming is happening, people are still buying in middle/higher price brackets, but at a lower value than previously

Yes, that basis of the council valuations - GV / RV / CV whatever you wish to call them. They form a decent basis from which to show change. So if properties were selling at 1.5 times their "CV" last month and 1.4 times this month, then house prices have fallen.

There's a bit more to it than this that accounts generally for composition , but that's the gist.

New acronym for 2022 is E.F.R. (Effer)

Enjoying free rent.

Why would any potential first home buyer buy now, when house prices are falling by more than rent? Potential first home buyers are "getting ahead" by tens of thousands of dollars each month just by sitting on their hands.

With any luck they will realize this, and there will be a massive buyers strike at the FHB end of the market.

Landlords across the country are going backwards while the Effers living in their rentals are "getting ahead" by leaps and bounds. About blimmin time. Long may it last.

Yeah. The tired old tropes of "mortgage payments are cheaper than rent", "renting is just dead money", and "why would you want to pay off somebody else's mortgage?" don't really work in an environment where house prices are falling and interest rates rising.

Think of rent as paying someone else to take the property price risk for you.

Another factor to watch is the effect increasing deposit rates will have on investors actions . Without capital gains the net yields on many rentals are very low as deposit rates increase many will start to look at these as compared to managing a rental with its attendant risks and problems. While fixed deposits aren't risk free due to no depositor guarantee here they carry less risk than tenants and maintenance .

A deposit guarantee (assuming that you trust the promises of this Government) is supposed to be introduced by end of next year

Good points. Also with the legislation restricting rent increases to once a year it provides some certainty to renters, and shifts the power balance somewhat. This fixed rent amount in real terms is also reduced by the (currently high) inflation rate.

The Minsky Moment is approaching.

https://www.investopedia.com/terms/m/minskymoment.asp

To be better insulated from the second-order effects of the housing bubble burst renters would be well advised to move abroad for a while. It's not going to be pretty here.

... how does our CGT ... sorry , I mean , how does our Bright Lime test work when house prices fall ? ... can sellers lock in losses to offset against gains elsewhere ...

GBH - sellers can only claim capital losses if they are a property speculator, which also means they must pay capital gains tax on any capital gains. You can’t claim capital losses if you are an investor, nor are you liable for capital gains tax, subject to the bright line test.

I expect there lots of ‘investors’ will now claim to be speculators. I imagine IRD will look askance at such claims unless there is already a pattern of paying capital gains tax. The term ‘hoist with one’s own petard’ comes to mind. Or perhaps I’m meanly engaging in schadenfreude.

I am informed , thank you ... oh dear , those poor " investors " ... how sad , never mind ...

Does this mean if you buy a house to live in, and need to sell due to job relocation and also sell this property the within the ten years of the purchase, you'll be subject to capital gains tax (brightline)? If so then the govt have snookered everyone in this position as just on the slim chance you have sold at below what you purchase, you cannot claim a capital loss?

Nigel

The brightline test does not apply to the primary residence (holiday home,yes) or a house you inherited.

I wonder what will remain of the New Zealand economy when the best and brightest of the working age generation have moved abroad ✈️✅ and those that remain are trapped in negative equity or a lifetime of debt servitude for a lousy townhouse in some god awful suburb.

Resilient stagnation is the best case scenario after the mind numbing stupidity of blowing one of the world's greatest housing bubbles.🫧💥⤵️

that should say "CREATING one of the.....house bubbles" surely

... I tried to move abroad , but she slapped me & said " sober up , you horrible little man ! " ...

One could go to Australia except more debt collection agencies have their primary operations/ head offices based out of Australia so delinquent debtors and runaways could easily be tracked and located with the various skip tracing tools available. The only viable options for people to flee is to go to UK/ US/ Canada or for temporary residents to return to their home emerging market countries (where latter is more troublesome given inflation is breaking out - I'm imagining more "Sri Lanka" situations breaking out in South East Asia in the coming year/s).

“I wonder what will remain of the New Zealand economy when the best and brightest of the working age generation have moved abroad..”

They will be replaced by the best and brightest from other countries.

If only. The best and brightest of other larger countries are better and brighter than the excellent Kiwis leaving but they will continue to go to California, Oxford/Cambridge, Canada, etc. We will get the second raters but they may be good enough.

“We will get the second raters but they may be good enough. ”

Exactly, good enough is enough for small country like NZ.

... true dat : to squeeze cows , deliver uber eats or pick kiwifruit you dont need to be a rocket surgeon ...

That reminds me of a good friend I have. Originally from Kenya he finished his training as an environmental engineer here in NZ, working in catering as a dish washer for a change of pace during his studies. Now doing very well for himself and his family in Oz as there wasn’t the work for him here.

We could all send a thank you letter to Mr Orr.

You've got a thumbs down from the spruikers...

This type of article will become the normal house price’s down for next few years.

These articles are written to attract readers, and no one has any idea about the future. Imagine Russian firing a nuke at Europe. Living in NZ might seem pretty good then. Applying logic, it would seem dangerous to raise interest rates too high on the back of a pandemic and Russia at war with the west through a Ukraine proxy war.

Doggog

First sensible comment I've read today.

Look around you!

In Auckland, at least, I'm now coming across Indian immigrants, some educated here, some not, in every sphere of commerce, government and health, etc on a daily basis I would make a prediction that if immigration was opened up today there would be thousands if not tens of thousands of Indians willing to work in New Zealand without complaining.

Of all the more than 200 countries in the world, only New Zealand, Canada, and Australia.....only these 3 countries .....are attractive to immigrants irrespective of high house prices. And they're willing to pay high rents; they just pack more occupants in to afford the rent. The townhouse next to me in my leafy suburb has had 3 separate lots of Indian tenants over the past 6 years, all valuing education for their kids and having high skills themselves, with every intention of settling in New Zealand.

And what's more, so many are blaming Ardern's Labour Party for everything, we could well have a right-wing government after the 2023 election i.e. National or National/Act. And they are always on the side of business, so expect them to reopen immigration to supply businesses' labour shortages, Indians will be straining at the leash to come to New Zealand. Thus, more pressure on housing and house prices. So, in a year or so expect house prices to soar up again.

Those leaving NZ for Australia will put more pressure on Government to relax immigration controls. Don't forget that a lot of those leaving for Australia are not needed in New Zealand.....they simply don't have the right skill set. Australia may be better able to supply jobs for the low skilled than New Zealand.

A TOP/Green/Lab/Maori govt is more likely, for sure not lab alone.

Nat alone is out of discussion, and ACT will push for even more intensification (and ACT immigration policy doesn't work in the way you dream)

Other than that I find your comment smelling a bit racist, other than being a bunch of nonsense.

India has a rising population , and a huge demographic of young people .... good English skills , democratic , business orientated , fantastic cuisine ... and ... they love cricket ! .... Joy ...

"yes Sameer "

New Zealand will be Fiji v2.0. What a splendid vision.

... there is strength in diversity ... Fiji doesn't have that ... we do , Australia , Canada , Britain , USA ... all multicultural ...

Points gun "always was"

“National or National/Act. And they are always on the side of business, so expect them to reopen immigration to supply businesses' labour shortages, Indians will be straining at the leash to come to New Zealand. Thus, more pressure on housing and house prices. So, in a year or so expect house prices to soar up again.”

The next 5 years or so provides best opportunity to buy with less/little competition before the market picks back up again. One of the houses we purchased back in 2012, best house buying experience ever, quiet open home, agents negotiate on our term…etc.

Yeah imagine that. or China doing over Taiwan and at the same time strangling AU and NZ while the US is bogged down elsewhere.

We aint as 'safe' as you might think...forgotten that the US saved the Pacific in the last dust up have we??

“Imagine Russian firing a nuke at Europe. Living in NZ might seem pretty good then.”

One of the reasons why NZ is one of the top countries people are lining up to move here, things we take for granted here, people are willing to pay to secure themselves a spot here.

Yeah they would just fire off one and that would be it. NO. The developed world would be dust by the next morning. Pray it never happens

I disagree, people want to move where there are opportunities to get ahead, if you travel you will see that there are many countries with opportunities outside of NZ.

Also it will depend heavily on easy availability of jobs, and although its a tight labour market now it can turn very quickly given that credit expansion is slowing rapid and the huge exposure to construction.

That’s exactly the common misconception.

Many bring their money here ain’t seeking for “opportunities to make big money” or to “ get ahead”. This country doesn’t provide that. People bring money from elsewhere and settle and enjoy the lifestyle here. (And buy houses) Some are already rich and are happy to take on a normal pay job to kill time and some have income stream from overseas…

If Russia were to fire a nuke at a Nato member, living in NZ would do you no good.

As I said in a comment yesterday, it seems like a reasonable bet that the Auckland HPI will be at least 15% down from peak before the year is out, and 20% is not out of the question.

We are yet to see what this week's OCR increase does to prices, but I imagine it will give them a decent nudge in the downwards direction. With further OCR increases all but certain, the absence of the (crazy) high net migration gains seen pre-covid, and a decent number of new builds coming online, it's safe to predict the market will continue to weaken. The only question is by how much.

Perhaps even -30% by December could be a certainty?

Houses near where I live used to sell for 2 million. In a very short space of time they went to 3 million or more. I suggest they are worth 2 million again.

How did you get to the 30% figure Brock?

Here's how I look at it: the Auckland HPI has lost on average about 2% a month for 4 months. Even if if that continues for the remaining 9 months of the year, the market would be about 26% down from peak. That would be reflected in the December HPI released in January 2023. So 30% seems unlikely to me.

I guess you could argue that panic will set into the market, thereby accelerating the decline. On the other hand people can be pretty stubborn and will try to avoid selling if it means taking a big loss. Plus the government is likely to take some action if things are getting too messy.

That 2022 guy told me and he seems to have a solid grasp on how 2022 is going to play out.

Lol, everybody knows what he's got a solid grasp of. Don't shake his hand!

Auckland HPI is down 2.4% in March, so if it keeps falling at that pace, it would be around -19% by December.

But it seems pretty clear that the speed of decline is picking up. There is a clear turning point in the data, from rising to slow fall, to faster falls.

So I'm picking greater than 20% falls in Auckland by December.

Remember these numbers are during peak selling season! I think incremental drops should get bigger during winter. I agree with Brocks guess.

The recent HPI changes for Auckland are:

Nov 2021: +2.96%. (Auckland's highest ever HPI was this month)

Dec 2021: -2.25%

Jan 2022: -2.68%

Feb 2022: -0.64%

Mar 2022: -2.40%

So it looks to me like December was the turning point, and January was the biggest fall so far. One thing is for sure: April's figures will be very interesting.

Depends on how the sentiment changes. Falls are already happening, but as it becomes more apparent you'll probably find more people coming of the realisation that prices are falling which could magnify the falls due to a stampede for the exits.

Particularly for those who are not far off retirement and hold a property or 2 which they plan to sell to supplement their retirement.

With the huge plans for intensification being announced in Auckland next week, I wouldn’t be surprised if that increases the rush for the exit. perhaps the final straw for some.

House prices may be falling further and faster than most figures suggest

Will see, once official data is below 20%....as growth has been much higher and faster, anywhere from 40% - 120%.

Falling further and faster is a relative term but universal truth is that it has a long way to go before some sanity comes into housing market - High time that is treated as a necessity and NOT a speculative chip as promoted and preferred by politicians of all breed and central bankers.

If Politicians and central bankers have forgotten what are the basic necessity of life - food, clothing and shelter. If any one of these basic needs is not met, then humans cannot survive.

Now they are fighting over air and water also, which has been taken for granted.

I can see the change in real terms ( we sold up in CHCH in December) as we are looking to settle In Dunedin so are actively looking to buy there.

I’ve travelled down to Dunedin twice and I’m pretty amazed at the fast price correction. Good houses that were priced at 800k now listed with a price at $680 and still unsold.

Sure some things are selling including a townhouse that I registered to bid on at auction, I was one of two bidders and I did not bid, bizarrely the other bidders bid over the vendor bid and the vendors got a very good price.

Poor financial literacy on behalf of the bidders!

So now of course like many people I am just watching and waiting, we are cash buyers so I am now looking/hoping to secure a family home with cash and at least 100k to spare.

How low is goes? Who knows? But I’d be very careful buying now

Christchurch is the " capital " of the South Island , and until recently had average house prices 50 to 100 % above Dunedin's .... when Dunedin got more expensive than CHCH , about 3 years ago , that was the mother of all RED light warnings ... this property bubble has surpassed insane FOMO frenzy ... we're in uncharted territory ... riding the housing rocket to infinity & beyond ...

Define good, poor overall housing stock in Dunedin, certainly in that price range.

House prices may be falling further and faster than figures suggest.

That's going to get the comment's section going! LOL

Be quick 🤡

While its just an index, I keep an occasional eye on house prices versus my 60/40 investment. So compared to the HPI...in Welly it is down 4.7% in March and 6.4% Q1, in AKL down 2.4% and 4.5%. My 60/40 was up 1.4% in March and down 3.6% for Q1. NZ really needs to get out of the residential housing as an investment mindset and treat it as the utility that it is. Note that past performance is no indicator of future performance!

Let's remember the 30% boom plus boom during covid was by a public in panic, and fueled by an unnecessary drop in OCR to levels never seen before. This Govt overreaction made money in the bank all but worthless. So where did that money and printed lolly water end up...?

Completely artificial.

A 30-40% drop just gets us back to pre covid level's. Prices were already stupid on the back of an investor culture of tax avoidance backed by long term Govt policy. With inflation now burning down the tax paying engine of NZ, the middle class, we need at least a 30-40% retreat in speculative housing stupidity. It is also essential the tax support for property continues to apply only to new construction post Election 2023. This will drive additional supply and prevent an exit of tradies to Aussie like the GFC.

Based on the comments of the speculative in the last two days on this website, debt speculators are swapping gloating for stress and fear. This is documented on the bubble cycle. It occurs right before "capitulation" and "dispair".

Enjoy the free fall, hope you packed your own parachute.

Icarus is catching fire...finally.

Of course if prices went up 30% then they only need to come down 23% to be back where they started.

Yip. I think it's more likely we'll have price declines of 15-20% from peak over 18 months, followed by 2-3 years of generally flat prices. If building materials investigation actually results in meaningful change, that could trigger a further 5% decline and softness for an extra 12-24 months.

All of that means a decline in prices in real terms especially due to inflation, but they may not get much cheaper nominally than they were in 2018.

Stick your property or any of your neighbours' property into the homes.co.nz price predictor and you'll mostly get quite a downwards shock....

On this indicator the market topped out several months ago and is already showing +5% falls. I know a lot of people who raved about how great this algorithm based system was on the way up (and how much richer they were).......let's see how they like the down slope.

Agent paid manipulation of displayed prices upward prior to listing, renders Homes.co.nz at best as artificial, at worst borderline fraudulent. Ignore it.

I could not agree more. This site needs to be more independent of agents than it actually is.

I agree…. except I would remove the word ‘borderline’…. its plain market manipulation

Not enough people know agents can set the price of properties on homes.co… for a monthly subscription.

Imagine if your share broker could inflate the price of your portfolio before they then sold it… it’s effectively what was happening.

Expect a rapid reversal of the price rise from the last two years followed by a grinding attrition over the ensuing 30 odd years. This is the top of the cycle of falling inflation and interest rates and the massive appreciation in asset prices. Geopolitics, inflation and demographics. Sell now.

The party is over. Agents are getting brutally honest. Very slow is a common description of the current market. Buyers are being very cautious is another. Lots more listings and vendors are generally unrealistic. Add that to it is hard to get finance and you have a perfect storm. Buckle up and hold on. And it’s winter. Properties do not look so nice. I hope the agents have put some hay away to get them through the next few years which are looking pretty tough.

Yes some listing in vain hope of getting a price re last Nov/Dec highs. Far far too late.

I’m kicking myself for not listing Oct/Nov last year. But in saying that there is nothing decent on the market that I’d buy instead. Seems to be people off loading rentals and junk. Proper family homes in good suburbs on 500sqm plus seem to be selling well.

Why didn’t you sell and rent. We see it as a waste of money and a hassle as two shifts but on this occasion it could save hundreds of thousands that flow to your pocket.

Looks ugly indeed.

Yvil’s favourite, Tony Alexander, said +5% for 2022, in January. Looks like he will be very wrong indeed. Ashley Church, too.

Some reputations will be in tatters later this year.

.... but but but , Ashley Church said houses double in price every 10 years , always have , always will ...

Ah the self proclaimed "real estate historian" - maybe he could join Ser Chong & Heir Max's RE development project - it could be called ...

Key Bwick

When you've had a cushy ride all your life it's incredibly difficult to imagine anything else...

It has been a long time coming but it has arrived. Like D day” it is the beginning of the end.” First home buyers should keep renting. They will save much more than their rental costs. The more you save on buying the less your repayments to the Bank will be.

Saving twenty grand a month at 2% price falls each month..... renting or going on an oe for the next two years will be on many peoples mind.

In usual times Orr/RBNZ would jump in and drop the OCR to support prices like he did in 2019 when Auckland prices were languishing. Not an option now with sky high inflation so my guess is prepare for an LVR drop in desperation.

... the question is , is the current inflation burst a short term occurrence , or entrenched ...

That is a question only Father Time can answer

Wonder why the expression is " father time " ... rather than " mother time " .... 'cos , if time flies , we could look up her skirt ...

..the price of popcorn is my priority at the mo.

its a slow moving train wreck - slow cooked brisket or ribs....

Removing lvrs won't do diddle squat imo.

Prices are falling as no one can afford the interest costs. Allowing people to take higher levels of debt won't change household cashflow.

And if you are planning right now to gear up to that level with all the negative indicators your just plain stupid.

They will most probably remove LVR, I see that too.

And you are right, it will not be effective.

More effective will be when/if they reinstate interest deductibility.... but hey political suicide?

But let's say they are THAT crazy, even that won't save the ponzi.

So in the 2nd week of November last year I sold a 800sq m property on Riddell rd Glendowie that had land value only, old 3bdrm house max rent about $850pw for $3.25 mil,, Akl was still in level 3 lockdown. there was nothing for sale and the market was right at the peak of stupidity as developers fought over limited supply.

Chinese developer got it, rank group where under bidder.thats $4062 a sq m. Thank the lord quick, a settlement and we had the dosh early Dec. if it had a long march settlement at 10%dep they would have walked.

It has to either have about 4-6 units on it possibly a massive exec house to break even imho or they bail, right now that site is prob only worth 2.4-2.5mil, in a year 1.8mil.

Be interesting to see how much they loose, can you imagine building delays and sky rocketing costs for All their options. i am a bid at 1 mil.

in markets there is a saying

'The first stop loss is the cheapest, after that they get more expensive."

I imagine even the likes of the RE industry will now be resigned to the fact that the party is over. They will go from “Be quick, the property market is on fire” to playing up the housing price drop and saying “Be quick, prices have bottomed out and it is a buyers market”.

Met a colleague today, who is looking for a house in Auckland. His feedback is though houses are not selling and iare priced by negotiation but still expectation of vendor is quite high as much as 20% to 30%.

In last two years under Jacinda and Orr, prices have gone up so high that will take time for vendors to face reality.

Just checked another property, out of curiosity and think should be between a million to 1.1million maximum, is asking for 1.5million [1.495 million to be precised) and on seeing history realised that was just bought by vendor last year for 1.221 million ( vow) .

Even though is negotiable but when asking 30% to 40% more than present value, how does one negotiate. Also is he investor or speculator as surely investors buy to hold and not sell in few months or is it FHB and having trouble, now with rising interest rate and if in trouble will he not be looking to sell without lose instead of trying to make $275000 in few months.

https://www.oneroof.co.nz/estimate/1-87-cook-street-howick-auckland-man…

A number of readers would be aware of my Hutt valley Updates. I also track rental properties and in particular rental yields for the Hutt region. I have extensive records of houses rented over the last 18 monrhts that were brought in 2019,2020 and 2021. For those bought in 2019 the yields( ie the annual rental income (at the time of listing) divided by the house purchase price ) are averaging at 6%, this fell to 3.0% for properties brought in 2021 and in some cases the yield has been as low as 2.8%.

Now back in 2021 - there was nowhere for people with a bit of money to park it to get a annual income, but looking at the latest term deposits a number of banks are now offering 3.5% for a 3 year fixed term and 3% for a 2 year term.

Now I know a lot of people invest in rentals for the capital gains but given that's likely to be minimal over the next 2-3 years and they have the additional costs of owning a rental- maintenance, insurance, rates and keeping up with changing tenancy laws ( all of which come with substantial expense). this is likely to mean for many people who saw a couple of years ago residential property as a good return due to low interest rates are likely to park their money somewhere safe with a guaranteed return and minimal hassles.

This is only going to drive reduced demand in residential property even further until yields come back to a level where they make that hassle worthwhile.

Over next couple of years as rates go up prices will go down and a number of people will sale their rental before all gains have disappeared. Hopefully the market will return to a place that average wage earners can afford to buy and still have a life.new housing is going to take a hit developers will go bust in many places it could be government buy sites at reduced price and builds rentals which would take down rent cost, so many people living in cars and emergency accommodation if something is not done soon society will breakdown even more.

An overwhelming amount of DGM lately... is it really all over for the property market? Very early days & we know the captains of the Ship Orr & Robo could easily change direction, or are they trying to sink this ship?

... far from DGM today ... many of us are well pleased the housing bubble is exploding ... those insanely stratospheric prices have skewed our economy & our thinking away from productive assets , businesses , research ... into house flipping amongst ourselves ... rampant poverty & struggle amongst a growing % of the population , due to some getting uber rich at the top end ... finally , reality is setting in ...

the housing bubble is exploding

It's dramatic DGM statements like this that I was talking about...

It's fact. There's nothing DGM about facts.

There's a whole wikipedia article about NZ's housing market bubble, it's existed for over 10 years and I'm surprised more people weren't talking about it. Is it because talk of a market bubble and how it could burst and a fall in prices is DGM, so that's fringe and taboo? There are rules to civilised society I was not aware of.

Wasn't good to talk about it being a bubble when we were pouring taxpayers' money into supporting yields on 60% of rental properties, price subsidies (FHB grants etc.), and monetary policy into continuing to inflate house prices. Talking about would've made that stuff look a bit untoward - not to mention making taxing only work and not speculation look pretty unethical.

Big assumption is that the Levers and Tillers, clutched so firmly by Robborr, are actually connected to something at the business end....

Well... they could try to change direction.

Saying that they can do that easily is way more than naive.

This thing is happening in many countries, NZ is very leveraged, so the effects are more accentuated.

I don't see anything "easy" here.

It probably wouldn't of seemed easy over two years ago to slash the OCR, remove LVR restrictions and pump billions into the market...

They only did what everybody else did, just... more.

No real guts involved, completely predictable given the situation.

We are in a completely different condition right now.

But I see many invoking RB and GOVT, well good luck with that. I 'm sure they will recommend you to be nice

It wasn't predictable at all...

really?

The first QE was supposed to be an exception. it become the rule.

Multiple forms of money printing are The Answer to every small or big problem.

2019... voila, pandemic!! let's see what we do, oh yeh, I know, I have The Answer!!!

Not predictable?!?!? are you 12?

Now we got Inflation, and The Answer doesn't work anymore. Game broken. Game over.

Look back on interest.co.nz comments section 2020, I think you'll see many thought the market was going to collapse then and couldn't comprehend what Orr & Robbo were doing. Heck even economists were predicting house price falls then.

Eg. ANZ June 2020

We see house prices down 12%, which will weigh on household spending, with risks now more balanced

QE had started in March 2020 & LVRs removed in May 2020, yet that was the type of commentary being made.

https://www.anz.co.nz/about-us/economic-markets-research/property-focus/

Clearly nothing was predictable then & nothing is predictable now...

So... first of all, my apologies... I think I switched pricky and that is not me.

I'm only nervous cause I got covid.

Second, I was surprised in seeing surprised peps like you said.

For me (and for many) it was an obvious answer, what happened, nothing special, director cut

Robbo is fond of saying that our public & private debt is conservative , compared to other OECD countries .... forgetting that they have far broader based economies than us , are thereby insulated against a downturn in one part of their economy ...

... we're so reliant on China to accept our primary produce , if they place tariffs or a ban on us we're up Poo-your-pants Street , without a fresh change of nappies ...

Auckland and to a lesser extent Welly are so inflated, they'll be the first to drop and drop hard. In a day where you can work remotely on a 6 figure salary from anywhere in New Zealand, it doesn't make sense anymore for these big cities to command the premiums they do over other regions.

what happens to Turangi? if you guys are in a p ssing contest re akl vs wtgn> the regions are always worth less..... think about that.... sure i can trade any global book from turangi but what is its relative value> interesting nightlife.... i love the hydro pool but is it worth more then the commute from panmure

It's needs to be somewhat comparative. So instead of picking a cold dump like Turangi.. how about a smaller sized city.. like Nelson or Napier.

Why is Auckland another 40% more expensive where my earning capability is the same or similar.

Edit: my belief is economics will figure this out and correct the marker in such ways over the next decade.

If house prices are only down 7% on an equivalent nominal basis then the market has been very slow in working out that fighting inflation means putting a lid back on asset price inflation. This is not a time when HODL will work.

Nobody knows the future. The Reserve Bank could crank the OCR to the sky or drop it to the floor. If they decide to crash the market even more, there is a good chance they will tank the economy. Political suicide for the current government for sure. If the economy tanks then the NZD will tank as well. In October 2000 the NZD went below US 40 cents. 1 million NZD is around 675K US today. If the dollar tanks to 40 cents then that property will be 400K US. That would be a 40% drop in USD terms with the NZ price staying the same. There are many factors at play and lots of hands on the various levers. The biggest driver will be Labour and how it polls. Politicians will say and do whatever they need to to retain power.

Does a rise/fall in house prices really make any difference for the probable bulk of homeowners living in in the sole home they own? There is no change in relative terms if they decided to buy and sell at the same time. If you are leveraging off your house value to borrow then I can see it matters heaps. But surely not the case for most folks who are NOT property investors -it is just the home they live in. Income /wage changes relative to cost of living are far more important.

Try buying and selling if your property falls below the loan amount. LVR restrictions don't just go out the window when you're buying and selling.

I traded up in December, and was told I needed a minimum of 20% deposit. This is despite having an unconditional sale on my old property which was mortgage free, having cash (family loan) to bring forward settlement on purchase to earlier than settlement on our sale, and proceeds from the sale put us at well over 40% equity.

Best news of the year so far, keep it up!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.