This year's Budget has raised or eliminated the price caps for First Home Grants and First Home Loans to take into account recent very high rates of house price inflation and is also providing additional support to not-for-profit rental housing providers.

The house price caps on both new and existing homes has been removed entirely for the First Home Loan scheme, however income caps for borrowers would remain.

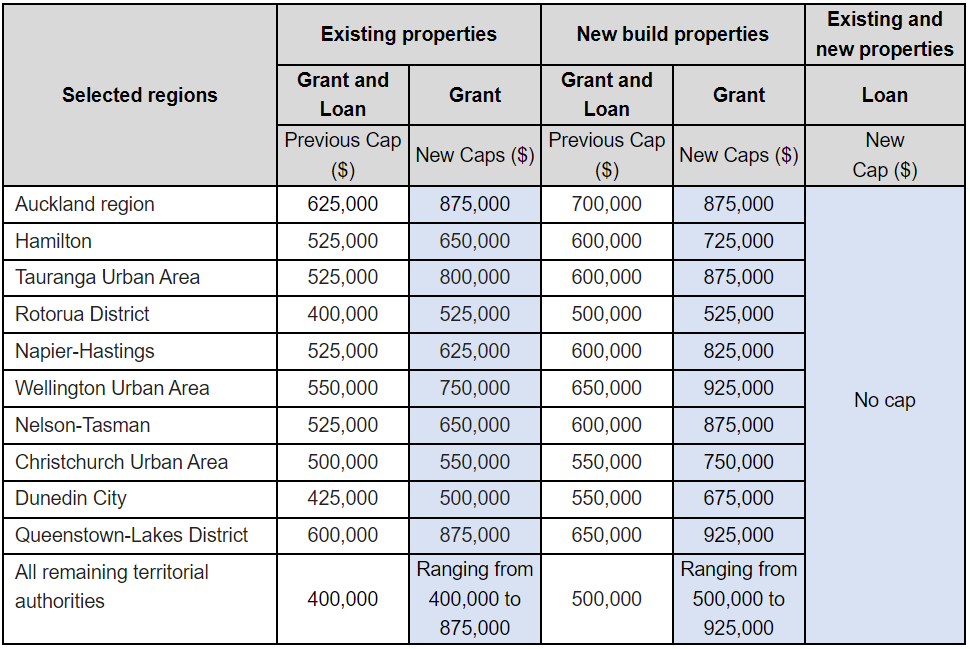

The existing house price caps vary by district, ranging from $400,000 to to $625,000 for existing properties and from $500,000 to $700,00 for new builds.

Those price caps will be removed entirely for First Home Loans from June 1.

House price caps will remain for the First Home Grant but are being increased substantially.

The current caps for the First Home Grant also range from $400,000 to $625,000 for existing properties, and will increase to $400,000 to $875,000 depending on location.

The First Home Grant price caps for new builds will be increased to between $500,000 and $925,000 depending on location (the table below shows the changes to the price caps in the main urban districts).

Housing Minister Megan Woods said funding would be available for approximately 7000 additional First Home Grants and 2500 additional First Home Loans annually.

The new price caps for the First home Grant take effect from 19 May.

Price caps were also being raised for the Kainga Whenua Loan scheme, which is available to people building, relocating or purchasing a home on whenua Maori.

The price cap for that scheme will be increased from $200,000 to $500,000 and will take effect from 1 June.

The Budget has also set aside $350 million for a new Affordable Housing Fund, which will assist affordable housing providers to build additional rental accommodation.

The first $50 million would be paid as grants to not-for-profit organisations to provide affordable rental housing in Auckland, Tauranga, Rotorua, Napier/Hastings, Wellington and Nelson/Tasman.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

20 Comments

No change to the income caps though.. which is a bit odd

They are trying to save the housing market to save themselves electorally.

The banks are not going to be willing to lend to marginal FHBs at excessive prices while prices are in free fall. The entire first home loan system is designed to be a price floor for the market.

The way it should really work is having no price cap at all, but having a serviceability test of whether the borrower can afford payment at the stress test interest rates using less than 50% of their income.

Removing the price caps and keeping the income caps just as the RBNZ is about to slam DTIs into place is a bit of a cruel joke, isn't it?

A very woke budget.

From a woke government....

Each time the cap has been raised, the price of entry level homes rises to about that level.

Wonder what'll happen with no cap.

Exactly. It's a Universal Pricing Signal.....where caps still exist why sell for a cent less than the cap? And Universal- so oh no Cartel.....

I think the other side of the coin is people will spend as much as they are able to.

Wowzers...no matter Labour or National, there's always this eager look to how we can pour taxpayer money into enabling young people to pay more. Price subsidies. Rental yield subsidies. We always seem willing to throw money at enabling higher prices that benefit speculators...

Morally reprehensible that we have been pouring so much taxpayer money into supporting or pushing up house prices and rents through such subsidies.

Yep without strict regulations on debt limits, these subsidies are enabling unsustainable house prices. The increased price cap is an admission of acceptance that they have nothing up their sleeves when it comes to affordable housing in NZ.

Ironically, should RBNZ implement regulatory DTI next year, this, along side rising interest rates, would be the most oppressing factor in house prices in NZ - and the government wouldn't get the credit for it.

Totally agree Rick, absolutely morally reprehensible. I’ve now come to expect this from our politicians especially around housing. Zero integrity, no real intention to address housing crisis, just empty rhetoric.

interesting link

https://www.macrobusiness.com.au/2022/05/ardern-hurls-first-home-buyers…

Increasing the caps and having no restrictions with accessing Kiwisaver for buying a house is good...although some will say that you are robbing your future self. I am very much a - more benefits exist with owning a home vs fewer benefits exist with renting a home...provided the rent you would pay is equal to or greater than what you would pay to own a house - buying a house is better. And I would go so far as to allow an increase in the term of mortgage provided it achieved the previously mentioned statement. Some may say that this statement is most definitely pro landlords, I believe it isn't because the person makes the decision to own their own home, they will look after their own home, and over time they will create equity that allows them to trade up, over time they will be able to pass their benefits to their children through a will and the passing down of the house/equity to their children - they will not pay a landlord rather they own the house but will pay the bank...just like a landlord would with the likely mortgage they have already. If you rented your entire life and were not able to create wealth in other investments, then there are no financial assets to pass on. Also purchasing a home and raising your family there that is passed onto your children has much more benefits than just purely financial. Early on in my life, paying rent to a landlord over the long term did not make sense to me.

FFS. Can this mob plunge any lower in terms of cluelessness?

This is close to meaningless.

Have I got this right - all this means is that the price cap to get a 10k grant…. Yes a measly 10k… has increased massively.

It will make almost no meaningful difference to the barriers that exist to buy a 875k property in Auckland - being size of mortgage relative to income, and rising cost of finance.

That is for a first home grant, however for a first home LOAN there are no limits related to the house price, rather it is with your income (single person 150k pa or less)...but this gives the borrower the ability to get 95% of the home loan with a 5% deposit tapping into your Kiwisaver (provided you have contributed to it for at least 3 years) - I believe. The number of these loans is 2,500 per year, so there are control measures and restrictions.

Thx. Realistically take up of that will be low, because of mortgage serviceability

Labour's just getting started on the housing market... let's keep this moving.

Moving ‘at pace and scale’

Like a Large Glacier....

Hopefully price’s will continue to fall this is only hope for FHB in Auckland. The market is way overpriced a young couple would need to be earning 250 k income between them and have 90k for deposit no children or debt.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.