Average dwelling values are now declining in most parts of New Zealand, according to Quotable Value.

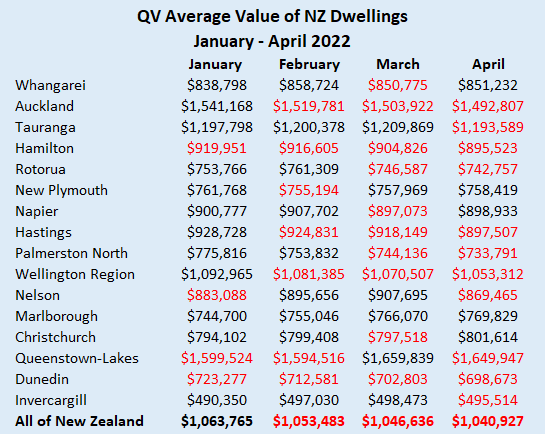

The average value of all NZ homes declined to $1,040,927 in April from $1,063,765 in January this year, according to the QV House Price Index.

While the $22,838 fall in value isn't huge, it is consistent, with average values dropping for three consecutive months.

It is also significant that the decline in values occurred over what is usually the busiest time of year for the residential property market.

The trend of declining values has also been spreading steadily throughout the country.

The table below shows the average value of residential dwellings in each region from January to April this year, with values highlighted in red where they were lower compared to the previous month.

This shows that in January just four regions had average values that had declined from the previous month. In February that number increased to seven, in March it had risen to 10 and in April it was up to 11.

In April there were only five regions where the average value was higher than it was the previous month compared to 12 in January.

The most consistent declines have occurred in Hamilton and Dunedin, where average values have fallen in every month this year.

The biggest decline since the start of the year has been in Auckland where the average dwelling value has declined by $48,361 since January, followed by Palmerston North -$42,025, Wellington Region -$39,653 and Hastings -$31,221.

The biggest increase in average dwelling value has been in Queenstown-Lakes where it is up by $50,423 since the start of the year.

"It's no surprise that the largest declines are occurring in locations that experienced the strongest growth over the past couple of years," QV General Manager David Nagel said.

"These markets were the first to become overheated and that makes them susceptible to a value correction as rising interest rates, tightening credit and affordability concerns start to kick in."

"It's difficult to see things getting better any time soon with interest rates forecast to rise further in response to inflationary pressure, while net migration is likely to be negative for the rest of the year as the borders open up.

"Fortunately we have a well insulated banking sector with LVRs having been in place for much of the past cycle and with the country at almost full employment, the likelihood of wholesale mortgage defaults is low," Nagel said.

The second chart below shows the percentage change in the QV House Price Index in each region over the three months to April.

The comment stream on this story is now closed.

109 Comments

Just the start of housing price correction with inflation high and rates raising, also NZD tumbling which will probably push inflation even higher. The decline in house price’s will accelerate.

Yes, the big correction has started.

It's now 7-8 months since house prices peaked. Yet significant segments of the market are still setting record prices.

No crash in sight. Property market remains the best long-term investment for most people.

TTP

The data is noisy, so there'll be little blips here and there, and maybe some genuine local effects. Nothing to get excited about - the market direction in general is clear.

Auckland housing in particular doesn't seem to stack up as an investment just now - I am happy to leave this field to those willing to accept negative cash flow and questionable future capital gains with a hostile government. I am more interested in the various NZX stocks with 8-10% yields right now, and a few interesting ASX stocks.

There's quite a few good stock and etf options out there right now providing good yeild.

Changes in Tauranga still lost in the noise. Still very slow to move downward when people claim a 30% drop is a given. Looking like the 2008 GFC all over again so far, bit of a blip I didn't even know had happened and we all know what happened from there.

For those with fuzzy memories, house prices took until late 2012 to recover to the early 2008 peak. A shallow but fairly long trough.

Of course many other countries suffered far worse at this time - NZ got off very lightly.

https://www.interest.co.nz/charts/real-estate/qv-house-price-index

And there were talking about “economic recovery post pandemic” on the news…

You seem to have a solid point here - houses like the one picked on below https://www.trademe.co.nz/a/property/residential/search?search_string=1… may be akin to that extra pallet of bog roll someone thought they could profiteer off, but anything with desirable fundamentals is still doing very well. Lots of chicken littles in here, but certainly not what I'm seeing and definitely ain't no 'crash' as of yet.

Investing in a home for yourself and your family is a good thing. Investing in housing in order to feather your own nest via 'people farming' isn't. I hope we can change the way houses are leased and tenancy laws and shredded and re-written and that they are owned by a combination of co-operatives and the state.

You can still rent your investment house out, as it is now, to those for whom such an arrangement suits best, but there will be a much smaller pool of tenants available

It was not so long ago that an ad for a rental "looking for a 5% return...do your maths........". Well I tried doing my maths yesterday. And reckon that 5% p.a. won't do , not anymore.

Reality is math has not stacked for some time. Commercial property trusts only promising 5% returns are in the same boat. Wont be long before term deposits are pushing that number with a whole lot less stress.

At that point there is only one variable that can change to correct the math. It starts with the letter "P".

Oh no, no no no. How will I afford my smashed avo on toast without my unrealised gains? I mean, I know I only have one home and would have to buy and sell in the same market anyway. But now I'm so much poorer than I was last year.

What ever shall I do?

Just wait.

And buy a jar of Biscoff.

Wasn’t the smashed avocado for potential first home buyers with large spending habits, so they couldn’t save the deposit?

I’ve never been able to buy smashed avo with unrealised capital gains.

May have been indeed. Still, the wealth effect has seen a number of those I know magically upgrade their lifestyle with new car, jet ski etc

House prices are doomed but has anyone a view on where farmland prices are heading? I see banks pulling back lending in this space. Will food prices/shortages support land values? Seen land prices decline in Europe after the GFC, they followed houses prices down, but took longer to fall.

looking to buy a farm at the mo.

Depends on the type of farm. There looks to be a mini boom in carbon farming that might keep some values high.

But with the govt considering ruling out the most effective and easy to grow tree species, C farming is going to get much much harder.

Its a Dairy farm with class 1 soils, figure that the forecasted food shortages later in year and next year should support land prices, its going to be a long term investment + 20 years, still I see risks for all asset values

The 'profit' in many types of farmland has been at cash out time (cap gains) not from the sale of produce. This has always been a problem for the sheep and beef farmers when holding onto the intergenerational family farm.

What a shame we didn't have more forward looking politicians - who weren't property speculators themselves - who could have used policy to reward productive work rather than land speculation. It would have been far preferable to reward hard-working Kiwis with lower taxes while having more balanced taxation of those who only sit on land to speculate.

Anything property only works out based on cashing out expected future gains. Make capital gains 0% and no property has paid for itself for 15 odd years!

The agri based funds and shares I'm invested in have all been gaining last few months. Not sure about local farm prices as these are all USA aussie based.

But my exposure here (and in a commodity etf) has largely negated the loss of share price against my usual growth / bond allocations

Finding agri to be a good hedge in these uncertain times.

Not of course to be taken as financial advice!!

House prices falling, but building costs rising - significantly.

Prices for NEW houses HAVE to keep on rising (inflation, shortages, higher wages and more regulation) or else the builders will fail.

But they ARE dropping - so guess what ? - the end of the labour shortage is in sight.

Land prices will probably drop. Significantly.

Yep, and developers going bust.

I built a house in late 2007, it was 2015 before it was worth what I spent. Just a basic 4 bedroom brick in the waikato.

A few commentors on here seem to believe that new housing costs reflect directly on what used houses are worth. I have mentioned a few times that this is just incorrect. I trained as a QS back in the roaring 90's, new was always more expensive. Thanks for your comment !!

What sort of a mass delusion were we suffering from, to think that the average Kiwi house was worth a million bucks?

The madness of crowds.

I agree 100%. Current valuations are completely ridiculous, so delusional and so out of synch with economic fundamentals and common sense that it is not even funny.

It's not funny - It's just the way it is. Our material and paperwork costs are horrendous. Most builders are not making a lot of profit. If a new house fails to sell for 6 months then the profit is gone.

There is very little slack in the COST of new houses, other than a a bit in the land. So what impact is that going to have on the market?

The demand is there - but not at current prices - and costs are going to keep on going up.

How do we square that circle?

There is huge slack in the price of land - how else can you explain such differences in house prices with Auckland three times the price of Invercargill? It's not much cheaper to build down there...

If and when the market calms down and building slows, and the worldwide supply issues begin to resolve, we will no doubt find some room to move in material and labour costs too.

I think the time is coming soon when the subbies won't be able to just make up a price for doing a job,a lot of the pricing has now connection with the time spent or hourly rate,it's just take it or leave it at the moment...might be a few less Rangers & HiLuxes being bought with cash soon.

Take the FBT tax dodge off utes and there'll be far fewer either way.

The average Kiwi house is worth over a million dollars. The average wage is the issue. Wages have declined in real terms over the last 40 years.

"Worth" is doing some heavy lifting in that sentence. Why don't you take a look at what a million kiwi will buy you overseas and then try and justify that price tag on a two bedroom rot box here.

Does this mean every registered residential valuer in the country is wrong? All house prices going down now, making previous valuations null and void.

Or has the word value lost its value??

As I've pointed out here for a number of years.....were the likes of the Irish, USA, Japanese, Spanish property markets 100% over valued at their peaks, or 50% undervalued after their crashes?

Not all… just the valuations that reckon a site in papakura that had a house on it and the year before sold for $650k is now worth $1.6 with no house on it.

but hey second tier finance companies will take that new valuation and lend $4-5m of other peoples money against it

of coarse if the project goes tits up at least they have a first mortgage over 800m/2 of bare land in the arse end of papakura that can’t be rented as collateral…lol

i think you get the jist of what’s been going on

by the way I see Jarden and Craig’s allocate five percent of their diversified funds into “alternative” investments… I enquired with a friend who’s in finance and thinks it’s probably ending up in development finance…can anyone confirm what the typical “alternative” investments are?

one way to get your returns up I guess

what could go wrong?

Alternatives are usually things like specialised hedge funds, catastrophe bonds, forestry, agriculture etc.

Valuers were very wrong in 87. Look at all the factors making then wrong again. Values completely devoid of any income basis, and only remotely related to development speculation.

No wonder the banks are in full handbrake mode.

Folks get your wet suits on... apart from upcoming winter, it will be handy for riding the RE market down a slippery slope

7% rates coming soon.

-30% by Christmas. Guaranteed.

Be quick!

7% by end of the year is a definite possibility, but I think that the 30% decrease will take a little longer, maybe it is something that will need a few months into 2023 before it happens, as the housing market is not as liquid as other markets.

If you do a little hunting, you could grab a 20-25% drop now. Trouble is it will be an unliveable POS unmaintained over the last 40yrs. It was never really worth that price in the first place but the new build next door may have been…

Yes Brock ...I would not bet against those figures. No fire power left to stop it.

I agree that would be my expectations as well. Perhaps not in that time frame but not much longer. With the NZD depreciating 5% you can add that to our inflation taking it into the double digits.

Unfortunately the point made earlier about wages is true. Even with a 30% drop we are still not going back to 2017 and Labours intervention.

As it should. Cheap money and greed fueled speculation has been waaaaay out of control for some time. Anyone leveraged to the nines, and inexperienced developers are now meeting reality, with a lot more pressure building.

Granny Herald says so.

https://www.newshub.co.nz/home/money/2022/05/reports-suggest-first-home…

What sort of a stupid question is been asked - as if a fall of 2% to 4% after a rise of 40% to 60% from already high prices in 2019/ 2020 does matter.

As a trend - downwards is good news but are value attractive - is a foolish comment to ask as know it is still a long way to go.

When presenting supporting data tables, can you separate out the Wairarapa valley from Wellington? The trend in all of the Wairarapa seems to be different from that of Wellington, Porirua, and the Hutt Valley.

The QV house price releases aren't that granular. You can search for specific regions on this page. https://www.qv.co.nz/price-index/

e.g.

Masterton District has increased by 2.4% over the past three month period with the average value now sitting at $707,635. This represents an annual growth rate of 16.5%.

Wairarapa. The adults playground!

The doller tanking putting pressure on interest rates rises, increases chances of more that one additional 50bp increases. Heard on the radio yesterday that petrol may hit $4.00. Thought no way, but if doller continues its fall it may be possible. Yikes.

Another comment / Headline in Bernard Hickey commentary : "First home buyers hammered to seven-year low by bank lending squeeze in March quarter; "

Why blame the bank alone, main culprit are all those who supported and promoted houses price growth , happening in double digit in a month, if not weeks and now with just 2% or 4% fall are shit scared and shedding crocodile tears.

FHB, not able to borrow in extreme may be a blessing in disguise if house prices catch up with fundamentals, which seems to be the case as economy cycle has taken over just like life cycle, which is inevitable.

I voted for John Key because he campaigned on dealing with the housing affordability crisis. Yet rising house prices soon became "a good problem to have" and a "sign of our success" (Bill English). I didn't vote for Labour but I did hope they'd do more than they have on housing, albeit they've done some good (e.g. making inroads into investor freeloading, tax-wise). However, they've also seemed to become National by nurturing house price rises instead and seeing rising prices as a good thing.

Have we an ideological infection in Treasury, RBNZ and parliament, something catchy that sees all regarding ever-increasing house prices as a good thing? There's history, I guess...it was ideology (and Treasury's, in part) that caused the leaky buildings crisis - the last most expensive, preceding yet ongoing housing crisis.

Similar attitude to myself...............however, got to hand it to labour, their new tax regime has evened up the playing field when it comes to fhb's and second hand houses.

In spite of everything, I am reluctant to vote Nat due to the unwinding of this tax. Pretty right leaning on most issues, however I'd love this tax to stay. Otherwise, no National vote...will go to TOP.

Agreed (this is becoming a trend Rastus :)), I voted TOP last time as they had the ideas, this time though they have fallen off the horse, the wealth tax is unworkable. The rest of their positions are largely the same but the wealth tax is a)unworkable and b)will simply create a new class of poor people with out resolving our current batch.

They really need to just simplify - perhaps an LVT on the unimproved value of land coupled with lower income taxes. Something that rewards hard work not just the sitting around on assets.

Yes, there needs to be something on sitting on asset valuations, I would start with something more basic like a flat 33% capital gains tax as it would be easier to administer.

Curious to hear what everyones thoughts on what the income to home price ratio 'should' be. Or what is 'sustainable' for the economy/next generation.

This might give us a better idea where house prices are going.

Median house price should be no more than 3x the median household income, at a resolution of no greater than a district level.

My thinking was an affordable DTI would be 3-4 (but doubt RBNZ would come to that conclusion straight off the bat), so with a deposit of 20%, median house price 4-5x median income would be inline with this.

No idea where this market bottoms out but it seems like there’s a hole under the rug that’s been pulled out.

I think we will get back to a ratio of around 4 or 4.5x median income. All depends on how high rates go.

3-4%

The issue is this:

Whatever the drop, if it's business as usual ie a rinse and repeat capital gains boom afterwards, then those holding property get through to retirement when they will need to use that capital growth as cashed-up income. ie 10x median income multiple. But if you have bought recently and are looking to retire soon, then it will be rough.

Or we reset at the bottom, which will be great for all the new future homeowners, but many others even if they can afford to hang on to recover some of their lost equity via normal inflation, will not be in a position to have any money left over for retirement. and will become Govt. dependants.

In the short term, a big fall could hurt everyone regardless.

Midterm depending on what we do, we are just trading one group against the other (homeowners vs renters), as we are doing now.

But long term, for the betterment of the whole economy, we need to reset policies at the bottom of this failure so no speculative rentier monopolistic capital gains can be had. This is different from true value-added development.

As far as what is a possible drop to get to a low sustainable median multiple. Simple maths shows that land and dwellings have approx. 50% of non-value-added costs, ie these are costs which our present policies have overinflated house prices by, and which the likes of low-interest rates act as an accelerate on.

With a new reset at the bottom, we would be better off for another generation to subsidize the homeowners that are trapped with negative equity than we would be to subside the growing inequity of the non-homeowners under our present scenario.

It has taken us 30 years to dig this hole but could probably get out of it in 15 years if Govt. got their %$*@ together, so at that time we are ALL better off.

You would own your own home at approx. 5x your median income. It would only rise by the annual rate of inflation. ie no capital gains. If you rented would be paying far less rent than you do now, but as a % of the value of the property a higher yield still so any rental investor now makes his return from yield rather than any capital gains.

We would all have more disposable income to save for retirement or invest in truly productive businesses. And can more easily pay for any user pays costs, like education, health, travel etc.

Too easy.

It is necessary and would make for a better country.

But it cuts squarely across a lot of entitlement mentality in our investors and propertied MPs/bureaucrats.

So when do you think the Government's going to jump in to try and save the day for property owners? Those polls on boomers probably aren't looking favorable at the moment. They've got an election next year to win remember...

That would piss off Maori Party, Greens and TOP.

There is almost no possibility Labour can govern alone, so they need to pay attention to them.

Also... for every vote of a boomer you recover you lose one millenial or one gen-x (you know, tax payers instead of tax consumers)

Indeed. Key point Boomers all vote. Millennials in much less numbers. Time to do so otherwise normal service continues.

I'm of the moderate opinion that Labour may actually be happy to lose the next election. Whoever governs in 2023 is going to have one heck of a time trying to dig the economy upwards.

I agree and I wouldn't be surprised if Jacinda gets out of Dodge beforehand : I mean why wouldn't you?!

The Nats will come in and save the day for property owners then...

Oh man, I am truly shocked.

You actually look like one that wants this madness to continue.

Why?

What you see that I don't?

How that would be good for the people to allocate most of what they can make in two life (or more) in an house?

I must think that you are just pretending to be that sociopath and in reality you are just trolling.

I suspect Nifty's sarcasm was lost in translation.

Or Nifty may be thinking they could not do worse on housing. Labour have had the greatest impact on housing of any government ever. The greatest gain in housing prices ever has been 28.4% for 2021.

hope so :D

To be honest, I have zero faith that Labour or National want to make housing affordable for your average kiwi. To me, it looks like it will be BAU and they'll do what ever they can to prop the market up. With a pending election, asset owners - who are the largest voting base, will be prioritised.

Only need to look at the Pecuniary Register of MPs' investments to see they have very personal motivation to bail out property investment with taxpayer money. Massive conflict of interest. It would be morally repugnant were they to do so, though.

I am not superconvinced about that.

Asset owners will split 50/50 between nats/lab

Give me one reason why a renter today would/should vote for any of them. And no renters will vote for national anyways.

With the grudge that has been accumulated so far non asset owners are going to be much more polarised than usual.

I see a good amount of votes going to minor (leftist) parties... and they are free to act/vote ideologically.

Stuff.co.nz headline - reflects the sentiment : Housing market downturn is picking up pace, QV says.

It's a Tom Petty song, "Free Fallin".

Wait for REINZ. I want to hear about properties that sold in April, not about properties that settled in the three months to April.

I suspect that the RBNZ were given a preview of the April figures prior to releasing their Financial (In)Stability Report on the 4th of May.

Case study. First glance reaction was WTF.

https://www.trademe.co.nz/a/property/residential/search?search_string=1…

Then you look at the history. Sold Oct 2021 888K. Some paint and a kitchen/bathroom reno. Now 930K.

Damn right you cant afford the mortgage. Who would. $500 a week would be more than fair rent. There isn't even an oven. Laugh or cry?

Cry.

Add it to your trademe watch list and you'll get regular updates as the price is reduced.... 800k... 700k...

Here it is in October 2021:

https://www.arizto.co.nz/property-search/17a-kereru-street-henderson/

There's an interesting video. Bought for 888k at the peak. Will be interesting to watch.

888 lucky for some, especially those with Asian sounding surnames

Sad thing is it had an oven back in October 2021 according to Zachary Smith's link above. They replaced all the cabinetry but decided portable camping stove was a suitable replacement. With all the storage cupboards on the adjacent wall there's no reason other than to skimp spending $2k on a new freestanding oven.

Amazing!

By the looks of it there's no logical place for an oven in the kitchen. The original had a splash...side...? Piece of tin foil on the wall. Kitchen would likely need to be re-done if you wanted an oven with a splashback.

What a lead in statement. Reckon its half of what they paid if they are lucky.

How many more are out there...?

One of the Mortgagors. Basecorp had an 800 million loan book as of October 2021. So that's encouraging!

Mortgage advisors selling on commission to BBB rated borrowers. What happens next. Sounds like a movie idea.

Anybody with 920k to drop on a house should be weighing up whether they want a life sentence in that dismal rat hole in Henderson or a life style just a few hours flight away.

https://www.realestate.com.au/buy/property-house-between-850000-950000-…

✈️ ✅

Quick title search shows that it's mortgaged to both Basecorp and Abcom. Looks like they could never afford a proper mortgage to begin with.

Nice Basecorp

https://tmmonline.nz/article/976519747/basecorp-secures-more-funding-to…

Abcom. Are you fricken serious

- Consumer Credit Contract annual interest rates range from 17.95% to 29.95%.

All we are missing are the strippers who own 5 houses.

Wow just read the Basecorp article, smells very familiar indeed...

So they may have been one of the crews who does a bit of tarting up then flips for profit, you reckon?

Lol

Things to think about before over extending.

Prices need to come down. Blood is acceptable and required.

They can forget about getting 888k back. My prediction is that if they are very lucky they may only lose 88k. Although I think more likely there will be a few suckers that would be interested around 750k. If they are unlucky, they may lose 444k.

The obsession with housing as an investment class rather than a basic human need is very problematic, and will continue to be so unless there is a significant mind shift in this country.

A price crash will resolve this.....and having discussed investment options with people from Spain, Japan, US and Ireland, and then compare them with people from NZ, Aus and Canada, its clear that experience is important....people who have never experienced a housing price crash, general assume that it only happens to other people/countries. Once you had one, it becomes a known and accepted risk (and associated change in behaviours).

Its worth noting that the upside of a property bubble erodes the ethical nature of its society..........(which we have clearly seen the last 5-10 years)...............then suddenly how humility returns after it crashes.....

The Scarlet Rot has set in.

I see red, I see red, I see red.

You have to keep in mind that inflation is running far above normal levels so in real (inflation adjusted) terms those falls are actually larger.

Few.

I could not understand why property investors were piling into the market over the last 18 months of the boom. Yes funding was cheap but liquidity from QE was very strong. Interest rates were at historic lows. A large chunk of the economy (hospitality,tourism) was very challenged. Most folk were aware of the greater fool theory and yet investors continued to buy.

Well its over now.

Investors are buying off the plan. I have a two-bedder coming on-line in July, it has been in the build for 24months and it needs to fall by 25% to not be worth what I will pay for it.

I totally agree tho that investors buying off the market are cruising for a bruising

Got a buyer sunset clause?

Many buying new builds to maintain the tax rinse on debt.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.