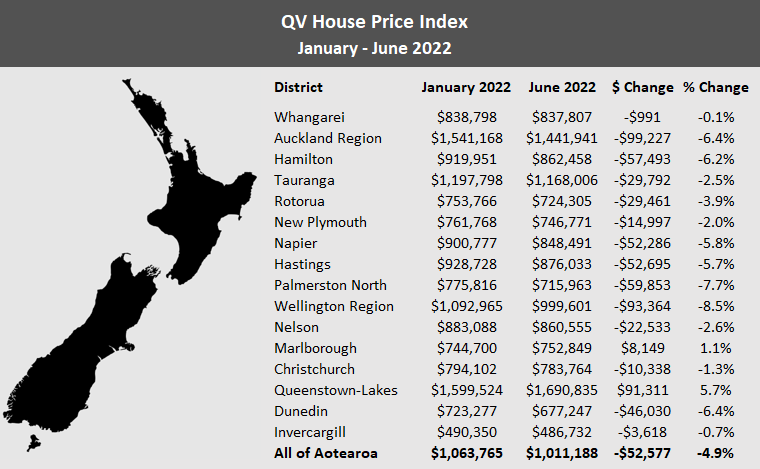

The average value of New Zealand homes is down more than $50,000 since the start of this year, with average values in Auckland dropping by almost $100,000, according to Quotable Value.

The average value of all NZ homes was $1,011,188 in June, according to the QV House Price Index, which tracks property values across the entire country. That was down $52,577 (-4.9%) compared to January when the average value was $1,063,765.

Only two of the 16 main urban districts tracked by the HPI had higher average values in June than they did in January, with the average value up by $91,311 (+5.7%) in Queenstown-Lakes and $8149 (+1.1%) in Marlborough.

All of the remining 14 districts had lower average values in June than they did in January, with the biggest declines occurring in Auckland -$99,227 (-6.4%), Wellington -$93,364 (-8.5%) and Palmerston North -$59,853 (-7.7%).

The table below shows shows the average value changes in all 16 major urban districts.

"The QV House Price Index for June shows the housing market continues to feel the heat from rising interest rates and an oversupply of listings," QV said in its latest report.

"Credit constraints are limiting the number of new buyers entering the market and a combination of newly completed developments and existing property being listed for sale means there's significantly more sellers than buyers, which is putting downward pressure on prices."

QV General Manager David Nagel said further price reductions were inevitable over the next few months, as what he described as "this home value correction" continues across Aotearoa.

"All eyes will be on the next Reserve Bank Official Cash Rate announcement as interest rates are expected to rise further to counter inflationary pressures," Nagel said.

"While prices are retreating across the country, the increase in borrowing costs means debt servicing and credit availability remain key stumbling blocks for new entrants to the market," he said.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

131 Comments

It was not so long ago, the Far North was one of many rural areas was where the poor could buy an ex-rental for $175,000. Sure it needed some work, and far from the buzz of a city, but one had a roof and a garden, with space to build a carport/shed.

Then it changed, demand from outside crept in. Prices sky rocketed in line with the bouyant market in Auckland.

With every sale, profits went into the bank account. Anyone who was an observer, and had the means and the will, got into the bandwagon. Tradies, used car dealers to grandpa and grandma.

All during COVID. A curse for some, and a blessing for others.

After two years of euphoria, our Gov't stepped in with legislation aimed at investors, mega landlord became a dirty word in social media.

Sales at auctions dropped, but not prices that increased, for another 6 months. Interest rose, and higher borrowing burden is perhaps the final nail.

2022 is the year of a correction, but will it make housing affordable.

I hope so, but some like wages, power, council rates, never go down.

'Tis remarkable, the constant rhetoric that "we need investors and things would be worse without them". Whenever they hit a regional location in numbers suddenly affordability of ownership and renting both seem to hit crisis levels.

Trends are right but the data series feels slightly behind the current auction sales, what do they base the series on?

Mostly settled sales coming from councils, can be 2-3 months behind the unconditional agreement date as used by REINZ, So you're right, this has happened already and isn't new. REINZ are 5.6% drop for the quarter reported last month and I'm betting it will be 6.5 - 7% down for the quarter when they report next week.

Hopefully this correction will break the kiwi psyche that housing is a one way bet…one can live in hope

But...but...but...property cycles...Ashley Church....

"I don't care, i'lL JuSt pUt uP mY rEnTs"

Sorry to say nm46 but rent increases are a fact of life, that ain't gonna change and is one reason why it is better to own. May not necessarily be in step with housing market either.

Of course people would rather own than rent. That's the problem - people are renting because they're trapped, not out of choice. That's not really my point.

B-b-b-b-b-b-but where will people live if we don't have 50% more landlords than FHB every month buying properties? (RBNZ C31)

Mind you, the last 6 months has seen this ratio drop down to 1:1.

Not true for everyone. Some people prefer the flexibility and convenience of renting. I think the issue here is that New Zealand is a shit place to rent. Landlords are not competent, the properties are substandard and tenancy regulations are not great.

Yes exactly. There are a number of reasons, especially for flexibility to be able to move to take advantage of opportunities as research shows, that renting is better than owning.

And in jurisdictions with stable housing markets, it makes very little difference in lost cost opportunity at what stage of life people buy. Which they do when they want their forever home and want the practical and emotional benefits that homeownership gives many people.

And because we don't have a stable market, yes it is a shit place to rent for most people.

Agree with all the problems described above. In addition, we have the highest rent to income ratios in the OECD.

Renting is simply too expensive. It has become oppressive.

NM46 If you think that landlords put up rent simply to spite tenants, then you are quite wrong. Most M and D landlords know what it is like for families etc. However there are people who on anonymous websites, like to paint others as evil personified.

Anyone who goes all in on that idea usually lasts 5 years before going broke

The reason for the price decline is really around interest rates and banking rules.

For example, the maths for first home buyers is now horrible

A year ago they could put a 10 percent deposit down and borrow at about 2.5 percent interest

Now they need a 20 percent deposit and to pay around 5.5 percent interest.

But at least the leaky sh**box you had to pay $1.3mil for in Auckland is now only $1.2mil...

For now. Interest rates now have borrowing power at 30% lower than last year (2.5% to 5.5%).

The speculative printed bubble is deflating. Quickly. Declines are more restrained than euphoric booms. Accordingly the much this quick is quite telling. One the herd panics, as listings indicate they are, it's all on for love and thunder.

Next MPS review in 5 days. Inflation is out of control.Another .5 or .75...?

Agree so far decline is more restrained than euphoric boom. May be more to follow soon.

Many houses listed are those that have been bought within last year or so and are trying to free themselves as now worried just as buyers were earlier. For all houses, reason for sell by agent is that vendors situation has changed.

House prices are down but still not much compare to the rise.

Houses selling pre pandemic for near around $900k had shot to 1.1 million ....1.2 million...1.3 million and some were even expecting 1.5 million plus.....yes this was the level of craziness...asking any price and why not as were also getting as it was now or never for those trying to secure basic necessity - Housing for themselves and their family. This FOMO was very well fuelled by RBNZ - printing and throwing literally free money, which was supported by Labour government.

No doubt today the expectation of 1.5 million is missing but still expecting 1.4 or 1.3 million for those houses .....and may be if desperate to sell are offloading at 1.2million plus ....still far from fall.

Fall YES but meaningful, NO. Next fall from this level, if and when it happens will be to look out and may be make some sense.

All downturns happen over a long period of time.

Eat your popcorn slowly so you have plenty for the whole movie.

Its an exciting/interesting period as it seems impossible for anyone to make predictions. But the opinions are interesting on the way.

My take is that it depends more now on human psychology and peoples reaction to the rate increases than the rate increases themselves. Habits (high spending), beliefs (house prices will always rise and global geopolitical stability is the norm ) take a while to break.. but break they must to tame inflation.

Also important to note is that global economics have become weaponised in the new 'cold war'.

Just this year we see the new geopolitical norm as groups of nations working together to implement and avoid sanctions, build nato, withold energy, constraining supply chains, witholding food, etc. Leveraging globalisation (which is hard to stop) to pressure democratic populations economically

Along with cyberwarfare and strange proxy wars this is a whole new driving factor in finance.. which will continue for a long time. The consequences of this on local economies and their effecta are hard to predict and largely in the hands of the elite decision makers.

So anyones guess but unlikely the usa china and russia will all suddenly make up and accept the usa should remain global kingpin.. thus long term economic uncertainty seems to be a given.

100% - given that most mortgage holders are on fixed terms.

Let's just wait and see what happens as re-fixing comes up over the next 12 months.

From historical low interest rates to more middled rates - it's going to be a whole different ball game.

TimeToPuke

The eternal question: more debt, less space, in a more central place, or the same debt, a much bigger block closer to the urban boundary with more space for kids and spring for an EV to help with commuting costs? One is losing its appeal much quicker than the other at the moment.

I think the Queenstown Lakes entry in the table shows how people are answering that question since the pandemic.

Is it? Would be good to know how many families are moving to Queenstown Lakes. I got the impression prices were being pushed up by retirees, holiday home owners and foreigner's buying apocalypse bolt holes. All of these people have better access to credit hence the high prices. But this is only anecdotal from what friends that live down there have told me. Would be great to see data on it.

The urban fringe is where the American dream is now being rediscovered. But these fringes remain widely disdained in academia, media, and the planning community.

https://americanaffairsjournal.org/2022/02/exurbia-rising/

Someone posted a link to this article a while back. I’ve read articles from NZ and Aus about similar trends.

The trend is back to the fringe and beyond to smaller regional hubs. Some of it is driven by work-from-home opportunities but It's no coincidence that in apocalypse movies/times that people flee the city to the safety of the countryside.

Getting close to 'sustainable levels'...

I can see the headlines soon... 'NZ house price average now under $1 million!' Implying it would now be be affordable...

History, human psychology and the typical series of related events suggests this will play out a long period of time

So maybe the headlines will evolve something like this..

August 2022 - approaching sustainability

Feb 2023 - sustainable

Nov 2023 - below sustainable

July 2024 - approaching affordable

Jan 2025 - nearly affordable

Dec 2025 - affordable

(Odds on i reckon)

With all the interelated headlines about unemployment, business bankrupcies, resources wars etc..

Then of course a plateau for a couple years. Followed by the news we should all invest in houses.

Hope it has an upswing in the meantime but history suggests its unlikely.

Sustainable based on RBNZ's definition...

NZ average house price under $1 million will get hyped up by media, property commentators/economist as a victory for FHB Implying that it's now the time to buy...

Yes for sure they will keep trying to convince people to buy all the way down.

As the RE agents, mortgage brokers, developers etc still have to try to make a living by convincing people to buy.

Over time (if i remember the previous cycles right) people increasing leave the RE industries in larger and larger numbers and the downward trend becomes so obvious that the number of positive stories dwindles.

Housing price falls are always slow, people are now starting to realise the crash is inevitable. This quarter prices will continue to fall but at quicker pace so if 100k drop in last two quarters this time same amount in one quarter. If inflation stays high and NZD keeps tanking rates will have to continue to climb causing more and quicker falls, nobody knows how long the downturn will last for but if you did sell last November these price’s will not be seen again for years even with high inflation.

If and when the headline is Auckland house prices under $1 million.

Be quick!

Love the headline photo.. reflective of the current housing market.. pictures speaks a million words!!!

If 20% of population is thinking of quitting NZ.....

https://www.newshub.co.nz/home/money/2022/07/cost-of-living-myob-poll-s…

6 weeks left for us ✈️✔️

When you get there popping into Waitrose or M&S is hilariously dirt cheap. Enjoy!

I'm considering it. Sick of this government. If you want to achieve, best to leave.

Genuine question, do you think National would provide better opportunities to 'achieve'? If so, why/how? How are you being constrained?

I get the impression people don't believe National will fix it either (or even intend to). Personally I put a lot, too much, faith in Labour making progress. They did the opposite, which is probably why so many are feeling defeated and deflated towards NZ. Just my take. I feel our problems are beyond both of them now, as we'll need leadership (not caretakers to the status quo) and uncomfortable selfless decisions need to be made.

And I don't think Labour's "yeah well National are worse!" tactic is working.

I think the failure is about equal but just so much harder to take given the specific mandate and absolute power with which Labour have to make changes, and almost all of that political capital is being used to promote ideological centralism and Wellington-driven thinking. Great if your job involves having a steady stream of cases studies for transport projects around the country, bad if your standard of living involves someone ever actually building something.

They are giving the people what they want, not what they need. This is the nature centrism, it's how Boris got in and stayed in power for so long.

If you try and enact actual policies to enable the outcomes you stood on people get up in arms. Look at any one of Labour's major promises and then look at what happened when they tried to enact policies to actually deliver those outcomes, they got smashed by the media and Joe Average.

If you take transport as an example, you'll see people support a transition to better public transport, cycling and walking but this means you have to take some of the priority away from cars like reallocate traffic lanes and reduce the amount of free parking. As soon as anyone tried to do this people have a hissy fit. It's wanting to have your cake and eat it. Nature of democracy, until things reach crisis point people are in denial and it's very difficult to make change

Very true.

Yep, nail on the head!.

People want change. They don't want TO change.....

They want everyone else to change so they don't have to, too often. Change is like another version of taxes.

Absolutely spot-on. We get the government that we, collectively deserve.

I think Labour had good intentions but simply lacked the talent or intellect to deliver anything.

Or lacked the buy in from various Government departments who have their heads stuck so firmly up their a**es? Remember it's these departments that are tasked with delivery. Central Government can only vote to legislate and direct funding in various directions.

We all knew what the Government's intentions were, which is why we're discussing the failures. And yes they should be held accountable for these promises, but we should also look past the party and deal with the wasteful unelected bureaucracy that plagues our taxes.

I do recall the head of MOH on TV at the start of COVID saying the government had given them a blank cheque. Did note the biggest constraint was skilled people, though.

True, I'm sure there's no shortage of skilled people to procure additional ICU beds for example through, say, a competitive tender process?

Yet we wait until 2021 for the Beehive to release additional funding for ICU.

https://www.beehive.govt.nz/release/funding-extra-icu-capacity

That's additional over and above the blank cheque given earlier on. Doesn't seem like a blank cheque is particularly constraining on finance for increasing ICU capacity as part of a response to COVID.

Moreover, I think his point was it's not that hard to buy beds but the beds aren't robotic - they need skilled people.

6-12 months for us. Just watching that exchange rate :P

We may be over reacting but are also considering it. We will likely need to take a huge pay CUT and its not cost of living that has got us down. Its things like not being able to get our son in day care for years, not being able to get on a GPs books, not being able to get urgent care for him at hospital last week (hes 9 months old), neighbours houses getting broken into, friends getting assaulted in Welly CBD, friends cars getting stolen the list goes on. I know we won’t do it but the thought helps reduce the frustration sometimes…

Sad indictment but well articulated.

All these "signs of our success" and "good problems to have" are starting to get people down. Beginning to sound like they're not actually good problems to have, after all.

Looking to get out of here asap - Aus here we come

Oh goodness gracious.

You shouldn't say utterances like that around here, the resident moron brigade will be after your blood.

Bluster and fluster. There is nothing better than enduring what's on offer in Nu Zuland. It's the bestest!

Sorry to see you go but you will be replaced by a high net individual who will probably be investing, creating jobs, or just building a bunker

The UAE, Australia, Singapore, Israel, Switzerland, the U.S, Portugal, Greece, Canada, and New Zealand ranked in the top 10 in attracting U.S. dollar millionaires, a group it also calls high net worth individuals, or HNWIs.

https://www.forbes.com/sites/russellflannery/2022/06/15/uae-ranks-no-1-…

Indeed.

It is unquestionably true that every aspirational kiwi driven out of New Zealand is being replaced by millionaires.

Be great if they actually had to invest in businesses that created jobs.

This is a bigger threat than anything else New Zealand faces. People who have taken more than their fair share from their own countries coming to do the same here because their own countries have collapsed under the weight of inequality. Be careful what you wish for, I see Greece is in there, isn't there something about Greeks bearing gifts?...

NZ is in for a bout of nasty stagflation. Less tax payers as boomer wave is retiring and moving to net tax loss with pension and greater health costs. Their property greed is driving their kids and gran kids to Aussie, which is a net tax loss after 13-18 years of tax loss feud dating and pro riding health care to raise them.

Winning...

It’s not just housing that is going backwards. I spoke to my best friend yesterday who manages a retail shop that sells home appliances. He said the last two weeks were particularly terrible in terms of sales and it was the same throughout the whole country. People are struggling with inflation. Housing is not exempt from the pain that is coming our way. Get those seat belts buckled up. We are heading for a rough landing.

Ate at Ippudo at Sylvia Park last night. About 25% full.

Typically in the past, when I have been there on Thursday nights, it’s been upwards of 70-80% full

It's probably up to the folk who received the most benefit from upward wealth transfers in the last couple of years to keep hospitality going now. Average working Kiwi families won't be doing that as inflation continues to bite.

There might be a few low LVR FHBs from last year, now in negative equity around the country (but who perhaps don’t realise it yet - I wonder if the banks do? 🤔)

Does it matter if they're paying the mortgage, enjoying home ownership & moving on with life...?

Wrong attitude for this site. They are to be dressed in flax shirts and flogged to death and then we will have a democracy

Negative equity is not a breeze even if your mortgage is fixed for long time at some point mortgage will go up could be paying double amount, people feel trapped can’t move young couples with kids really struggle this over a long period can lead all sorts of problems.

Shhh you're not allowed to talk about the effects of house prices coming down, you have to just pretend there's no downsides at all.

If they jumped in with a short-term fix, it might matter a lot very soon. What do the banks do when someone comes to refix and is in negative equity these days? In 1990, my parents were forced to sell and spent the next 6 years paying off a debt they no longer had the asset for, while renting.

I'll use the words 'depends'....as long as they don't need to move, don't get divorced, don't lose their job, don't have an unexpected health event etc.

But having witnessed the stress that people were under in the US during the GFC that were in negative equity, it may not be the walk in the park that you are possibility trying to say it is? (if that is the point of your post?).

There were stress related deaths resulting from negative equity and job losses in the US so it may not be just as simple as getting on with life and paying the mortgage.

Then again, if you have never experienced such an environment, its possible that one can be naive to the negative consequences of such circumstances - my warning is that it isn't great and should be avoided (if it happens to a friend or relative that you know, it might be enough to push them over the edge).

Never been quite sure that they are the ones the banks look to first.

From a cynics view point it's the ones struggling on maybe 70-80% lv where the banks will retrieve all their money quickly who are the go-to.

After the Royal Commission the banks will do all they can to keep families in homes, investors... not so much. They will look to close out Investors first. I know that there are people in the commercial borrowing space under a lot of pressure to sell...... they leveraged there assets and purchased residential housing now the bank is actively pushing for them to lighten up debt wise, some have been through auctions and got no bids.... these will be the first or amongst the earlier vendors to have to accept whats on the table. Some of these purchased in better suburbs as well.....

This is a tragedy for any person trying to buy their first home. We bought our one and only house in 1991 for $138 in New Plymouth. Just like everyone else to put a roof over our heads and raise a family. I was on $48k at the time. A good salary at the time. My wife was a stay at home mum based on my salary. $38k deposit. We kept our $100k mortgage quiet as we were embarrassed about the size of it. But we loved the views etc. 31 years later the house is worth north of 1 million. Same house, same section. If our son wanted to buy it he would have to save $200k for a deposit and have to service $800k plus! For a 1940’s bungalow in a small city. I feel despair for our children.

if you had to rebuild on the same spot, what do you think the cost would be...... gives you an idea of our problem.... building is so expensive here and people want new vs old. Often ending up with poorly built new.... Its very sad and younf mid wives nurses teach voting with feet and going offshore where they can get a lot more for way less..

Yes very sad IT GUY. Our son is considering the same thing. On above average money with good prospects but living in Wellington no chance of buying something. Earn another 50% more on salary in Oz. Advising him patience as like the rest of us he has to wait for promotion. He says these days people have to change employers to increase salary substantially. As waiting for pay rises takes too long. Only way to enter the salary territory high enough to afford to buy he says. He is tempted to jump the ditch to get that salary bump. Of course the Oz situation is similar to us in the big cities. With stamp duty to add to the costs.

Rebuild costs based on house insurance approximately $700k as it has rimu etc. Madness. I think where we have gone wrong as well is the land price. Farmland on the outskirts of a population centre is rezoned. Now worth a huge amount more with subdivision. Why not subdivide based on land price plus a reasonable margin to reduce land price for our kids?

Yes lots of big companies give a generic % pay rise, the ONLY way to truely see what you are worth is to shop around and consider moving companies... land bankers own the next two farms of subdivisions.... councils want there dev fees and GST goes on everything..... opening up so almost anyone can subdivide is one way but someone has to build the schools roads water etc....

Your son is not wrong here. I moved to Oz in 2018. Went from 60k to 90k immediately. And then to 150k over four years over 3 employer changes. Obviously individual circumstances vary. Under the capitalist model businesses are always incentivised to keep wages to stagnating or falling. And over time overwhelming proportion of businesses/business owners will always act towards their incentives.

My parents bought in Howick in 1989, and couldn't sleep at night knowing they'd just forked out $166K for the place (150sqm 4-bed on a 900sqm section with separate double garage/workshop), which was more than twice their combined incomes. Horrible, horrible times.

Now they have 5 properties scattered across the Coromandel Peninsula. Horrible, horrible times.

The conditioning of the last 30 years means that people assume if they take risk now that they will be rewarded down-track.

But like concept of Taleb's turkey, it might also mean that you have decided to become the fattest turkey the week before thanks-giving.

Very funny.

We had the opportunity to get on the property owning bandwagon at the time too. Friends of ours certainly did. Based on the taxation advantages at the time. Became quite wealthy. There were so many courses about getting rich from property ownership and books written. Can’t put my finger on exactly why we never got involved. Didn’t seem right in some way. Our friends were constantly dealing with problem tenants and stressed all the time. I find it hard to blame them for their choices at the time as we were not far away from the disaster of the stock market crash in 1987. Zero trust in shares. I do not begrudge them their wealth from property. I do begrudge the governments of the time abrogating responsibility for housing the poor. All in the name of the balance sheet. Cash was king then in the eighties. Sell off anything to pay down the national debt. At least that was how it was sold to us voters. With disastrous consequences unfortunately. Here we are today with most if not all of those tax advantages wound back and we have unaffordable housing.

But they pulled themselves up by their bootstraps......

What is the point of your comment?

That your parent were geniuses and now they happy people?

I think that a man is miserable if he need 5 properties to feel rich/safe

Yes... horrible times when people brag about these things.

You might need to take a course on irony or similar abstract concepts.

I suspect English is not your first language and you have missed the subtext of my comment.

They aren't geniuses, but they certainly think they are. For them it's a case of being born at the right time, and then grabbing all the prizes before younger generations even had a chance. They weren't even high income earners, both of them were primary school teachers. They live a life that no teacher couple could afford now. Many would be happy to scrape together the deposit for even one house.

My apologies.

I missed the sarcasm.

English is actually my third language (or fourth depending on povs) , so I misinterpreted.

I've spent a fair bit of time in NP over the last 5 years and the current vibe is a lot like Auckland about 5 years ago : tradies screaming around in new Rangers, couples furiously renovating & pumping money into do-ups etc ... you can almost smell the capital gains on their breath. but I fear that the music may stop soon and someone has removed the chairs.

3x your median income gives us almost bang on what you paid for your house and is recognized as affordable in a functional housing market. This time was one of the last years it happened. I wonder where you have all heard that before?

As we move away from this measure is more and more a sign of a dysfunctional housing market to where we are today at 10x median income and the peak of the boom.

The real despair is the solution is known and is best reset at the bottom of a cycle, but our politicians will be too gutless to make the correct changes when the time comes.

Plenty of solutions available. Only thing missing is political will.

It's not political will, it's political mandate.

There is no party that will win a majority on a policy platform of crashing the market to 3 times average national income. Any party that is in power if that were to happen would struggle to get re-elected.

Disagree. The disaffected and non leveraged who want their grandchildren raised in NZ far outweigh the leveraged speculator community. I think promising DTi of 3x on investors, and helping the small group of recent FHB'ers with redirected accommodation supplement could be a winning policy. Any polling would clearly identify this as a no brainer. Anyone leading such a policy would exit their own rentals down to this margin before the election.

Watch this space...

Unfortunately you can't crash the market just for investors, that makes no sense. The owner occupiers who are also responsible for buying at inflated prices will have to take a hit.

Yes you can. That Rent subsidy teat that landlords have been sucking on for decades can be redirected to support leveraged FHBers, or ex tenants who want to be home owners. Let's flip the property incentive to keep young Kiwis in NZ vs. driving them offshore and making National party voters fatter.

Both parties have run on addressing the housing affordability crisis and prioritising productivity, yet both have seemed to abandon ship on affordability once elected. Sounds like a mandate without a will.

Yes exactly, we had National say they were doing to fix it, and acknowledge what the right solution was, but lacked the will, ie reneged on their election promise.

Labour initially had the will via Twyford, but used the incorrect ideological methodology, with the inevitable failure.

No, National reneged because they didn't really have the answer, it was the usual get rid of red tape, be more efficient, invest in massive roads bollocks that sounds good on paper but does nothing to address the issue, because it isn't the fundamental problem.

Labour reneged because when they suggested doing some of the things that would actually address the problem they realised they would get booted out.

I and a number of others had meetings with National's Senior Ministerial advisors. They knew alright. They either didn't want to upset their multiple property-owning voters, or they didn't have the MMP majority to do it. Not sure which, but the result is the same as you say. And I don't see any difference in the present lot.

Labour's ideology and incompetence prevented them from succeeding.

974 brand new townhouses and apartments for sale in Auckland on Trademe today. Slow and steady march towards 1000.

Absolute joke, the greed from these property developers is appalling. Who's going to pay 1.2 for a shoebox in Mt Albert. My prediction will be developers wont be able to flick them and they'll rent them to the govt for emergency housing. Love to see the state of these in 10-20years.

https://www.trademe.co.nz/a/property/new-homes/new-townhouse-terraced/a…

Or the govt bids a mortgagee salee... in some cases finishing the builds

$1 reserve, and let the govt bid. The government can always employ the tradies to complete the work.

2 interesting charts which tell an important story for those that are interested

https://tradingeconomics.com/new-zealand/price-to-rent-ratio

https://tradingeconomics.com/new-zealand/money-supply-m1

Which equals lower and lower yields, it that were possible. All in a time of increasing interest rates, and less tax rinse from debt vs income tax. What could go wrong...?

And the good news is that if house values fall faster than rents, then the yield improves without the landlords having to do anything.

Unless the tenant moves for lower rent elsewhere, and then you have to find new tenants unless you then have to lower your rent. Love how people think rent can never decline.

I'm not sure how your comment is talking to my point. If rents were to fall faster than value, then the yield would decline. At the moment value is falling faster than rents, mainly because there is a lag between people wanting or needing to move due to fixed-term or minimum notice requirements.

My point is, while landlords/speculators may not be happy with falling values, their yields are increasing because of that, so perversely they should be happy (but won't be) if the real reason is they are yield driven which is what happens in a more stable market, or in dysfunctional markets for a brief period of time when the boom/bust pendulum swings the other way.

Yield is pretty funny measure though.

If a landlord bought a house with for $800k, rents for $600 per week that's a 3.9% yield. House drops to $600k, yield is now 5.2% but they've lost $200k.

Most people fail to understand the link between yield(Rate) and value, which of course is simply R=I/V and V=I/R.

If one goes up the other goes down in, There are only very brief moments in time where you get high yield and high value(capital growth) or low yield and low value.

A boom and bust market has high value/low yield followed by low value/high yield (relatively) but in the fall this equates to lost equity.

In a stable market with median income multiples of around 3 to 4x then you have a stable value, going up by only the rate of inflation, and a higher yield to compensate.

At these lower median multiple levels, rents are higher as a percentage of value but still a lot cheaper than when the median multiple is 10x.

Interesting Stats

Rent prices are out of control, you'll see all the young ones pack up and leave if they aren't able to afford a 1.2mil townhouse.

The M1 (and M3) measures are particularly interesting, and something I wish this site focused more on. The increase in the supply of money (and credit) seems to be levelling off a bit now as monetary policy tightens, and if these measures turn a corner and start decreasing, then that's deflationary by definition.

The CPI doesn't tell us the whole story, and can be easily misleading.

The chart on NZ M1 money supply is fascinating. It’s gone up from 480000 to 1400000 million since 2017. There’s your smoking gun for house price rises and massive inflation economy wide.

With banks calling this "storm clouds of a recession and rising interest rates" best to wait a while or relocate to Aussie for a bit. https://www.oneroof.co.nz/news/41793

Renting is even worse in Australia, vacancy rates are less than 1% in many cities and rent prices rose 15.6% in capital cities in the last year.

https://nz.news.yahoo.com/no-end-in-sight-for-rental-crisis-014050951.h…

Eh, a mate of mine rents in a safe, decent area of central Melbourne for $420 per week for a large 2 bedroom apartment (~80sqm). That's much better than you'd get anywhere in central Auckland. Yeah, they've gone up a little since his term started but this is much better than what you'd typically get for the same money in Auckland: https://www.realestate.com.au/property-apartment-vic-melbourne-420256062

Palmy North chasing Wellington for the biggest looser. Wouldn't want to be heavily exposed to either market with recent purchases. Time To Panic.

You underestimate the faith in government and central bank policy riding to the rescue. Surely it will continue as it has these last decades...?

& if you've had one too many drinks at the free-all-you-can-drink bar ( 0% LVR's ) , it may be about to come all up

TimeToPuke

.

Our 3yr old house on QV estimate has gone down from 1250000 to 970000. Thats 22.4% drop.

What price was it 3 year’s ago

RV was 750000.

Don’t be surprised if it goes back to 750k over next year. The last 3 years price’s just pumped up by emergency rates now this has been replaced by higher rates and inflation most people just can’t afford million dollar mortgages.

I picked a 30% one from peak (Nov 2021) by December 2022 - not far off now.

While its hard to see that coming to realisation.... I expected much longer and eventually much deeper, given the start of the year we have had... ie about 5-6% drops each quarter..... wow we are close.....

Palm Vegas was way overcooked from 2020-2021.

Demand from a mix of purchasers , FHB and regional investors , including from Welly, stupidly .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.